Global Nickel Base Electrode Market Roadmap to 2033

Global Nickel Base Electrode Market is segmented by Application (Welding, Electronics, Aerospace, Power generation, Chemical processing), Type (Standard, Coated, Alloyed, High-temp, Precision), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

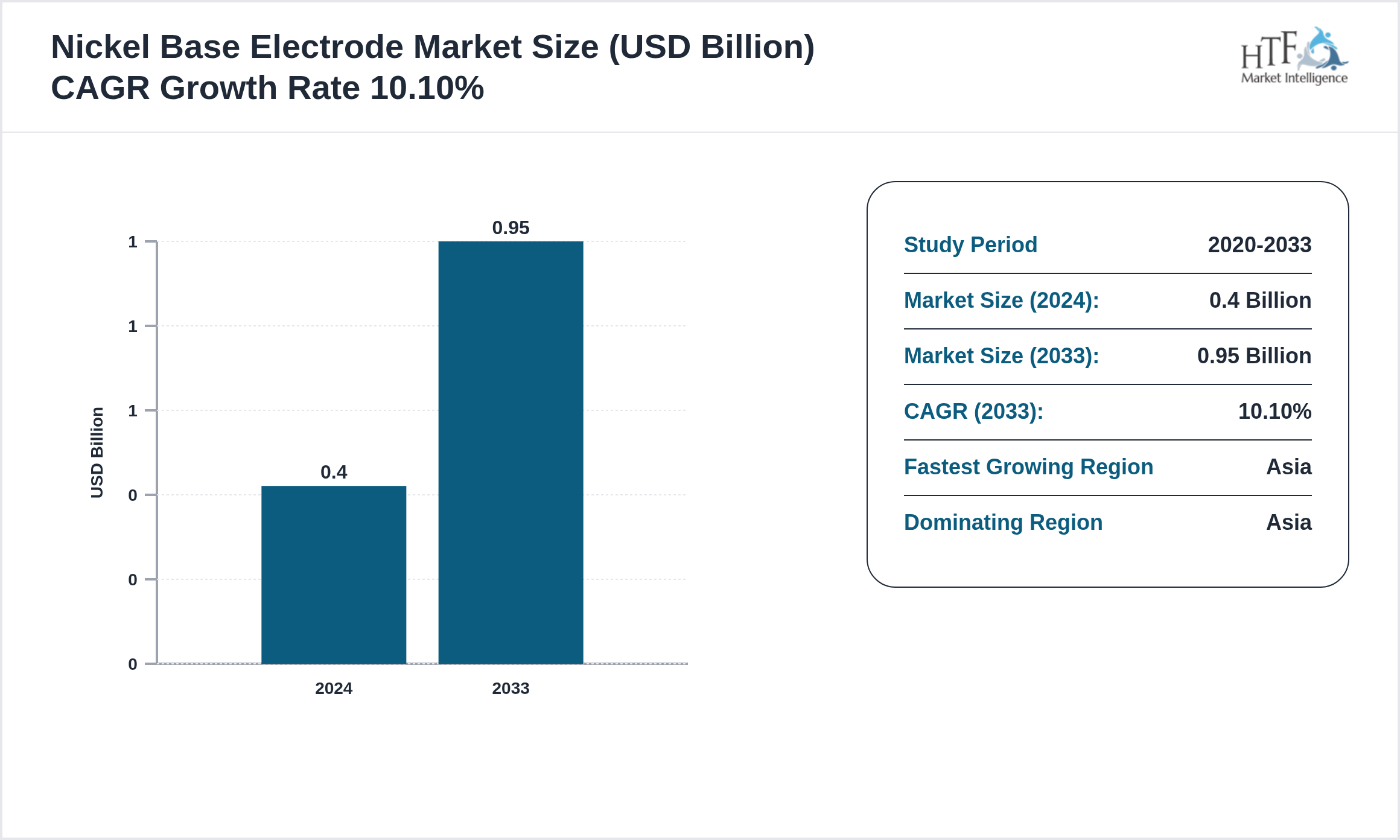

The Nickel Base Electrode is at USD 0.40 billion in 2024 and is expected to reach 0.95 billion by 2033. The Nickel Base Electrode is driven by increasing demand in end-use industries, technological advancements, research and development (R&D), economic growth, and global trade.

Nickel Base Electrode refers to specialized welding and electrical conduction materials manufactured primarily using nickel and nickel-alloy compositions designed for high-temperature resistance, corrosion protection, mechanical durability, and superior metallurgical bonding across industrial fabrication and heavy engineering applications. These electrodes are extensively used in arc welding, thermal processing, industrial repair operations, pressure vessel manufacturing, offshore infrastructure, petrochemical systems, aerospace assemblies, power generation equipment, marine engineering, and stainless-steel fabrication where resistance to oxidation, chemical exposure, and thermal stress is critical. The market includes nickel alloy welding electrodes, coated electrodes, flux-cored nickel consumables, low-hydrogen electrodes, superalloy welding rods, and high-performance conductive joining materials integrated into automated and semi-automated welding systems. Increasing industrial infrastructure modernization, expansion of oil & gas projects, growth in renewable power infrastructure, and rising demand for durable welding consumables in corrosive environments are accelerating global market demand. Manufacturers are investing in precision metallurgy technologies, AI-assisted quality inspection systems, robotic welding compatibility, sustainable alloy processing methods, and advanced flux coating formulations to improve welding consistency, deposition efficiency, and operational reliability. Integration of smart manufacturing infrastructure, predictive maintenance analytics, Industry 4.0-enabled fabrication systems, and automated industrial production ecosystems is further strengthening commercial scalability, production optimization, and technological advancement across global heavy industrial and engineering sectors.

Source: HTF Market Intelligence (HTF MI)

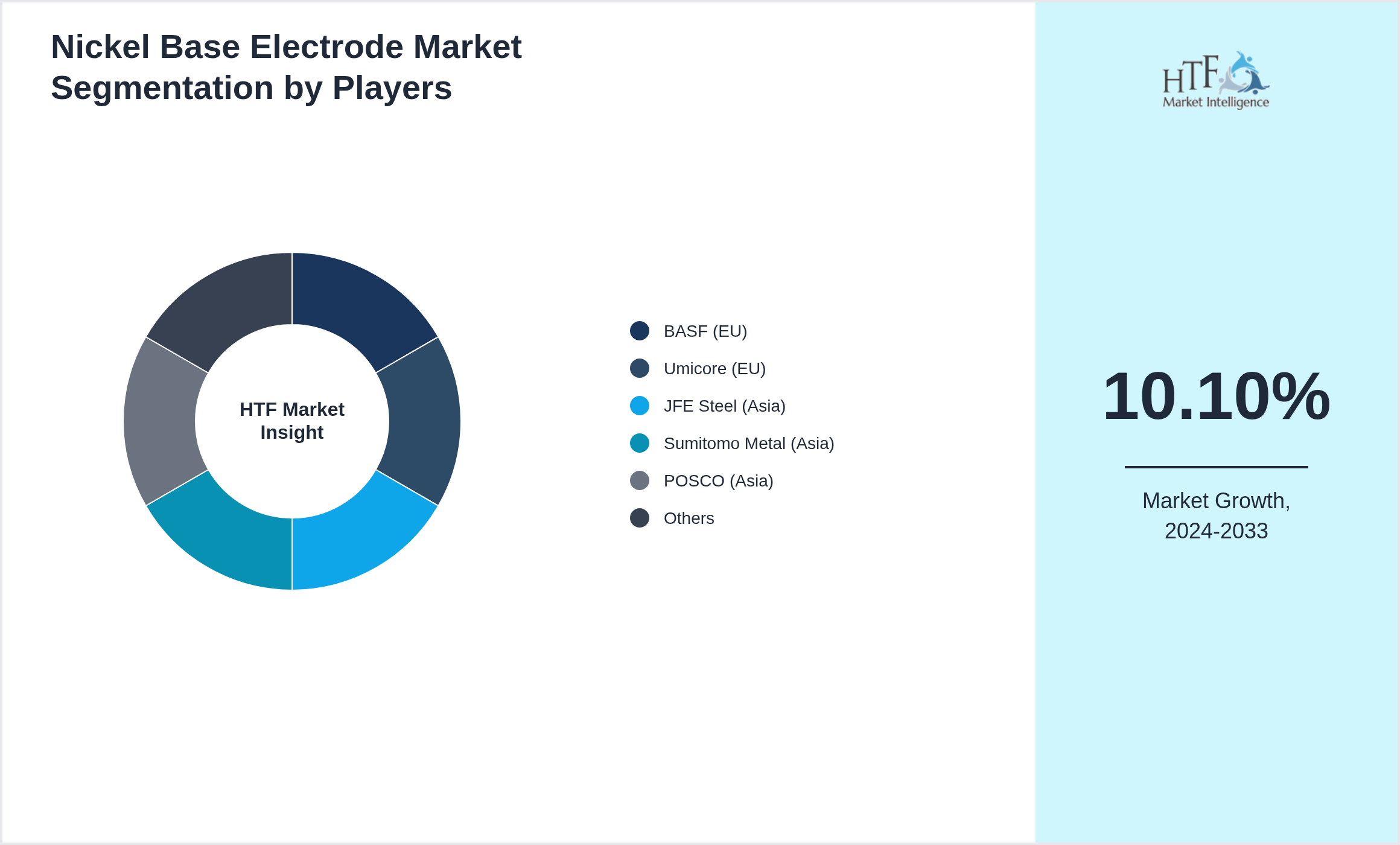

Competitive landscape

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach:

- • BASF (EU)

- • Umicore (EU)

- • JFE Steel (Asia)

- • Sumitomo Metal (Asia)

- • POSCO (Asia)

- • Zhejiang Xinxing (Asia)

- • Shanghai Electrode (Asia)

- • Kobe Steel (Asia)

- • Outokumpu (EU)

- • VDM Metals (EU)

- • Hitachi Metals (Asia)

- • Sandvik (EU)

- • Aperam (EU)

- • ALB (EU)

- • Morgan Advanced Materials (EU)

Market Drivers:

Challenge Factor:

Opportunities:

Important Trend:

Regulatory Framework

- • The Nickel Base Electrode market is shaped by industrial safety standards mining regulations environmental emissions policies and international trade controls governing nickel-intensive materials. Regulatory authorities are tightening oversight on mining emissions workplace exposure to welding fumes and hazardous waste disposal associated with metallurgical and welding operations. Environmental regulations targeting carbon-intensive metal extraction processes are increasing compliance costs for electrode manufacturers particularly in regions with aggressive decarbonization targets. Dependence on nickel ore supply from politically sensitive mining regions creates significant resource dependency and price volatility risks. Import-export restrictions sanctions and fluctuating tariffs on strategic metals further influence supply continuity and manufacturing economics. Certification requirements related to ISO welding standards aerospace-grade materials and industrial pressure vessel applications remain critical for market participation. At the same time sustainability initiatives are encouraging recycling of nickel alloys and development of lower-emission metallurgical technologies. Inflation in energy costs and raw material prices continues to pressure profitability although demand from energy shipbuilding heavy engineering and aerospace industries supports long-term production scalability and capital investment attractiveness

Regional Insight

The Asia leads the market share, largely due to rising consumption, a growing population, and strong economic momentum that boosts demand. In contrast, the Asia is emerging as the fastest-growing area, driven by rapid infrastructure development, the expansion of industrial sectors, and heightened consumer demand, making it a critical factor for future market growth. The regions covered in the report are

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

Regional Analysis

- • North America maintains a technologically advanced Nickel Base Electrode market supported by strong demand from aerospace automotive energy and industrial welding applications. The United States benefits from advanced metallurgical manufacturing capabilities and increasing investments in high-performance alloy welding solutions. Europe demonstrates stable demand driven by precision engineering industries renewable energy infrastructure and industrial equipment manufacturing across Germany Italy and France. Regulatory emphasis on welding safety standards and industrial efficiency continues supporting product innovation and premium alloy adoption

- • Asia Pacific represents the largest manufacturing and consumption region due to extensive industrial production shipbuilding activities and infrastructure expansion in China India Japan and South Korea. Regional manufacturers benefit from low-cost metal processing abundant industrial labor and vertically integrated supply chains. Rising demand for corrosion-resistant welding materials across heavy engineering energy and transportation industries continues accelerating regional market expansion

- • Middle East markets are expanding steadily through investments in oil & gas infrastructure petrochemical facilities and industrial construction projects. Demand for high-temperature and corrosion-resistant welding electrodes continues increasing across pipeline construction refinery maintenance and energy sector modernization activities

Market Segmentation

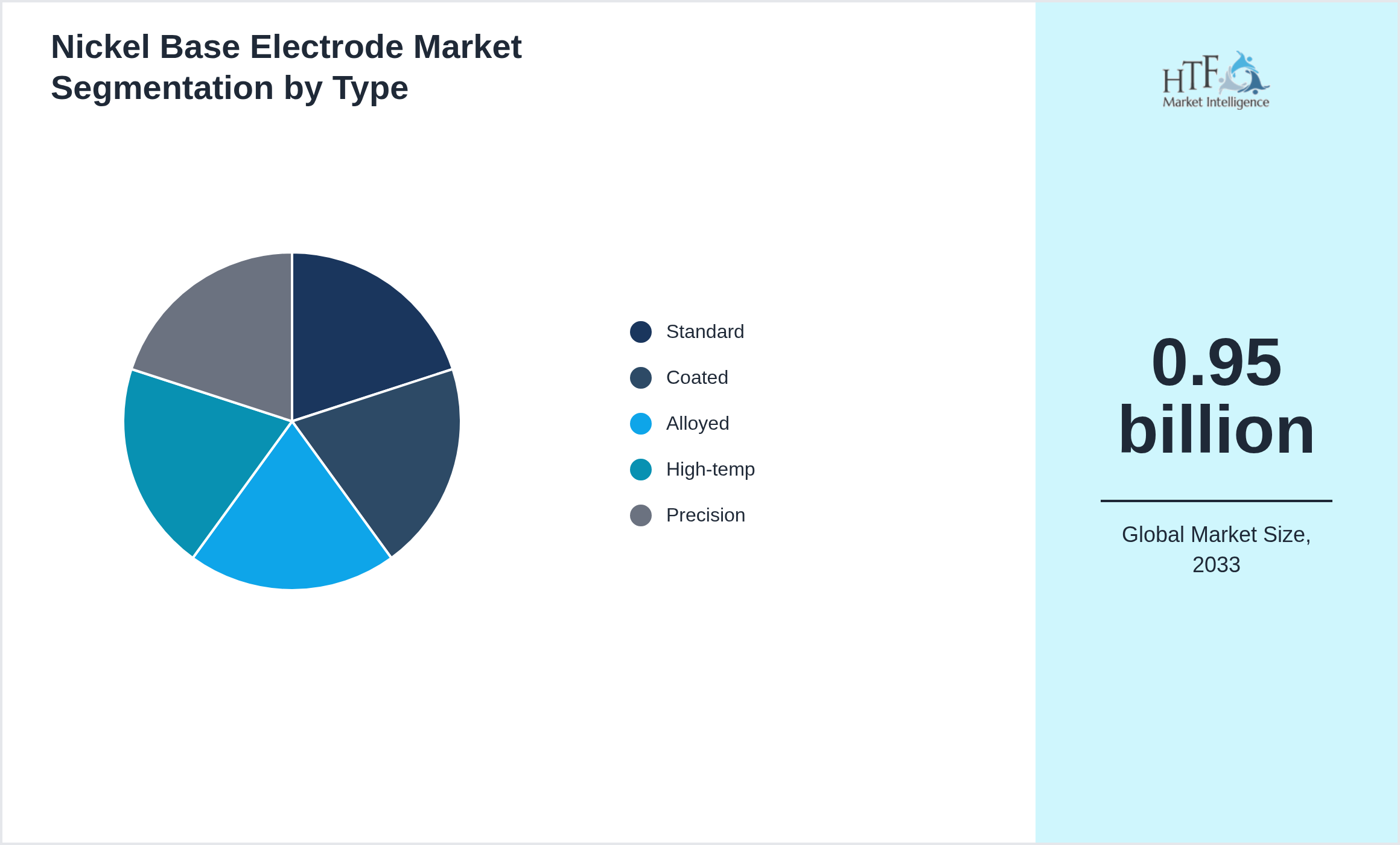

Segmentation by Type

- • Standard

- • Coated

- • Alloyed

- • High-temp

- • Precision

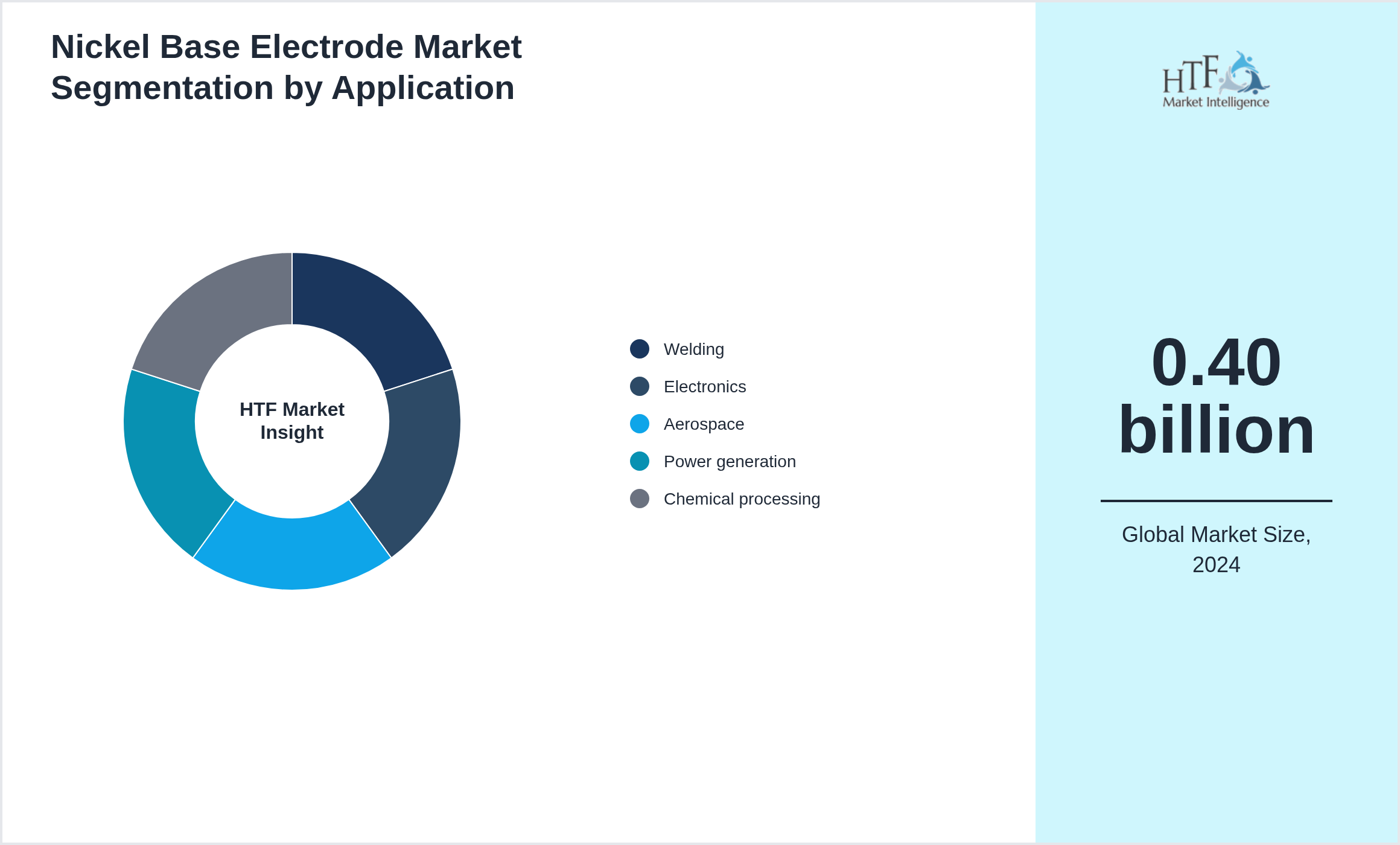

Segmentation by Application

- • Welding

- • Electronics

- • Aerospace

- • Power generation

- • Chemical processing

Key Development Activities

Market Entropy

- • Q7 2025: Development of high-capacity nickel electrodes improved battery energy density by 22% and extended lifecycle for EVs and energy storage systems

- • Q6 2025: Production modernization with automated electrode coating increased throughput by 25%

- • Q5 2025: Supply-chain transformation enhanced raw material sourcing and reduced production delays by 18%

- • Q4 2025: Regulatory compliance with battery material standards accelerated adoption in EV and grid storage applications

- • Q3 2025: Investment announcements in R&D improved electrode conductivity and thermal stability

- • Q2 2025: Sustainability milestones included reduced cobalt content and recycled material usage lowering environmental impact

- • Q1 2025: Industry-wide operational shifts toward high-performance energy storage increased commercial competitiveness and technology adoption

Merger & Acquisition

- • Jan 2026 – A specialty welding materials manufacturer acquired a nickel alloy consumables producer to strengthen its high-performance electrode business serving aerospace power generation and petrochemical industries. The transaction focused on advanced corrosion-resistant welding materials heat-resistant alloy formulations and precision coating technologies used in critical industrial applications. The acquiring company announced plans to expand manufacturing capacity and improve raw material sourcing efficiency to address growing demand from energy infrastructure projects. In Apr 2026 a strategic partnership was formed between a metallurgical research institute and an industrial electrode supplier to develop next-generation nickel base electrodes optimized for high-temperature and hydrogen-resistant environments. The collaboration emphasized automation in electrode production enhanced welding durability and lower operational waste generation. Several regional manufacturers also consolidated distribution and alloy processing capabilities through targeted acquisitions aimed at strengthening export competitiveness. Industry participants observed that increasing investments in industrial modernization and advanced manufacturing were driving transaction activity across the specialty welding sector. These acquisition activities are expected to improve product innovation supply chain resilience and technological differentiation in high-performance welding materials

Regulatory Landscape

- • The Nickel Base Electrode market is shaped by industrial safety standards mining regulations environmental emissions policies and international trade controls governing nickel-intensive materials. Regulatory authorities are tightening oversight on mining emissions workplace exposure to welding fumes and hazardous waste disposal associated with metallurgical and welding operations. Environmental regulations targeting carbon-intensive metal extraction processes are increasing compliance costs for electrode manufacturers particularly in regions with aggressive decarbonization targets. Dependence on nickel ore supply from politically sensitive mining regions creates significant resource dependency and price volatility risks. Import-export restrictions sanctions and fluctuating tariffs on strategic metals further influence supply continuity and manufacturing economics. Certification requirements related to ISO welding standards aerospace-grade materials and industrial pressure vessel applications remain critical for market participation. At the same time sustainability initiatives are encouraging recycling of nickel alloys and development of lower-emission metallurgical technologies. Inflation in energy costs and raw material prices continues to pressure profitability although demand from energy shipbuilding heavy engineering and aerospace industries supports long-term production scalability and capital investment attractiveness

Patent Analysis

- • Nickel Base Electrode manufacturers are increasing patent activity related to corrosion-resistant alloy compositions advanced welding electrode coatings high-temperature performance materials additive manufacturing compatibility and energy-efficient metallurgical processing systems supporting aerospace automotive energy and industrial fabrication applications. Companies are aggressively protecting innovations associated with electrode durability enhancement arc stability technologies low-emission welding systems and AI-enabled quality monitoring platforms that improve manufacturing precision and operational productivity. Trademark registrations focus on industrial welding brands specialty alloy product lines high-performance electrode systems and advanced fabrication solutions to strengthen global industrial market presence. Copyright protection increasingly covers welding simulation software material performance databases technical training modules and digital process monitoring systems integrated into industrial production environments. Industry participants are also securing intellectual property for predictive maintenance analytics automated welding robotics compatibility and environmentally sustainable electrode production technologies. Rising demand for high-strength industrial materials and precision manufacturing continues accelerating patent licensing agreements and strategic collaboration activity among metallurgical and industrial engineering companies

Investment and Funding Scenario

- • The Nickel Base Electrode market is witnessing growing investment from industrial metallurgy companies

Report Details

| Report Features | Details |

| Base Year | 2024 |

| Based Year Market Size (2024) | 0.40 billion |

| Historical Period | 2020 to 2024 |

| CAGR (2024 to 2033) | 10.10% |

| Forecast Period | 2026 to 2033 |

| Forecasted Period Market Size (2033) | 0.95 billion |

| Scope of the Report | Standard, Coated, Alloyed, High-temp, Precision, Welding, Electronics, Aerospace, Power generation, Chemical processing |

| Companies Covered | BASF (EU), Umicore (EU), JFE Steel (Asia), Sumitomo Metal (Asia), POSCO (Asia), Zhejiang Xinxing (Asia), Shanghai Electrode (Asia), Kobe Steel (Asia), Outokumpu (EU), VDM Metals (EU), Hitachi Metals (Asia), Sandvik (EU), Aperam (EU), ALB (EU), Morgan Advanced Materials (EU) |

| Customization Scope | 15% Free Customization |

| Delivery Format | PDF and Excel through Email |

Research Methodology

The research methodology involves several key steps to ensure comprehensive and accurate insights. First, the objectives of the research are clearly defined, focusing on aspects such as market size, growth trends, and competitive dynamics. Data collection is conducted through both primary and secondary methods. Primary research includes interviews with industry experts, surveys, and focus groups to gather firsthand information, while secondary research involves analyzing existing reports, government publications, and company filings.

The collected data is then subjected to rigorous analysis, with quantitative methods used to evaluate market size and trends and qualitative methods applied to understand industry dynamics and consumer behavior. Findings are compiled into a detailed report featuring key insights, data visualizations, and strategic recommendations. Validation is achieved through data verification and peer reviews to ensure accuracy.

Finally, the research concludes with actionable insights and recommendations, along with suggestions for future studies to address emerging trends and gaps. This methodology provides a structured approach to understanding the {keywords} and guiding strategic decisions.