Ev Battery Leasing Services Market Size & Share Trends Report

Global Ev Battery Leasing Services Market is segmented by Application (Two-Wheelers, Three-Wheelers, Fleets, Urban Mobility, Logistics), Type (Swap-based, Subscription, Pay-per-use, OEM-linked, Fleet-based), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

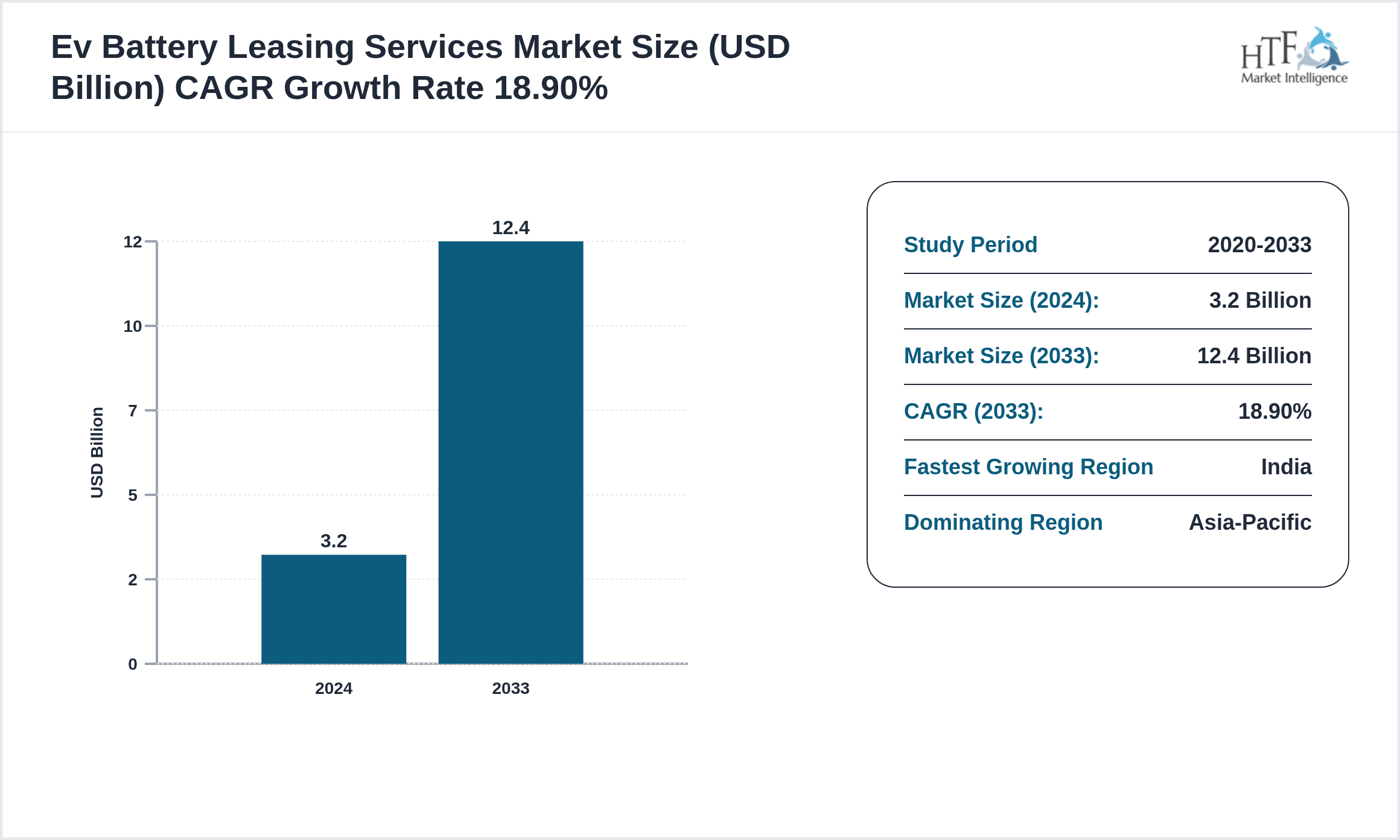

The North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA Ev Battery Leasing Services market was valued at 3.2 billion in 2024 and is expected to reach 12.4 billion by 2020, growing at a compound annual growth rate (CAGR) of 18.90% over the forecast period.

EV battery leasing services allow users to separate battery ownership from the vehiclepaying periodic fees for battery use. This model reduces upfront EV costtransfers performance riskand supports flexible upgrades while enabling providers to manage lifecyclereuseand recycling efficiently.

Source: HTF Market Intelligence (HTF MI)

The North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA insurance industry is a cornerstone of economic stability, offering risk management solutions across various sectors, including life, health, property, and casualty. The industry is undergoing a transformative phase, driven by technological advancements such as artificial intelligence, automation, and digital platforms. These innovations are reshaping customer expectations, pushing insurers to enhance user experiences through personalized policies and faster claims processing.

Ev Battery Leasing Services Market Dynamics

Influencing Trend:

- • Subscription-based battery accessOEM-backed leasing programsand integration with EV-as-a-service models are gaining traction. Data-driven battery health monitoring is becoming a standard trend.

- • High EV adoption costsrapid battery tech evolutionand demand for lower upfront vehicle pricing are driving battery leasing. Fleets and consumers prefer flexible ownership models that reduce depreciation risk and improve affordability.

- • Complex asset valuationregulatory uncertaintyand battery degradation risks challenge scalability. Managing ownershipwarrantiesand end-of-life liabilities remains operationally intensive.

- • Strong opportunity exists in fleet electrificationride-hailingand logistics sectors. Leasing enables circular economy modelsresidual value optimizationand cross-market battery redeployment.

If you need any specifications, please suggest

Regional Insight

The Asia-Pacific currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, India is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth. In our report, we cover a comprehensive analysis of the regions and countries, including

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

Market Segmentation

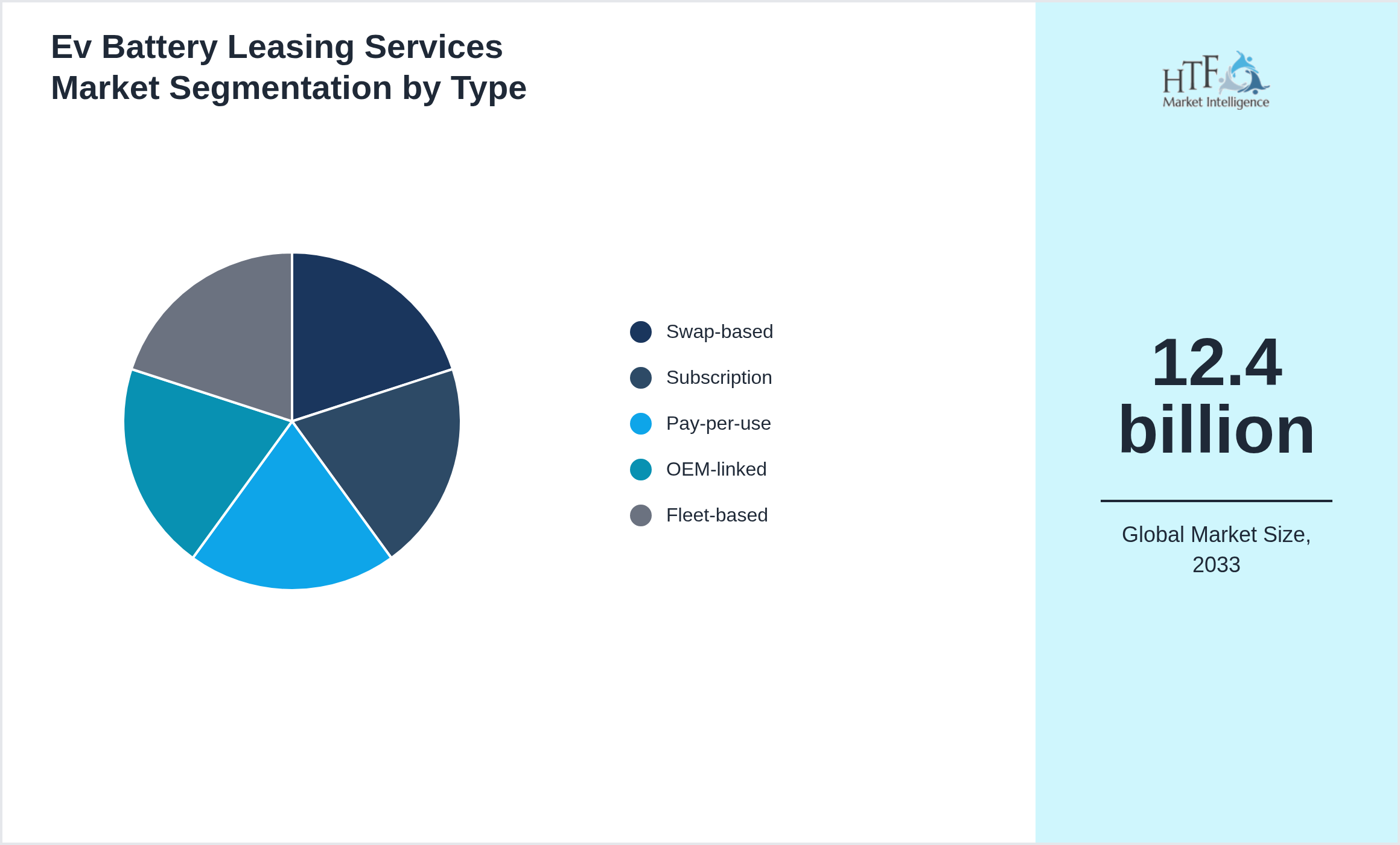

Segmentation by Type

- • Swap-based

- • Subscription

- • Pay-per-use

- • OEM-linked

- • Fleet-based

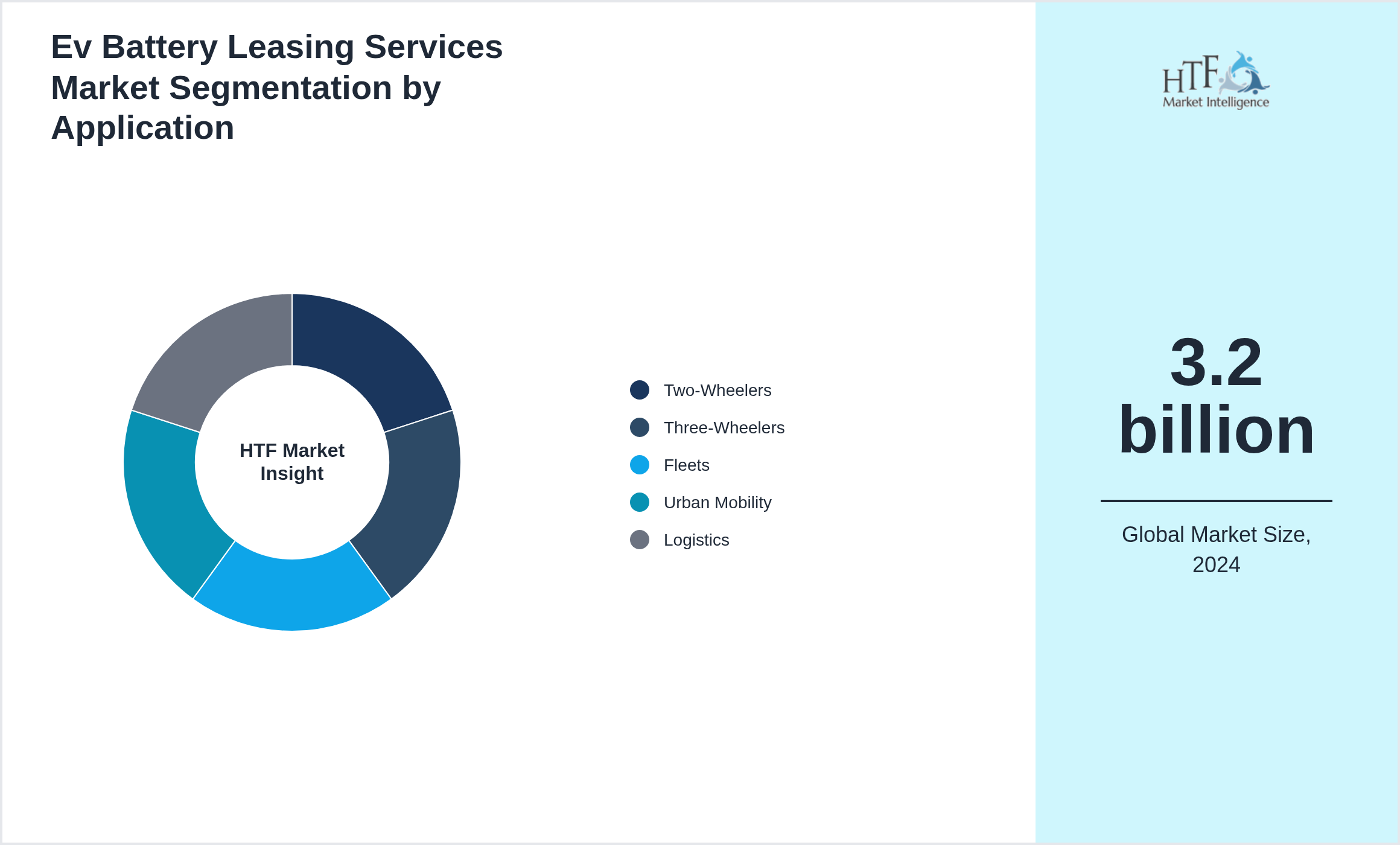

Segmentation by Application

Segmentation by Application

- • Two-Wheelers

- • Three-Wheelers

- • Fleets

- • Urban Mobility

- • Logistics

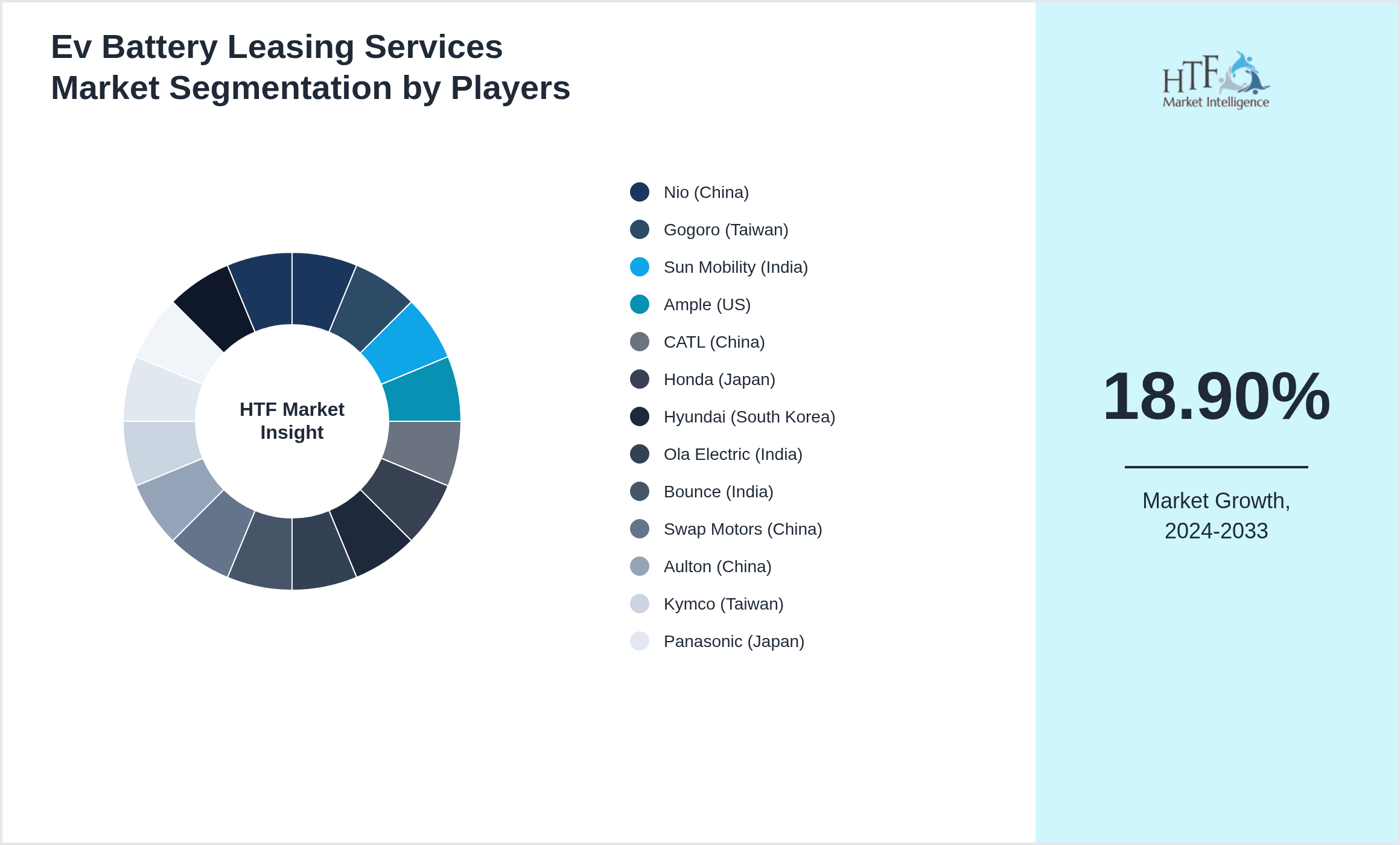

Key Players

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach.

- • Nio (China)

- • Gogoro (Taiwan)

- • Sun Mobility (India)

- • Ample (US)

- • CATL (China)

- • Honda (Japan)

- • Hyundai (South Korea)

- • Ola Electric (India)

- • Bounce (India)

- • Swap Motors (China)

- • Aulton (China)

- • Kymco (Taiwan)

- • Panasonic (Japan)

- • LGES (Korea)

- • Tata Motors (India)

- • Hero MotoCorp (India)

{

Market Entropy

- • Sep 2024 – Leasing models reduced upfront EV costs.

Marger & Acquisition

- • In February 2024

Regulatory Landscape

- • Regs touch consumer financeleasing disclosureswarranty allocationbattery ownership liabilityinsuranceand end-of-life obligations. Data privacy for telematics is key. Some markets require clear SoH reporting and recycling take-back compliance.

Patent Analysis

- • Patents cluster around SoH/SoC estimationresidual value modelsusage-based pricingdigital contractsand remote lock/unlock. IP includes fleet analyticsbattery health scoringand integration with swap/charging ecosystems and fintech rails.

Investment Funding

- • Fintech + OEM captive finance + fleet lessors drive funding. Investors favor predictable cashflows with risk controls. Partnerships with insurers and recyclers reduce downside. Warehousing/ABS structures emerge as portfolios mature with stable default rates.

Regional Analysis

- • China and EU pilots are most active India interest grows for 2/3-wheelers and fleets North America exploring subscription models for commercial EVs. Adoption depends on residual value confidence and swap/repair networks.

Market Highlights

|

Report Features |

Details |

|

Base Year |

2024 |

|

Based Year Market Size |

3.2 billion |

|

Historical Period |

2020 |

|

CAGR (2024to 2033) |

18.90% |

|

Forecast Period |

2033 |

|

Forecasted Period Market Size (2033) |

12.4 billion |

|

Scope of the Report |

By |

|

Companies Covered |

Nio (China), Gogoro (Taiwan), Sun Mobility (India), Ample (US), CATL (China), Honda (Japan), Hyundai (South Korea), Ola Electric (India), Bounce (India), Swap Motors (China), Aulton (China), Kymco (Taiwan), Panasonic (Japan), LGES (Korea), Tata Motors (India), Hero MotoCorp (India) |

|

Companies Covered |

Nio (China), Gogoro (Taiwan), Sun Mobility (India), Ample (US), CATL (China), Honda (Japan), Hyundai (South Korea), Ola Electric (India), Bounce (India), Swap Motors (China), Aulton (China), Kymco (Taiwan), Panasonic (Japan), LGES (Korea), Tata Motors (India), Hero MotoCorp (India) |

|

Customization Scope |

15% Free Customization (For EG) |

|

Delivery Format |

PDF and Excel through Email |

Research Methodology

The research methodology for studying the insurance industry combines both qualitative and quantitative approaches. It begins with secondary research, gathering data from industry reports, government publications, and regulatory filings to understand market trends and dynamics. This is followed by primary research, involving interviews and surveys with industry stakeholders, such as insurers and regulators, to capture insights on market challenges and customer behavior. Quantitative analysis includes examining market size, growth rates, and segmentation by product type and geography. Competitive analysis and trend evaluation are conducted to assess key players and emerging industry shifts, culminating in forecasts and actionable insights for strategic planning.