Global Takaful Insurance Market - Global Outlook 2021-2033

Global Takaful Insurance Market is segmented by Application (Life Protection, Health Coverage, Property Insurance, Business Insurance, Personal Finance), Type (Family Takaful, General Takaful, Health Takaful, Motor Takaful, Micro Takaful), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

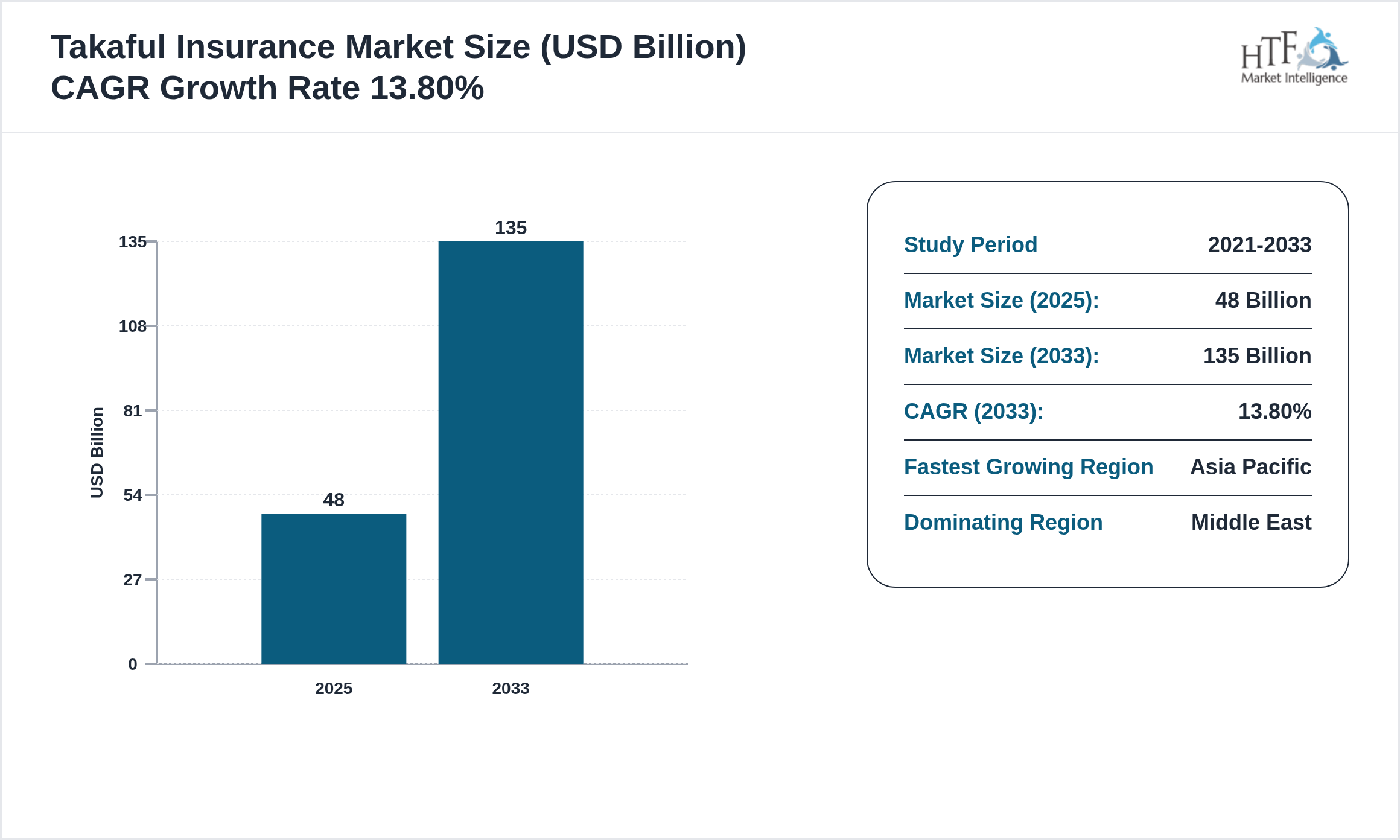

The Takaful Insurance market is expected to reach 135.00 billion by 2033 and is growing at a CAGR of13.80% between 2025 and 2033.

Takaful insurance Market is a cooperative insurance system based on Islamic principles where participants contribute to a pooled fund to support each other in case of loss or damage. Unlike conventional insurancetakaful operates on the concept of mutual assistance and shared responsibilityavoiding elements such as interest (riba) and uncertainty (gharar). The model ensures that policyholders share risks collectively while the operator manages the fund for a fee. Takaful products include familyhealthand general insurance solutions tailored to Sharia compliance. The market is driven by increasing demand for ethical and faith-based financial productsespecially in Muslim-majority regions. With digital transformation and fintech integrationtakaful insurance is expanding globallyoffering inclusive financial protection solutions and supporting sustainable financial ecosystems

Source: HTF Market Intelligence (HTF MI)

Market Size & Forecast

Market Segmentation

Selecting segmentation criteria in Takaful Malaysia (Malaysia), Salama Islamic Arab Insurance (UAE), Qatar Islamic Insurance (Qatar), Dubai Islamic Insurance & Reinsurance (UAE), Abu Dhabi National Takaful (UAE), Allianz Takaful (Germany), Prudential BSN Takaful (Malaysia), Etiqa Takaful (Malaysia), Al Rajhi Takaful (Saudi Arabia), Watania Takaful (UAE), Noor Takaful (UAE), Pak-Qatar Takaful (Pakistan), Jubilee General Takaful (Pakistan), Islamic Insurance Company (Jordan), Dar Al Takaful (UAE), Takaful Emarat (UAE), Gulf Takaful (Kuwait), Solidarity Group (Bahrain), SALAMA Cooperative Insurance (Saudi Arabia), AXA Takaful (France) involves several key steps. Researchers begin by defining their objectives, such as understanding consumer behavior or identifying market opportunities. They then gather relevant data on demographics, psychographics, and buying behavior. Next, they identify segmentation variables like age, location, lifestyle, and purchase patterns. Using analytical tools, they analyze the data to find distinct market segments and evaluate their attractiveness based on size, growth potential, and alignment with business goals. Detailed profiles are created for each segment, and the most promising ones are selected for targeting. Finally, tailored marketing strategies are developed, and the performance of these strategies is monitored and adjusted as needed. This process ensures that segmentation effectively identifies valuable market opportunities and aligns with strategic goals.

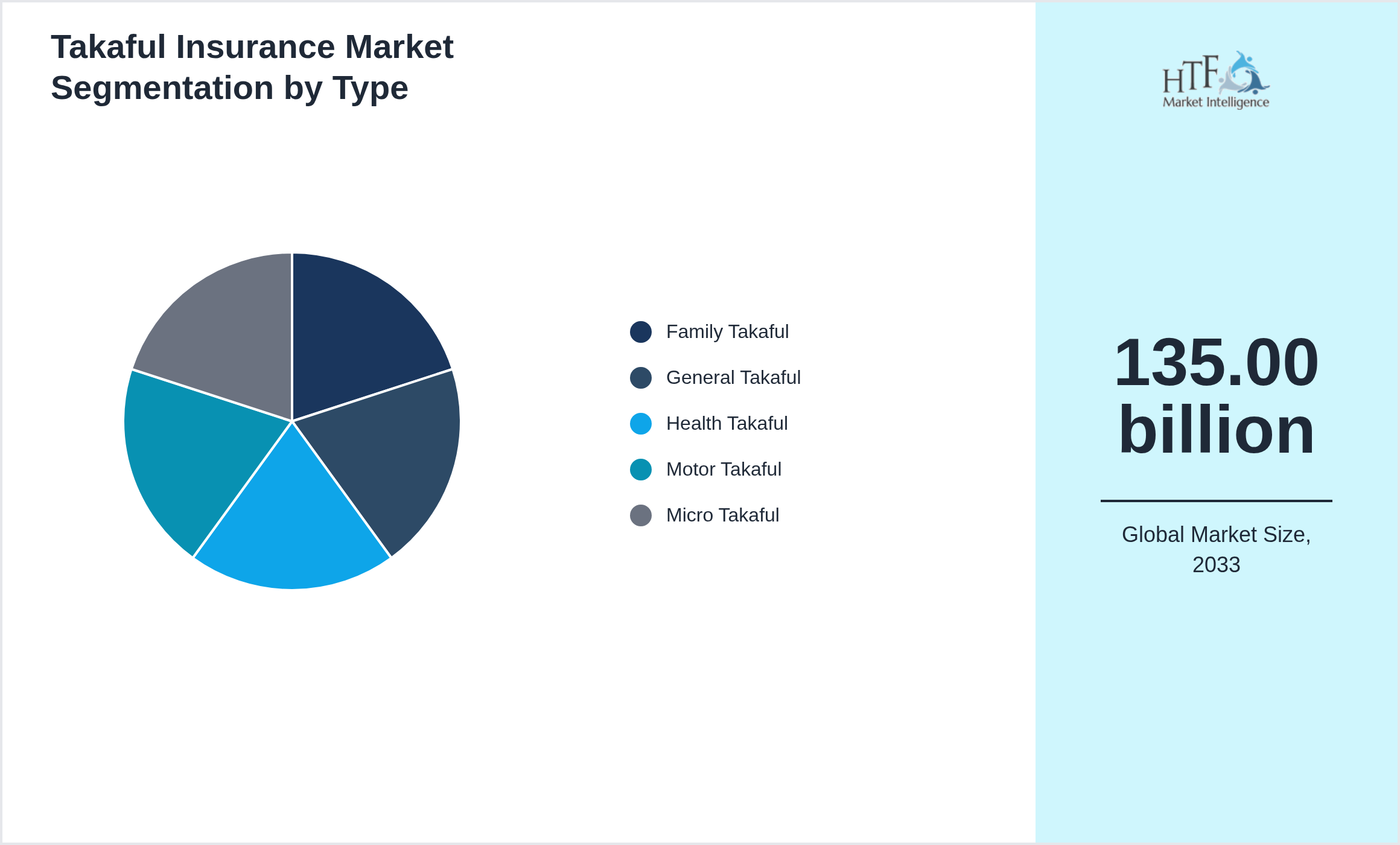

Segmentation by Type

- • Family Takaful

- • General Takaful

- • Health Takaful

- • Motor Takaful

- • Micro Takaful

Segmentation by Application

- • Life Protection

- • Health Coverage

- • Property Insurance

- • Business Insurance

- • Personal Finance

Takaful Insurance Market Dynamics

TheTakaful Insurance is driven by factors such as increasing demand in end-use industries, technological advancements, research and development (R&D), economic growth, and increasing global trade.

Influencing Trend:

- • Digital takaful platforms adoption

- • Integration with Islamic fintech solutions

- • Customized micro takaful offerings

- • Growth in health and family takaful products

- • Partnerships with banks and fintech firms

- • Rising demand for Sharia-compliant financial products

- • Increasing Muslim population globally

- • Government support for Islamic finance

- • Growing awareness of ethical insurance models

- • Expansion of Islamic banking ecosystem

- • Regulatory inconsistencies across regions

- • Lack of awareness in some markets

- • Operational complexity in risk-sharing models

- • Competition from conventional insurance

- • Limited standardization in Sharia compliance

- • Expansion in non-Muslim markets seeking ethical finance

- • Growth in emerging economies

- • Product innovation in microinsurance

- • Digital distribution channels

- • Increasing penetration in underserved regions

![Takaful Insurance Market trend by end use applications [Life Protection, Health Coverage, Property Insurance, Business Insurance, Personal Finance]](https://htf-insight.s3.us-east-1.amazonaws.com/generated-charts/chart-pie-and-donut-chart-application-4400455-takaful-insurance-market-1776843101402-1776843104604-a9fe480dacce09d8.png)

Regional Insight

The Middle Eastregion holds a dominant market share, primarily driven by growing consumption patterns, a rising population, and robust economic activity that fuels market demand. Meanwhile, the Asia Pacific Region is experiencing the fastest growth, propelled by increasing infrastructure developments, expanding industrial activities, and a surge in consumer demand, positioning it as a key driver for future market expansion.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

- • The GCC region dominates the Takaful Insurance Market due to strong Islamic finance infrastructure

Key Players

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach:

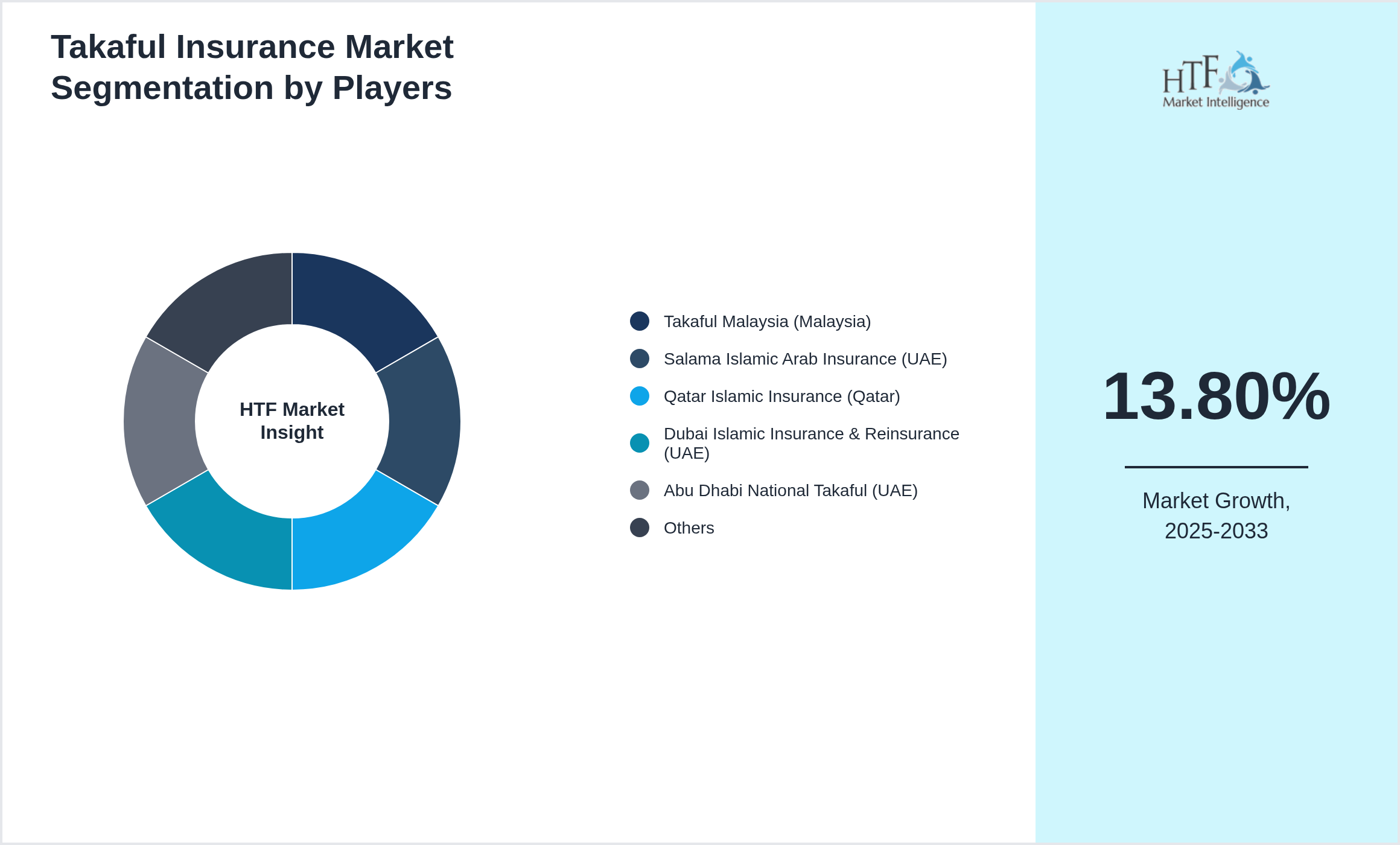

- • Takaful Malaysia (Malaysia)

- • Salama Islamic Arab Insurance (UAE)

- • Qatar Islamic Insurance (Qatar)

- • Dubai Islamic Insurance & Reinsurance (UAE)

- • Abu Dhabi National Takaful (UAE)

- • Allianz Takaful (Germany)

- • Prudential BSN Takaful (Malaysia)

- • Etiqa Takaful (Malaysia)

- • Al Rajhi Takaful (Saudi Arabia)

- • Watania Takaful (UAE)

- • Noor Takaful (UAE)

- • Pak-Qatar Takaful (Pakistan)

- • Jubilee General Takaful (Pakistan)

- • Islamic Insurance Company (Jordan)

- • Dar Al Takaful (UAE)

- • Takaful Emarat (UAE)

- • Gulf Takaful (Kuwait)

- • Solidarity Group (Bahrain)

- • SALAMA Cooperative Insurance (Saudi Arabia)

- • AXA Takaful (France)

Regulatory Framework

The regulatory framework for the Takaful Insurance ensures product safety, fair competition, and consumer protection. It encompasses setting standards for product quality and safety, enforcing truthful advertising and labeling, and implementing environmental sustainability practices. Regulations include robust procedures for product recalls, data protection, and anti-competitive practices, while also overseeing import/export controls and intellectual property rights. Regulatory bodies enforce these rules through inspections and penalties, and consumer education programs help individuals make informed decisions. This framework aims to protect consumers, promote fair market conditions, and encourage ethical business practices.

- • Regulatory frameworks for Takaful insurance are evolving rapidlyparticularly in GCC and Southeast Asia where regulators are strengthening solvency requirementsgovernance standardsand Shariah compliance monitoring. Countries are implementing unified supervisory frameworks to improve transparencyrisk managementand capital adequacy requirements across Islamic financial institutions. Regulatory bodies are also promoting digital insurance regulations to support online policy issuance and automated claims management systems. Emerging markets are gradually introducing dedicated Takaful laws to improve insurance penetration and encourage cross-border participation. Ongoing regulatory modernization is expected to improve consumer confidence and stabilize long-term industry growth.

Competitive Insights

The key players in the Takaful Insurance are intensifying their focus on research and development (R&D) activities to innovate and stay competitive. Major companies, such as Takaful Malaysia (Malaysia), Salama Islamic Arab Insurance (UAE), Qatar Islamic Insurance (Qatar), Dubai Islamic Insurance & Reinsurance (UAE), Abu Dhabi National Takaful (UAE), Allianz Takaful (Germany), Prudential BSN Takaful (Malaysia), Etiqa Takaful (Malaysia), Al Rajhi Takaful (Saudi Arabia), Watania Takaful (UAE), Noor Takaful (UAE), Pak-Qatar Takaful (Pakistan), Jubilee General Takaful (Pakistan), Islamic Insurance Company (Jordan), Dar Al Takaful (UAE), Takaful Emarat (UAE), Gulf Takaful (Kuwait), Solidarity Group (Bahrain), SALAMA Cooperative Insurance (Saudi Arabia), AXA Takaful (France), are heavily investing in R&D to develop new products and improve existing ones. This strategic emphasis on innovation is driving significant advancements in product formulation and the introduction of sustainable and eco-friendly products.

In addition to R&D and acquisitions, there is a notable shift towards green investments among key players in the consumer goods industry. Companies are increasingly committing resources to sustainable practices and the development of environmentally friendly products. This green investment is in response to growing consumer demand for sustainable solutions and stringent environmental regulations. By prioritizing sustainability, these companies are not only contributing to environmental protection but also positioning themselves as leaders in the green movement, thereby fueling market growth.

Merger Acquisition

- • Jan 2024: Allianz Takaful acquired GulfShield Takaful to expand Sharia-compliant risk pooling and underwriting services across the GCC regionstrengthening product offerings in motormedicaland family takaful segments.

- • Sep 2024: Syarikat Takaful Malaysia partnered with Amana Takaful Pakistan to integrate digital distribution platforms and expand cross-border retakaful capacity into ASEAN and South Asian markets.

- • Feb 2025: Dana Takaful PJSC (UAE) merged with Arabia Takaful Group to form one of the largest composite operators in the Middle East and North Africaenhancing capital base and breadth of Sharia-compliant insurance solutions.

Patent Analysis

- • Patent activity in the Takaful Insurance Market is largely driven by digital insurance technology providers developing automated underwriting systemsblockchain-based claims processing platformsand advanced risk analytics tools. InsurTech firms are filing patents focused on distributed ledger technologies that enhance transparency in policy issuance and claims settlement workflows. Innovations in predictive analytics and AI-driven actuarial modeling are improving risk evaluation accuracy and operational efficiency. Cybersecurity-related patents covering digital identity authentication and fraud detection mechanisms are also gaining importance as insurers expand mobile-based and cloud-enabled insurance platforms. Overalldigital transformation technologies remain the primary focus of intellectual property development.

Investment and Funding Scenario

- • Investment activity in the Takaful Insurance Market is expanding as institutional investors and sovereign funds allocate capital toward digitalization and regional expansion strategies. Venture capital funding is increasingly directed toward InsurTech startups that offer Shariah-compliant digital insurance platforms and mobile-based customer engagement solutions. Government-supported Islamic finance institutions are investing heavily in micro-takaful infrastructure to expand coverage across underserved populations. Strategic investments are also supporting technology upgradesproduct innovationand regional market penetration. The growing emphasis on ethical finance and sustainability-driven investments is expected to attract additional funding from global investors seeking long-term growth opportunities.

Market Entropy

- • In 2024: Rising demand for Sharia-compliant financial products increased adoption of takaful insurance across Middle EastAfricaand Southeast Asia markets. Ethical risk-sharing models strengthened consumer trust. Regulatory support in Islamic finance supported market penetration.

- • In 2025: Digital takaful platforms and insurtech integration improved policy accessibility and claims management performance. Micro-takaful products expansion strengthened demand growth among underserved populations. Cross-border Islamic finance innovation supported sustained utilization.

Report Infographics:

| Report Features | Details |

| Base Year | 2025 |

| Based Year Market Size 2025 | 48.00 billion |

| Historical Period Market Size 2021 | USD Million ZZ |

| CAGR (2025 to 2033) | 13.80% |

| Forecast Period | 2025 to2033 |

| Forecasted Period Market Size 2033 | 135.00 billion |

| Scope of the Report | Family Takaful, General Takaful, Health Takaful, Motor Takaful, Micro Takaful, Life Protection, Health Coverage, Property Insurance, Business Insurance, Personal Finance |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Year-on-Year Growth | 11.34% |

| Companies Covered | Takaful Malaysia (Malaysia), Salama Islamic Arab Insurance (UAE), Qatar Islamic Insurance (Qatar), Dubai Islamic Insurance & Reinsurance (UAE), Abu Dhabi National Takaful (UAE), Allianz Takaful (Germany), Prudential BSN Takaful (Malaysia), Etiqa Takaful (Malaysia), Al Rajhi Takaful (Saudi Arabia), Watania Takaful (UAE), Noor Takaful (UAE), Pak-Qatar Takaful (Pakistan), Jubilee General Takaful (Pakistan), Islamic Insurance Company (Jordan), Dar Al Takaful (UAE), Takaful Emarat (UAE), Gulf Takaful (Kuwait), Solidarity Group (Bahrain), SALAMA Cooperative Insurance (Saudi Arabia), AXA Takaful (France) |

| Customization Scope | 15% Free Customization (For EG) |

| Delivery Format | PDF and Excel through Email

Want to Buy Specific Sections of This Report?

|

Research Methodology

The research methodology for the consumer goods industry involves several key steps to ensure comprehensive and actionable insights. First, the research objectives are clearly defined, focusing on aspects like consumer behavior, market opportunities, competitive dynamics, or regulatory impacts. A thorough literature review follows, drawing from academic journals, industry reports, government publications, and market analyses to establish a knowledge base and identify research gaps. Data collection encompasses both primary methods, such as surveys, interviews, and focus groups with consumers and industry experts, and secondary methods, including analysis of market reports, government data, and industry publications. Quantitative data is analyzed using statistical tools to identify patterns and market segments, while qualitative data from interviews and focus groups is examined to extract key themes and insights.

The market is then segmented based on demographics, psychographics, geography, and purchasing behavior, and competitive analysis is conducted to evaluate key players' strategies and strengths. Trend analysis identifies current and emerging industry trends. Findings are compiled into a detailed report with data visualizations and strategic recommendations. The research is validated and refined through cross-checking and expert feedback, and a framework for continuous monitoring is established to keep the research current and relevant.