North America Smart Conveyor Systems Market Size, Growth & Revenue 2024-2034

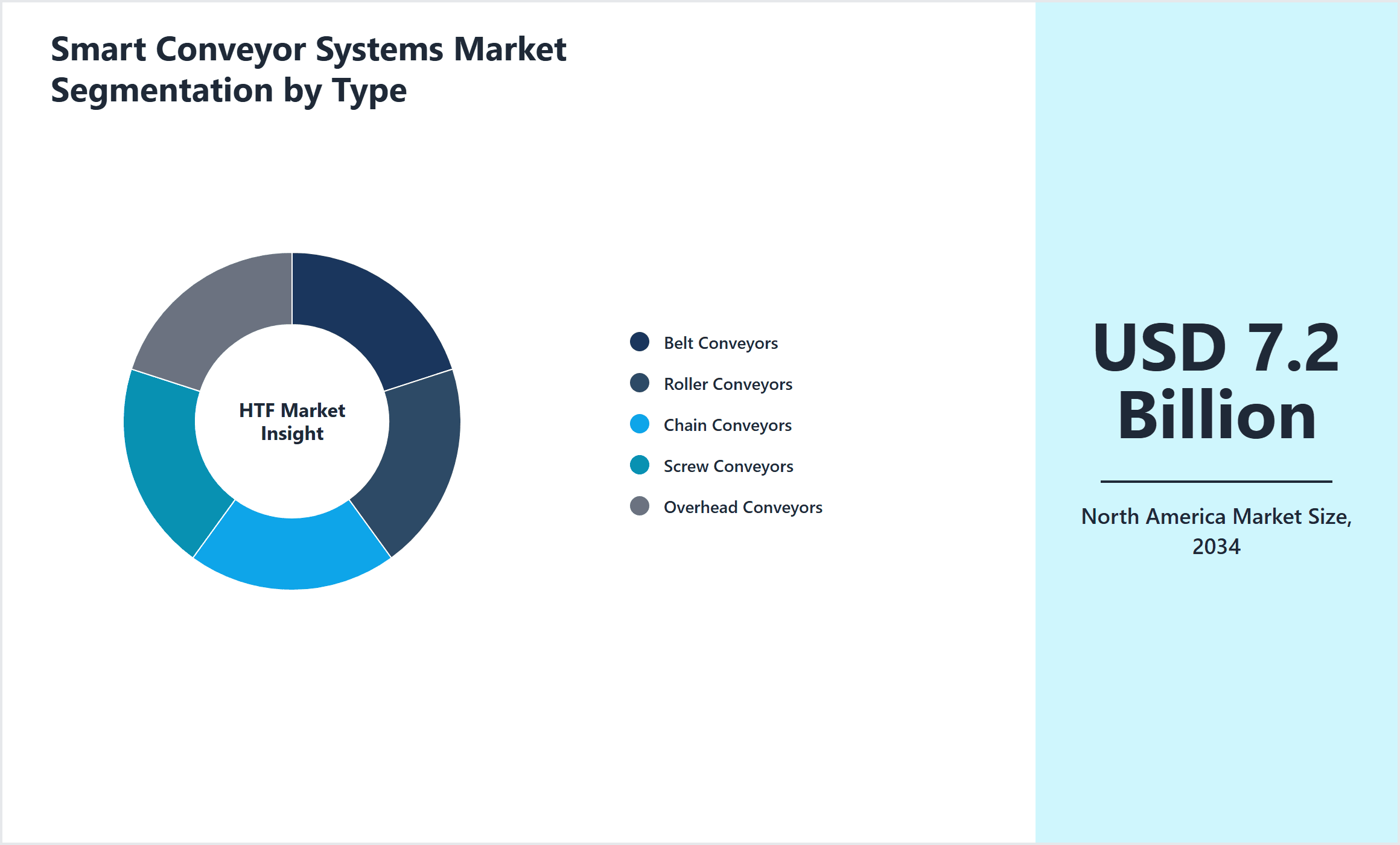

North America Smart Conveyor Systems Market is segmented by Type (Belt Conveyors, Roller Conveyors, Chain Conveyors, Screw Conveyors, Overhead Conveyors), Application (Automotive, Food & Beverage, Pharmaceuticals, E-commerce, Manufacturing), End-Use Industry (Logistics & Warehousing, Automotive Manufacturing, Pharmaceutical Production, Retail Distribution), Distribution Channel (Direct Sales, Distributors, OEM Partnerships), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

- •The North America Smart Conveyor Systems Market is defined by the integration of intelligent automation technologies into traditional conveyor solutions to enhance material handling efficiency across key industries such as automotive, food & beverage, pharmaceuticals, e-commerce, and manufacturing. These systems leverage IoT sensors, AI analytics, and real-time data exchange to enable predictive maintenance, reduce downtime, and optimize throughput in warehouses and production lines. The scope includes various conveyor types—belt, roller, chain, screw, and overhead—that cater to diverse operational needs, from lightweight parcel handling to heavy-duty automotive components transport. The market's boundaries cover system design, manufacturing, installation, and after-sales services, reflecting a comprehensive ecosystem driven by increasing demand for automation and digital transformation in supply chains. Key use cases involve assembly line automation, order fulfillment, and inventory management, positioning smart conveyors as critical infrastructure in North America's evolving industrial landscape.

- •Key market highlights reveal a robust CAGR of 10.1% from 2024 to 2034, with the market size projected to grow from USD 2.8 billion in 2024 to USD 7.2 billion by 2034. The United States dominates the region with the largest market share, while Canada emerges as the fastest-growing country due to increasing investments in warehouse automation and e-commerce fulfillment centers. Belt conveyors lead in adoption due to their versatility, followed by overhead conveyors which are experiencing rapid growth driven by space optimization needs. Applications in automotive and e-commerce sectors account for the highest demand, propelled by the increasing need for streamlined production and logistics operations.

- •Strategically, smart conveyor systems represent a significant value proposition for manufacturers, logistics providers, and retail operations by minimizing labor costs, enhancing operational accuracy, and enabling scalable automation solutions. Stakeholders benefit from improved asset tracking, reduced downtime, and adaptive workflows that respond dynamically to order volume fluctuations. This positions the market as a critical enabler of North America's Industry 4.0 initiatives and sustainable supply chain advancements, fostering competitive advantages through technological innovation and integrated system design.

Competitive Landscape

The competitive environment in the North America Smart Conveyor Systems Market is characterized by a dynamic mix of global technology leaders and specialized regional manufacturers focusing on innovation, customization, and scalable automation solutions. Companies compete through continuous R&D investments to integrate AI, IoT, and robotics into conveyor designs, enhancing system intelligence and operational efficiency. Strategic partnerships and collaborations with industrial automation providers and logistics firms are common to expand market reach and develop end-to-end material handling systems. Pricing strategies balance cost with advanced feature sets, targeting mid-to-large scale enterprises seeking to optimize throughput and reduce labor dependencies. Market rivalry intensifies around rapid deployment capabilities, service reliability, and after-sales support excellence. Additionally, mergers and acquisitions have played a pivotal role in consolidating technological capabilities and expanding product portfolios, intensifying competitive pressures. Regional market entrants focus on niche applications with customized solutions to address sector-specific challenges, contributing to a fragmented yet technologically advanced competitive landscape poised for sustained growth.

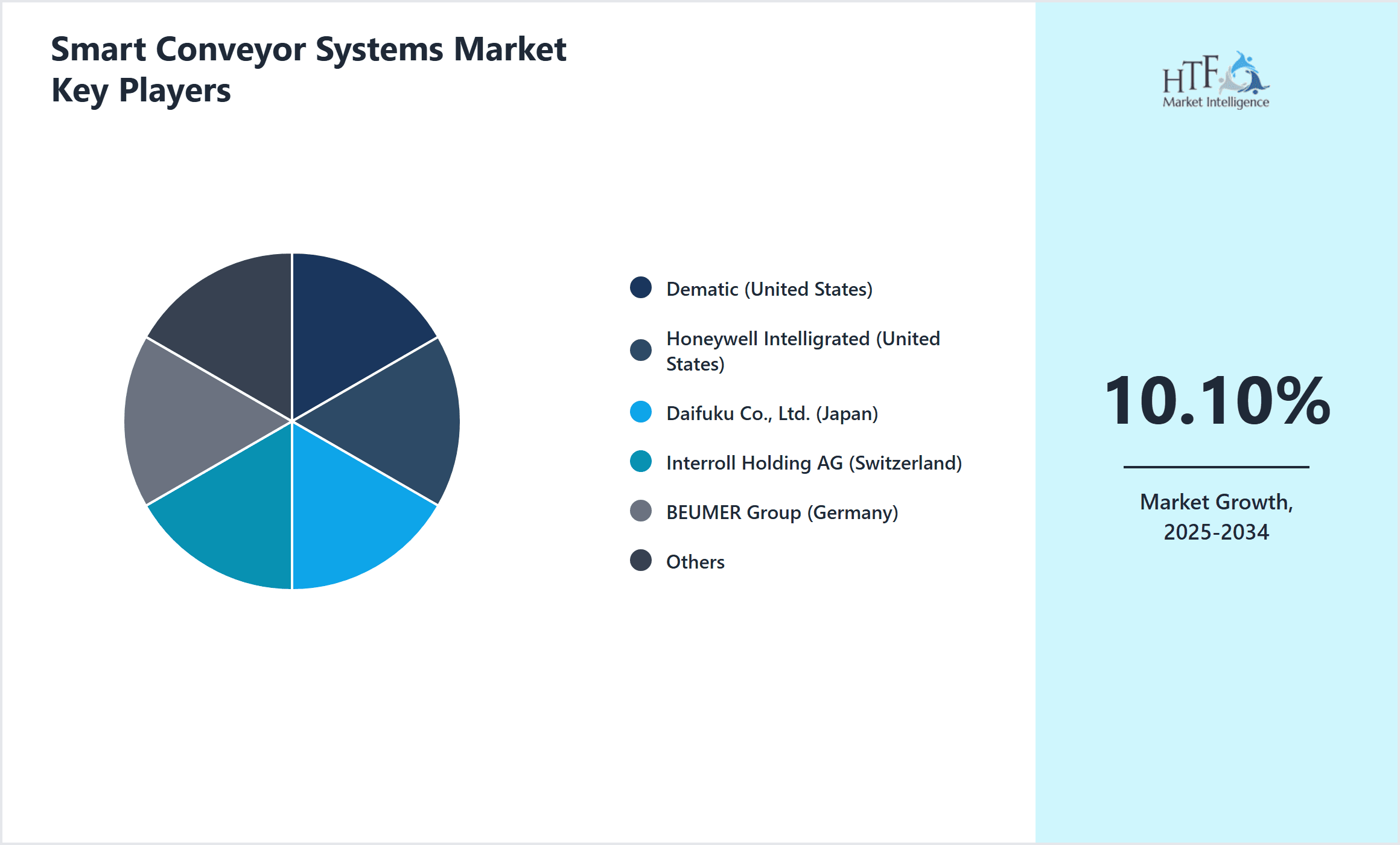

Leading Companies in Smart Conveyor Systems Market

- •Dematic (United States)

- •Honeywell Intelligrated (United States)

- •Daifuku Co., Ltd. (Japan)

- •Interroll Holding AG (Switzerland)

- •BEUMER Group (Germany)

- •Siemens AG (Germany)

- •Vanderlande Industries (Netherlands)

- •Bastian Solutions (United States)

- •Intelligrated (United States)

- •FlexLink Systems AB (Sweden)

- •Fives Group (France)

- •Hytrol Conveyor Company, Inc. (United States)

- •MHS Global (United States)

- •TGW Logistics Group (Austria)

- •Nedap N.V. (Netherlands)

- •Westfalia Technologies, Inc. (United States)

- •FlexLink (Sweden)

- •Daifuku North America (United States)

- •Intralox, LLC (United States)

- •Rexnord Corporation (United States)

- •SSI Schaefer (Germany)

- •Toyota Industries Corporation (Japan)

- •Pratt Industries (United States)

- •Kardex Remstar (Switzerland)

- •Schenck Process GmbH (Germany)

Market Breakdown

- •By Type

- ◦Belt Conveyors

- ◦Roller Conveyors

- ◦Chain Conveyors

- ◦Screw Conveyors

- ◦Overhead Conveyors

- •By Application

- ◦Automotive

- ◦Food & Beverage

- ◦Pharmaceuticals

- ◦E-commerce

- ◦Manufacturing

- •By End-Use Industry

- ◦Logistics & Warehousing

- ◦Automotive Manufacturing

- ◦Pharmaceutical Production

- ◦Retail Distribution

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦OEM Partnerships

Growth Dynamics

- •Increasing automation demand in warehouses and manufacturing plants is a primary growth driver, as companies seek to reduce labor costs and enhance throughput with smart conveyor systems integrated with AI and IoT technologies. For example, e-commerce giants are investing heavily in automated sorting and packing lines to meet growing consumer expectations for fast delivery.

- •The rise of Industry 4.0 initiatives across North America encourages adoption of smart conveyors that enable real-time data collection and predictive maintenance, improving operational efficiency and minimizing downtime. Companies like Honeywell Intelligrated have pioneered solutions that integrate seamlessly with warehouse management systems.

- •Growing complexity in automotive assembly lines requires customizable conveyor systems capable of handling diverse components efficiently. Smart conveyor solutions facilitate agility and flexibility in production, supporting just-in-time manufacturing and reducing inventory costs.

- •Advancements in sensor technologies and AI-powered analytics enable smart conveyors to optimize energy consumption and improve safety standards, driving market growth through sustainable and compliant operations.

- •Government incentives promoting automation and digital infrastructure investments further propel market expansion by supporting modernization of logistics and manufacturing facilities.

Emerging Market Trends

- •Integration of autonomous mobile robots (AMRs) with smart conveyor systems is gaining traction, enabling hybrid material handling solutions that increase flexibility and reduce fixed infrastructure costs in warehouses.

- •Cloud-based monitoring and control platforms are becoming standard, allowing remote management and predictive analytics to reduce unplanned downtime and optimize maintenance schedules.

- •Sustainability trends drive adoption of energy-efficient conveyor components and recyclable materials, aligning with corporate social responsibility goals and regulatory compliance.

- •Customization and modular design are increasingly demanded by end-users to tailor conveyor systems to specific industry needs and facility layouts, enhancing scalability and reducing lead times.

- •Collaborations between technology providers and logistics firms are fostering ecosystem development, accelerating innovation cycles and adoption of integrated smart conveyor solutions.

Market Opportunities

- •Expanding e-commerce fulfillment centers in North America present significant growth opportunities for smart conveyor systems that can handle high order volumes efficiently and adapt to fluctuating demand patterns.

- •Emerging demand for food & beverage automation due to stringent hygiene regulations opens avenues for specialized conveyors with easy cleaning and contamination control features.

- •Integration of AI-driven vision systems with conveyors for quality inspection offers innovation potential and value addition, enabling early defect detection and reducing waste.

- •Geographical expansion into secondary markets within Canada and Mexico allows companies to tap into growing industrial hubs and diversify revenue streams.

- •Investment in retrofit solutions for legacy conveyor systems enables market players to capitalize on modernization projects without full system replacements.

Market Challenges

- •High initial capital expenditure for smart conveyor systems limits adoption among small and medium enterprises, necessitating innovative financing and leasing models.

- •Complex integration processes with existing warehouse management and ERP systems pose technical challenges, increasing deployment timelines and costs.

- •Shortage of skilled workforce to operate and maintain advanced conveyor systems restricts scalability and operational efficiency in some regions.

- •Cybersecurity risks associated with IoT-enabled conveyor networks require robust protective measures, increasing compliance and operational complexity.

- •Fluctuations in raw material prices impact manufacturing costs, creating pricing pressures in a competitive market environment.

Regulatory Framework

- •Between 2019 and 2024, the Occupational Safety and Health Administration (OSHA) updated safety standards mandating enhanced guarding and emergency stop systems on conveyor equipment, increasing compliance requirements for manufacturers and end-users.

- •The North American Electrical Safety Code revisions introduced in 2022 require smart conveyor systems to incorporate advanced electrical protection and grounding measures to prevent hazards in automated environments.

- •Environmental regulations enacted in 2021 emphasize energy efficiency and waste reduction in industrial equipment, encouraging adoption of sustainable conveyor technologies.

- •Federal incentives and grants launched in 2023 promote investments in automation and Industry 4.0 technologies, supporting the deployment of smart conveyor systems across manufacturing and logistics sectors.

- •Data privacy and cybersecurity regulations introduced in 2024 require manufacturers to implement stringent safeguards for IoT-enabled conveyor systems, ensuring protection of operational data and preventing unauthorized access.

Market Intelligence

- •January 2025, Dematic announced the launch of its next-generation Smart Conveyor Platform featuring AI-powered predictive maintenance and seamless integration with warehouse management systems. This innovation aims to reduce downtime by 30% and optimize throughput for large-scale distribution centers across North America, reinforcing Dematic's leadership in intelligent material handling solutions. The platform supports modular upgrades, enabling scalable adoption for diverse industry applications and enhancing operational transparency through cloud-based analytics.

- •March 2025, Honeywell Intelligrated unveiled a cutting-edge roller conveyor system embedded with IoT sensors capable of real-time load monitoring and automated fault detection. Designed for automotive and e-commerce sectors, this system improves safety and efficiency by enabling instant alerts and remote diagnostics, facilitating proactive maintenance interventions. The launch is expected to accelerate the adoption of smart conveyors in high-demand environments, driving competitive advantages through technology integration.

- •May 2025, Interroll Holding AG announced a strategic partnership with a leading logistics automation provider to co-develop smart conveyor solutions optimized for cold chain and pharmaceutical distribution. This collaboration targets enhanced product traceability and compliance through advanced sensor networks and AI analytics, addressing critical industry needs for temperature-sensitive logistics. The initiative positions both companies to capitalize on the growing pharmaceutical supply chain automation market in North America.

- •July 2025, Bastian Solutions completed the acquisition of a regional conveyor systems integrator specializing in customized overhead conveyors for manufacturing clients. This acquisition expands Bastian’s portfolio and regional footprint, allowing faster deployment of tailored smart conveyor solutions in the Midwest and Southern United States. The move strengthens Bastian’s competitive position, enabling deeper market penetration and enhanced service capabilities.

- •Source: Official press releases and company websites

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 2.8 Billion |

| Forecast Year Market Size | USD 7.2 Billion |

| CAGR | 10.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10.1% |

| Scope of Report | Market is segmented by Type (Belt Conveyors, Roller Conveyors, Chain Conveyors, Screw Conveyors, Overhead Conveyors), Application (Automotive, Food & Beverage, Pharmaceuticals, E-commerce, Manufacturing), End-Use Industry (Logistics & Warehousing, Automotive Manufacturing, Pharmaceutical Production, Retail Distribution), Distribution Channel (Direct Sales, Distributors, OEM Partnerships) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Dematic (United States), Honeywell Intelligrated (United States), Daifuku Co., Ltd. (Japan), Interroll Holding AG (Switzerland), BEUMER Group (Germany), Siemens AG (Germany), Vanderlande Industries (Netherlands), Bastian Solutions (United States), Intelligrated (United States), FlexLink Systems AB (Sweden), Fives Group (France), Hytrol Conveyor Company, Inc. (United States), MHS Global (United States), TGW Logistics Group (Austria), Nedap N.V. (Netherlands), Westfalia Technologies, Inc. (United States), FlexLink (Sweden), Daifuku North America (United States), Intralox, LLC (United States), Rexnord Corporation (United States), SSI Schaefer (Germany), Toyota Industries Corporation (Japan), Pratt Industries (United States), Kardex Remstar (Switzerland), Schenck Process GmbH (Germany) |

North America Smart Conveyor Systems Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.