Drone Payload Release System Industry Growth & Trend Analysis

Global Drone Payload Release System Market is segmented by Application (Medical delivery, Humanitarian drops, SAR supply drops, Agriculture inputs, Industrial spares, E-commerce pilots, Defense logistics, Disaster relief), Type (Servo-dropper, Winch/tether release, Multi-payload bay, Precision guided drop, Medical delivery pods, Agriculture dispersal, Search & rescue drop kits, Defense-certified release units), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Key Values Provided by a Drone Payload Release System Market

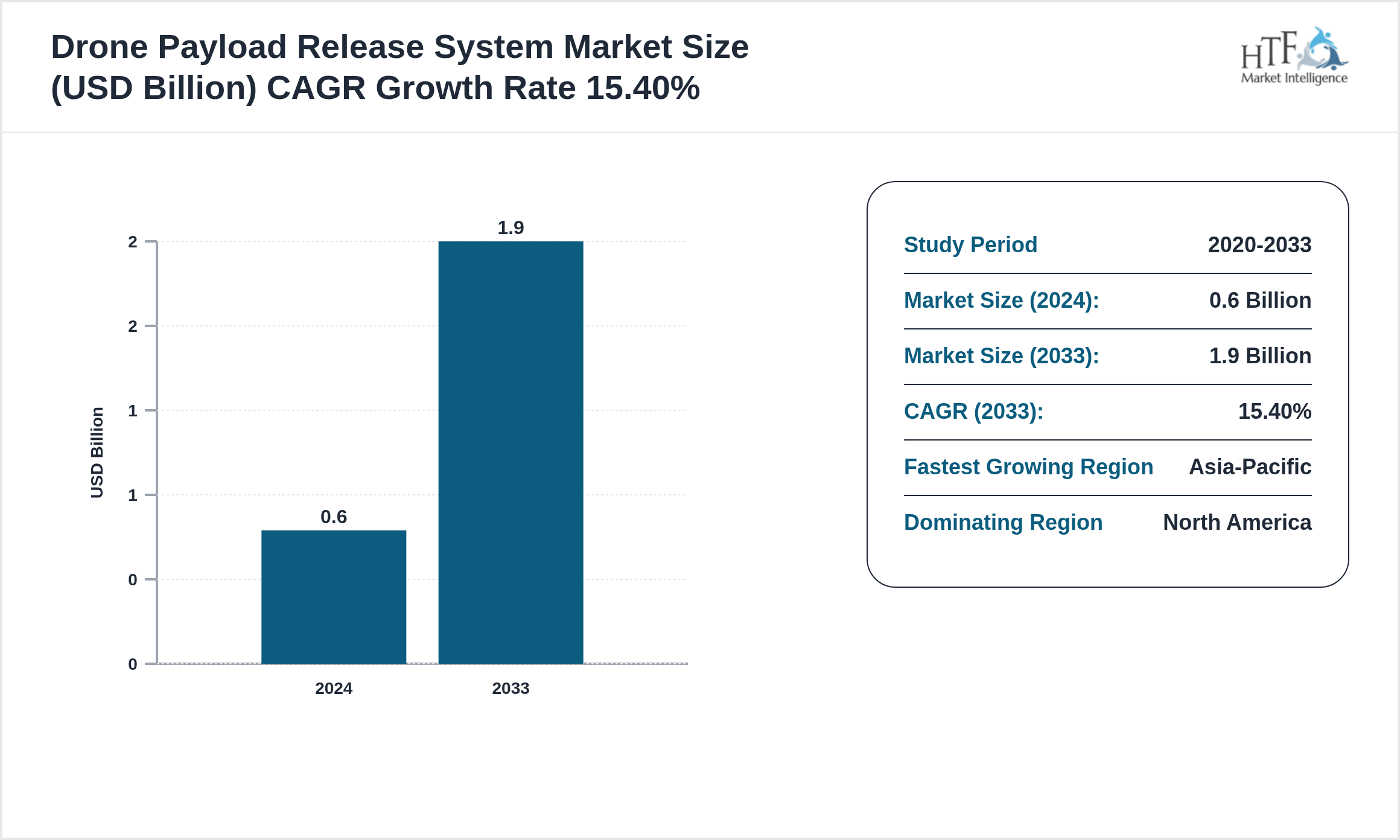

The Drone Payload Release System market was valued at 0.60 billion in 2024 and is expected to reach 1.90 billion by 2020, growing at a compound annual growth rate (CAGR) of 15.40% over the forecast period.

Drone payload release systems are mechanical/electro-mechanical modules that securely carry and deploy payloads (drops winches pods) from UAVs with controlled triggering and safety redundancies. They support logistics emergency response agriculture and defense use-cases requiring reliable release timing and payload integrity.

Source: HTF Market Intelligence (HTF MI)

A Drone Payload Release System market research study provides invaluable data-driven insights that allow businesses to make informed decisions based on accurate market trends, customer behaviors, and competitor analysis. These reports help organizations better understand the evolving needs of their target audience, enabling more customer-focused strategies.

Market Dynamics

Influencing Trend:

- • Smart release with sensors geofenced drop approval standardized payload interfaces lighter composite mechanisms and certification-ready designs for regulated airspace.

- • Beyond-visual-line operations emergency response needs defense modernization and last-mile delivery pilots push payload release hardware that is safe redundant and auditable.

- • Regulatory approvals safety liability payload stability in wind interoperability across drones and cybersecurity risks in command links slow commercial scaling.

- • Serviceable modular payload bays partnerships with logistics/healthcare and retrofit kits for popular drone platforms expand TAM and enable recurring service revenue.

The North America Dominant Region currently dominates the market share, fueled by increasing consumption, population growth, and sustained economic progress, which collectively enhance market demand. Conversely, the {FASTEST GROWING REGION} is rapidly becoming the fastest-growing region, driven by significant infrastructure investments, industrial expansion, and rising consumer demand.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

Competitive Insights

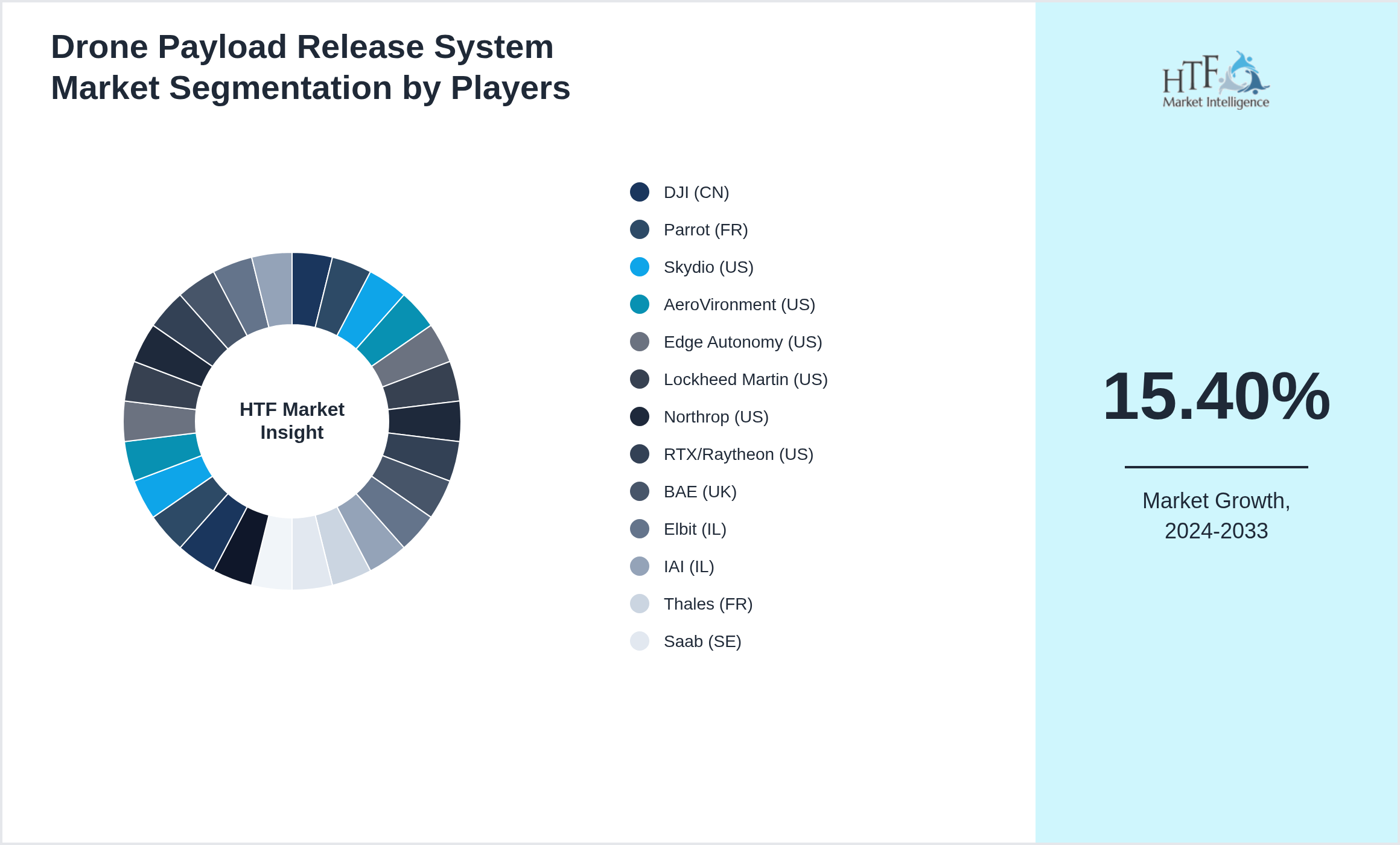

The key players in the Drone Payload Release System are intensifying their focus on research and development (R&D) activities to innovate and stay competitive. Major companies, such as DJI (CN), Parrot (FR), Skydio (US), AeroVironment (US), Edge Autonomy (US), Lockheed Martin (US), Northrop (US), RTX/Raytheon (US), BAE (UK), Elbit (IL), IAI (IL), Thales (FR), Saab (SE), Leonardo (IT), Quantum-Systems (DE), Autel (CN), Draganfly (CA), Yuneec (CN), Gremsy (VN), Elistair (FR), Teledyne FLIR (US), Moog (US), Curtiss-Wright (US), Hexagon (SE), Sierra-Olympia (US), Flyability (CH), are heavily investing in R&D to develop new products and improve existing ones. This strategic emphasis on innovation drives significant advancements in product formulation and the introduction of sustainable and eco-friendly products.

Moreover, these established industry leaders are actively pursuing acquisitions of smaller companies to expand their regional presence and enhance their market share. These acquisitions not only help in diversifying their product portfolios but also provide access to new technologies and markets. This consolidation trend is a critical factor in the growth of the consumer goods industry, as it enables larger companies to streamline operations, reduce costs, and increase their competitive edge.

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach:

- • DJI (CN)

- • Parrot (FR)

- • Skydio (US)

- • AeroVironment (US)

- • Edge Autonomy (US)

- • Lockheed Martin (US)

- • Northrop (US)

- • RTX/Raytheon (US)

- • BAE (UK)

- • Elbit (IL)

- • IAI (IL)

- • Thales (FR)

- • Saab (SE)

- • Leonardo (IT)

- • Quantum-Systems (DE)

- • Autel (CN)

- • Draganfly (CA)

- • Yuneec (CN)

- • Gremsy (VN)

- • Elistair (FR)

- • Teledyne FLIR (US)

- • Moog (US)

- • Curtiss-Wright (US)

- • Hexagon (SE)

- • Sierra-Olympia (US)

- • Flyability (CH)

Key Highlights

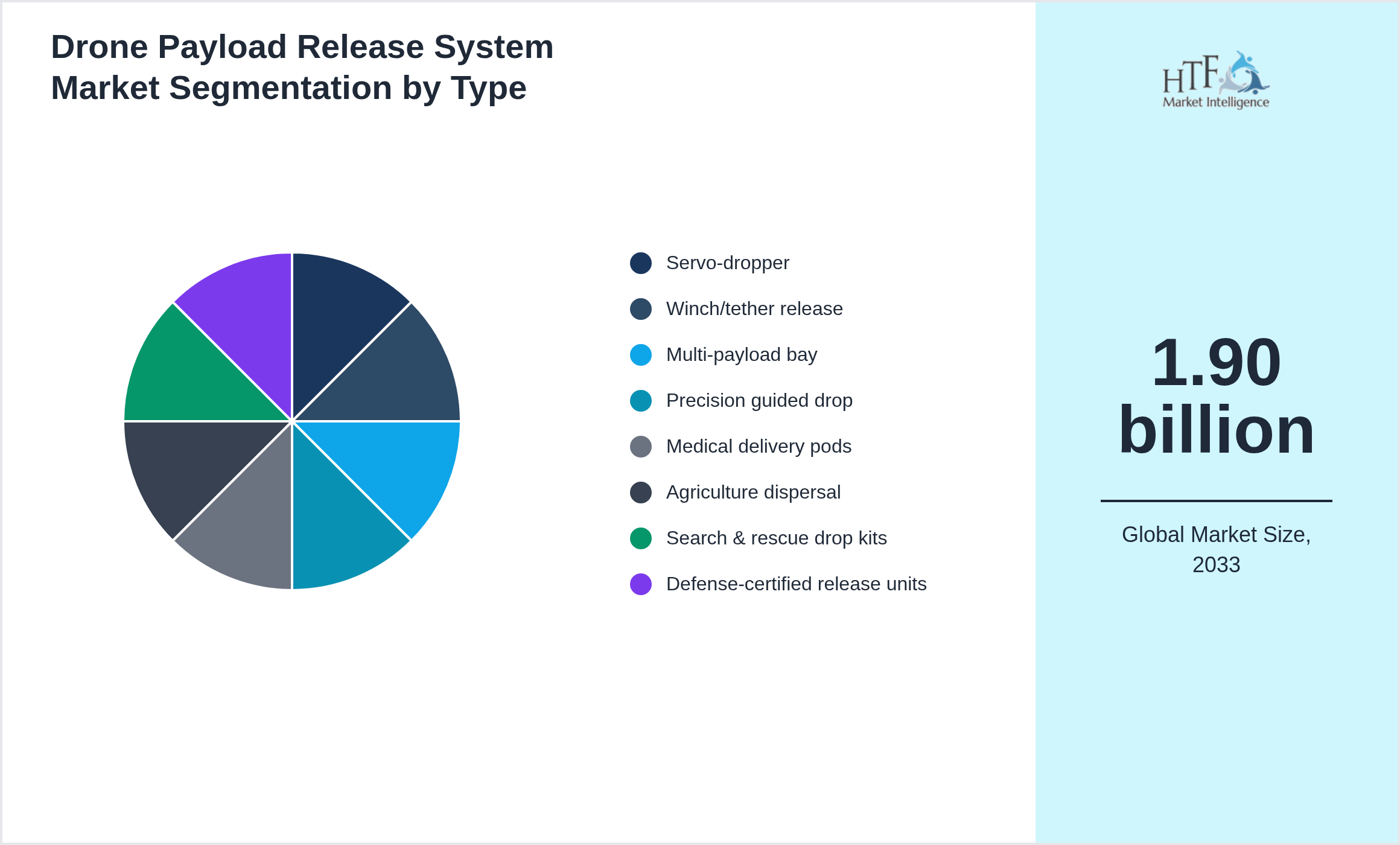

Segmentation by Type

- • Servo-dropper

- • Winch/tether release

- • Multi-payload bay

- • Precision guided drop

- • Medical delivery pods

- • Agriculture dispersal

- • Search & rescue drop kits

- • Defense-certified release units

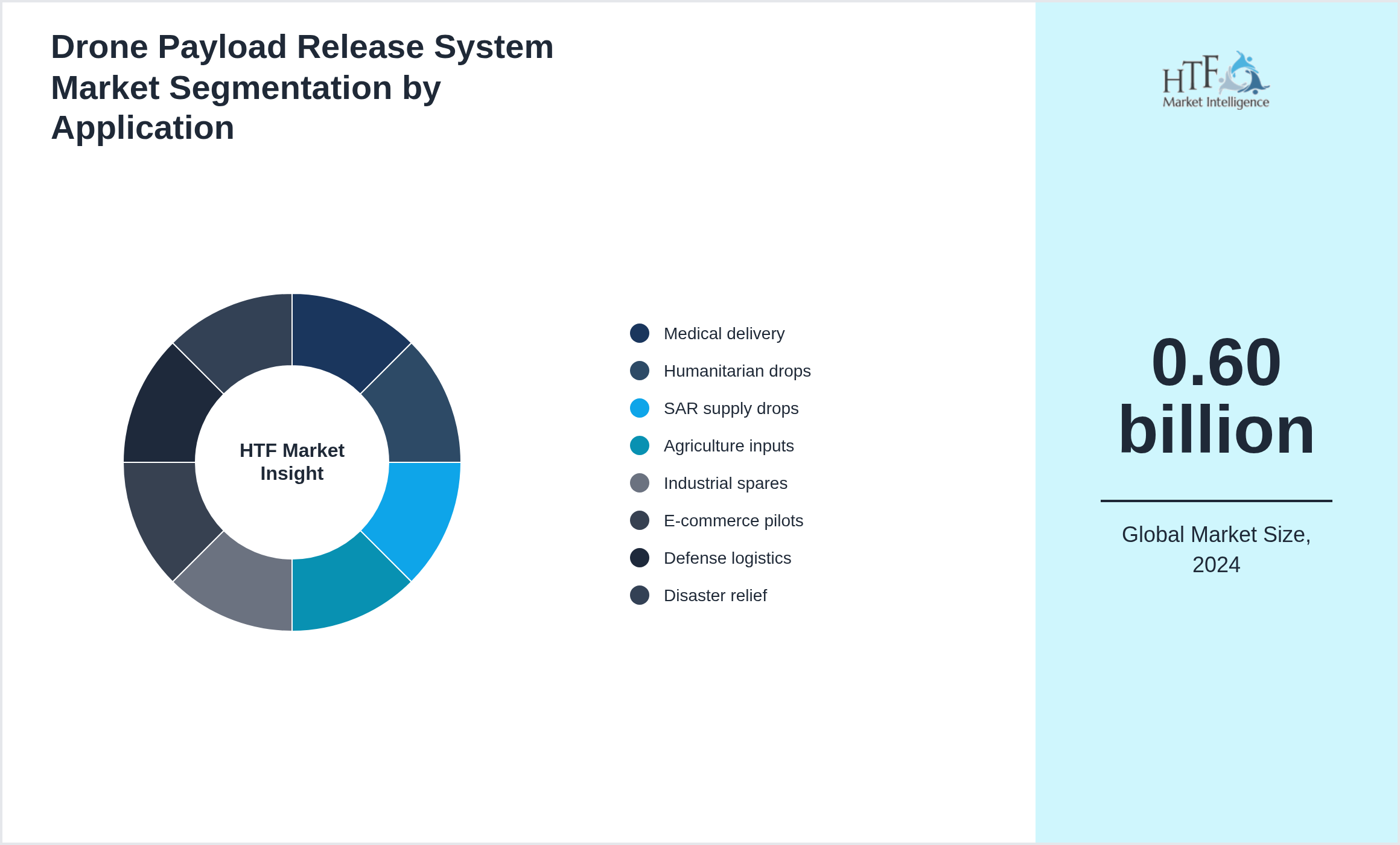

Segmentation by Application

- • Medical delivery

- • Humanitarian drops

- • SAR supply drops

- • Agriculture inputs

- • Industrial spares

- • E-commerce pilots

- • Defense logistics

- • Disaster relief

Market Entropy

- • Apr 2025 – Payload release systems expanded for logistics and emergency use cases with safer locking mechanisms and precise drop control.

Merger & Acquisition

- • In February 2024 a drone systems integrator acquired a payload release mechanism company to expand delivery and drop applications. The acquisition improved safety locks quick-swap mounts and mission software compatibility for logistics emergency response and agriculture use cases.

Regulatory Landscape

- • Highly regulated: UAV airworthiness/operations rules safety case approvals for dropping payloads geofencing and fail-safe requirements and radio compliance. Defense/export controls may apply. Industrial use often needs risk assessments redundancy and documentation for authority approvals.

Patent Analysis

- • Patents cover redundant locking mechanisms smart release triggers load sensing anti-swing stabilization encrypted command links and quick-swap mounts. Claims often combine hardware + flight-control integration. FTO requires checking interface standards and safety-critical redundancy designs.

Investment and Funding Scenario

- • Funding comes from defense primes industrial drone service firms and logistics pilots. Venture funding targets modular payload ecosystems. Procurement cycles can be long but contracts are sticky with certification. Revenue models include hardware + certification support + maintenance spares and software updates.

Competitive Innovation Radar

- • Innovation race: safer redundant releases lower weight higher payload-to-mass ratio and integration with mission planning. Competitors add real-time load verification tamper detection and autonomous drop accuracy. Differentiation via multi-drone compatibility ruggedization rapid certification packages and field service support.

The Top-Down and Bottom-Up Approaches

The top-down approach begins with a broad theory or hypothesis and breaks it down into specific components for testing. This structured, deductive process involves developing a theory, creating hypotheses, collecting and analyzing data, and drawing conclusions. It is particularly useful when there is substantial theoretical knowledge, but it can be rigid and may overlook new phenomena.

Conversely, the bottom-up approach starts with specific data or observations, from which broader generalizations and theories are developed. This inductive process involves collecting detailed data, analyzing it for patterns, developing hypotheses, formulating theories, and validating them with additional data. While this approach is flexible and encourages the discovery of new phenomena, it can be time-consuming and less structured.

Swot and Pestel Analysis

SWOT Analysis

A SWOT analysis evaluates a company’s internal strengths and weaknesses, as well as external opportunities and threats. This Drone Payload Release System analysis helps businesses identify their competitive advantages, address internal challenges, and seize external opportunities while mitigating potential risks. It is performed to gain a comprehensive understanding of the organization's position in the market, align strategies with its strengths, and effectively navigate competitive landscapes.

PESTEL Analysis

Political, economic, social, technological, environmental, and legal factors impacting the business environment. This analysis helps organizations anticipate external changes, adapt strategies to macroeconomic trends, and ensure compliance with regulatory requirements. It is crucial for understanding the external forces that could influence business operations and for planning long-term strategies that align with evolving market conditions.

Report Infographics:

| Report Features | Details |

| Base Year | 2024 |

| Based Year Market Size 2024 | 0.60 billion |

| Historical Period | 2020 |

| CAGR (2024 to 2033) | 15.40% |

| Forecast Period | 2033 |

| Forecasted Period Market Size (2033) | 1.90 billion |

| Scope of the Report | By Type, By Application, By Sales Channel, By Region |

| Quantitative Units |

Revenue in USD million/billion, volume in kilotons, and CAGR from 2024 to 2033 |

| Companies Covered | DJI (CN), Parrot (FR), Skydio (US), AeroVironment (US), Edge Autonomy (US), Lockheed Martin (US), Northrop (US), RTX/Raytheon (US), BAE (UK), Elbit (IL), IAI (IL), Thales (FR), Saab (SE), Leonardo (IT), Quantum-Systems (DE), Autel (CN), Draganfly (CA), Yuneec (CN), Gremsy (VN), Elistair (FR), Teledyne FLIR (US), Moog (US), Curtiss-Wright (US), Hexagon (SE), Sierra-Olympia (US), Flyability (CH) |

| Customization Scope | 15% Free Customization (For example)

Want to Buy Specific Sections of This Report?

|

| Delivery Format | PDF and Excel through Email |

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.