Smartwatch Sale Market - Global Size & Outlook 2020-2033

Global Smartwatch Sale Market is segmented by Application (Health tracking, Notifications, Payments, Sports coaching, Safety/SOS, Sleep analysis, Enterprise workforce, Remote patient monitoring), Type (Fitness, Lifestyle, Rugged, Kids, Luxury, LTE/Cellular, Hybrid, Medical-grade), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

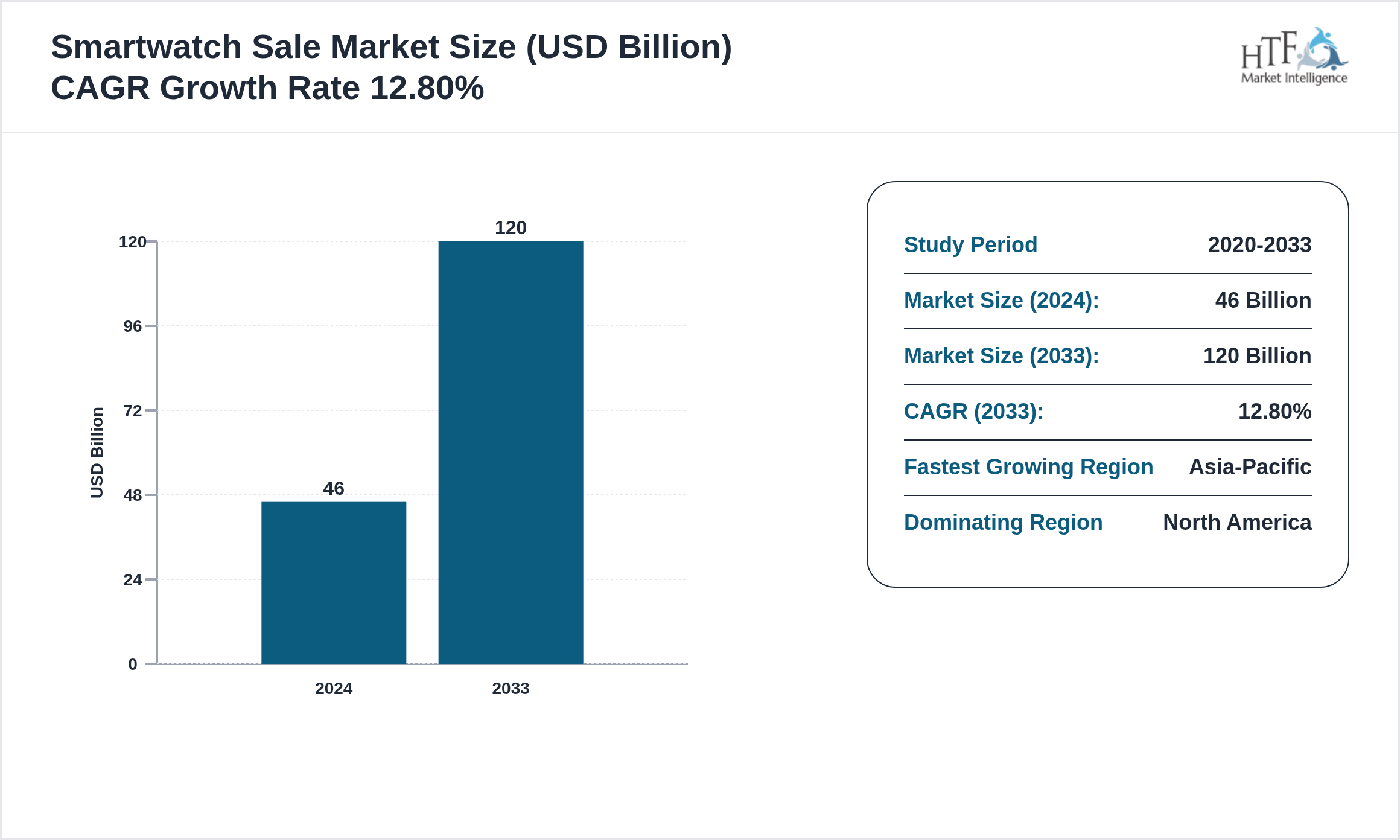

The Smartwatch Sale market is expected to reach 120.0 billion by 2033 and is growing at a CAGR of12.80% between 2024 and 2033.

Smartwatch sale market covers online/offline retail of wrist-worn connected devices offering timekeeping plus apps sensors and wireless connectivity. It includes device hardware bundled services accessories and merchandising across price tiers. Demand is driven by fitness notifications payments and safety features supported by e-commerce promotions and carrier plans.

Source: HTF Market Intelligence (HTF MI)

Market Size & Forecast

Market Segmentation

Selecting segmentation criteria in Apple (US), Samsung (KR), Huawei (CN), Xiaomi (CN), Google/Fitbit (US), Garmin (US), Fossil (US), Amazfit/Zepp (CN), OnePlus (CN), Oppo (CN), Vivo (CN), Lenovo/Motorola (CN/US), Sony (JP), Casio (JP), Polar (FI), Suunto (FI), Withings (FR), Mobvoi (CN), Realme (CN), boAt (IN), Noise (IN), Fire-Boltt (IN), Titan (IN), Seiko (JP), Panasonic (JP), Qualcomm (US) involves several key steps. Researchers begin by defining their objectives, such as understanding consumer behavior or identifying market opportunities. They then gather relevant data on demographics, psychographics, and buying behavior. Next, they identify segmentation variables like age, location, lifestyle, and purchase patterns. Using analytical tools, they analyze the data to find distinct market segments and evaluate their attractiveness based on size, growth potential, and alignment with business goals. Detailed profiles are created for each segment, and the most promising ones are selected for targeting. Finally, tailored marketing strategies are developed, and the performance of these strategies is monitored and adjusted as needed. This process ensures that segmentation effectively identifies valuable market opportunities and aligns with strategic goals.

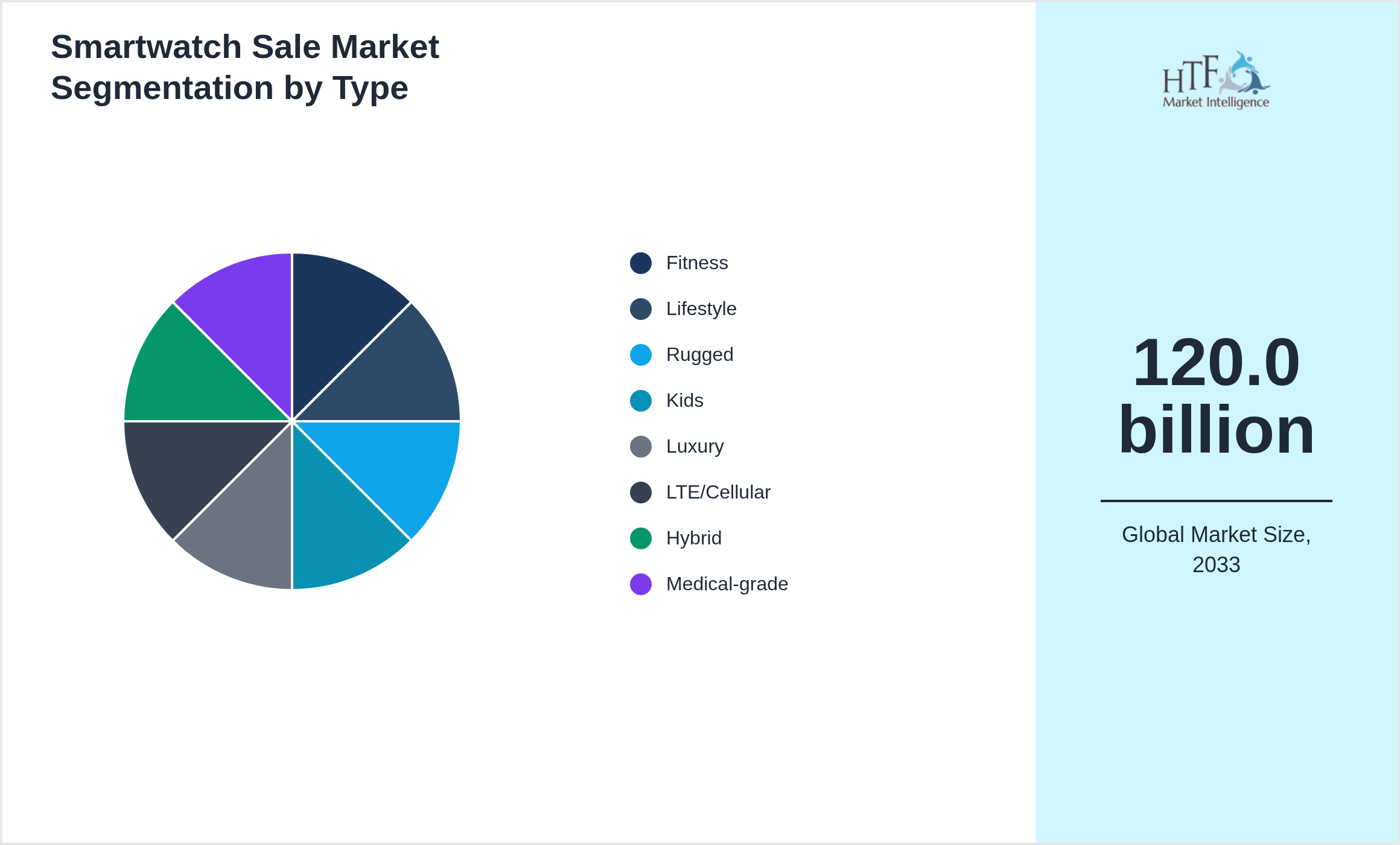

Segmentation by Type

- • Fitness

- • Lifestyle

- • Rugged

- • Kids

- • Luxury

- • LTE/Cellular

- • Hybrid

- • Medical-grade

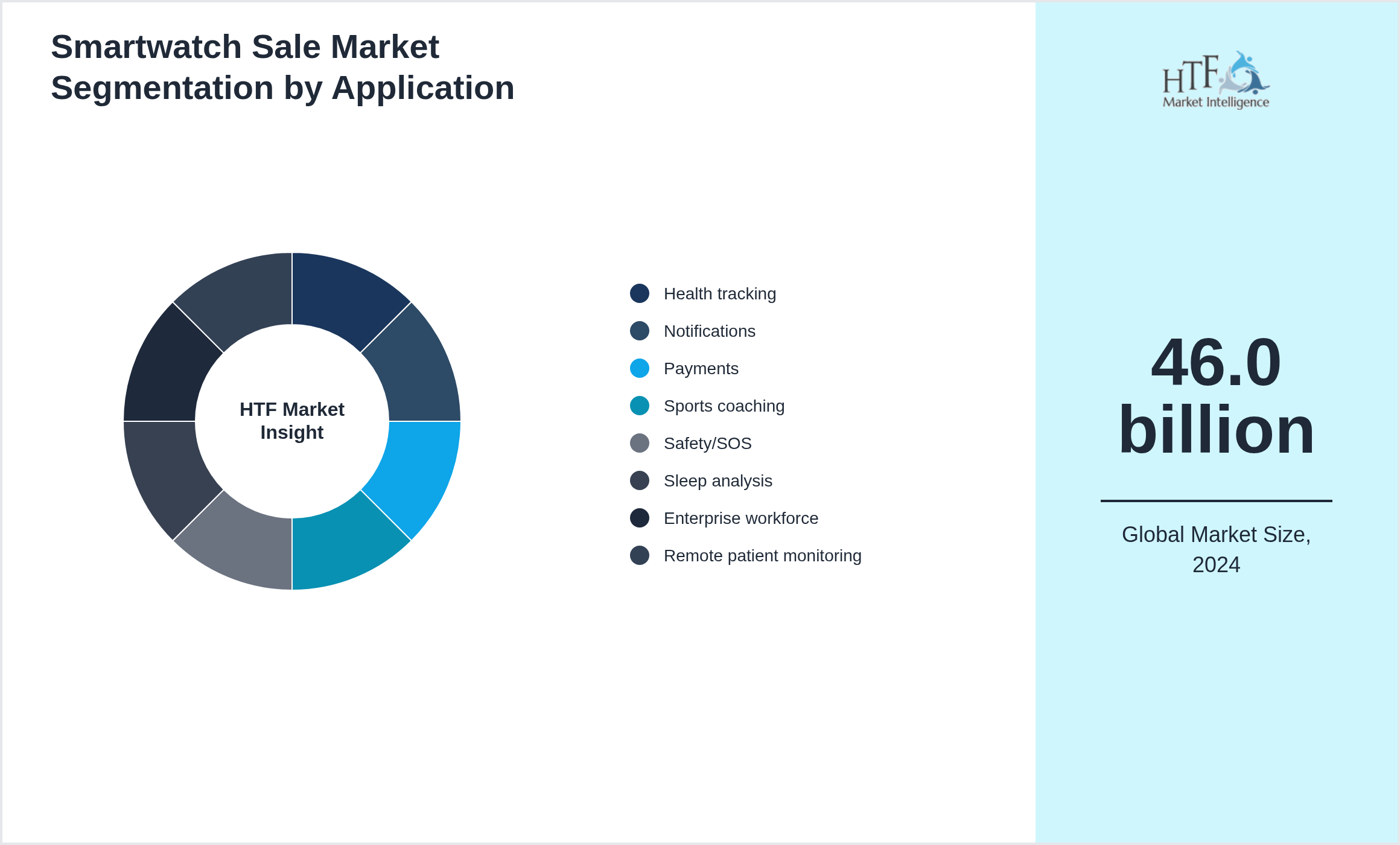

Segmentation by Application

- • Health tracking

- • Notifications

- • Payments

- • Sports coaching

- • Safety/SOS

- • Sleep analysis

- • Enterprise workforce

- • Remote patient monitoring

Smartwatch Sale Market Dynamics

TheSmartwatch Sale is driven by factors such as increasing demand in end-use industries, technological advancements, research and development (R&D), economic growth, and increasing global trade.

Influencing Trend:

- • Shift to AI-driven coaching advanced biosensors LTE eSIM models app ecosystem expansion premium materials subscription services and cross-device continuity with phones/earbuds for stickiness.

- • Rising health awareness affordable sensors smartphone bundling corporate wellness contactless payments and improved battery/SoC efficiency are accelerating upgrades and first-time adoption across mass and premium segments.

- • Accuracy/regulatory claims privacy concerns battery constraints ecosystem lock-in high return rates counterfeit products online price competition and component supply volatility pressure margins.

- • Room for clinical partnerships women’s health features insurance-backed wearables mid-tier LTE models India/SEA offline-to-online channels refurbished programs and enterprise safety deployments.

Regional Insight

The North Americaregion holds a dominant market share, primarily driven by growing consumption patterns, a rising population, and robust economic activity that fuels market demand. Meanwhile, the Asia-Pacific Region is experiencing the fastest growth, propelled by increasing infrastructure developments, expanding industrial activities, and a surge in consumer demand, positioning it as a key driver for future market expansion.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

- • US/EU lead branded smartwatch sales APAC grows fastest in value bands and fitness-first models China drives manufacturing and aggressive online promos Japan/Korea prefer premium ecosystems LATAM/MEA expand via affordable devices and telco bundles. Seasonality peaks around holidays and fitness campaigns.

Key Players

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach:

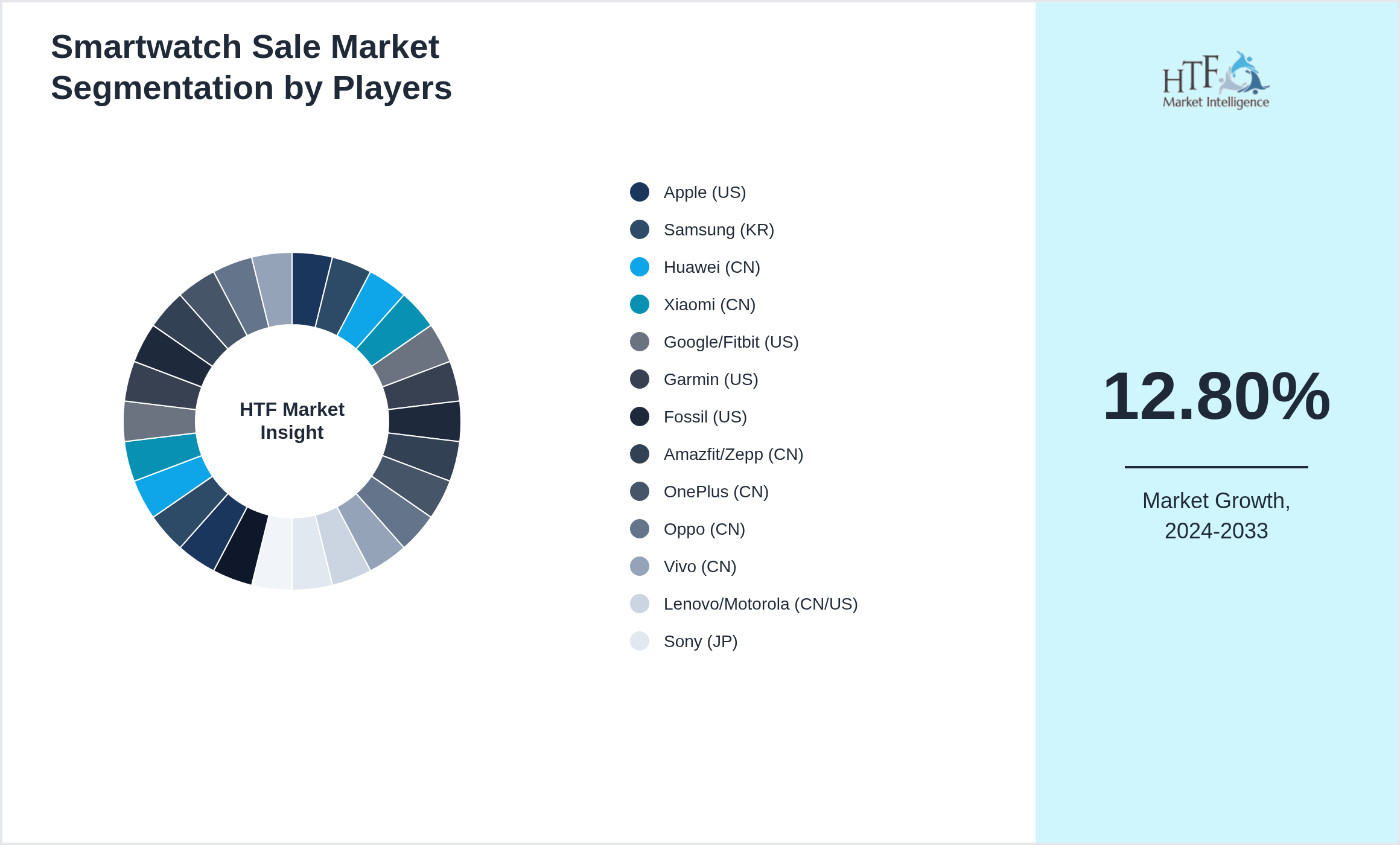

- • Apple (US)

- • Samsung (KR)

- • Huawei (CN)

- • Xiaomi (CN)

- • Google/Fitbit (US)

- • Garmin (US)

- • Fossil (US)

- • Amazfit/Zepp (CN)

- • OnePlus (CN)

- • Oppo (CN)

- • Vivo (CN)

- • Lenovo/Motorola (CN/US)

- • Sony (JP)

- • Casio (JP)

- • Polar (FI)

- • Suunto (FI)

- • Withings (FR)

- • Mobvoi (CN)

- • Realme (CN)

- • boAt (IN)

- • Noise (IN)

- • Fire-Boltt (IN)

- • Titan (IN)

- • Seiko (JP)

- • Panasonic (JP)

- • Qualcomm (US)

Regulatory Framework

The regulatory framework for the Smartwatch Sale ensures product safety, fair competition, and consumer protection. It encompasses setting standards for product quality and safety, enforcing truthful advertising and labeling, and implementing environmental sustainability practices. Regulations include robust procedures for product recalls, data protection, and anti-competitive practices, while also overseeing import/export controls and intellectual property rights. Regulatory bodies enforce these rules through inspections and penalties, and consumer education programs help individuals make informed decisions. This framework aims to protect consumers, promote fair market conditions, and encourage ethical business practices.

- • Compliance includes battery transport radio certifications health/fitness claims scrutiny and privacy rules for biometric/health data. App ecosystem policies kids’ wearables safeguards and warranty/returns apply. Some regions require language labeling local repairability and e-waste take-back participation for electronics.

Competitive Insights

The key players in the Smartwatch Sale are intensifying their focus on research and development (R&D) activities to innovate and stay competitive. Major companies, such as Apple (US), Samsung (KR), Huawei (CN), Xiaomi (CN), Google/Fitbit (US), Garmin (US), Fossil (US), Amazfit/Zepp (CN), OnePlus (CN), Oppo (CN), Vivo (CN), Lenovo/Motorola (CN/US), Sony (JP), Casio (JP), Polar (FI), Suunto (FI), Withings (FR), Mobvoi (CN), Realme (CN), boAt (IN), Noise (IN), Fire-Boltt (IN), Titan (IN), Seiko (JP), Panasonic (JP), Qualcomm (US), are heavily investing in R&D to develop new products and improve existing ones. This strategic emphasis on innovation is driving significant advancements in product formulation and the introduction of sustainable and eco-friendly products.

In addition to R&D and acquisitions, there is a notable shift towards green investments among key players in the consumer goods industry. Companies are increasingly committing resources to sustainable practices and the development of environmentally friendly products. This green investment is in response to growing consumer demand for sustainable solutions and stringent environmental regulations. By prioritizing sustainability, these companies are not only contributing to environmental protection but also positioning themselves as leaders in the green movement, thereby fueling market growth.

Merger Acquisition

- • In February 2024 an online wearables retailer acquired a smartwatch sales platform to strengthen health-tech retail presence.

Patent Analysis

- • Patents are heavy in sensors (PPG ECG) algorithms UI and strap/charging designs. Sales features rely on couponing dynamic pricing and bundle logic. Risk: infringement disputes around health sensing and watch-OS UX. Many sellers avoid “medical” claims unless cleared and validated especially for ECG-like features.

Investment and Funding Scenario

- • Investment flows to health tech wearables sensor startups and DTC brands retailers fund loyalty-driven promo personalization. OEMs invest in chip efficiency and health features to defend ASPs while using controlled discounting. Funding also supports refurbished wearables and subscription services (coaching insights) to offset hardware discounts.

Market Entropy

- • May 2024 – Smartwatch sales grew with health tracking fitness analytics and lifestyle positioning.

Report Infographics:

| Report Features | Details |

| Base Year | 2024 |

| Based Year Market Size 2024 | 46.0 billion |

| Historical Period Market Size 2020 | USD Million ZZ |

| CAGR (2024 to 2033) | 12.80% |

| Forecast Period | 2024 to2033 |

| Forecasted Period Market Size 2033 | 120.0 billion |

| Scope of the Report | Fitness, Lifestyle, Rugged, Kids, Luxury, LTE/Cellular, Hybrid, Medical-grade, Health tracking, Notifications, Payments, Sports coaching, Safety/SOS, Sleep analysis, Enterprise workforce, Remote patient monitoring |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Year-on-Year Growth | 9.50% |

| Companies Covered | Apple (US), Samsung (KR), Huawei (CN), Xiaomi (CN), Google/Fitbit (US), Garmin (US), Fossil (US), Amazfit/Zepp (CN), OnePlus (CN), Oppo (CN), Vivo (CN), Lenovo/Motorola (CN/US), Sony (JP), Casio (JP), Polar (FI), Suunto (FI), Withings (FR), Mobvoi (CN), Realme (CN), boAt (IN), Noise (IN), Fire-Boltt (IN), Titan (IN), Seiko (JP), Panasonic (JP), Qualcomm (US) |

| Customization Scope | 15% Free Customization (For EG) |

| Delivery Format | PDF and Excel through Email

Want to Buy Specific Sections of This Report?

|

Research Methodology

The research methodology for the consumer goods industry involves several key steps to ensure comprehensive and actionable insights. First, the research objectives are clearly defined, focusing on aspects like consumer behavior, market opportunities, competitive dynamics, or regulatory impacts. A thorough literature review follows, drawing from academic journals, industry reports, government publications, and market analyses to establish a knowledge base and identify research gaps. Data collection encompasses both primary methods, such as surveys, interviews, and focus groups with consumers and industry experts, and secondary methods, including analysis of market reports, government data, and industry publications. Quantitative data is analyzed using statistical tools to identify patterns and market segments, while qualitative data from interviews and focus groups is examined to extract key themes and insights.

The market is then segmented based on demographics, psychographics, geography, and purchasing behavior, and competitive analysis is conducted to evaluate key players' strategies and strengths. Trend analysis identifies current and emerging industry trends. Findings are compiled into a detailed report with data visualizations and strategic recommendations. The research is validated and refined through cross-checking and expert feedback, and a framework for continuous monitoring is established to keep the research current and relevant.

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.