Global Touch Screen Cover Glass Market Roadmap to 2032

Global Touch Screen Cover Glass Market is segmented by Application (Smartphones, Tablets, Consumer Electronics, Automotive Displays, Wearable Devices, Industrial Machines, Public Information Displays, Healthcare Equipment), Type (Glass Technology, Touch Panels, Electronic Displays, Glass Covering, Protective Films, Transparent Conductors, Flexible Displays, AMOLED Panels), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

INDUSTRY OVERVIEW

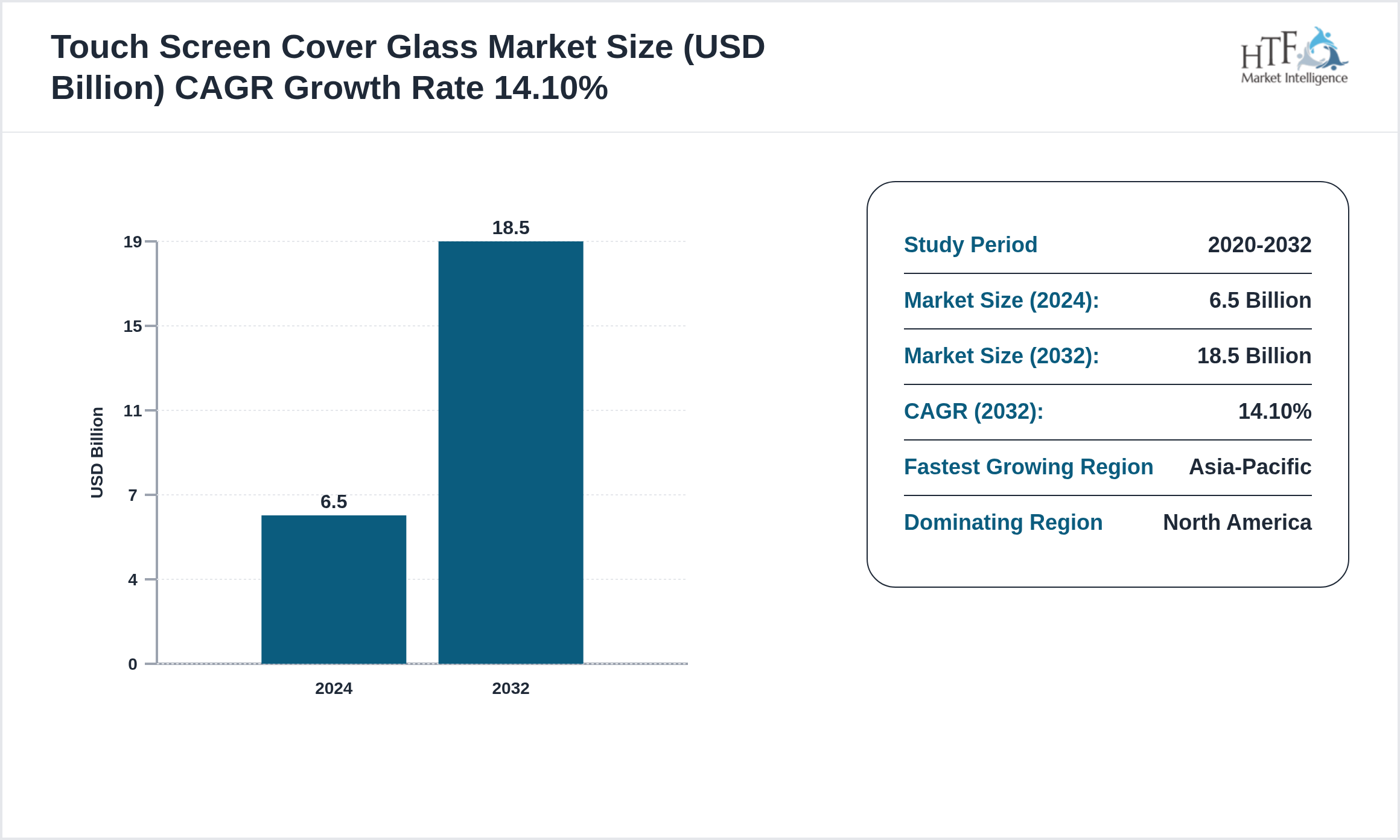

The Touch Screen Cover Glass market is experiencing robust growth, projected to achieve a compound annual growth rate CAGR of 14.10% during the forecast period. Valued at 6.5 Billion, the market is expected to reach 18.5 Billion by 2032, with a year-on-year growth rate of 14.70%. This upward trajectory is driven by factors such as evolving consumer preferences, technological advancements, and increased investment in innovation, positioning the market for significant expansion in the coming years. Companies should strategically focus on enhancing their offerings and exploring new market opportunities to capitalize on this growth potential.

Source: HTF Market Intelligence (HTF MI)

Touch screen cover glass is a crucial component in electronic devices, providing protection to the underlying touch-sensitive screens while maintaining functionality. Made of durable materials like tempered glass or chemically strengthened glass, it is designed to resist scratches, impacts, and breakage. Touch screen cover glass is used in various applications, including smartphones, tablets, and other portable devices. It also serves as the outermost layer in industrial control systems, automotive displays, and public kiosks, offering both protection and tactile feedback for user interaction.

Geographic Analysis of Touch Screen Cover Glass

The Touch Screen Cover Glass market exhibits significant regional variation, shaped by different economic conditions and consumer behaviors.

Currently, North America dominates the market due to high consumption, population growth, and sustained economic progress. Meanwhile, Asia-Pacific is experiencing the fastest growth, driven by large-scale infrastructure investments, industrial development, and rising consumer demand.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

Regulatory Landscape

- • Safety standards (UL

Key Highlights

• The Touch Screen Cover Glass is growing at a CAGR of 14.10% during the forecasted period of 2020 to 2032

• Year-on-year growth for the market is 14.70%.

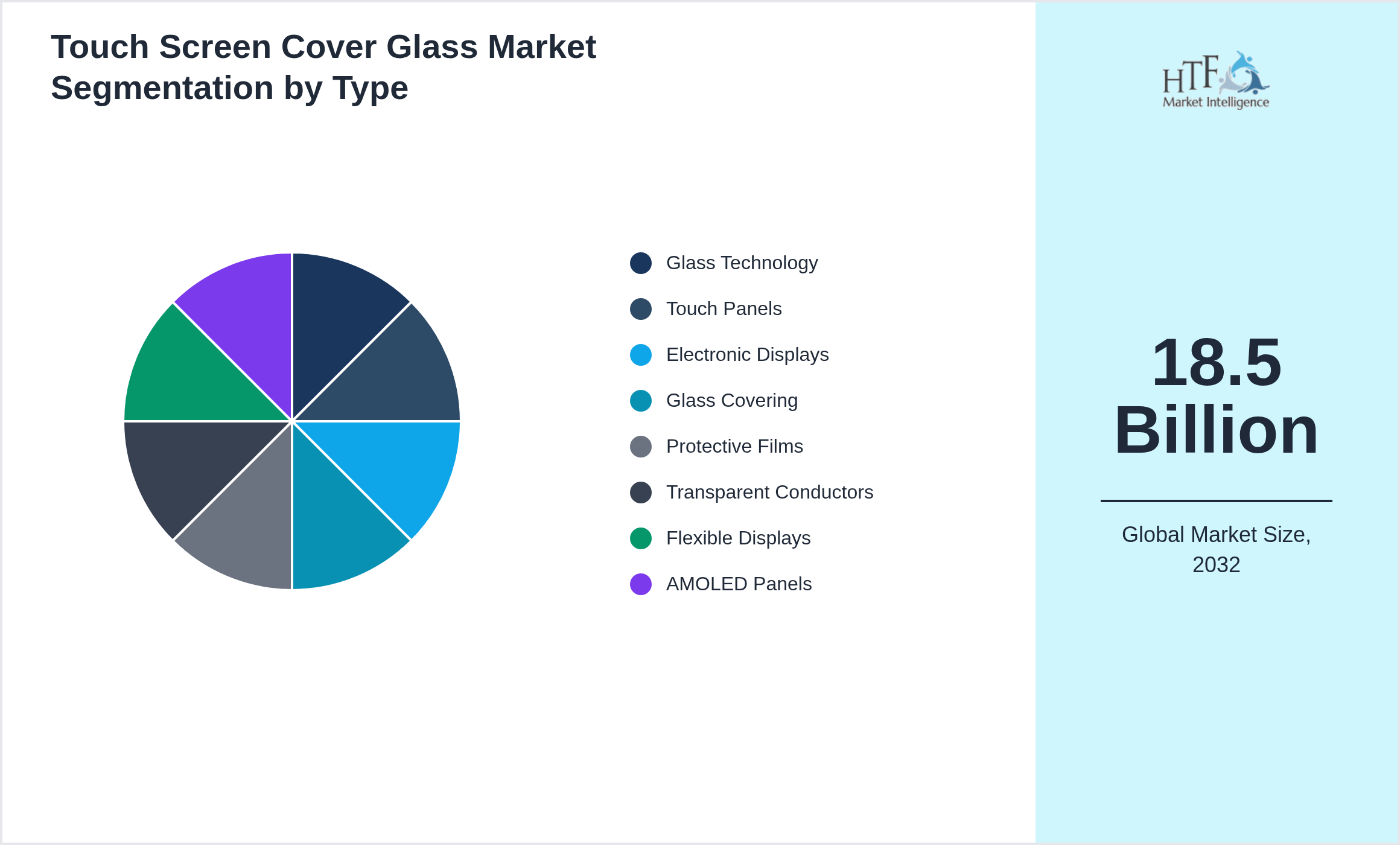

• Based on type, the market is bifurcated into Glass Technology, Touch Panels, Electronic Displays, Glass Covering, Protective Films, Transparent Conductors, Flexible Displays, AMOLED Panels

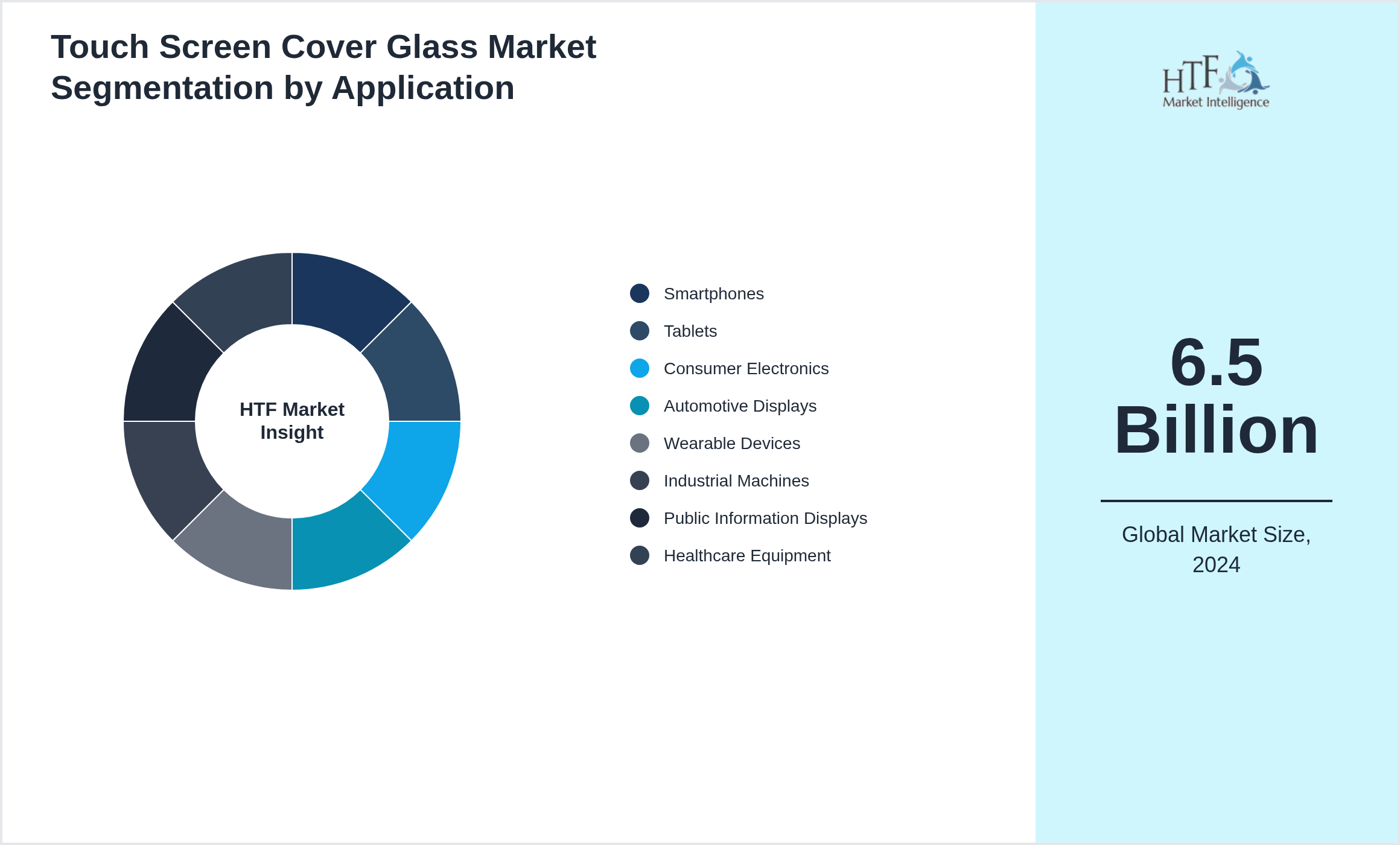

• Based on application, the market is segmented into Smartphones, Tablets, Consumer Electronics, Automotive Displays, Wearable Devices, Industrial Machines, Public Information Displays, Healthcare Equipment

• Global import/export in terms of K tons, K units, and metric tons will be provided if applicable, based on industry best practices.

Market Segmentation Analysis

Segmentation by Type

- • Glass Technology

- • Touch Panels

- • Electronic Displays

- • Glass Covering

- • Protective Films

- • Transparent Conductors

- • Flexible Displays

- • AMOLED Panels

Segmentation by Application

- • Smartphones

- • Tablets

- • Consumer Electronics

- • Automotive Displays

- • Wearable Devices

- • Industrial Machines

- • Public Information Displays

- • Healthcare Equipment

Key Players

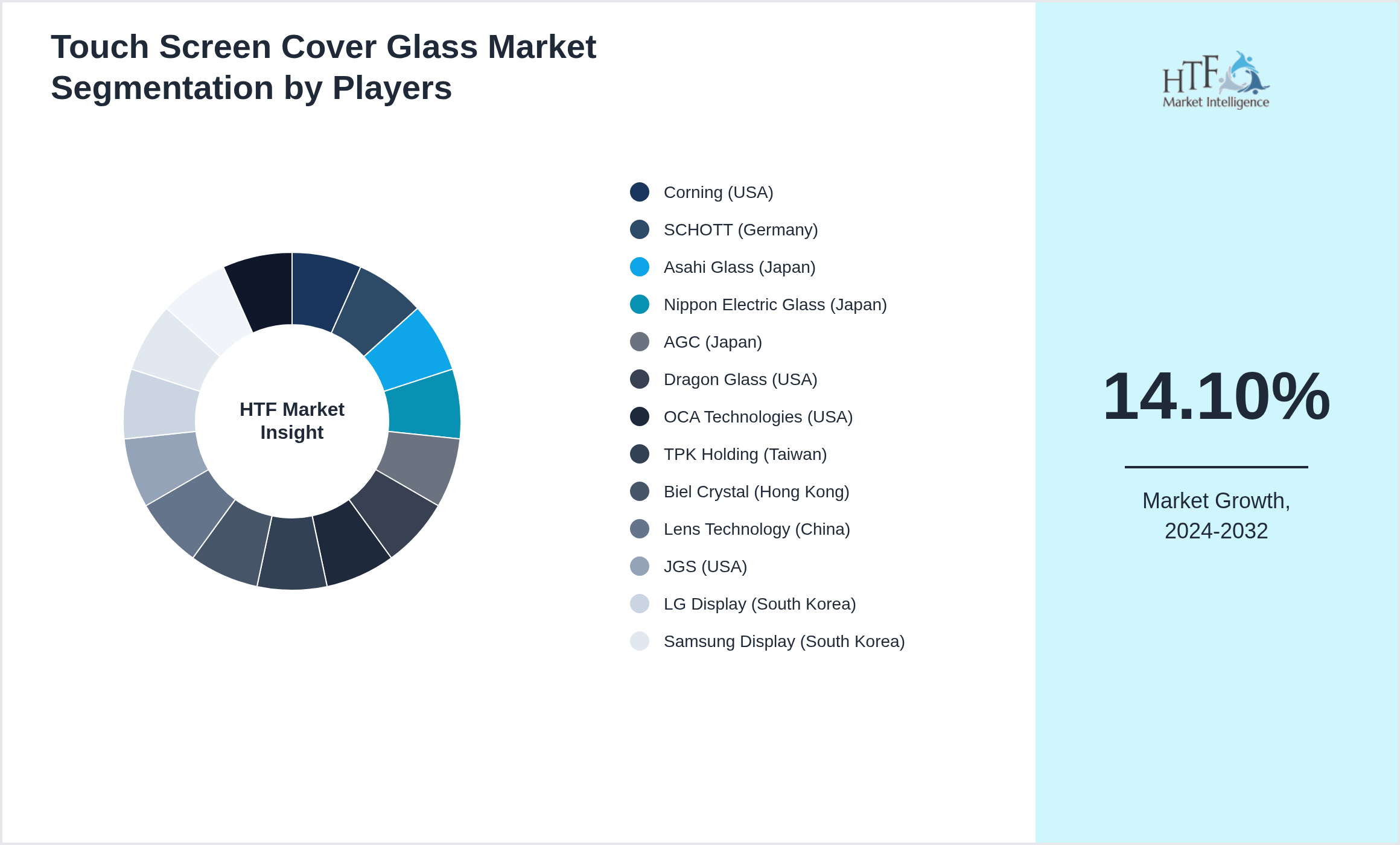

Several key players in the Touch Screen Cover Glass market are strategically focusing on expanding their operations in developing regions to capture a larger market share, particularly as the year-on-year growth rate for the market stands at 14.70%. The companies featured in this profile were selected based on insights from primary experts, evaluating their market penetration, product offerings, and geographical reach. By targeting emerging markets, these companies aim to leverage new opportunities, enhance their competitive advantage, and drive revenue growth. This approach not only aligns with their overall business objectives but also positions them to respond effectively to the evolving demands of consumers in these regions.

- • Corning (USA)

- • SCHOTT (Germany)

- • Asahi Glass (Japan)

- • Nippon Electric Glass (Japan)

- • AGC (Japan)

- • Dragon Glass (USA)

- • OCA Technologies (USA)

- • TPK Holding (Taiwan)

- • Biel Crystal (Hong Kong)

- • Lens Technology (China)

- • JGS (USA)

- • LG Display (South Korea)

- • Samsung Display (South Korea)

- • CSG (China)

- • G-Tech Optoelectronics (Taiwan)

Research Methodology

The comprehensive market research is provided that combines both secondary and primary methodologies. The secondary research involves rigorous analysis of existing data sources, such as industry reports, market databases, and competitive landscapes, to provide a robust foundation of market knowledge. This is complemented by our primary research services to gather firsthand data through surveys, interviews, and focus groups tailored specifically to your business needs. By integrating these approaches, we offer a thorough understanding of market trends, consumer behavior, and competitive dynamics, enabling us to make well-informed strategic decisions.

Market Dynamics

Market dynamics refer to the forces that influence the supply and demand of products and services within a market. These forces include factors such as consumer preferences, technological advancements, regulatory changes, economic conditions, and competitive actions. Understanding market dynamics is crucial for businesses as it helps them anticipate changes, identify opportunities, and mitigate risks.

By analyzing market dynamics, companies can better understand market trends, predict potential shifts, and develop strategic responses. This analysis enables businesses to align their product offerings, pricing strategies, and marketing efforts with evolving market conditions, ultimately leading to more informed decision-making and a stronger competitive position in the marketplace.

Market Driver

- • Growing demand for smartphones

- • tablets

- • and laptops

- • Advancements in touch screen technology

- • Increased adoption of AR/VR devices

- • Rising use of touchscreens in automotive and industrial applications

- • Technological advancements in glass durability

- • Growth in wearable tech with touchscreen displays

- • Focus on improving touchscreen response time

- • Development of more energy-efficient touchscreens

- • Increase in demand for foldable and flexible touchscreens

- • Development of ultra-thin and durable touch screens

- • Growth of touchscreen technology in automotive interiors

- • Rise of touchscreens in IoT and smart appliances

- • Advancements in scratch-resistant and anti-glare coatings

- • Increased use of touchscreens in medical devices

- • Focus on energy-efficient touchscreen displays

- • Demand for multi-touch screens in consumer products

- • Opportunities in automotive and industrial touchscreen applications

- • Expansion in wearable tech and IoT

- • Growing demand for gaming consoles and AR/VR displays

- • Market growth for foldable and flexible touchscreens

- • Opportunities in medical and health-tech touchscreen devices

- • Rise of touchscreens in smart home devices

- • Growth in the demand for premium smartphones

- • Development of eco-friendly touch screens

Challenge

- • Intense competition in display technology

- • High manufacturing and raw material costs

- • Short product life cycles

- • Market saturation in consumer electronics

- • Environmental impact of glass disposal

- • Technological barriers in flexible and foldable displays

- • Supply chain disruptions for critical materials

- • Regulatory challenges in different regions

Regional Analysis

- • North America and Asia-Pacific lead in consumer electronics manufacturing

- • Europe growing with industrial applications

- • regulations on material safety and environmental impact influence production

- • emerging markets increasing smartphone and tablet adoption

- • infrastructure for glass processing expanding

- • manufacturers innovate for durability and clarity

- • local suppliers increasing

- • demand driven by consumer electronics and automotive sectors.

Market Entropy

- • In February 2025

Merger & Acquisition

- • In Jan 2024

Regulatory Landscape

- • Safety standards (UL

Patent Analysis

- • Patents focus on glass composition

Investment and Funding Scenario

- • Investments from consumer electronics manufacturers

Regional Outlook

The North America region holds the largest market share in 2024 and is expected to grow at a good CAGR. The Asia-Pacific Region is the fastest-growing region due to increasing development and disposable income.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

|

Report Features |

Details |

|

Base Year |

2024 |

|

Based Year Market Size (2024) |

6.5 Billion |

|

Historical Period Market Size (2020) |

USD Million ZZ |

|

CAGR (2024 to 2032) |

14.10% |

|

Forecast Period |

2026 to 2032 |

|

Forecasted Period Market Size (2032) |

18.5 Billion |

|

Scope of the Report |

By Type, By Application, By Region |

|

Quantitative Units |

Revenue in USD million/billion, volume in kilotons, and CAGR from 2024 to 2032 |

|

Year-on-Year Growth |

14.70% |

|

Companies Covered |

Corning (USA), SCHOTT (Germany), Asahi Glass (Japan), Nippon Electric Glass (Japan), AGC (Japan), Dragon Glass (USA), OCA Technologies (USA), TPK Holding (Taiwan), Biel Crystal (Hong Kong), Lens Technology (China), JGS (USA), LG Display (South Korea), Samsung Display (South Korea), CSG (China), G-Tech Optoelectronics (Taiwan) |

|

Customization Scope |

15% Free Customization (For EG) |

|

Delivery Format |

PDF and Excel through Email

|

Regulatory Framework

The Information and Communications Technology (ICT) industry is primarily regulated by the Federal Communications Commission (FCC) in the United States, along with other national and international regulatory bodies. The FCC oversees the allocation of spectrum, ensures compliance with telecommunications laws, and fosters fair competition within the sector. It also establishes guidelines for data privacy, cybersecurity, and service accessibility, which are crucial for maintaining industry standards and protecting consumer interests.

Globally, various regulatory agencies, such as the European Telecommunications Standards Institute (ETSI) and the International Telecommunication Union (ITU), play significant roles in standardizing practices and facilitating international cooperation. These bodies work together to create a cohesive regulatory framework that addresses emerging technologies, cross-border data flow, and infrastructure development. Their regulations aim to ensure the ICT industry's growth is both innovative and compliant with global standards, promoting a secure and competitive market environment.