Global Cybersecurity in Aerospace Systems Market - Global Outlook 2020-2033

Global Cybersecurity in Aerospace Systems Market is segmented by Application (Aviation, defense, satellite systems), Type (Network security, secure communications, threat detection), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

INDUSTRY OVERVIEW

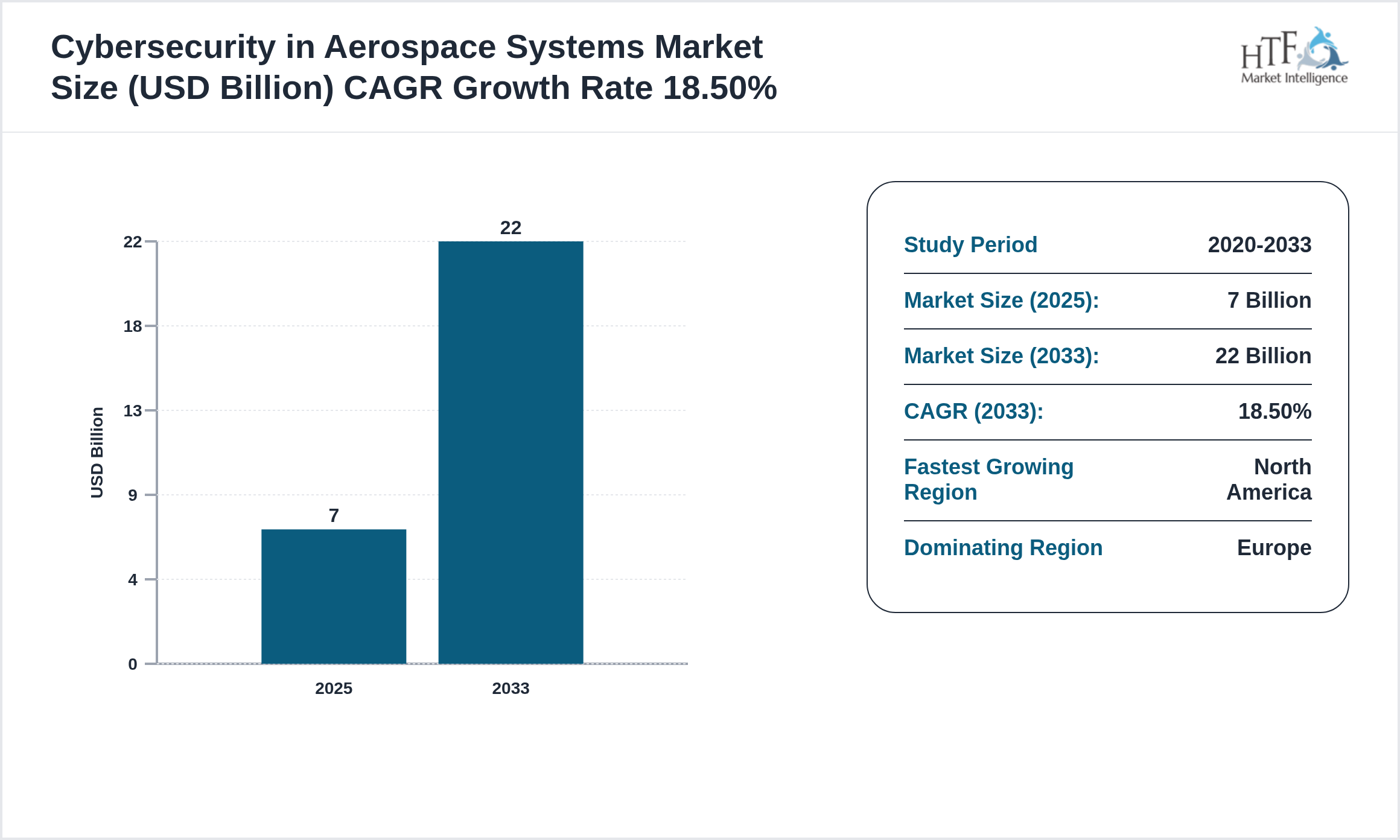

The Cybersecurity in Aerospace Systems market is experiencing robust growth, projected to achieve a compound annual growth rate CAGR of 18.50% during the forecast period. Valued at 7 Billion, the market is expected to reach 22 Billion by 2033, with a year-on-year growth rate of 17.60%. This upward trajectory is driven by factors such as evolving consumer preferences, technological advancements, and increased investment in innovation, positioning the market for significant expansion in the coming years. Companies should strategically focus on enhancing their offerings and exploring new market opportunities to capitalize on this growth potential.

Source: HTF Market Intelligence (HTF MI)

Cybersecurity in aerospace protects aircraft systems, ground control, and supply chains from cyber threats including hacking, data breaches, and system sabotage, ensuring safety, operational integrity, and regulatory compliance in increasingly connected aerospace environments.

Geographic Analysis of Cybersecurity in Aerospace Systems

The Cybersecurity in Aerospace Systems market exhibits significant regional variation, shaped by different economic conditions and consumer behaviors.

Currently, Europe dominates the market due to high consumption, population growth, and sustained economic progress. Meanwhile, North America is experiencing the fastest growth, driven by large-scale infrastructure investments, industrial development, and rising consumer demand.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

Regulatory Landscape

- • In 2024

If you need any customization, you can connect with us

Key Highlights

• The Cybersecurity in Aerospace Systems is growing at a CAGR of 18.50% during the forecasted period of 2020 to 2033

• Year-on-year growth for the market is 17.60%.

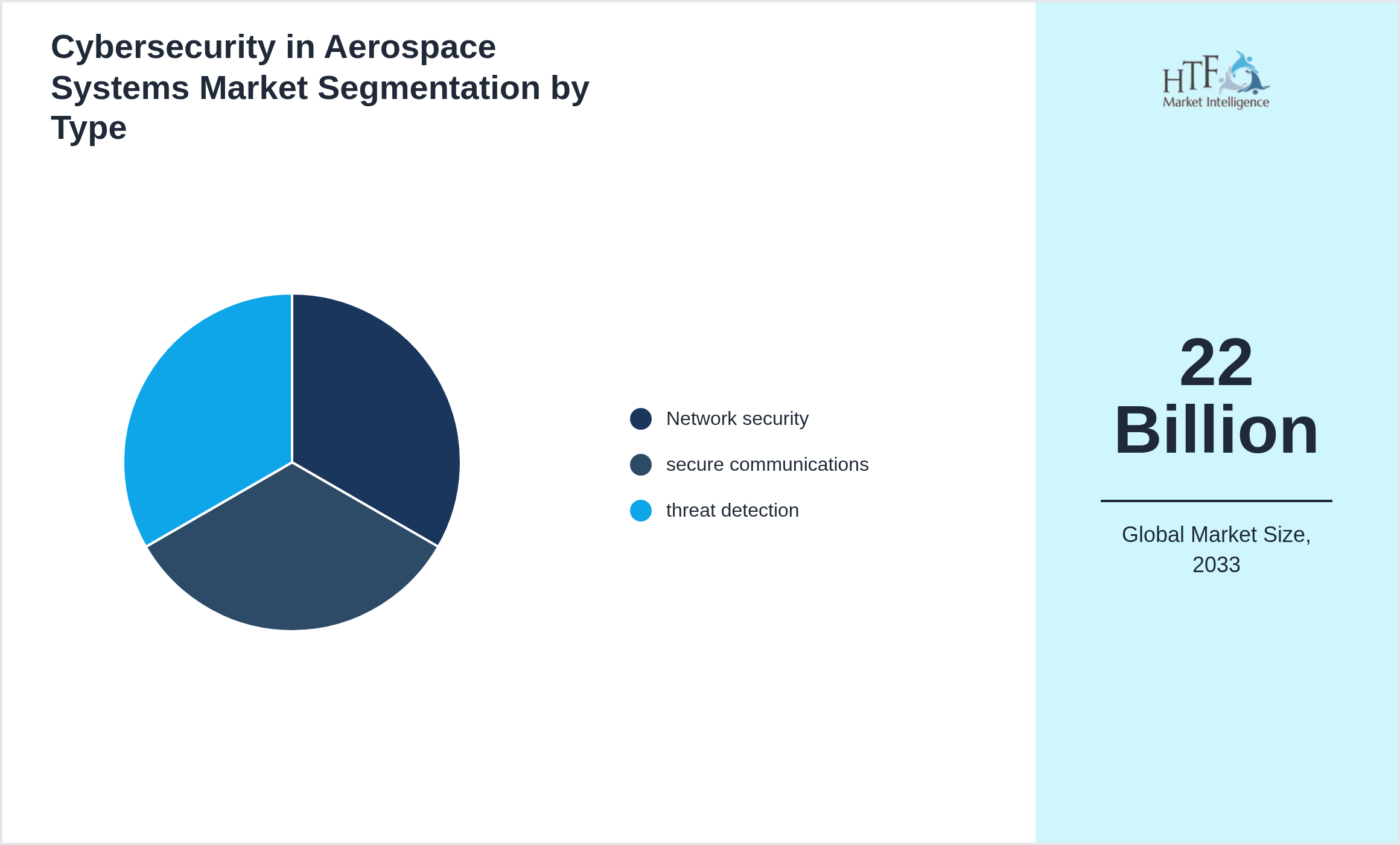

• Based on type, the market is bifurcated into Network security, secure communications, threat detection

• Based on application, the market is segmented into Aviation, defense, satellite systems

• Global import/export in terms of K tons, K units, and metric tons will be provided if applicable based on industry best practices.

Market Segmentation Analysis

Segmentation by Type

- • Network security

- • secure communications

- • threat detection

Segmentation by Application

- • Aviation

- • defense

- • satellite systems

![Cybersecurity in Aerospace Systems Market trend by end use applications [Aviation, defense, satellite systems]](https://htf-insight.s3.us-east-1.amazonaws.com/generated-charts/chart-pie-and-donut-chart-application-4364027-na-1760545198699-1760545203478-ef696587a1a2a6a0.png)

Key Players

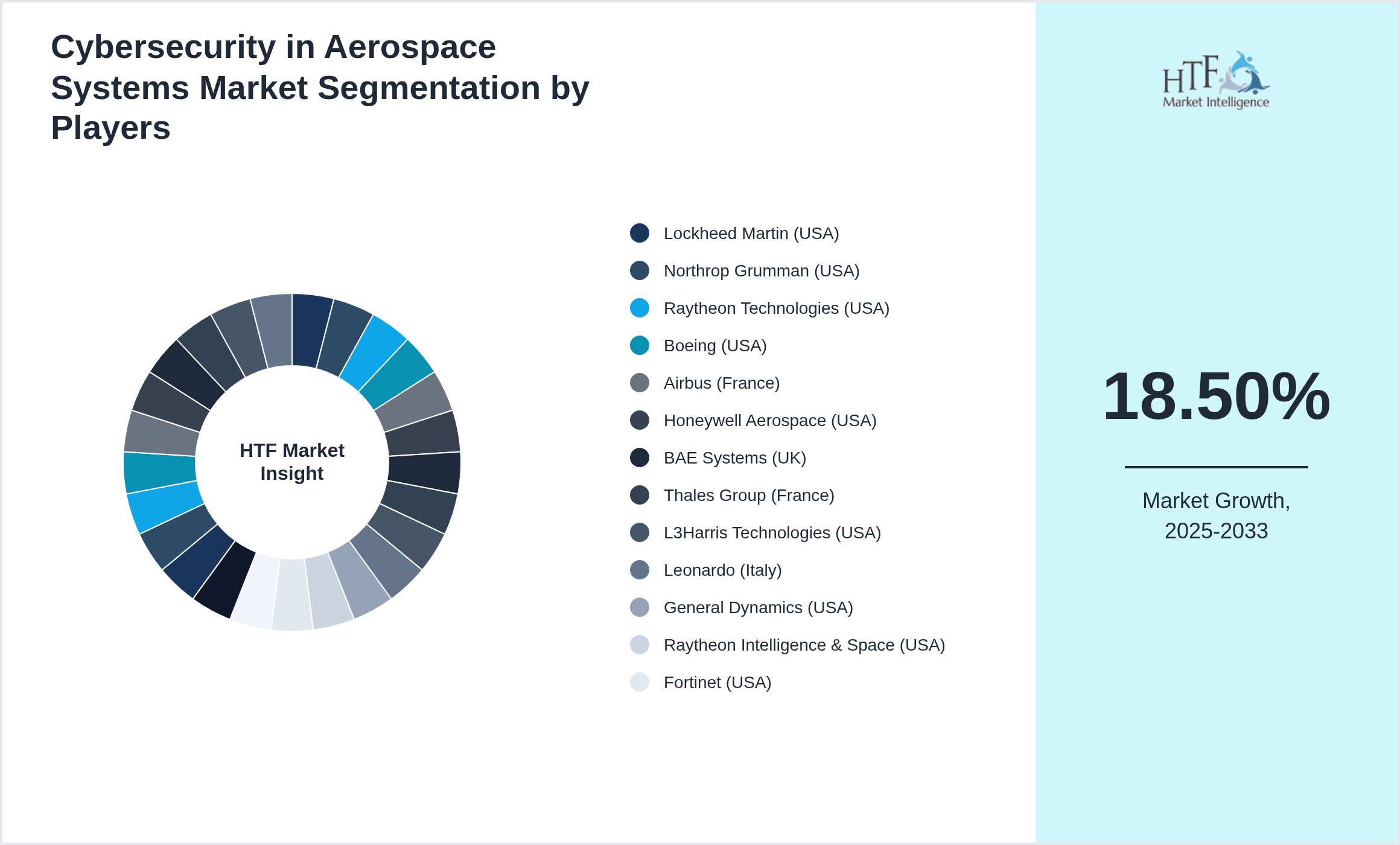

Several key players in the Cybersecurity in Aerospace Systems market are strategically focusing on expanding their operations in developing regions to capture a larger market share, particularly as the year-on-year growth rate for the market stands at 17.60%. The companies featured in this profile were selected based on insights from primary experts, evaluating their market penetration, product offerings, and geographical reach. By targeting emerging markets, these companies aim to leverage new opportunities, enhance their competitive advantage, and drive revenue growth. This approach not only aligns with their overall business objectives but also positions them to respond effectively to the evolving demands of consumers in these regions.

- • Lockheed Martin (USA)

- • Northrop Grumman (USA)

- • Raytheon Technologies (USA)

- • Boeing (USA)

- • Airbus (France)

- • Honeywell Aerospace (USA)

- • BAE Systems (UK)

- • Thales Group (France)

- • L3Harris Technologies (USA)

- • Leonardo (Italy)

- • General Dynamics (USA)

- • Raytheon Intelligence & Space (USA)

- • Fortinet (USA)

- • Palo Alto Networks (USA)

- • IBM Security (USA)

- • Cisco Systems (USA)

- • Check Point Software (Israel)

- • FireEye (USA)

- • Trend Micro (Japan)

- • McAfee (USA)

- • Rapid7 (USA)

- • CrowdStrike (USA)

- • Darktrace (UK)

- • Cybereason (USA)

- • CyberArk (USA)

Research Methodology

The comprehensive market research is provided that combines both secondary and primary methodologies. The secondary research involves rigorous analysis of existing data sources, such as industry reports, market databases, and competitive landscapes, to provide a robust foundation of market knowledge. This is complemented by our primary research services to gather firsthand data through surveys, interviews, and focus groups tailored specifically to your business needs. By integrating these approaches, we offer a thorough understanding of market trends, consumer behavior, and competitive dynamics, enabling us to make well-informed strategic decisions.

Market Dynamics

Market dynamics refer to the forces that influence the supply and demand of products and services within a market. These forces include factors such as consumer preferences, technological advancements, regulatory changes, economic conditions, and competitive actions. Understanding market dynamics is crucial for businesses as it helps them anticipate changes, identify opportunities, and mitigate risks.

By analyzing market dynamics, companies can better understand market trends, predict potential shifts, and develop strategic responses. This analysis enables businesses to align their product offerings, pricing strategies, and marketing efforts with evolving market conditions, ultimately leading to more informed decision-making and a stronger competitive position in the marketplace.

Market Driver

- • Increasing digitalization and connectivity create larger attack surfaces

- • regulatory requirements mandate strict cybersecurity compliance

- • growing state-sponsored cyber threats target aerospace

- • dependence on cloud and IoT increases vulnerabilities

- • adoption of AI for threat detection expands

- • need to protect sensitive IP and data drives investment

- • rise in ransomware and supply chain attacks

- • increased integration of OT and IT systems complicates defense.

- • Use of AI and machine learning in real-time threat detection

- • adoption of zero-trust architectures

- • integration of cybersecurity in early design phases (Security by Design)

- • increased collaboration across industry and government on threat intelligence

- • development of aerospace-specific cybersecurity standards

- • rise of cybersecurity training programs

- • growth of managed security service providers (MSSPs) in aerospace

- • use of blockchain for supply chain security.

- • Opportunities to lead in aerospace cybersecurity products and services

- • development of advanced threat intelligence platforms

- • growth in aerospace-focused cybersecurity consulting

- • potential to secure critical infrastructure and government contracts

- • partnerships with IT security firms

- • increased funding from governments for R&D

- • fostering cybersecurity innovation hubs

- • addressing emerging threats in supply chain and satellite systems.

Challenge

- • Complexity of legacy systems and their vulnerabilities

- • shortage of skilled cybersecurity professionals

- • balancing security with system usability and performance

- • evolving and sophisticated threat landscape

- • high cost of cybersecurity implementation

- • regulatory fragmentation across countries

- • insider threats and supply chain risks

- • challenges in securing increasingly autonomous and AI-driven systems.

Regional Analysis

- • North America leads due to heavy defense and commercial aerospace investment. Europe focuses on satellite communication and avionics cyber resilience. Asia-Pacific

Market Entropy

- • In July 2025

Merger & Acquisition

- • In July 2025

Regulatory Landscape

- • In 2024

Patent Analysis

- • Patent filings are dominated by avionics and secure satellite communication. Boeing and Lockheed lead US filings in intrusion detection systems. India and Israel have emerging aerospace cybersecurity IPs. Patent focus includes threat detection

Investment and Funding Scenario

- • Venture capital interest in aerospace cybersecurity rose by 70% in the past three years. Israel’s aerospace startups secured $400M in cumulative funding. US DoD has increased budget allocations for cyber avionics. Major aerospace primes are acquiring cyber-defense firms. EU’s Horizon Europe funds now include cyber-resilience R&D. Partnerships with cybersecurity startups are accelerating. Indian firms like BEL are investing in aerospace cyber labs. Satellite operators are also major investors in space cyber safety.

Regional Outlook

The Europe Region holds the largest market share in 2025 and is expected to grow at a good CAGR. The North America Region is the fastest-growing region due to increasing development and disposable income.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

|

Report Features |

Details |

|

Base Year |

2025 |

|

Based Year Market Size (2025) |

7 Billion |

|

Historical Period Market Size (2020) |

USD Million ZZ |

|

CAGR (2025 to 2033) |

18.50% |

|

Forecast Period |

2026 to 2033 |

|

Forecasted Period Market Size (2033) |

22 Billion |

|

Scope of the Report |

By Type: Network security, secure communications, threat detection, By Application:Aviation, defense, satellite systems |

|

Regions Covered |

North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

|

Year-on-Year Growth |

17.60% |

|

Companies Covered |

Lockheed Martin (USA), Northrop Grumman (USA), Raytheon Technologies (USA), Boeing (USA), Airbus (France), Honeywell Aerospace (USA), BAE Systems (UK), Thales Group (France), L3Harris Technologies (USA), Leonardo (Italy), General Dynamics (USA), Raytheon Intelligence & Space (USA), Fortinet (USA), Palo Alto Networks (USA), IBM Security (USA), Cisco Systems (USA), Check Point Software (Israel), FireEye (USA), Trend Micro (Japan), McAfee (USA), Rapid7 (USA), CrowdStrike (USA), Darktrace (UK), Cybereason (USA), CyberArk (USA) |

|

Customization Scope |

15% Free Customization (For EG) |

|

Delivery Format |

PDF and Excel through Email |

Regulatory Framework

The Information and Communications Technology (ICT) industry is primarily regulated by the Federal Communications Commission (FCC) in the United States, along with other national and international regulatory bodies. The FCC oversees the allocation of spectrum, ensures compliance with telecommunications laws, and fosters fair competition within the sector. It also establishes guidelines for data privacy, cybersecurity, and service accessibility, which are crucial for maintaining industry standards and protecting consumer interests.

Globally, various regulatory agencies, such as the European Telecommunications Standards Institute (ETSI) and the International Telecommunication Union (ITU), play significant roles in standardizing practices and facilitating international cooperation. These bodies work together to create a cohesive regulatory framework that addresses emerging technologies, cross-border data flow, and infrastructure development. Their regulations aim to ensure the ICT industry's growth is both innovative and compliant with global standards, promoting a secure and competitive market environment.