Carbon Capture Materials Market - Global Share, Size & Changing Dynamics 2020-2033

Global Carbon Capture Materials Market is segmented by Application (Power Generation, Industrial Emissions, Oil & Gas, Cement Production, Steel Manufacturing), Type (Adsorbents, Solvents, Membranes, Catalysts, Amine-Based Materials), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

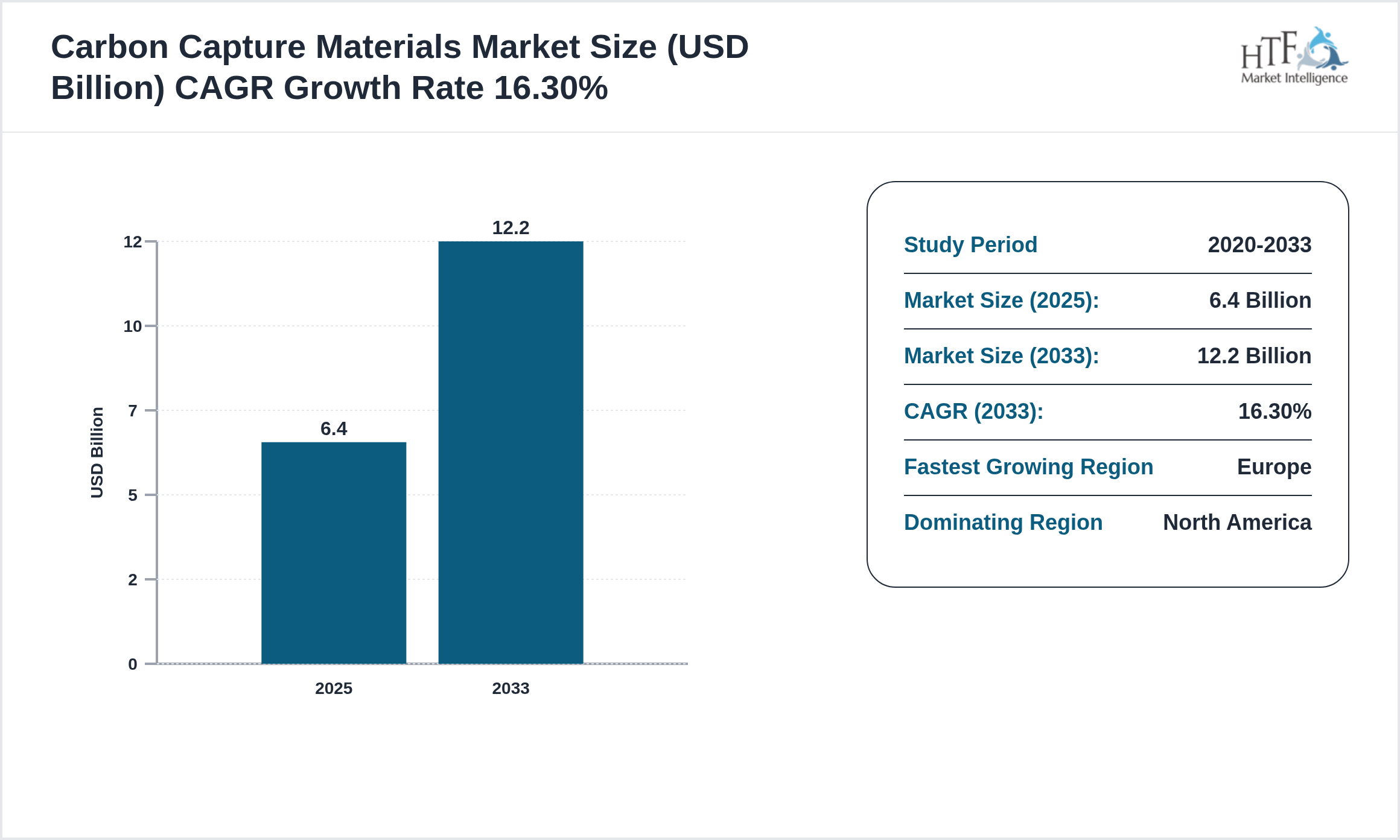

The Carbon Capture Materials market is witnessing significant growth and is expected to expand at a CAGR of 16.30% during the forecast period from 2025 to 2033. This growth is primarily driven by increasing technological advancements, rising consumer demand, and expanding applications across various industries. Businesses are increasingly adopting innovative solutions to improve operational efficiency, enhance customer experiences, and gain a competitive advantage, further fueling market expansion.

Source: HTF Market Intelligence (HTF MI)

The carbon capture materials market is focused on technologies and materials that capture and store carbon dioxide (CO2) emissions. This is crucial for reducing greenhouse gases and achieving carbon neutrality. The market is growing rapidly, driven by government regulations on emissions and the demand for low-carbon solutions. These materials are used in power generation, industrial processes, and cement production, helping industries reduce their environmental footprint.

The research study Carbon Capture Materials Market gives readers information on tactical business choices and strategic planning that affect and stabilize the growth prediction in the Carbon Capture Materials market. However, a few disruptive trends will have opposite and significant effects on the distribution among players and the growth of the Carbon Capture Materials market. To give further advice on why certain developments in the Carbon Capture Materials market would have a significant impact and specifically why these trends can be taken into account when determining the market's trajectory and industry participants' strategic plans.

Key Highlights

• The Carbon Capture Materials is growing at a CAGR of 16.30% during the forecasted period of 2025 to 2033

• Year-on-year growth for the market is 14.90%.

• North America dominated the market share in 2025

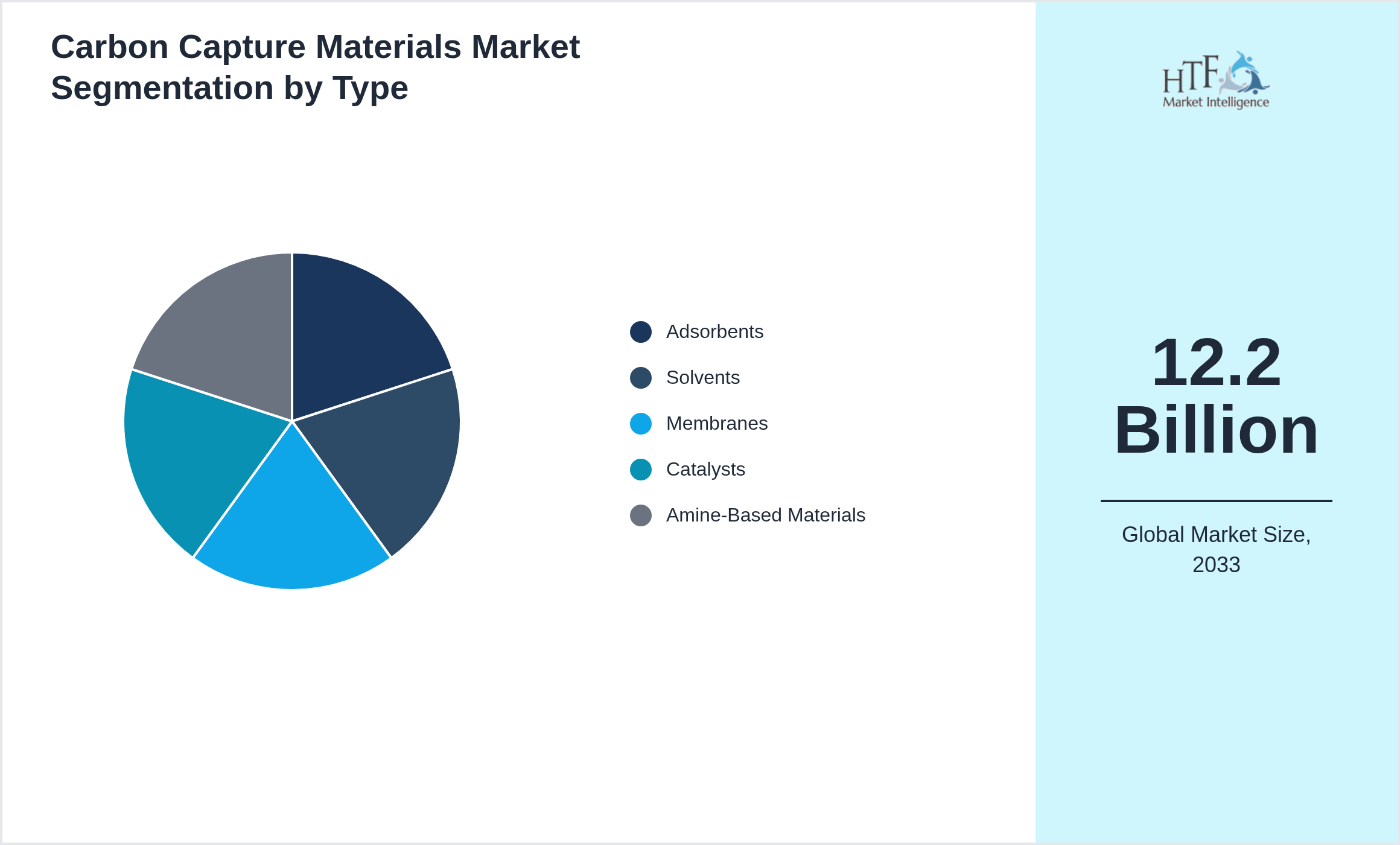

• Based on type, the market is bifurcated into the Adsorbents, Solvents, Membranes, Catalysts, Amine-Based Materials segment, which dominated the market share during the forecasted period

• Based on application, the market is segmented into Application Power Generation, Industrial Emissions, Oil & Gas, Cement Production, Steel Manufacturing as the fastest-growing segment.

• North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA import/export in terms of K tons, K units, and metric tons will be provided if applicable, based on industry best practices.

Market Dynamics Highlighted

Market Driver

The Carbon Capture Materials market is experiencing significant growth due to various factors.

- • Increasing Global CO2 Emissions

- • Rising Government Regulations On Carbon Emissions

- • Increased Focus On Sustainable Practices

- • Demand For Carbon Neutral Solutions

- • Investment In Carbon Capture Technologies

Market Trend

The Carbon Capture Materials market is growing rapidly due to various factors.

- • Integration With Renewable Energy Systems

- • Rise In Carbon Credit Trading

- • Demand For Low-Cost Carbon Capture Solutions

- • Increase In Circular Economy Initiatives

- • Focus On CO2 Reduction

Opportunity

The Carbon Capture Materials has several opportunities, particularly in developing countries where industrialization is growing.

Challenge

The market for fluid power systems faces several obstacles despite its promising growth possibilities.

Carbon Capture Materials Market Segment Highlighted

Segmentation by Type

- • Adsorbents

- • Solvents

- • Membranes

- • Catalysts

- • Amine-Based Materials

Segmentation by Application

- • Power Generation

- • Industrial Emissions

- • Oil & Gas

- • Cement Production

- • Steel Manufacturing

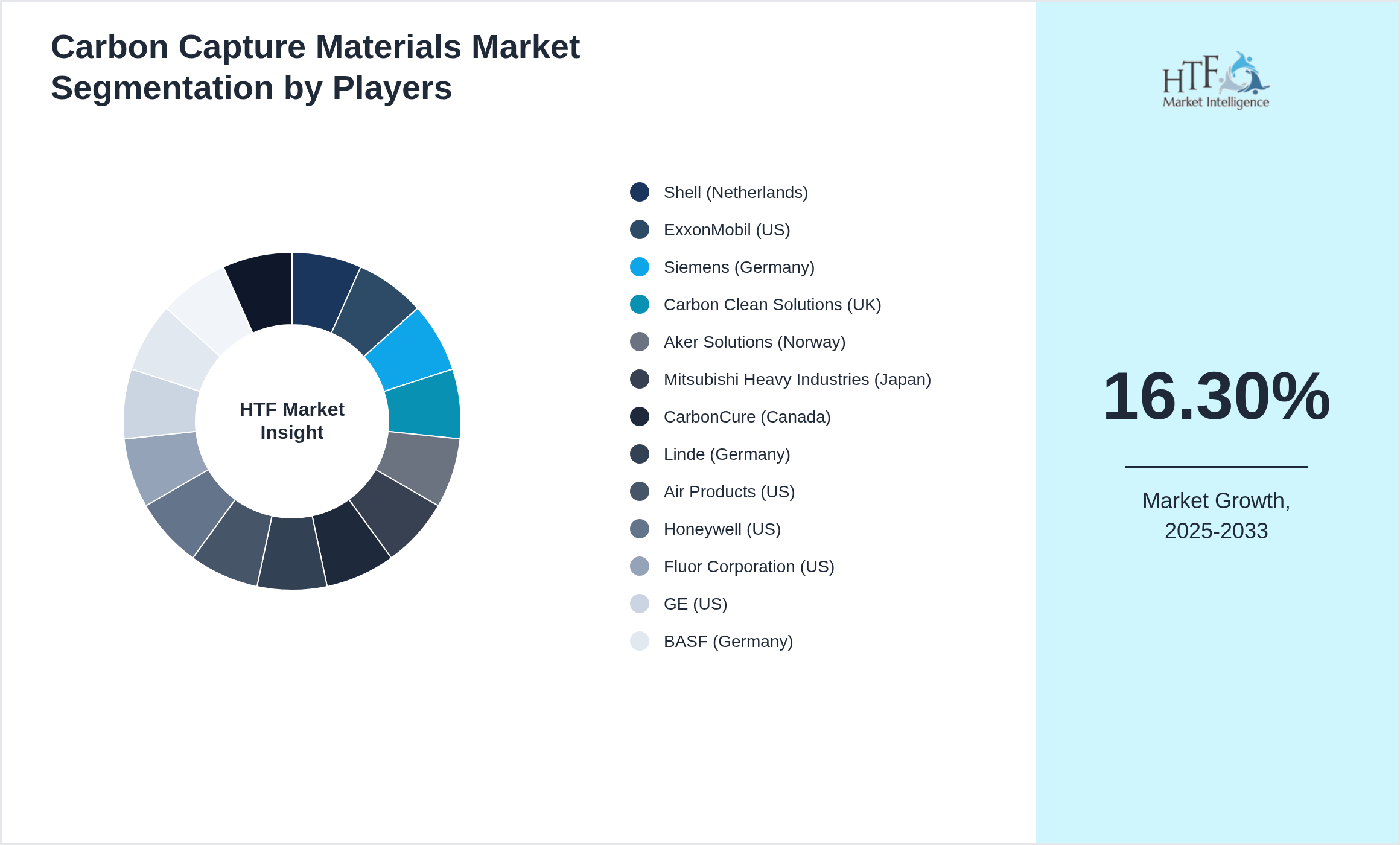

Key Players

The companies featured in this profile were selected based on insights from primary experts, evaluating their market penetration, product offerings, and geographical reach. By targeting emerging markets, these companies aim to leverage new opportunities, enhance their competitive advantage, and drive revenue growth. This approach not only aligns with their overall business objectives but also positions them to respond effectively to the evolving demands of consumers in these regions. Several key players in the Carbon Capture Materials market are strategically focusing on expanding their operations in developing regions to capture a larger market share, particularly as the year-on-year growth rate for the market stands at 14.90%.

- • Shell (Netherlands)

- • ExxonMobil (US)

- • Siemens (Germany)

- • Carbon Clean Solutions (UK)

- • Aker Solutions (Norway)

- • Mitsubishi Heavy Industries (Japan)

- • CarbonCure (Canada)

- • Linde (Germany)

- • Air Products (US)

- • Honeywell (US)

- • Fluor Corporation (US)

- • GE (US)

- • BASF (Germany)

- • SABIC (Saudi Arabia)

- • TotalEnergies (France)

Regional Insight

The North America dominant region currently dominates the market share, fueled by increasing consumption, population growth, and sustained economic progress, which collectively enhance market demand. Conversely, the Europe is growing rapidly, driven by significant infrastructure investments, industrial expansion, and rising consumer demand.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

- • Carbon capture materials are gaining momentum globally

Market Entropy

Merger & Acquisition

- • May 2023: CarbonTech Solutions acquired by GreenEnergy

Patent Analysis

- • Patents focus on improving the efficiency and scalability of carbon capture materials for industrial and energy applications.

Investment and Funding Scenario

- • Investment in carbon capture technologies is surging as industries look for ways to meet climate targets and reduce their carbon footprints.

Report Infographics

| Report Features | Details |

| Base Year | 2025 |

| Based Year Market Size (2025) | 6.4 Billion |

| Historical Period | 2020 to 2025 |

| CAGR (2025 to 2033) | 16.30% |

| Forecast Period | 2026 to 2033 |

| Forecasted Period Market Size (2033) | 12.2 Billion |

| Scope of the Report |

By Type, By Application, By Region |

| Companies Covered | Shell (Netherlands), ExxonMobil (US), Siemens (Germany), Carbon Clean Solutions (UK), Aker Solutions (Norway), Mitsubishi Heavy Industries (Japan), CarbonCure (Canada), Linde (Germany), Air Products (US), Honeywell (US), Fluor Corporation (US), GE (US), BASF (Germany), SABIC (Saudi Arabia), TotalEnergies (France) |

| Customization Scope | 15% Free Customization

Want to Buy Specific Sections of This Report?

|

| Delivery Format | PDF and Excel through Email |

The Top-Down and Bottom-Up Approaches

The top-down approach begins with a broad theory or hypothesis and breaks it down into specific components for testing. This structured, deductive process involves developing a theory, creating hypotheses, collecting and analyzing data, and drawing conclusions. It is particularly useful when there is substantial theoretical knowledge, but it can be rigid and may overlook new phenomena.

Conversely, the bottom-up approach starts with specific data or observations, from which broader generalizations and theories are developed. This inductive process involves collecting detailed data, analyzing it for patterns, developing hypotheses, formulating theories, and validating them with additional data. While this approach is flexible and encourages the discovery of new phenomena, it can be time-consuming and less structured.

Regulatory Framework

The healthcare sector is overseen by various regulatory bodies that ensure the safety, quality, and efficacy of health services and products. In the United States, the U.S. Department of Health and Human Services (HHS) plays a crucial role in protecting public health and providing essential human services. Within HHS, the Food and Drug Administration (FDA) regulates food, drugs, and medical devices, ensuring they meet safety and efficacy standards. The Centers for Disease Control and Prevention (CDC) focuses on disease control and prevention, conducting research, and providing health information to protect public health.