Clothing Manufacturing Sector Market - Global Size & Outlook 2021-2034

Global Clothing Manufacturing Sector Market is segmented by Application (Retail, E-commerce, Export, Uniforms, Fashion, Costumes, Private Label, Custom Orders), Type (Casual, Formal, Sportswear, Outerwear, Kidswear, Workwear, Lingerie, Accessories), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

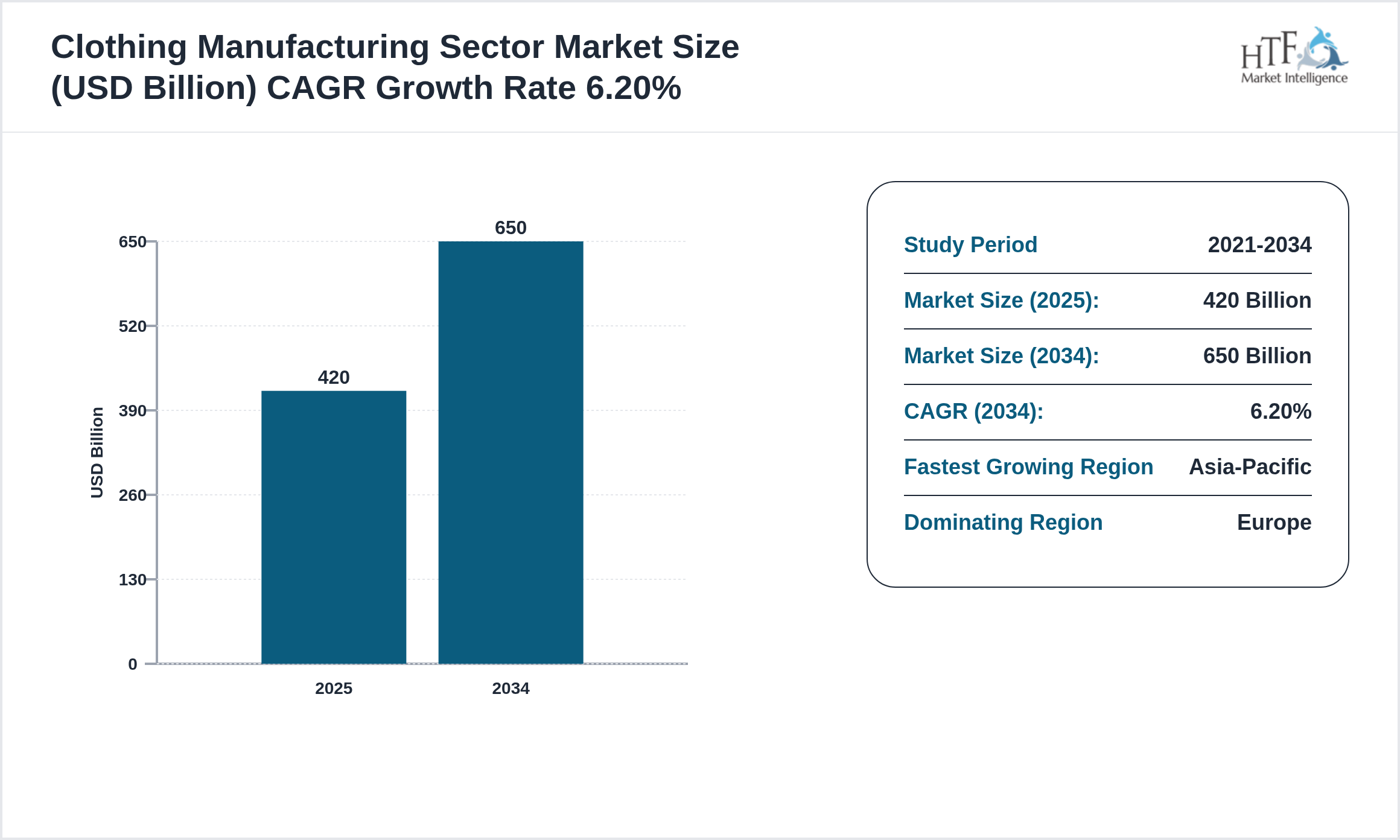

The Clothing Manufacturing Sector market is witnessing significant growth and is expected to expand at a CAGR of 6.20% during the forecast period from 2025 to 2034. This growth is primarily driven by increasing technological advancements, rising consumer demand, and expanding applications across various industries. Businesses are increasingly adopting innovative solutions to improve operational efficiency, enhance customer experiences, and gain a competitive advantage, further fueling market expansion.

Source: HTF Market Intelligence (HTF MI)

The Clothing Manufacturing Sector represents the industrial production, processing, assembly, and commercialization of apparel and textile-based garments for global consumer, institutional, and industrial markets. The market scope includes casual wear, formal wear, sportswear, workwear, knitwear, fashion garments, and textile finishing operations across mass-market and luxury segments. The report analyzes textile sourcing, garment production, labor-intensive manufacturing operations, export-import structures, and retail supply chains while excluding raw fiber farming and non-apparel textile production. Rising global fashion demand, fast-fashion expansion, and increasing e-commerce penetration are major growth catalysts. Demand-side dynamics are shaped by changing lifestyle preferences, seasonal fashion trends, and rising disposable income. Supply-side transformation includes nearshore manufacturing, sustainable textile processing, and automated garment assembly systems. Technological evolution includes AI-driven fashion forecasting, robotic sewing systems, digital textile printing, smart fabric innovation, and supply-chain digitization

The research study Clothing Manufacturing Sector Market gives readers information on tactical business choices and strategic planning that affect and stabilize the growth prediction in the Clothing Manufacturing Sector market. However, a few disruptive trends will have opposite and significant effects on the distribution among players and the growth of the Clothing Manufacturing Sector market. To give further advice on why certain developments in the Clothing Manufacturing Sector market would have a significant impact and specifically why these trends can be taken into account when determining the market's trajectory and industry participants' strategic plans.

Key Highlights

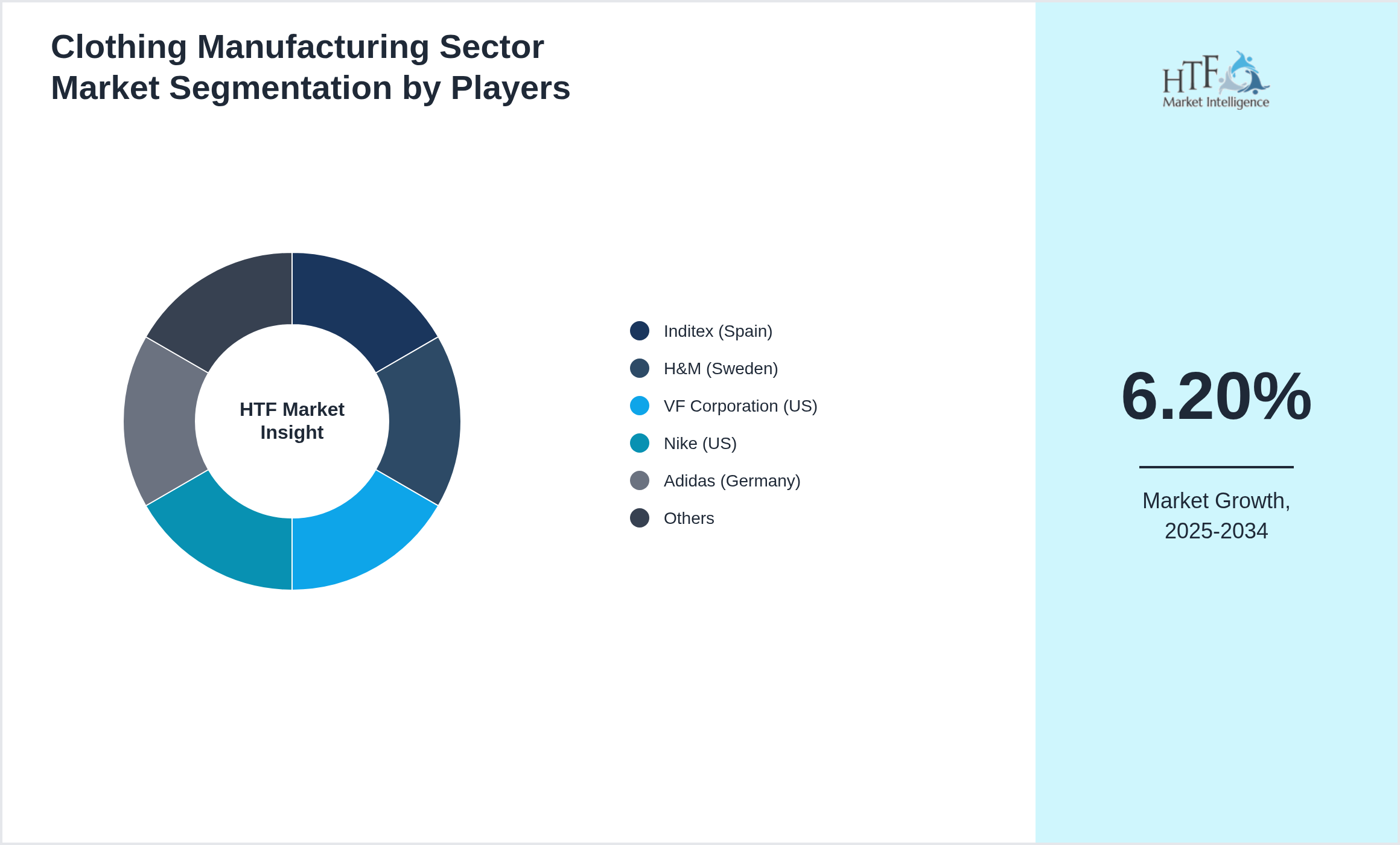

• The Clothing Manufacturing Sector is growing at a CAGR of 6.20% during the forecasted period of 2025 to 2034

• Year-on-year growth for the market is 5.70%.

• Europe dominated the market share in 2025

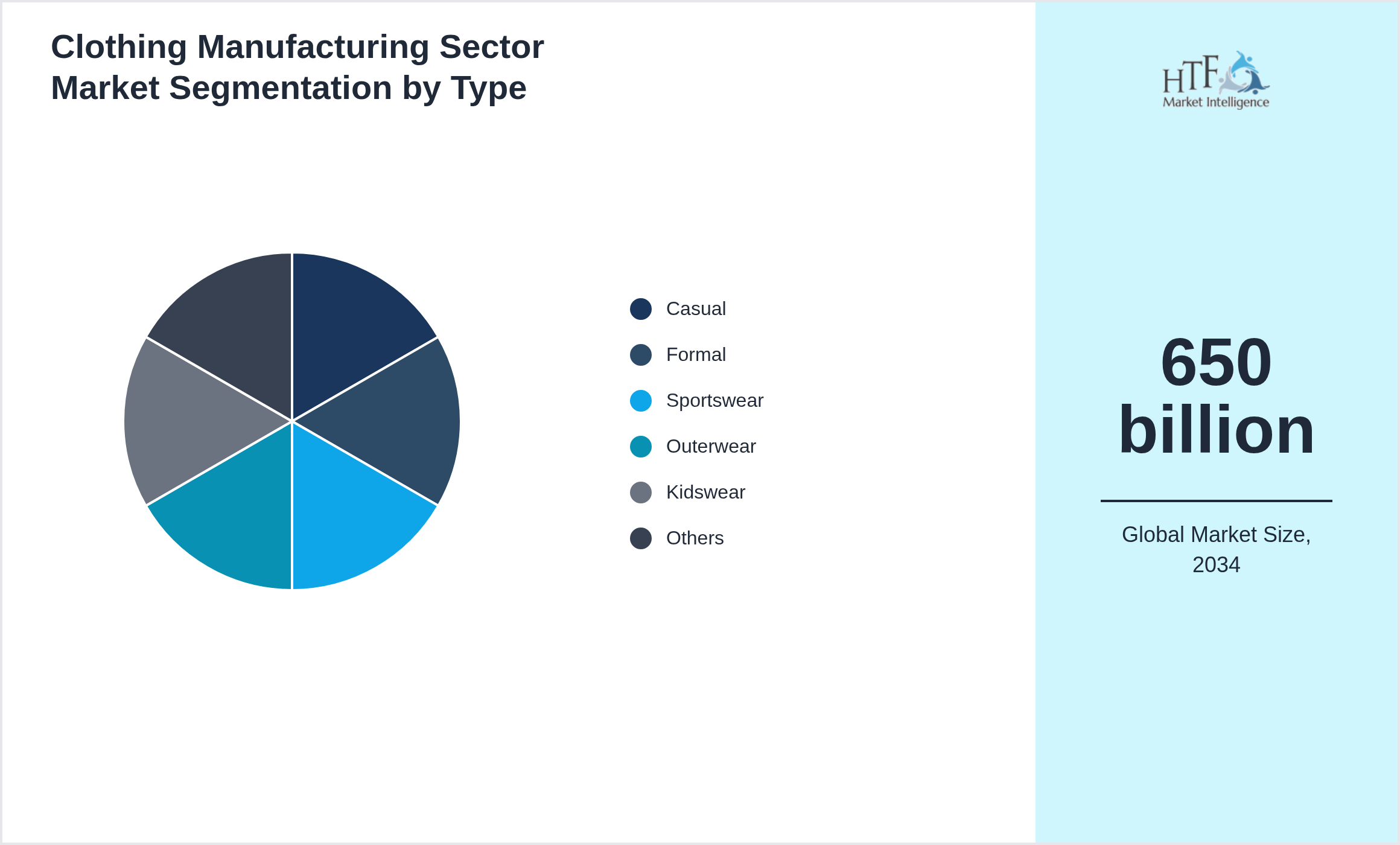

• Based on type, the market is bifurcated into the Casual, Formal, Sportswear, Outerwear, Kidswear, Workwear, Lingerie, Accessories segment, which dominated the market share during the forecasted period

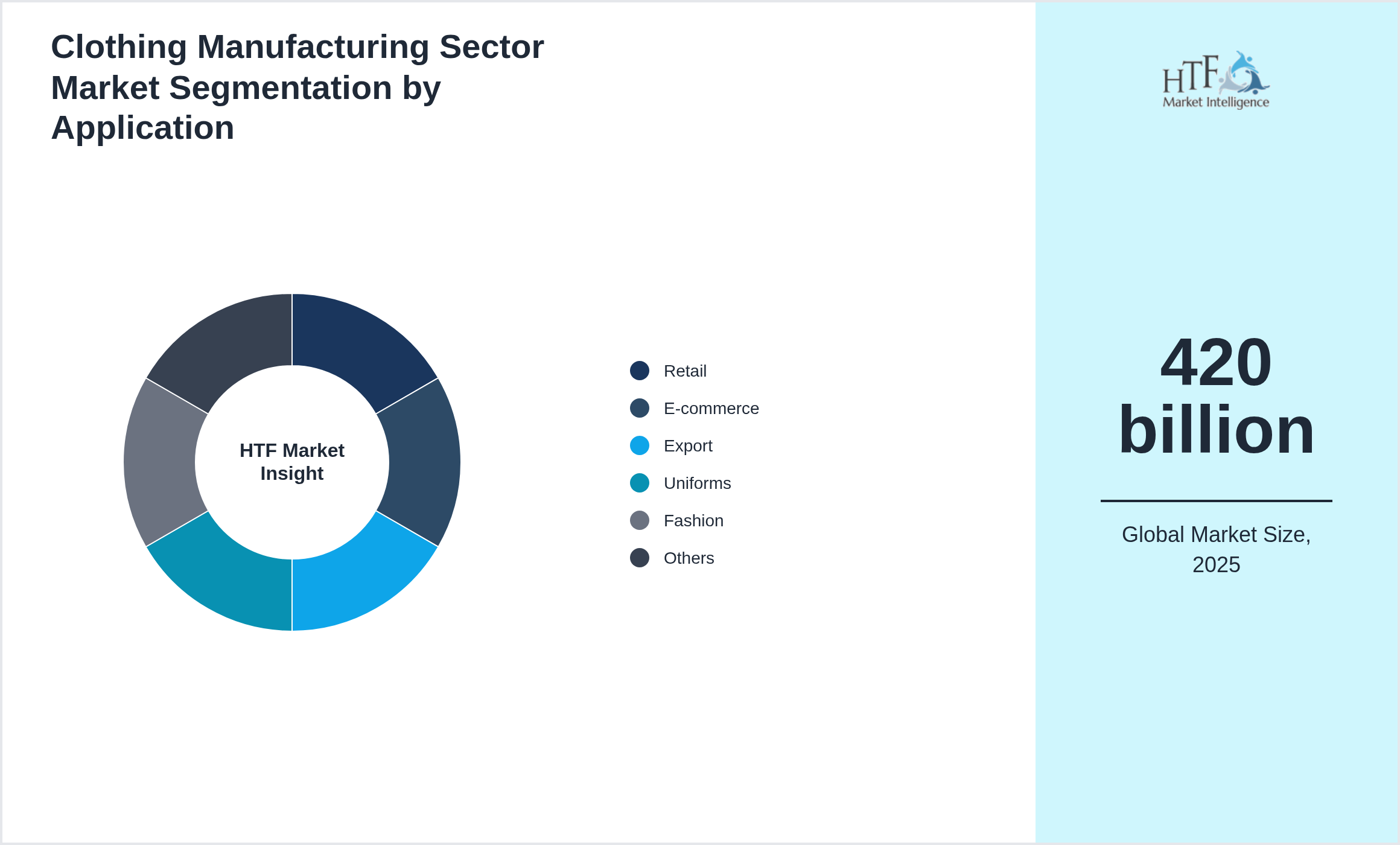

• Based on application, the market is segmented into Application Retail, E-commerce, Export, Uniforms, Fashion, Costumes, Private Label, Custom Orders as the fastest-growing segment.

• North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA import/export in terms of K tons, K units, and metric tons will be provided if applicable, based on industry best practices.

Market Dynamics Highlighted

What Growth Drivers are Powering Demand in the Clothing Manufacturing Sector Market?

- • Rising global fashion consumption and fast fashion trends drive sector growth Technological advancements in automation and supply chain management improve efficiency Increasing demand for sustainable and ethical manufacturing influences production practices Drivers: fashion demand tech innovation sustainability concerns.

- • Trends include adoption of automated cutting and sewing technologies Growing use of eco-friendly materials and sustainable supply chains Expansion of on-demand and customized manufacturing models to reduce waste Trends: automation sustainability customization.

Why does the Clothing Manufacturing Sector Market Face Growth Challenges?

Clothing Manufacturing Sector Market Segment Highlighted

Segmentation by Type

- • Casual

- • Formal

- • Sportswear

- • Outerwear

- • Kidswear

- • Workwear

- • Lingerie

- • Accessories

Segmentation by Application

- • Retail

- • E-commerce

- • Export

- • Uniforms

- • Fashion

- • Costumes

- • Private Label

- • Custom Orders

Key Players

The companies featured in this profile were selected based on insights from primary experts, evaluating their market penetration, product offerings, and geographical reach. By targeting emerging markets, these companies aim to leverage new opportunities, enhance their competitive advantage, and drive revenue growth. This approach not only aligns with their overall business objectives but also positions them to respond effectively to the evolving demands of consumers in these regions. Several key players in the Clothing Manufacturing Sector market are strategically focusing on expanding their operations in developing regions to capture a larger market share, particularly as the year-on-year growth rate for the market stands at 5.70%.

- • Inditex (Spain)

- • H&M (Sweden)

- • VF Corporation (US)

- • Nike (US)

- • Adidas (Germany)

- • Gap Inc. (US)

- • Fast Retailing (Japan)

- • PVH Corp. (US)

- • Levi Strauss & Co. (US)

- • LVMH (France)

- • Kering (France)

- • Uniqlo (Japan)

- • American Eagle Outfitters (US)

- • Columbia Sportswear (US)

- • Patagonia (US)

- • Under Armour (US)

- • ASOS (UK)

- • Zalando (Germany)

- • Next plc (UK)

- • C&A (Belgium)

- • Guess? (US)

- • Tommy Hilfiger (US)

- • Ralph Lauren (US)

- • Burberry (UK)

- • Calvin Klein (US)

- • Michael Kors (US)

- • Chanel (France)

Regional Insight

The Europe dominant region currently dominates the market share, fueled by increasing consumption, population growth, and sustained economic progress, which collectively enhance market demand. Conversely, the Asia-Pacific is growing rapidly, driven by significant infrastructure investments, industrial expansion, and rising consumer demand.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

- • North America maintains a technologically advanced Clothing Manufacturing Sector supported by automation premium apparel production and growing demand for sustainable fashion solutions. The United States and Mexico contribute significantly through nearshoring strategies advanced textile processing and integrated regional supply chains serving domestic and international apparel brands. Manufacturers increasingly adopt robotics AI-driven production planning and digital textile printing to improve operational efficiency and reduce lead times. Demand for ethically sourced clothing customized apparel and environmentally responsible manufacturing continues reshaping regional production strategies. Premium sportswear workwear and fashion apparel categories remain commercially significant across North American markets

- • Europe demonstrates strong global competitiveness in the Clothing Manufacturing Sector through luxury fashion leadership advanced textile engineering and sustainability-focused manufacturing ecosystems. Italy France Germany Spain and Portugal maintain highly specialized apparel production clusters supported by skilled labor premium fabric innovation and established export networks. Regulatory frameworks promoting circular fashion carbon reduction and ethical labor practices continue influencing regional manufacturing investments. High-value fashion exports designer collections and technical apparel production remain key revenue contributors across European textile industries

- • Asia Pacific functions as the dominant global Clothing Manufacturing Sector due to extensive apparel production capabilities in China Bangladesh Vietnam India and Indonesia. Cost-efficient labor vertically integrated textile ecosystems and large-scale export infrastructure support mass apparel manufacturing for international fashion brands. Rapid urbanization rising disposable income and expansion of domestic retail markets continue increasing regional apparel consumption. Investments in smart factories automated sewing technologies and sustainable textile production continue improving manufacturing efficiency and export competitiveness. Asia Pacific remains central to global apparel supply-chain operations and commercial scalability

- • Middle East markets are experiencing gradual growth through textile diversification initiatives expansion of regional apparel retailing and increasing investments in local garment manufacturing facilities. Gulf countries continue promoting industrial development and free trade zones to strengthen regional textile production capabilities. Demand for modest fashion premium apparel imports and climate-appropriate clothing products remains commercially significant. Commercial opportunities continue expanding through e-commerce growth fashion retail modernization and strategic trade positioning connecting Asian and European apparel supply chains

Market Entropy

Merger & Acquisition

- • Jan 2024: VF Corporation acquired ApparelWorks to expand clothing manufacturing globally.

- • Sep 2024: Gildan partnered with EcoFabric Labs to integrate sustainable textile production.

- • Feb 2025: HanesBrands merged with FashionTech Systems to strengthen industrial apparel portfolios.

Patent Analysis

- • Clothing Manufacturing Sector participants aggressively secure trademarks for fashion labels private apparel collections industrial garment solutions and sustainability-focused clothing lines to strengthen market competitiveness in global retail and export markets. Patent innovation is heavily focused on automated cutting systems robotic sewing technologies digital textile printing methods eco-friendly dyeing processes wrinkle-resistant fabrics and AI-driven production optimization tools that reduce manufacturing waste and improve productivity. Copyright protection increasingly applies to fashion designs technical garment specifications digital production templates marketing visuals and virtual apparel showrooms used across omnichannel retail ecosystems. Industry participants also protect proprietary supply chain software digital product lifecycle management systems and smart manufacturing analytics platforms through software-related copyrights and licensing agreements. Sustainability compliance and circular fashion initiatives continue accelerating intellectual property development related to recyclable textiles and low-emission manufacturing technologies

Investment and Funding Scenario

- • The Clothing Manufacturing Sector continues to attract substantial investment due to rising global apparel demand expansion of fast fashion and premium fashion categories increasing e-commerce penetration and technological modernization across textile production facilities. Manufacturers are securing institutional capital to automate sewing lines implement robotics-enabled cutting systems and establish digitally integrated smart factories capable of high-volume production with lower operational costs. Venture capital investment is increasing in startups focused on sustainable fabrics AI-based fashion analytics digital pattern generation and on-demand apparel manufacturing technologies. Joint ventures between international apparel brands and regional manufacturers are supporting localized production expansion and export diversification strategies. Shareholding acquisitions across textile and garment companies are enabling global brands to secure sourcing stability and strengthen control over vertically integrated manufacturing ecosystems. Commercial banks and export-import institutions are extending financing support for factory expansion machinery upgrades and raw material procurement operations. Sustainability-focused investments are accelerating deployment of renewable energy systems water recycling technologies and eco-friendly dyeing infrastructure to meet international environmental standards. Seed-funded fashion technology firms are introducing blockchain-based supply-chain transparency solutions and AI-driven production planning systems that improve operational efficiency and compliance management. Institutional investors are increasingly supporting apparel manufacturing clusters focused on technical textiles premium garments and sportswear production. Several large clothing manufacturers are also investing in nearshoring facilities and regional distribution centers to reduce shipping delays and improve responsiveness to consumer demand trends. Private equity-driven consolidation within garment production networks is further improving economies of scale supplier bargaining power and commercial competitiveness across global textile markets

Report Infographics

| Report Features | Details |

| Base Year | 2025 |

| Based Year Market Size (2025) | 420 billion |

| Historical Period | 2021 to 2025 |

| CAGR (2025 to 2034) | 6.20% |

| Forecast Period | 2026 to 2034 |

| Forecasted Period Market Size (2034) | 650 billion |

| Scope of the Report |

By Type, By Application, By Region |

| Companies Covered | Inditex (Spain), H&M (Sweden), VF Corporation (US), Nike (US), Adidas (Germany), Gap Inc. (US), Fast Retailing (Japan), PVH Corp. (US), Levi Strauss & Co. (US), LVMH (France), Kering (France), Uniqlo (Japan), American Eagle Outfitters (US), Columbia Sportswear (US), Patagonia (US), Under Armour (US), ASOS (UK), Zalando (Germany), Next plc (UK), C&A (Belgium), Guess? (US), Tommy Hilfiger (US), Ralph Lauren (US), Burberry (UK), Calvin Klein (US), Michael Kors (US), Chanel (France) |

| Customization Scope | 15% Free Customization

Want to Buy Specific Sections of This Report?

|

| Delivery Format | PDF and Excel through Email |

The Top-Down and Bottom-Up Approaches

The top-down approach begins with a broad theory or hypothesis and breaks it down into specific components for testing. This structured, deductive process involves developing a theory, creating hypotheses, collecting and analyzing data, and drawing conclusions for Clothing Manufacturing Sector Market. It is particularly useful when there is substantial theoretical knowledge, but it can be rigid and may overlook new phenomena developing in Clothing Manufacturing Sector Industry.

Conversely, the bottom-up approach starts with specific data or observations, from which broader generalizations and theories were developed in Clothing Manufacturing Sector Industry. This inductive process involves collecting detailed data, analyzing it for patterns, developing hypotheses, formulating theories, and validating them with additional data identified for Clothing Manufacturing Sector Market. While this approach is flexible and encourages the discovery of new phenomena, it can be time-consuming and less structured.

Regulatory Framework

The healthcare sector is overseen by various regulatory bodies that ensure the safety, quality, and efficacy of health services and products. In the United States, the U.S. Department of Health and Human Services (HHS) plays a crucial role in protecting public health and providing essential human services. Within HHS, the Food and Drug Administration (FDA) regulates food, drugs, and medical devices, ensuring they meet safety and efficacy standards. The Centers for Disease Control and Prevention (CDC) focuses on disease control and prevention, conducting research, and providing health information to protect public health.

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.