Food-Grade Packaging Materials Market - Global Size & Outlook 2021-2034

Global Food-Grade Packaging Materials Market is segmented by Application (Dairy, Beverages, Packaged Foods, Snacks, Frozen Foods, Ready-to-Eat, Meat & Seafood, Confectionery), Type (Flexible Films, Paperboard, PET Containers, Aluminum Foil, Plastic Trays, Glass Jars, Metal Cans, Laminates), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

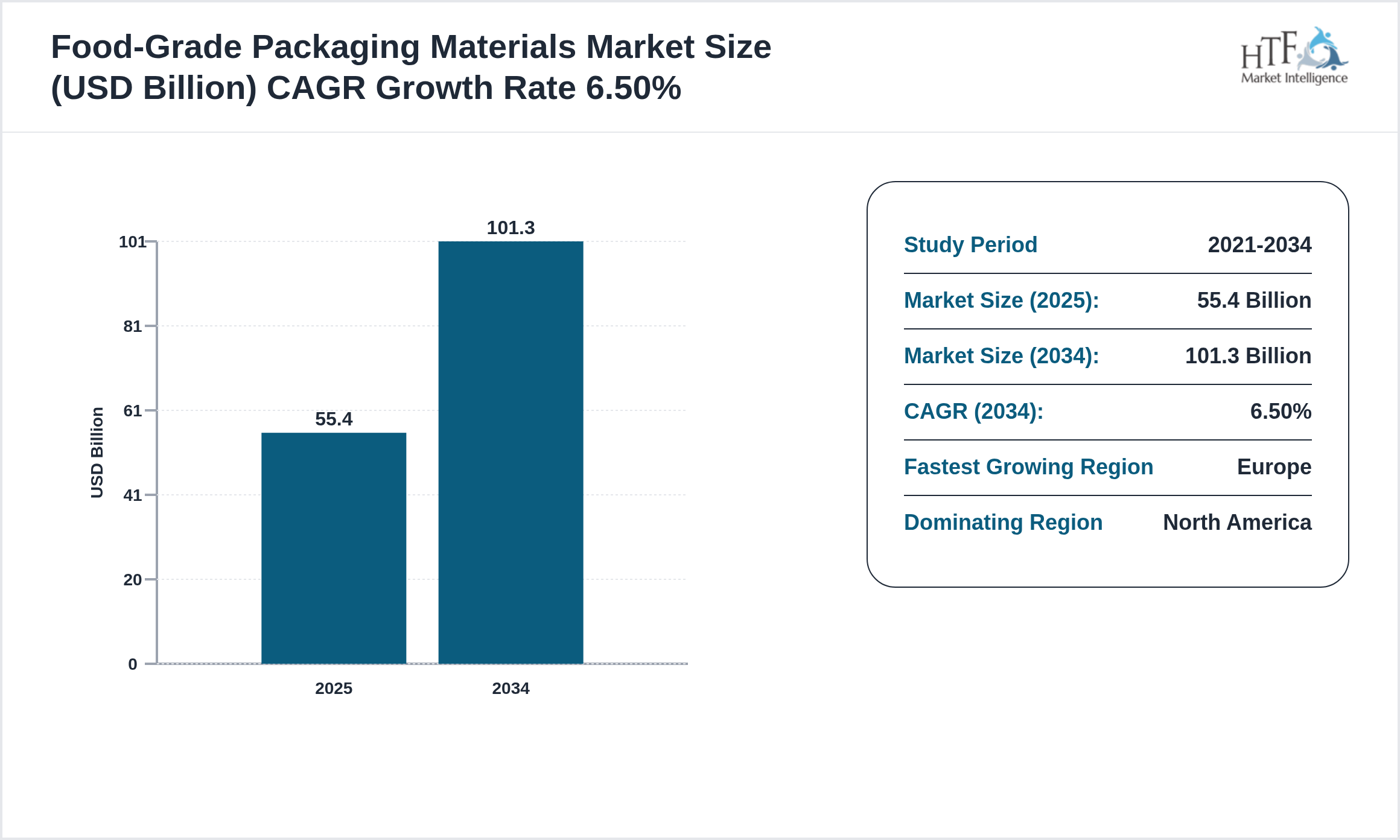

The Food-Grade Packaging Materials market is witnessing significant growth and is expected to expand at a CAGR of 6.50% during the forecast period from 2025 to 2034. This growth is primarily driven by increasing technological advancements, rising consumer demand, and expanding applications across various industries. Businesses are increasingly adopting innovative solutions to improve operational efficiency, enhance customer experiences, and gain a competitive advantage, further fueling market expansion.

Source: HTF Market Intelligence (HTF MI)

The Food-Grade Packaging Materials market refers to packaging solutions specifically manufactured using safe, compliant, and contamination-resistant materials designed for storing, transporting, and preserving food and beverage products. These materials ensure product integrity, hygiene, shelf-life extension, and regulatory compliance across the global food supply chain. The market scope includes paper-based packaging, food-safe plastics, aluminum foils, flexible laminates, biodegradable wraps, and protective barrier materials used in processed foods, dairy, beverages, frozen foods, and ready-to-eat products. It excludes industrial packaging unrelated to food applications and non-certified packaging materials lacking food safety compliance. Primary growth catalysts include rising packaged food consumption, increasing food safety regulations, expansion of e-commerce grocery delivery, and demand for sustainable packaging alternatives. Demand-side dynamics are shaped by consumer preference for convenient and eco-friendly packaging, while manufacturers seek enhanced preservation efficiency. Supply-side transformation is driven by recyclable materials, bio-based polymers, and advanced barrier coating technologies. Technological evolution continues through smart labeling, active packaging systems, and AI-enabled packaging quality monitoring solutions

The research study Food-Grade Packaging Materials Market gives readers information on tactical business choices and strategic planning that affect and stabilize the growth prediction in the Food-Grade Packaging Materials market. However, a few disruptive trends will have opposite and significant effects on the distribution among players and the growth of the Food-Grade Packaging Materials market. To give further advice on why certain developments in the Food-Grade Packaging Materials market would have a significant impact and specifically why these trends can be taken into account when determining the market's trajectory and industry participants' strategic plans.

Key Highlights

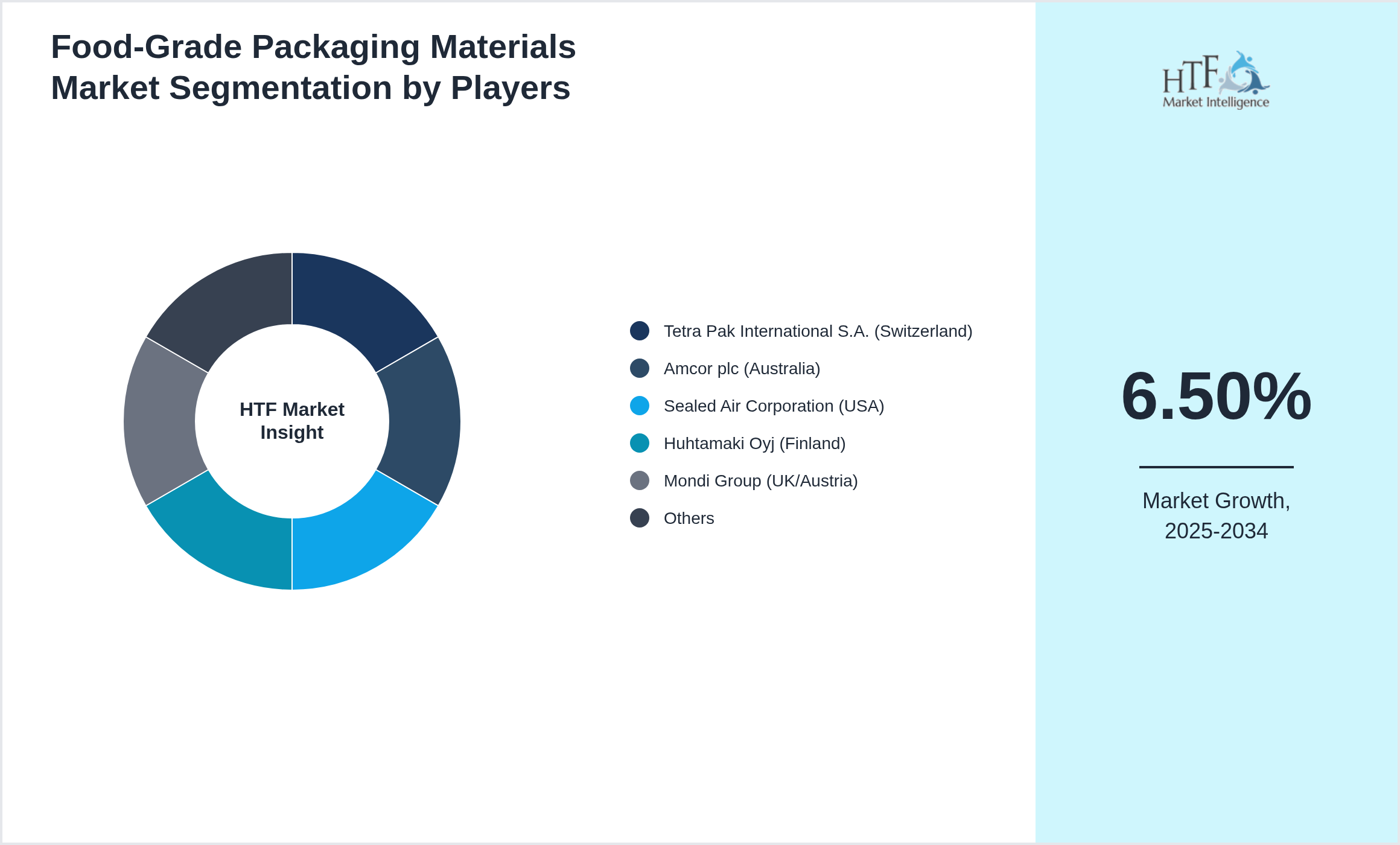

• The Food-Grade Packaging Materials is growing at a CAGR of 6.50% during the forecasted period of 2025 to 2034

• Year-on-year growth for the market is 6.20%.

• North America dominated the market share in 2025

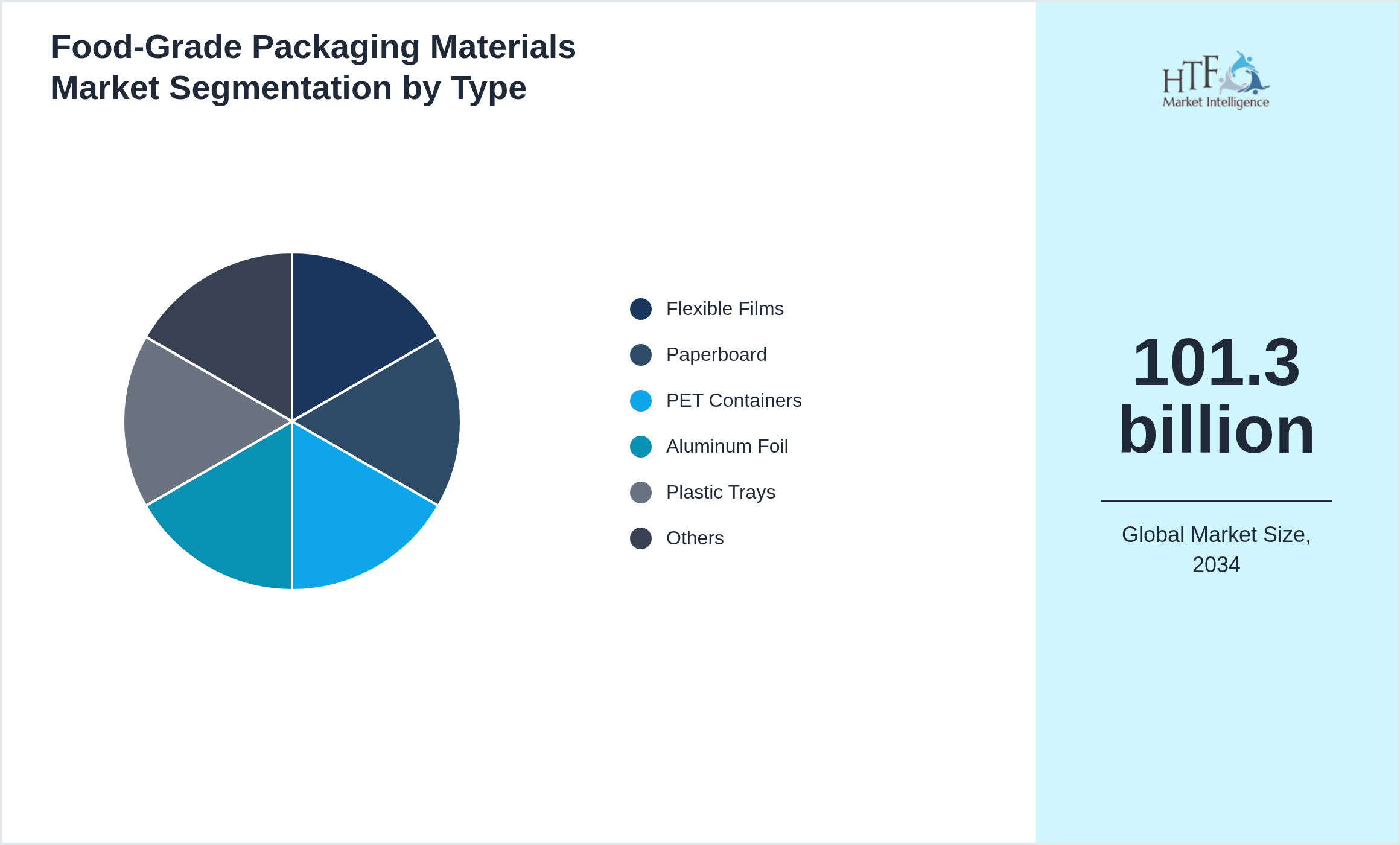

• Based on type, the market is bifurcated into the Flexible Films, Paperboard, PET Containers, Aluminum Foil, Plastic Trays, Glass Jars, Metal Cans, Laminates segment, which dominated the market share during the forecasted period

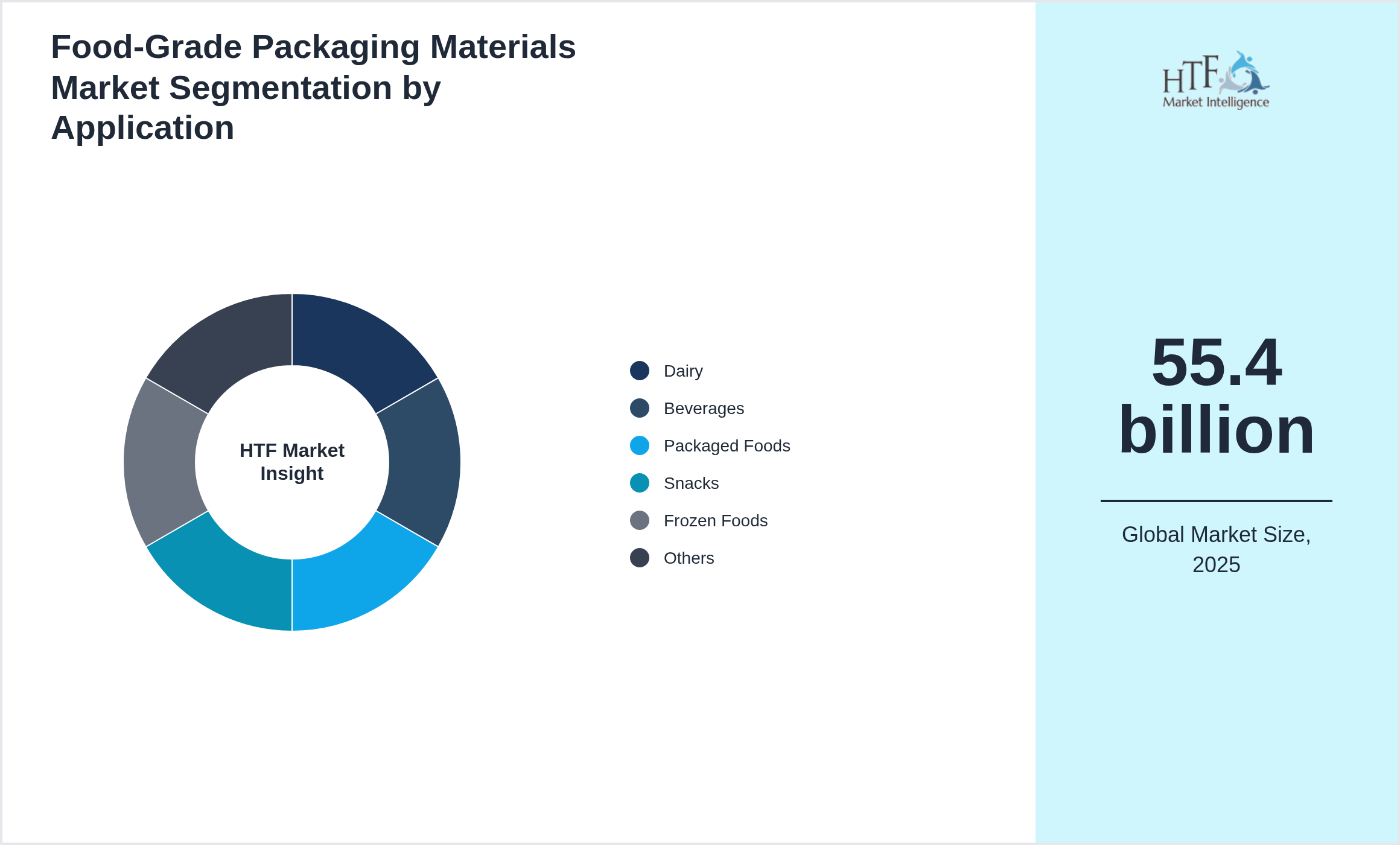

• Based on application, the market is segmented into Application Dairy, Beverages, Packaged Foods, Snacks, Frozen Foods, Ready-to-Eat, Meat & Seafood, Confectionery as the fastest-growing segment.

• North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA import/export in terms of K tons, K units, and metric tons will be provided if applicable, based on industry best practices.

Market Dynamics Highlighted

Market Driver

The Food-Grade Packaging Materials market is experiencing significant growth due to various factors.

- • The Food-Grade Packaging Materials market is driven by increasing food production growing packaged food consumption and stringent food safety regulations. Manufacturers require packaging materials that protect product quality prevent contamination extend shelf life and comply with regulatory standards. Growth in convenience foods food delivery services and international food trade is accelerating demand for advanced food-grade packaging solutions. Rising consumer awareness regarding food safety and product freshness is further encouraging adoption of high-performance packaging materials across food processing and distribution industries

Market Trend

The Food-Grade Packaging Materials market is growing rapidly due to various factors.

- • The market is witnessing strong adoption of high-barrier materials sustainable food packaging solutions active packaging technologies and recyclable food-contact materials. Manufacturers are increasingly utilizing advanced coatings antimicrobial packaging systems and intelligent freshness monitoring solutions to improve product performance. There is growing emphasis on PFAS-free materials bio-based packaging alternatives and lightweight structures that maintain food protection standards. Digital traceability technologies and food safety compliance systems are also becoming important trends supporting transparency and quality assurance across food supply chains

Opportunity

The Food-Grade Packaging Materials has several opportunities, particularly in developing countries where industrialization is growing.

Challenge

The market for fluid power systems faces several obstacles despite its promising growth possibilities.

Food-Grade Packaging Materials Market Segment Highlighted

Segmentation by Type

- • Flexible Films

- • Paperboard

- • PET Containers

- • Aluminum Foil

- • Plastic Trays

- • Glass Jars

- • Metal Cans

- • Laminates

Segmentation by Application

- • Dairy

- • Beverages

- • Packaged Foods

- • Snacks

- • Frozen Foods

- • Ready-to-Eat

- • Meat & Seafood

- • Confectionery

Key Players

The companies featured in this profile were selected based on insights from primary experts, evaluating their market penetration, product offerings, and geographical reach. By targeting emerging markets, these companies aim to leverage new opportunities, enhance their competitive advantage, and drive revenue growth. This approach not only aligns with their overall business objectives but also positions them to respond effectively to the evolving demands of consumers in these regions. Several key players in the Food-Grade Packaging Materials market are strategically focusing on expanding their operations in developing regions to capture a larger market share, particularly as the year-on-year growth rate for the market stands at 6.20%.

- • Tetra Pak International S.A. (Switzerland)

- • Amcor plc (Australia)

- • Sealed Air Corporation (USA)

- • Huhtamaki Oyj (Finland)

- • Mondi Group (UK/Austria)

- • Berry Global

- • Inc. (USA)

- • Uflex Ltd. (India)

- • Stora Enso Oyj (Finland)

- • Sonoco Products Company (USA)

- • Smurfit Kappa Group (Ireland)

- • WestRock Company (USA)

- • Constantia Flexibles GmbH (Austria)

- • Coveris Holdings S.A. (Austria)

- • RPC Group Plc (UK)

- • AptarGroup

- • Inc. (USA)

Regional Insight

The North America dominant region currently dominates the market share, fueled by increasing consumption, population growth, and sustained economic progress, which collectively enhance market demand. Conversely, the Europe is growing rapidly, driven by significant infrastructure investments, industrial expansion, and rising consumer demand.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

- • North America: North America’s food-grade packaging materials market is dominated by stringent safety standards regulatory compliance with FDA and high consumer demand for fresh ready-to-eat and convenient foods. Production strengths include high-capacity polymer and paper packaging plants advanced sterilization and sealing technology and integrated supply chains. Sustainability initiatives encourage recyclable and compostable materials.

- • Europe: Europe maintains strong food-grade packaging demand led by Germany France and Italy focusing on compliance with EU food safety regulations and consumer preference for environmentally sustainable materials. Smart packaging for freshness and traceability is gaining traction.

- • Asia Pacific: Rapid population growth and urbanization in China India and Southeast Asia drive high demand for food-grade packaging. Local manufacturing benefits from low-cost production and raw material availability. E-commerce food delivery and packaged convenience foods further accelerate adoption.

- • Middle East: Demand grows in UAE Saudi Arabia and Qatar due to increasing packaged food imports and domestic consumption. Food safety regulations and compliance requirements influence packaging selection while supply chains rely on a mix of imports and local manufacturing for durable and hygienic materials.

Market Entropy

Merger & Acquisition

- • Jan 2024: Tetra Pak acquired SafeFood Packaging Systems to expand food-grade materials globally.

- • Sep 2024: Huhtamaki partnered with BioSafe Labs to integrate hygienic and sustainable packaging.

- • Feb 2025: Berry Global merged with FoodPack Innovations to strengthen FMCG supply chains.

Patent Analysis

- • Patent activity focuses on antimicrobial coatings barrier films sustainable polymers vacuum packaging modified-atmosphere food packaging active packaging and multilayer composite solutions. North America leads patents in functional food packaging and smart barrier films. Europe emphasizes biodegradable and recyclable innovations as well as anti-contamination solutions. Asia-Pacific patents increasingly target cost-effective high-volume production shelf-life optimization and food preservation technologies.

Investment and Funding Scenario

- • Investment is driven by e-commerce food delivery processed food expansion convenience foods and retail-ready packaging. Asia-Pacific attracts significant manufacturing investment due to cost and scale advantages. North America funds sustainable packaging startups antimicrobial solutions and advanced material development. Europe focuses on recyclable renewable and premium-grade packaging materials. Investment also flows into R&D for active and intelligent packaging solutions that extend shelf life and reduce spoilage.

Report Infographics

| Report Features | Details |

| Base Year | 2025 |

| Based Year Market Size (2025) | 55.4 billion |

| Historical Period | 2021 to 2025 |

| CAGR (2025 to 2034) | 6.50% |

| Forecast Period | 2026 to 2034 |

| Forecasted Period Market Size (2034) | 101.3 billion |

| Scope of the Report |

By Type, By Application, By Region |

| Companies Covered | Tetra Pak International S.A. (Switzerland), Amcor plc (Australia), Sealed Air Corporation (USA), Huhtamaki Oyj (Finland), Mondi Group (UK/Austria), Berry Global, Inc. (USA), Uflex Ltd. (India), Stora Enso Oyj (Finland), Sonoco Products Company (USA), Smurfit Kappa Group (Ireland), WestRock Company (USA), Constantia Flexibles GmbH (Austria), Coveris Holdings S.A. (Austria), RPC Group Plc (UK), AptarGroup, Inc. (USA) |

| Customization Scope | 15% Free Customization

Want to Buy Specific Sections of This Report?

|

| Delivery Format | PDF and Excel through Email |

The Top-Down and Bottom-Up Approaches

The top-down approach begins with a broad theory or hypothesis and breaks it down into specific components for testing. This structured, deductive process involves developing a theory, creating hypotheses, collecting and analyzing data, and drawing conclusions. It is particularly useful when there is substantial theoretical knowledge, but it can be rigid and may overlook new phenomena.

Conversely, the bottom-up approach starts with specific data or observations, from which broader generalizations and theories are developed. This inductive process involves collecting detailed data, analyzing it for patterns, developing hypotheses, formulating theories, and validating them with additional data. While this approach is flexible and encourages the discovery of new phenomena, it can be time-consuming and less structured.

Regulatory Framework

The healthcare sector is overseen by various regulatory bodies that ensure the safety, quality, and efficacy of health services and products. In the United States, the U.S. Department of Health and Human Services (HHS) plays a crucial role in protecting public health and providing essential human services. Within HHS, the Food and Drug Administration (FDA) regulates food, drugs, and medical devices, ensuring they meet safety and efficacy standards. The Centers for Disease Control and Prevention (CDC) focuses on disease control and prevention, conducting research, and providing health information to protect public health.

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.