Laboratory Airborne Particle Counters Market - Global Share, Size & Changing Dynamics 2021-2034

Global Laboratory Airborne Particle Counters Market is segmented by Application (Pharmaceuticals, Clean Rooms, Semiconductor Manufacturing, Healthcare, Research Laboratories), Type (Handheld Counters, Portable Counters, Online Continuous Counters), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

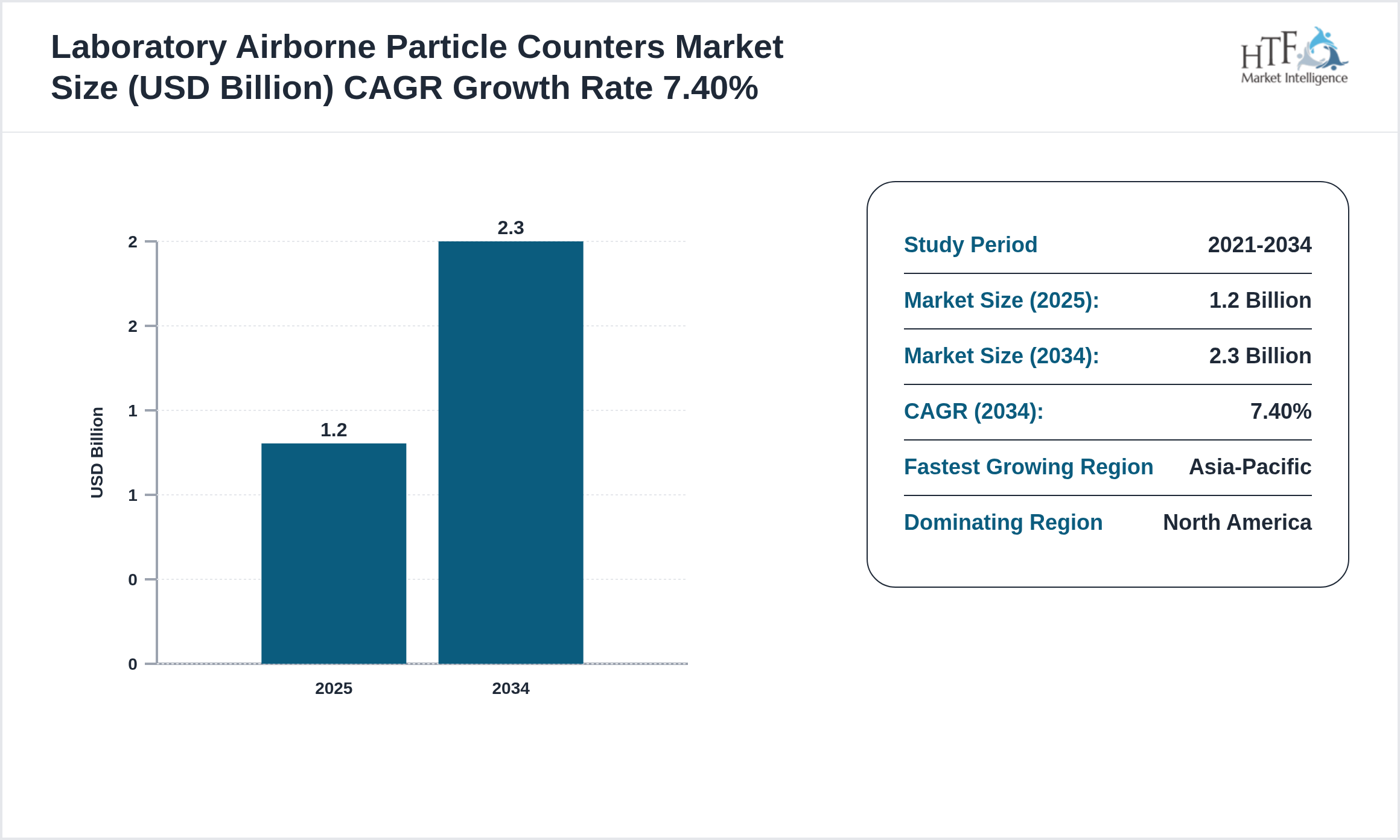

The Laboratory Airborne Particle Counters market is witnessing significant growth and is expected to expand at a CAGR of 7.40% during the forecast period from 2025 to 2034. This growth is primarily driven by increasing technological advancements, rising consumer demand, and expanding applications across various industries. Businesses are increasingly adopting innovative solutions to improve operational efficiency, enhance customer experiences, and gain a competitive advantage, further fueling market expansion.

Source: HTF Market Intelligence (HTF MI)

The Laboratory Airborne Particle Counters market involves devices used for monitoring particulate contamination in cleanrooms laboratories and pharmaceutical environments. The operational ecosystem includes manufacturers distributors research laboratories and regulatory authorities. Technology evolution focuses on real-time monitoring wireless data transmission and integration with environmental control systems. Digital transformation enables centralized monitoring platforms automated alert systems and predictive maintenance analytics. Platform integration allows seamless deployment across multiple sites enhancing scalability and operational efficiency. Commercial deployment models include direct sales lease arrangements and service contracts. Infrastructure monetization is achieved through value-added software calibration services and extended warranty programs. Future revenue growth is driven by stringent regulatory standards increased pharmaceutical and biotech research activities and expansion in semiconductor and precision manufacturing industries

The research study Laboratory Airborne Particle Counters Market gives readers information on tactical business choices and strategic planning that affect and stabilize the growth prediction in the Laboratory Airborne Particle Counters market. However, a few disruptive trends will have opposite and significant effects on the distribution among players and the growth of the Laboratory Airborne Particle Counters market. To give further advice on why certain developments in the Laboratory Airborne Particle Counters market would have a significant impact and specifically why these trends can be taken into account when determining the market's trajectory and industry participants' strategic plans.

Key Highlights

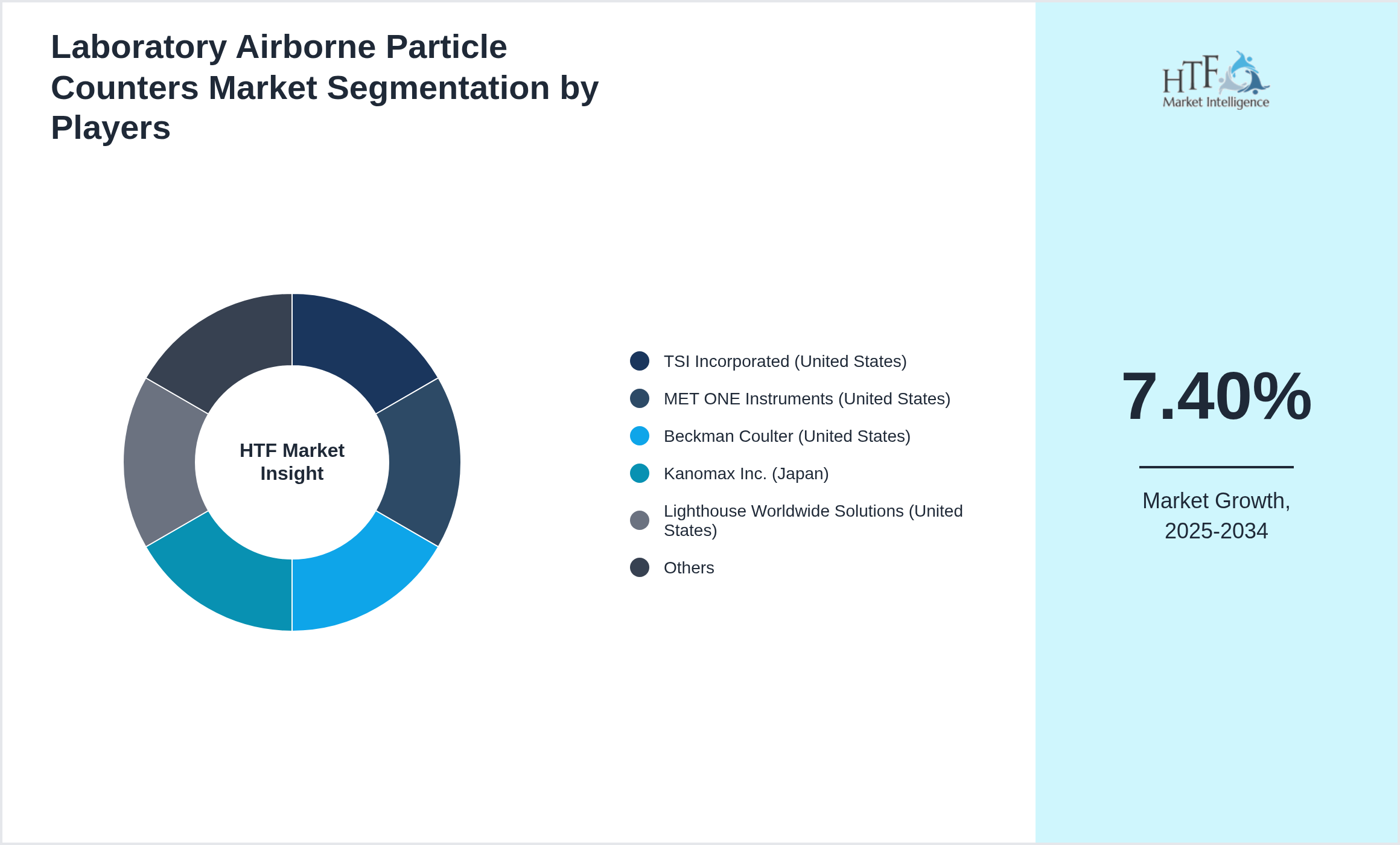

• The Laboratory Airborne Particle Counters is growing at a CAGR of 7.40% during the forecasted period of 2025 to 2034

• Year-on-year growth for the market is 6.80%.

• North America dominated the market share in 2025

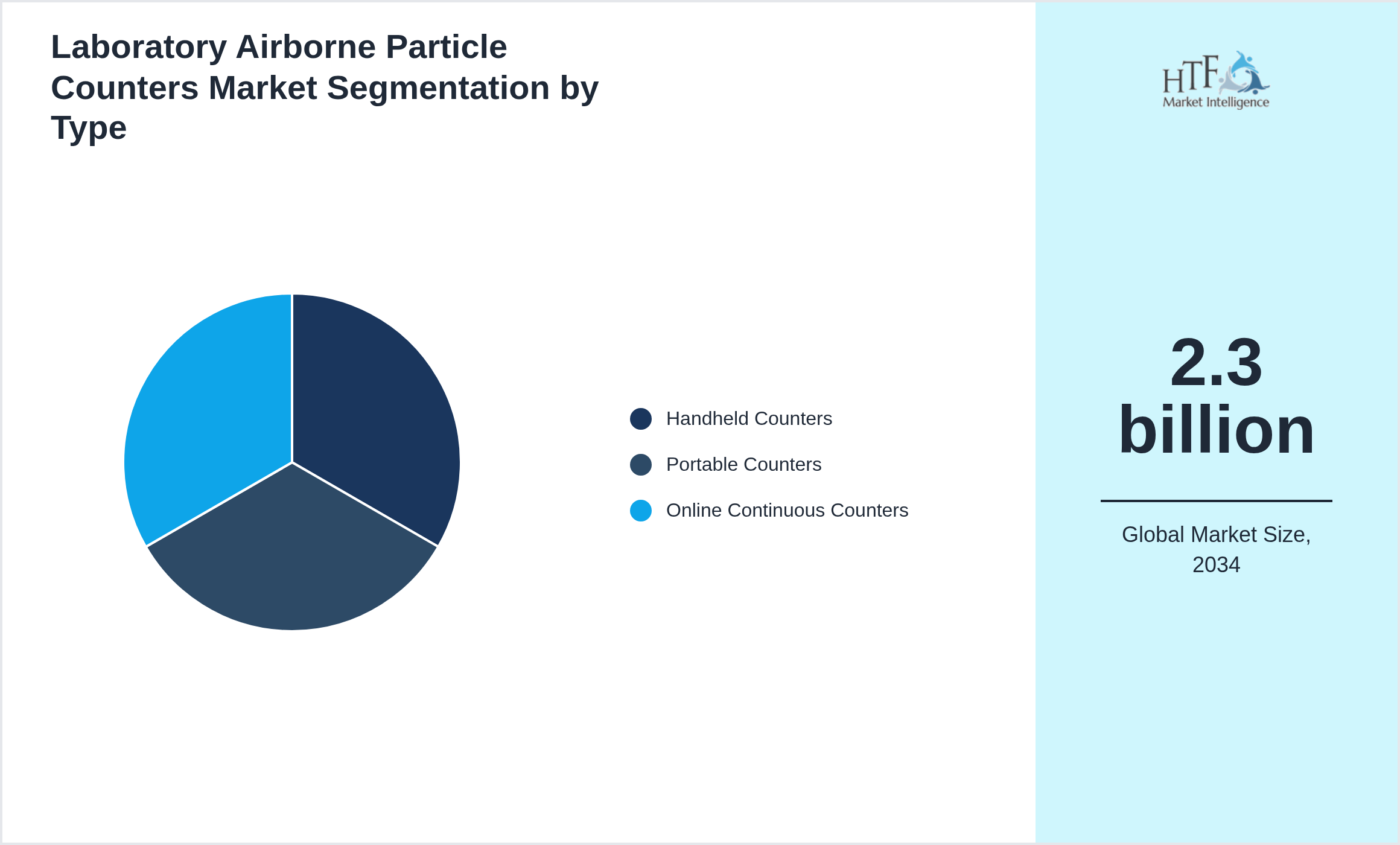

• Based on type, the market is bifurcated into the Handheld Counters, Portable Counters, Online Continuous Counters segment, which dominated the market share during the forecasted period

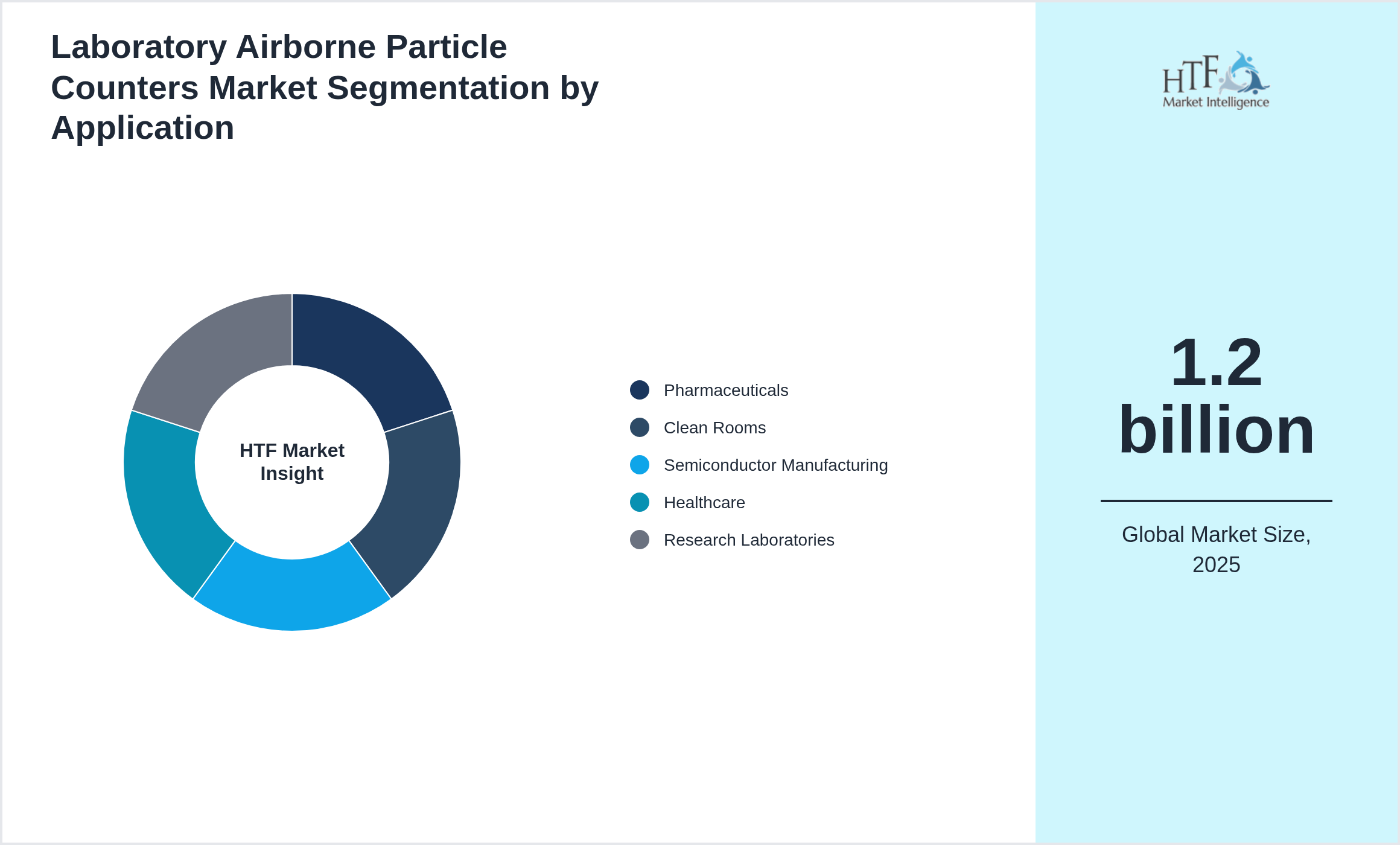

• Based on application, the market is segmented into Application Pharmaceuticals, Clean Rooms, Semiconductor Manufacturing, Healthcare, Research Laboratories as the fastest-growing segment.

• North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA import/export in terms of K tons, K units, and metric tons will be provided if applicable, based on industry best practices.

Market Dynamics Highlighted

Market Driver

The Laboratory Airborne Particle Counters market is experiencing significant growth due to various factors.

- • The Laboratory Airborne Particle Counters market is primarily driven by increasing adoption of strict cleanliness and contamination control standards across pharmaceuticals biotechnology semiconductor and food industries. Rising demand for precise monitoring in cleanrooms laboratories and controlled environments coupled with regulatory mandates such as ISO 14644 and FDA guidelines is fueling growth. The need to ensure product safety reduce contamination risks and maintain compliance with international standards is accelerating the adoption of advanced particle counters. Additionally increasing investment in research laboratories expansion of life sciences infrastructure and growing awareness about airborne contamination in critical environments further strengthen market demand.

Market Trend

The Laboratory Airborne Particle Counters market is growing rapidly due to various factors.

- • Market trends include miniaturization of particle counters integration with IoT and cloud platforms and the adoption of real-time data analytics for continuous monitoring. Automated and portable counters are increasingly preferred to reduce manual intervention while AI-assisted predictive analytics are enhancing contamination control strategies. Integration with environmental monitoring systems and remote monitoring capabilities are gaining traction supporting proactive decision-making in laboratories and industrial cleanrooms.

Opportunity

The Laboratory Airborne Particle Counters has several opportunities, particularly in developing countries where industrialization is growing.

Challenge

The market for fluid power systems faces several obstacles despite its promising growth possibilities.

Laboratory Airborne Particle Counters Market Segment Highlighted

Segmentation by Type

- • Handheld Counters

- • Portable Counters

- • Online Continuous Counters

Segmentation by Application

- • Pharmaceuticals

- • Clean Rooms

- • Semiconductor Manufacturing

- • Healthcare

- • Research Laboratories

Key Players

The companies featured in this profile were selected based on insights from primary experts, evaluating their market penetration, product offerings, and geographical reach. By targeting emerging markets, these companies aim to leverage new opportunities, enhance their competitive advantage, and drive revenue growth. This approach not only aligns with their overall business objectives but also positions them to respond effectively to the evolving demands of consumers in these regions. Several key players in the Laboratory Airborne Particle Counters market are strategically focusing on expanding their operations in developing regions to capture a larger market share, particularly as the year-on-year growth rate for the market stands at 6.80%.

- • TSI Incorporated (United States)

- • MET ONE Instruments (United States)

- • Beckman Coulter (United States)

- • Kanomax Inc. (Japan)

- • Lighthouse Worldwide Solutions (United States)

- • Fluke Corporation (United States)

- • Palas GmbH (Germany)

- • Extech Instruments (United States)

- • Particle Measuring Systems (United States)

- • Horiba Ltd. (Japan)

- • E Instruments International (United States)

- • Topas GmbH (Germany)

- • LaMotte Company (United States)

- • Air Techniques International (United States)

- • Sensidyne Inc. (United States)

Regional Insight

The North America dominant region currently dominates the market share, fueled by increasing consumption, population growth, and sustained economic progress, which collectively enhance market demand. Conversely, the Asia-Pacific is growing rapidly, driven by significant infrastructure investments, industrial expansion, and rising consumer demand.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

- • North America: The United States leads the Laboratory Airborne Particle Counters market due to advanced cleanroom standards in semiconductor pharmaceutical and biotech industries coupled with robust investment in laboratory infrastructure and ISO-classified manufacturing facilities. Enterprise digitalization through IoT-enabled monitoring systems and automated data reporting platforms supports operational scalability. Canada is increasing adoption of precision air monitoring systems in pharmaceutical and research labs supported by regulatory compliance mandates. Strong venture funding for cleanroom technology startups and smart laboratory equipment strengthens competitive positioning

- • Europe: Germany France and the United Kingdom dominate due to strict GMP compliance and growing biotechnology and pharmaceutical production facilities. Germany’s manufacturing and R&D centers adopt AI-enabled particle monitoring and automated reporting systems while the UK expands cleanroom upgrades in academic and industrial labs. France emphasizes integration of digital laboratory infrastructure with IoT sensors to optimize operational efficiency. Regulatory frameworks such as EU GMP reinforce product safety and quality assurance fostering commercial opportunities across laboratories

- • Asia-Pacific: China Japan South Korea and India are rapidly expanding cleanroom and laboratory monitoring infrastructure. China invests in pharmaceutical electronics and biotech facilities with automated particle counting and real-time environmental monitoring. Japan and South Korea lead in advanced sensor integration and IoT-based laboratory data analytics. India shows growth through private research labs and pharmaceutical manufacturing expansions. Digital ecosystem strength and modernization of laboratory infrastructure are improving commercial opportunities and future operational expansion

- • Middle East & Africa: UAE and Saudi Arabia are modernizing laboratory infrastructure in pharmaceutical and industrial sectors integrating advanced airborne particle monitoring for quality assurance. South Africa remains the primary African market with growing demand in pharmaceutical medical device and research labs. Investment in smart laboratory technology is increasing although broader adoption is limited by infrastructure and specialist availability

- • Latin America: Brazil Mexico and Argentina are expanding adoption of laboratory airborne particle counters in pharmaceutical and food industries. Brazil leads with growing cleanroom implementations and private research facilities while Mexico strengthens laboratory digitalization and IoT integration. Regional infrastructure modernization and increasing regulatory compliance drive commercial opportunities although uneven funding limits full-scale expansion

Market Entropy

Merger & Acquisition

- • Jan 2026 – A leading European laboratory instrumentation company acquired a specialized airborne particle monitoring firm to strengthen its cleanroom and contamination control solutions. The acquisition focused on advanced laser particle counting technologies real-time data logging and IoT-enabled environmental monitoring for pharmaceutical semiconductor and biopharmaceutical manufacturing facilities. The integration allows the acquiring company to offer automated cleanroom compliance solutions reducing manual inspection and improving operational efficiency. In Mar 2026 a strategic partnership was formed with a global cleanroom validation service provider to offer turnkey particle monitoring systems. Regional distributors also consolidated smaller local suppliers to ensure faster deployment and support services. Market analysts noted that increasing regulatory requirements for GMP compliance and sterile manufacturing were driving consolidation in the particle counter industry. These mergers are expected to accelerate technology adoption improve data accuracy and expand market reach for advanced laboratory environmental monitoring

Patent Analysis

- • Dominates revenue due to widespread adoption in pharma and biotech; advanced optical and laser particle detection technologies are heavily patented; automation in data acquisition integrated reporting software and low-maintenance designs enhance throughput; modular sensor designs and AI-assisted detection improve accuracy; long sensor lifespan reduces operational costs; patented calibration methods extend lifecycle; supply-chain optimized for just-in-time delivery; premium pricing supported by validation and compliance requirements; critical in regulated labs and quality-control settings contributing disproportionately to market profitability

Investment and Funding Scenario

- • Investment in laboratory airborne particle counters has increased substantially via venture capital and private equity targeting R&D of high-precision sensors automated monitoring systems and calibration infrastructure while partnerships with research labs hospitals and pharmaceutical companies accelerate adoption infrastructure investment emphasizes cleanroom testing facilities AI-driven data analysis and scalable production trends indicate rising demand in life sciences and environmental monitoring recurring service contracts ensure predictable revenue streams co-investments in predictive maintenance and calibration technology enhance scalability operational efficiency and long-term profitability

Report Infographics

| Report Features | Details |

| Base Year | 2025 |

| Based Year Market Size (2025) | 1.2 billion |

| Historical Period | 2021 to 2025 |

| CAGR (2025 to 2034) | 7.40% |

| Forecast Period | 2026 to 2034 |

| Forecasted Period Market Size (2034) | 2.3 billion |

| Scope of the Report |

By Type, By Application, By Region |

| Companies Covered | TSI Incorporated (United States), MET ONE Instruments (United States), Beckman Coulter (United States), Kanomax Inc. (Japan), Lighthouse Worldwide Solutions (United States), Fluke Corporation (United States), Palas GmbH (Germany), Extech Instruments (United States), Particle Measuring Systems (United States), Horiba Ltd. (Japan), E Instruments International (United States), Topas GmbH (Germany), LaMotte Company (United States), Air Techniques International (United States), Sensidyne Inc. (United States) |

| Customization Scope | 15% Free Customization

Want to Buy Specific Sections of This Report?

|

| Delivery Format | PDF and Excel through Email |

The Top-Down and Bottom-Up Approaches

The top-down approach begins with a broad theory or hypothesis and breaks it down into specific components for testing. This structured, deductive process involves developing a theory, creating hypotheses, collecting and analyzing data, and drawing conclusions. It is particularly useful when there is substantial theoretical knowledge, but it can be rigid and may overlook new phenomena.

Conversely, the bottom-up approach starts with specific data or observations, from which broader generalizations and theories are developed. This inductive process involves collecting detailed data, analyzing it for patterns, developing hypotheses, formulating theories, and validating them with additional data. While this approach is flexible and encourages the discovery of new phenomena, it can be time-consuming and less structured.

Regulatory Framework

The healthcare sector is overseen by various regulatory bodies that ensure the safety, quality, and efficacy of health services and products. In the United States, the U.S. Department of Health and Human Services (HHS) plays a crucial role in protecting public health and providing essential human services. Within HHS, the Food and Drug Administration (FDA) regulates food, drugs, and medical devices, ensuring they meet safety and efficacy standards. The Centers for Disease Control and Prevention (CDC) focuses on disease control and prevention, conducting research, and providing health information to protect public health.