Global AI Computing Center Market Scope & Changing Dynamics 2024-2033

Global AI Computing Center Market is segmented by Application (Cloud AI Training, Data Analytics, Deep Learning, NLP, Computer Vision), Type (GPU Cluster, CPU Cluster, AI Supercomputer, Edge AI Center, Hybrid AI Cloud), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

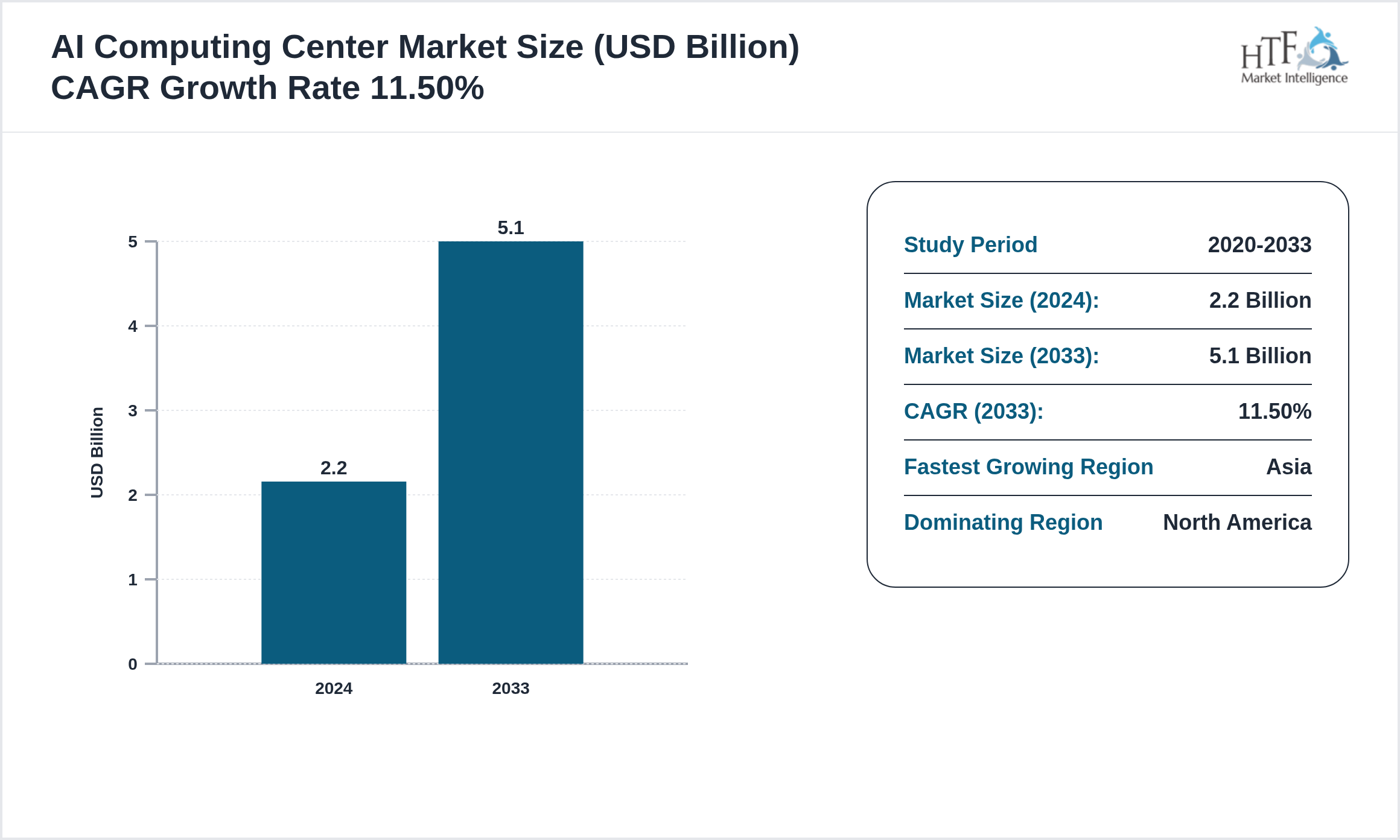

The AI Computing Center market is witnessing significant growth and is expected to expand at a CAGR of 11.50% during the forecast period from 2024 to 2033. This growth is primarily driven by increasing technological advancements, rising consumer demand, and expanding applications across various industries. Businesses are increasingly adopting innovative solutions to improve operational efficiency, enhance customer experiences, and gain a competitive advantage, further fueling market expansion.

Source: HTF Market Intelligence (HTF MI)

AI Computing Center refers to large-scale digital infrastructure facilities designed to support artificial intelligence model training, high-performance computing, deep learning analytics, generative AI workloads, and real-time data processing through advanced GPU clusters, AI accelerators, cloud computing frameworks, and energy-efficient server architectures. These centers integrate high-density data processing units, liquid cooling technologies, AI orchestration software, edge-cloud hybrid systems, and cybersecurity frameworks to deliver scalable computational performance across enterprise, government, healthcare, financial services, and research applications. The market includes hyperscale AI data centers, enterprise AI infrastructure hubs, sovereign AI computing facilities, cloud AI processing ecosystems, and edge AI computing platforms supporting machine learning deployment, autonomous systems, predictive analytics, and digital transformation projects. Rising investments in generative AI, enterprise automation, smart manufacturing, and data-intensive business operations are accelerating commercial demand for advanced AI computing infrastructure globally. Technological advancements include energy-optimized processors, AI workload balancing systems, automated resource orchestration, low-latency networking technologies, and sustainable cooling infrastructure designed to improve processing efficiency and operational scalability. Expansion of cloud ecosystems, national AI development initiatives, and high-performance digital infrastructure modernization is further strengthening long-term market growth and strategic commercial deployment opportunities.

The research study AI Computing Center Market gives readers information on tactical business choices and strategic planning that affect and stabilize the growth prediction in the AI Computing Center market. However, a few disruptive trends will have opposite and significant effects on the distribution among players and the growth of the AI Computing Center market. To give further advice on why certain developments in the AI Computing Center market would have a significant impact and specifically why these trends can be taken into account when determining the market's trajectory and industry participants' strategic plans.

Key Highlights

• The AI Computing Center is growing at a CAGR of 11.50% during the forecasted period of 2024 to 2033

• Year-on-year growth for the market is 11.50%.

• North America dominated the market share in 2024

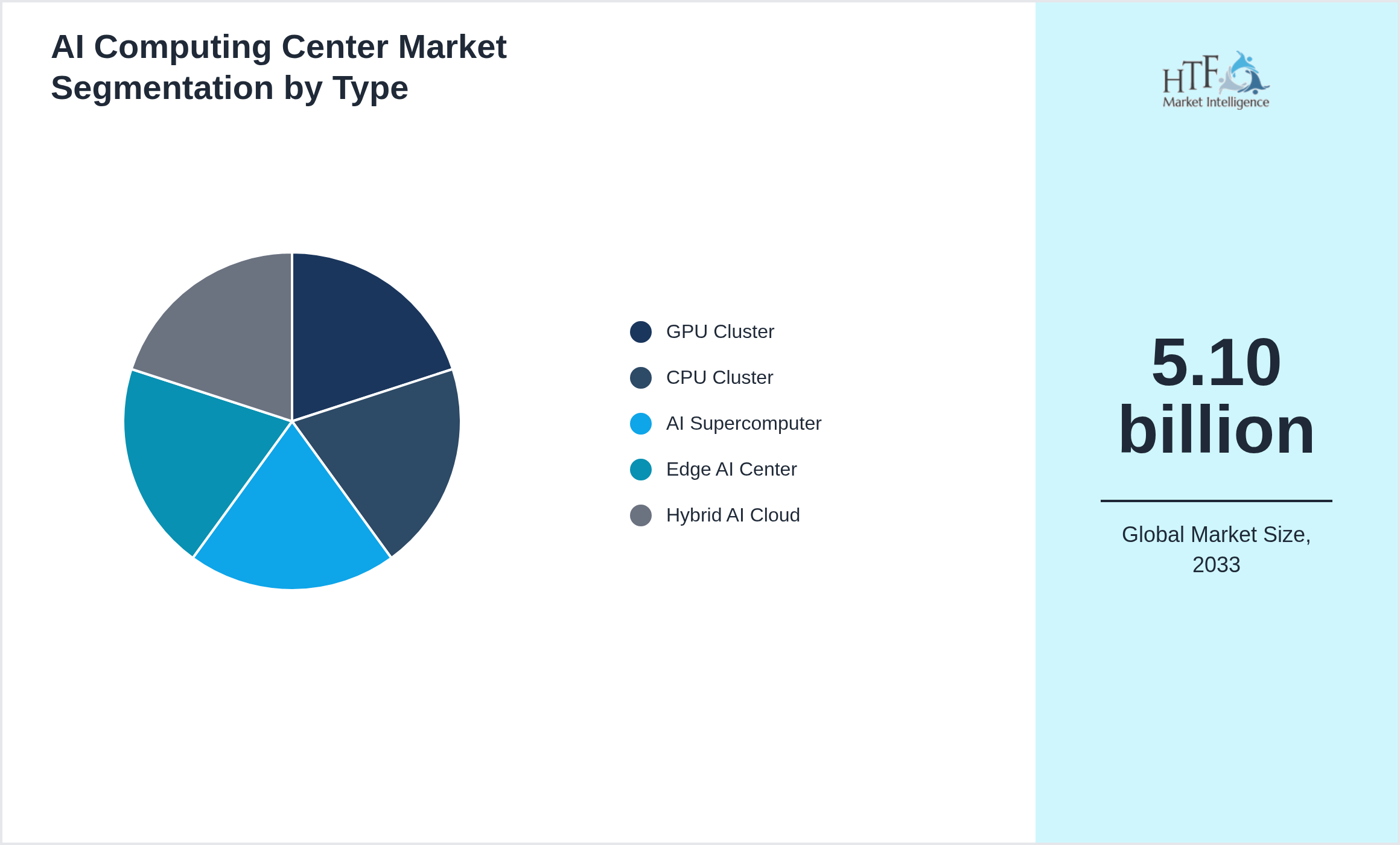

• Based on type, the market is bifurcated into the GPU Cluster, CPU Cluster, AI Supercomputer, Edge AI Center, Hybrid AI Cloud segment, which dominated the market share during the forecasted period

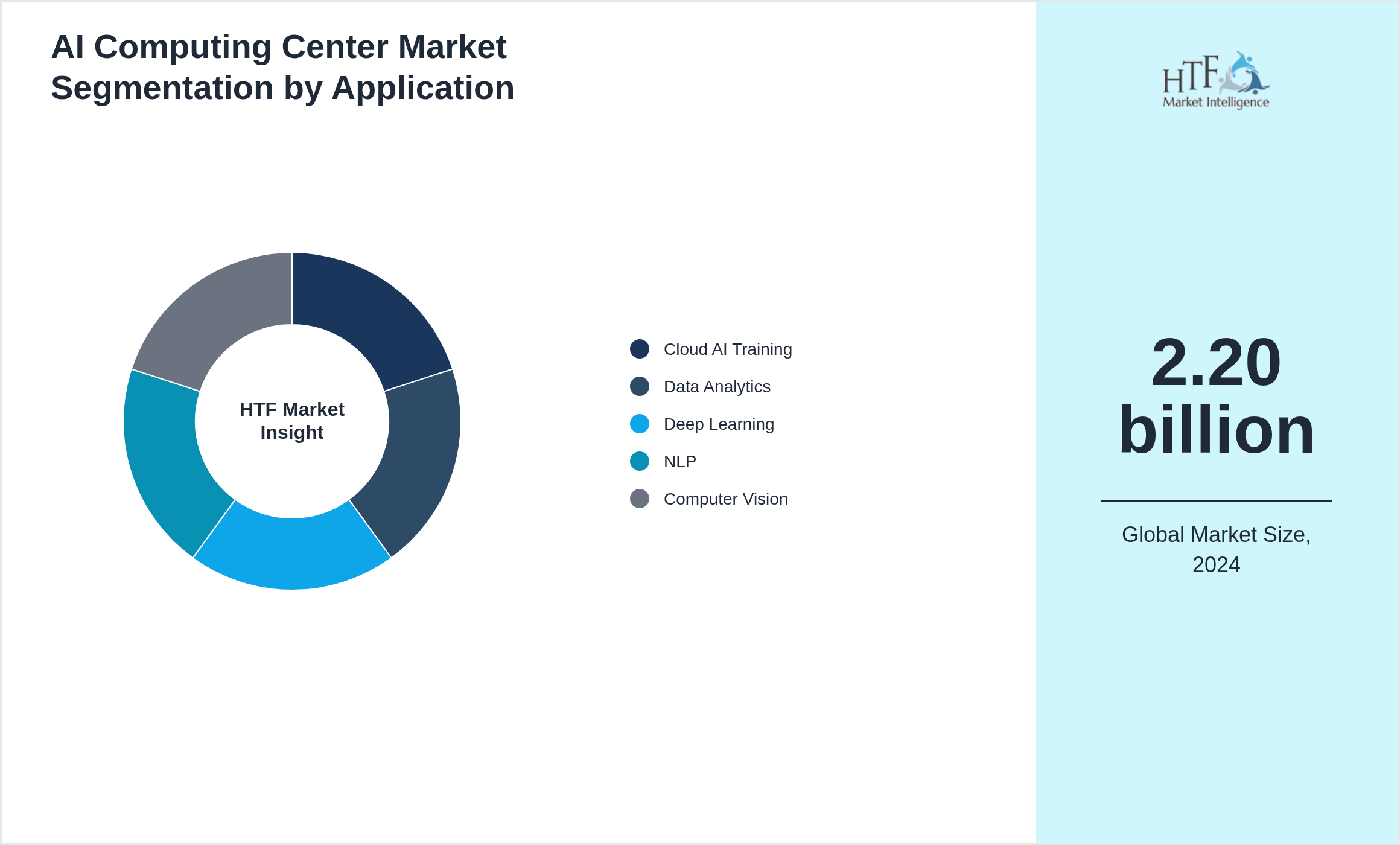

• Based on application, the market is segmented into Application Cloud AI Training, Data Analytics, Deep Learning, NLP, Computer Vision as the fastest-growing segment.

• North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA import/export in terms of K tons, K units, and metric tons will be provided if applicable, based on industry best practices.

Market Dynamics Highlighted

Market Driver

The AI Computing Center market is experiencing significant growth due to various factors.

- • Rising adoption of artificial intelligence technologies exponential growth in enterprise data generation and increasing demand for high-performance computing infrastructure strongly drive the AI Computing Center market. Enterprises governments and research institutions increasingly invest in dedicated AI computing facilities to support machine learning training generative AI applications and advanced data analytics workloads. Expansion of cloud computing services autonomous systems and smart city projects further accelerates demand for scalable AI processing environments globally

Market Trend

The AI Computing Center market is growing rapidly due to various factors.

- • GPU acceleration liquid cooling systems and energy-efficient data center architectures are major trends shaping the AI Computing Center market. Operators increasingly integrate AI-driven workload optimization automated infrastructure management and advanced cybersecurity systems to improve operational efficiency. Edge AI processing capabilities modular computing infrastructure and sustainable renewable-powered data centers gain strong traction across enterprise and hyperscale deployments. Semiconductor innovation high-speed networking technologies and quantum-inspired computing research continue accelerating computational performance and scalability improvements

Opportunity

The AI Computing Center has several opportunities, particularly in developing countries where industrialization is growing.

Challenge

The market for fluid power systems faces several obstacles despite its promising growth possibilities.

AI Computing Center Market Segment Highlighted

Segmentation by Type

- • GPU Cluster

- • CPU Cluster

- • AI Supercomputer

- • Edge AI Center

- • Hybrid AI Cloud

Segmentation by Application

- • Cloud AI Training

- • Data Analytics

- • Deep Learning

- • NLP

- • Computer Vision

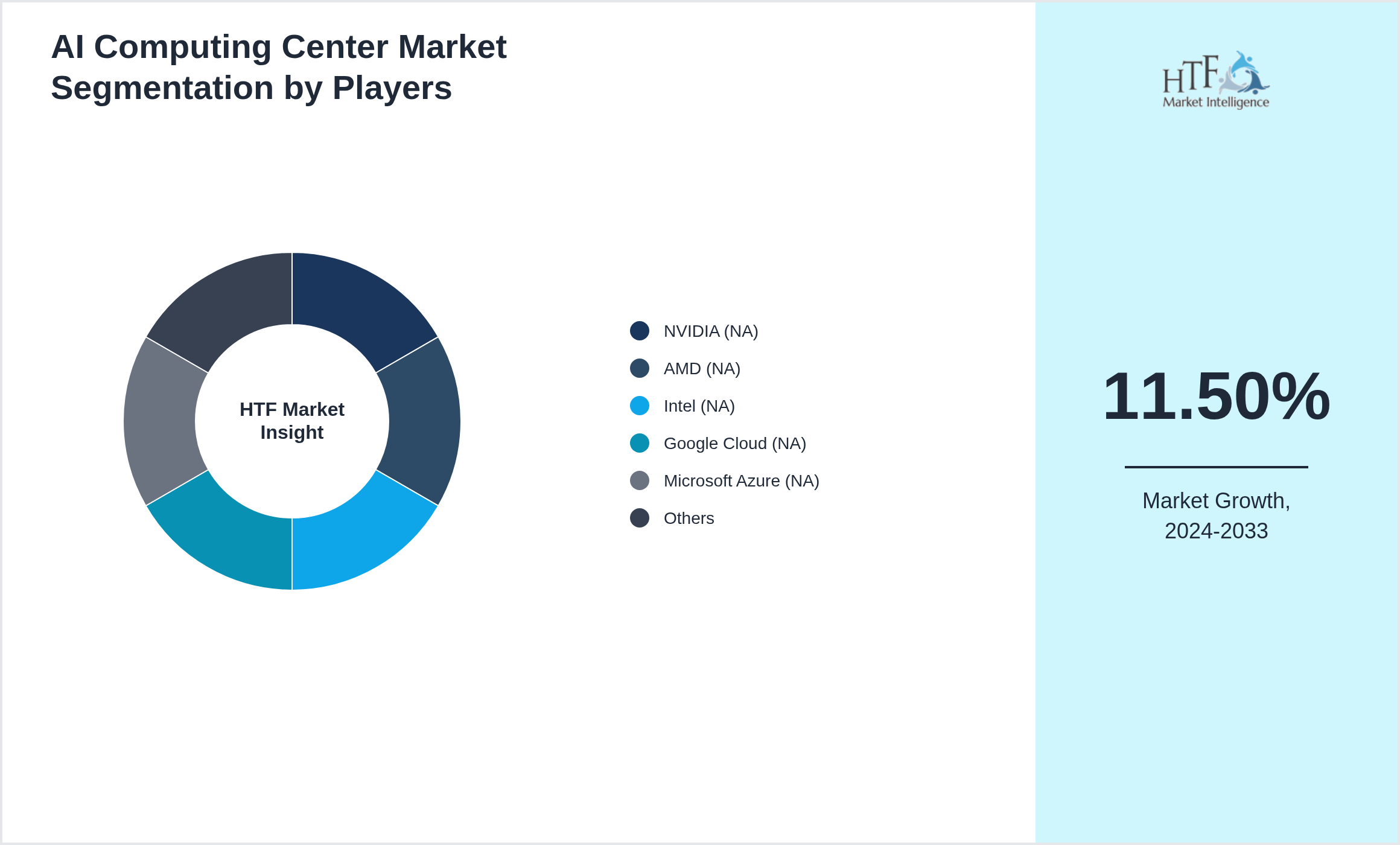

Key Players

The companies featured in this profile were selected based on insights from primary experts, evaluating their market penetration, product offerings, and geographical reach. By targeting emerging markets, these companies aim to leverage new opportunities, enhance their competitive advantage, and drive revenue growth. This approach not only aligns with their overall business objectives but also positions them to respond effectively to the evolving demands of consumers in these regions. Several key players in the AI Computing Center market are strategically focusing on expanding their operations in developing regions to capture a larger market share, particularly as the year-on-year growth rate for the market stands at 11.50%.

- • NVIDIA (NA)

- • AMD (NA)

- • Intel (NA)

- • Google Cloud (NA)

- • Microsoft Azure (NA)

- • Amazon AWS (NA)

- • Huawei Cloud (Asia)

- • Baidu Cloud (Asia)

- • Alibaba Cloud (Asia)

- • Lenovo (Asia)

- • IBM (NA)

- • Dell (NA)

- • Fujitsu (Asia)

- • Oracle Cloud (NA)

- • Cisco (NA)

Regional Insight

The North America dominant region currently dominates the market share, fueled by increasing consumption, population growth, and sustained economic progress, which collectively enhance market demand. Conversely, the Asia is growing rapidly, driven by significant infrastructure investments, industrial expansion, and rising consumer demand.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

- • North America dominates the AI Computing Center market through large-scale hyperscale data center infrastructure strong cloud computing ecosystems and aggressive investments in generative AI and high-performance computing technologies. The United States contributes the majority of regional market value due to the presence of global cloud service providers AI software developers and semiconductor companies. Rapid enterprise adoption of machine learning workloads GPU acceleration platforms and edge AI processing continues driving large-scale infrastructure expansion. Federal investments in AI research and digital infrastructure further strengthen long-term commercial growth opportunities

- • Europe demonstrates increasing investment momentum in AI Computing Center infrastructure driven by digital sovereignty initiatives enterprise AI deployment and regional cloud computing expansion. Germany France and the Nordic countries lead infrastructure development through energy-efficient data center construction and government-supported AI innovation programs. Regulatory emphasis on data privacy cybersecurity and sustainable computing practices significantly influences infrastructure modernization strategies. Demand for localized AI processing capabilities and sovereign cloud platforms continues creating commercial opportunities for advanced computing providers

- • Asia Pacific represents the fastest-growing AI Computing Center market due to rapid digitalization strong semiconductor manufacturing ecosystems and large-scale AI adoption across industries. China Japan South Korea Singapore and India continue investing heavily in hyperscale computing facilities AI model training infrastructure and advanced GPU clusters. Expanding cloud services smart manufacturing initiatives and government-backed AI transformation programs continue accelerating demand for high-capacity computing infrastructure. Competitive energy costs extensive fiber connectivity and strong electronics manufacturing ecosystems provide substantial regional advantages for long-term market scalability

- • Middle East markets are increasingly investing in AI Computing Centers through smart city programs sovereign cloud initiatives and digital economy diversification strategies. Gulf economies continue developing advanced data center ecosystems supported by government-backed AI innovation policies creating strong commercial opportunities for international cloud infrastructure and AI hardware providers

Market Entropy

Merger & Acquisition

- • Feb 2026 – A hyperscale cloud infrastructure provider acquired a regional AI data center operator to strengthen its AI computing center capabilities and expand GPU-intensive cloud services across enterprise markets. The acquisition included advanced liquid cooling infrastructure high-density server architecture and AI workload optimization technologies designed for generative AI and large language model training applications. The acquiring company announced multi-billion-dollar investments to scale energy-efficient AI computing clusters and improve data processing efficiency. In Aug 2026 a strategic joint venture was formed between a telecommunications company and an AI chip manufacturer to establish next-generation edge AI computing centers supporting low-latency industrial applications. Several regional colocation providers also consolidated operations to secure power supply agreements and improve high-performance computing infrastructure availability. Industry experts noted that rapid growth in enterprise AI adoption was intensifying acquisition and partnership activity across the data center sector. These developments are expected to improve computational scalability strengthen cloud AI infrastructure and accelerate deployment of enterprise-grade AI services

Patent Analysis

- • AI Computing Center providers are rapidly building intellectual property portfolios around hyperscale computing architectures AI accelerator infrastructure distributed GPU cluster management systems energy-efficient data center technologies and cloud-native AI orchestration platforms supporting large-scale machine learning workloads. Patent filings increasingly target liquid cooling technologies workload optimization algorithms high-speed interconnect systems AI-specific semiconductor integration predictive power management systems and edge-cloud computing synchronization designed to improve computational efficiency and scalability. Technology firms also register trademarks for AI cloud platforms enterprise computing ecosystems generative AI infrastructure services and intelligent data processing environments aimed at government and enterprise customers. Copyright activity is highly concentrated around AI training frameworks orchestration software cybersecurity systems digital twin infrastructure models and proprietary workload management dashboards. Industry participants actively secure legal protections for proprietary AI compiler technologies resource allocation systems and advanced neural network deployment platforms. Rising enterprise demand for generative AI and sovereign AI infrastructure continues accelerating cross-border partnerships licensing agreements and infrastructure-related patent competition

Investment and Funding Scenario

- • Investment in the AI Computing Center market has surged significantly as enterprises

Report Infographics

| Report Features | Details |

| Base Year | 2024 |

| Based Year Market Size (2024) | 2.20 billion |

| Historical Period | 2020 to 2024 |

| CAGR (2024 to 2033) | 11.50% |

| Forecast Period | 2026 to 2033 |

| Forecasted Period Market Size (2033) | 5.10 billion |

| Scope of the Report |

By Type, By Application, By Region |

| Companies Covered | NVIDIA (NA), AMD (NA), Intel (NA), Google Cloud (NA), Microsoft Azure (NA), Amazon AWS (NA), Huawei Cloud (Asia), Baidu Cloud (Asia), Alibaba Cloud (Asia), Lenovo (Asia), IBM (NA), Dell (NA), Fujitsu (Asia), Oracle Cloud (NA), Cisco (NA) |

| Customization Scope | 15% Free Customization

Want to Buy Specific Sections of This Report?

|

| Delivery Format | PDF and Excel through Email |

The Top-Down and Bottom-Up Approaches

The top-down approach begins with a broad theory or hypothesis and breaks it down into specific components for testing. This structured, deductive process involves developing a theory, creating hypotheses, collecting and analyzing data, and drawing conclusions. It is particularly useful when there is substantial theoretical knowledge, but it can be rigid and may overlook new phenomena.

Conversely, the bottom-up approach starts with specific data or observations, from which broader generalizations and theories are developed. This inductive process involves collecting detailed data, analyzing it for patterns, developing hypotheses, formulating theories, and validating them with additional data. While this approach is flexible and encourages the discovery of new phenomena, it can be time-consuming and less structured.

Regulatory Framework

The healthcare sector is overseen by various regulatory bodies that ensure the safety, quality, and efficacy of health services and products. In the United States, the U.S. Department of Health and Human Services (HHS) plays a crucial role in protecting public health and providing essential human services. Within HHS, the Food and Drug Administration (FDA) regulates food, drugs, and medical devices, ensuring they meet safety and efficacy standards. The Centers for Disease Control and Prevention (CDC) focuses on disease control and prevention, conducting research, and providing health information to protect public health.