Global Construction Tools Market - Global Outlook 2020-2033

Global Construction Tools Market is segmented by Application (Building, Civil works, Renovation, Workshop, Woodworking, Metalworking, DIY, Industrial), Type (Hand tools, Power tools, Cordless, Pneumatic, Hydraulic, Measuring, Fastening, Cutting), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Key Values Provided by a Construction Tools Market

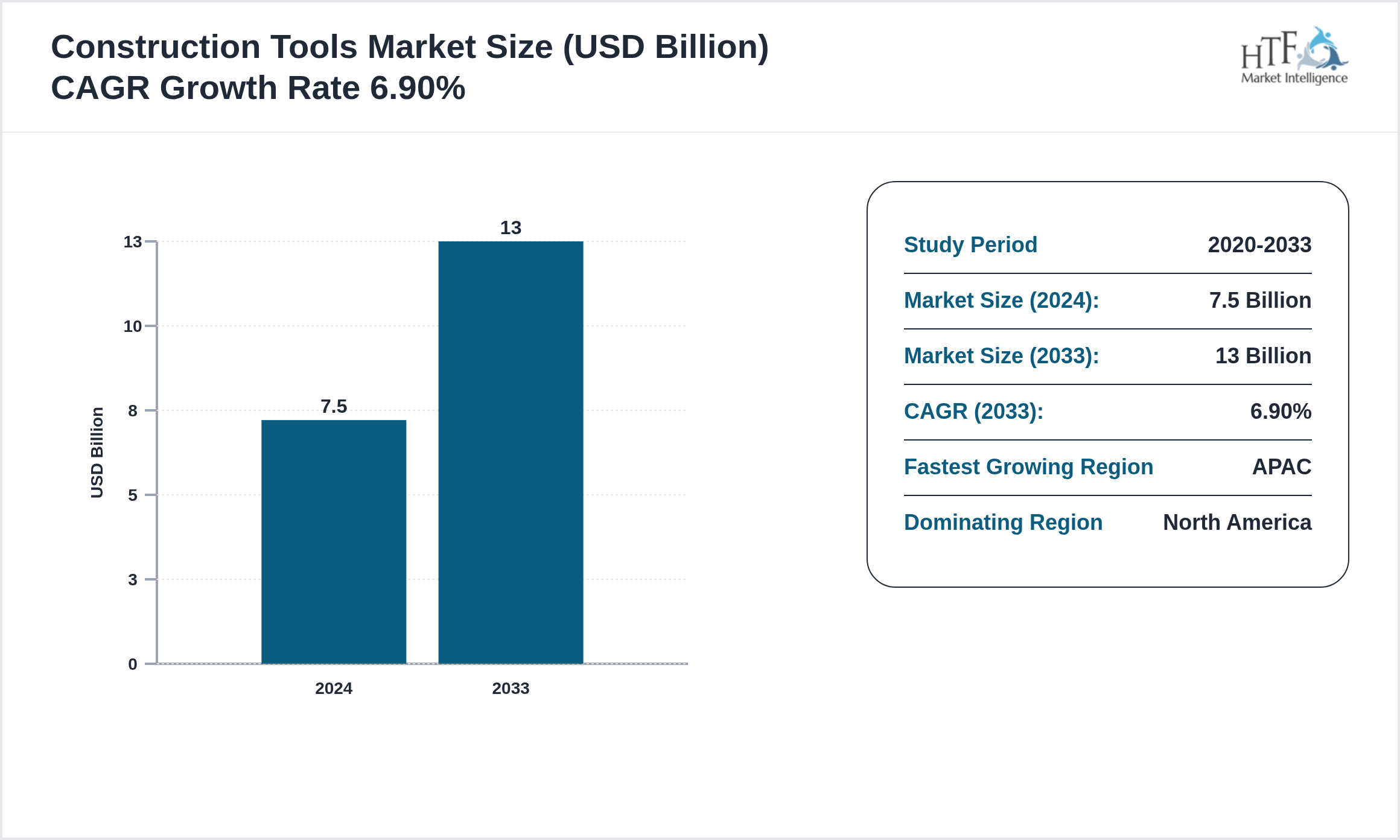

The Construction Tools market was valued at 7.5 billion in 2024 and is expected to reach 13.0 billion by 2020, growing at a compound annual growth rate (CAGR) of 6.90% over the forecast period.

Construction tools comprise manual electric pneumatic and hydraulic equipment used in building infrastructure and civil engineering projects. They include drills cutters concrete mixers compactors and surveying tools. Designed for durability and performance in harsh environments construction tools improve productivity precision and safety across residential commercial and industrial construction activities while supporting faster project execution and reduced labor intensity

Source: HTF Market Intelligence (HTF MI)

A Construction Tools market research study provides invaluable data-driven insights that allow businesses to make informed decisions based on accurate market trends, customer behaviors, and competitor analysis. These reports help organizations better understand the evolving needs of their target audience, enabling more customer-focused strategies.

Market Dynamics

Influencing Trend:

- • Ongoing trends include rapid digitalization adoption of AI-enabled platforms and integration of IoT for real-time monitoring. Companies are focusing on lightweight designs energy efficiency and environmentally responsible materials. Subscription-based services predictive analytics and remote management capabilities are gaining popularity. Collaboration between technology providers and end users is accelerating innovation and shortening product development cycles

- • Increasing demand for reliability efficiency and scalable solutions across commercial and industrial sectors is a key growth driver. Digital transformation initiatives automation adoption and smart infrastructure development are accelerating market penetration. Favorable government initiatives modernization of legacy systems and increased spending on advanced technologies further support demand. Growing awareness of sustainability safety and long-term cost savings continues to drive adoption worldwide

- • The market encounters challenges such as high deployment costs technical complexity and interoperability issues with existing systems. Regulatory uncertainty certification requirements and compliance burdens may slow commercialization. Global supply chain risks component shortages and cost volatility affect operations. Intense competition margin pressure rapid innovation cycles and lack of skilled professionals pose ongoing operational challenges

- • Growth opportunities are expanding in developing regions due to rising industrial activity and infrastructure investments. Demand for customized application-specific and sustainable solutions supports innovation-led growth. Aftermarket services upgrades and digital add-ons offer recurring revenue potential. Increased funding for research adoption of next-generation technologies and expansion into niche applications provide strong long-term market prospects

The North America Dominant Region currently dominates the market share, fueled by increasing consumption, population growth, and sustained economic progress, which collectively enhance market demand. Conversely, the {FASTEST GROWING REGION} is rapidly becoming the fastest-growing region, driven by significant infrastructure investments, industrial expansion, and rising consumer demand.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

Competitive Insights

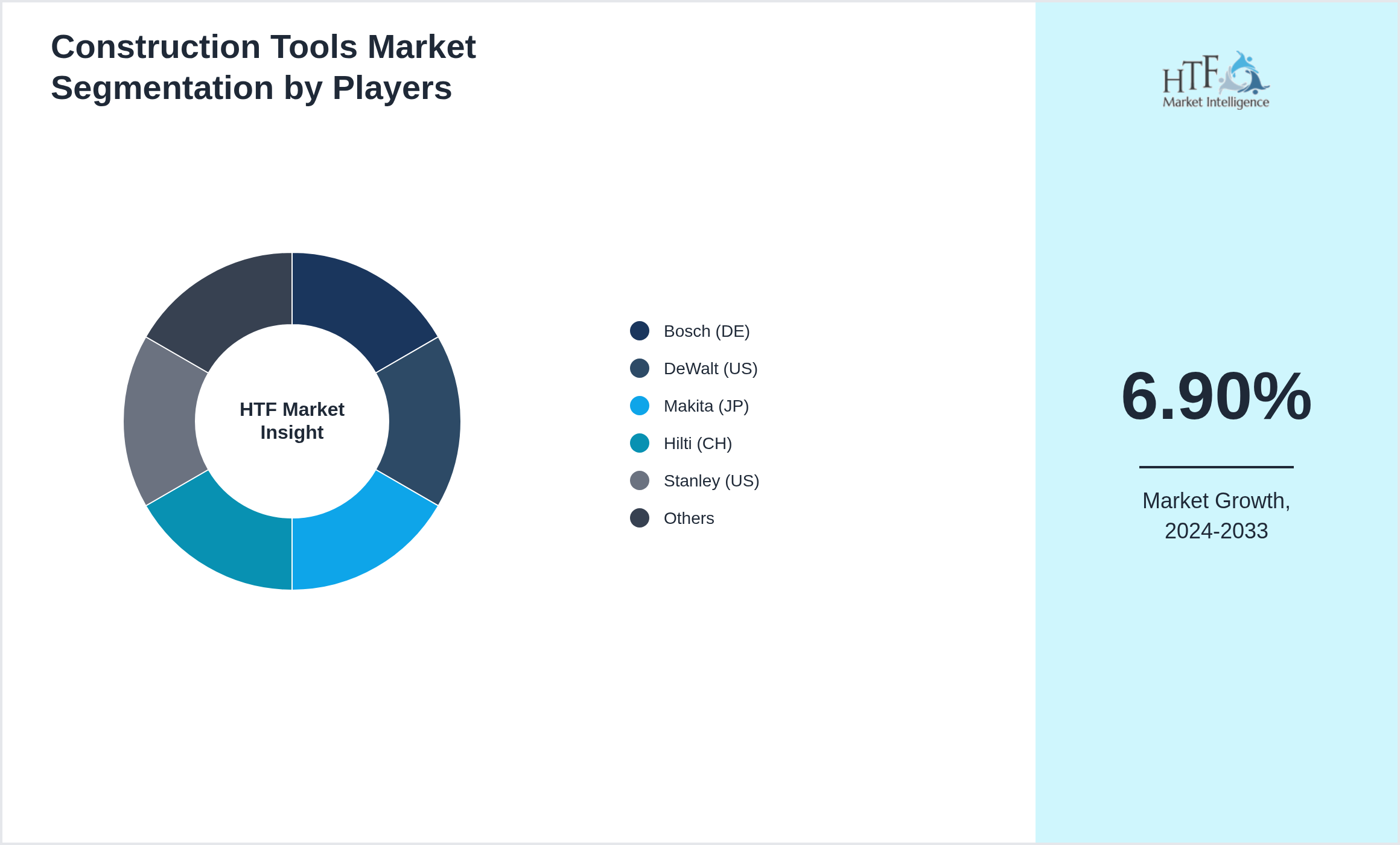

The key players in the Construction Tools are intensifying their focus on research and development (R&D) activities to innovate and stay competitive. Major companies, such as Bosch (DE), DeWalt (US), Makita (JP), Hilti (CH), Stanley (US), Snap-on (US), Festool (DE), Apex (US), Milwaukee (US), Black+Decker (US), Ryobi (JP), Metabo (DE), Fein (DE), Dremel (US), Proxxon (DE), Atlas Copco (SE), Wurth (DE), Ingersoll Rand (US), Sandvik (SE), SKF (SE), Porter-Cable (US), Norton (US), Craftsman (US), Foredom (US), are heavily investing in R&D to develop new products and improve existing ones. This strategic emphasis on innovation drives significant advancements in product formulation and the introduction of sustainable and eco-friendly products.

Moreover, these established industry leaders are actively pursuing acquisitions of smaller companies to expand their regional presence and enhance their market share. These acquisitions not only help in diversifying their product portfolios but also provide access to new technologies and markets. This consolidation trend is a critical factor in the growth of the consumer goods industry, as it enables larger companies to streamline operations, reduce costs, and increase their competitive edge.

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach:

- • Bosch (DE)

- • DeWalt (US)

- • Makita (JP)

- • Hilti (CH)

- • Stanley (US)

- • Snap-on (US)

- • Festool (DE)

- • Apex (US)

- • Milwaukee (US)

- • Black+Decker (US)

- • Ryobi (JP)

- • Metabo (DE)

- • Fein (DE)

- • Dremel (US)

- • Proxxon (DE)

- • Atlas Copco (SE)

- • Wurth (DE)

- • Ingersoll Rand (US)

- • Sandvik (SE)

- • SKF (SE)

- • Porter-Cable (US)

- • Norton (US)

- • Craftsman (US)

- • Foredom (US)

Key Highlights

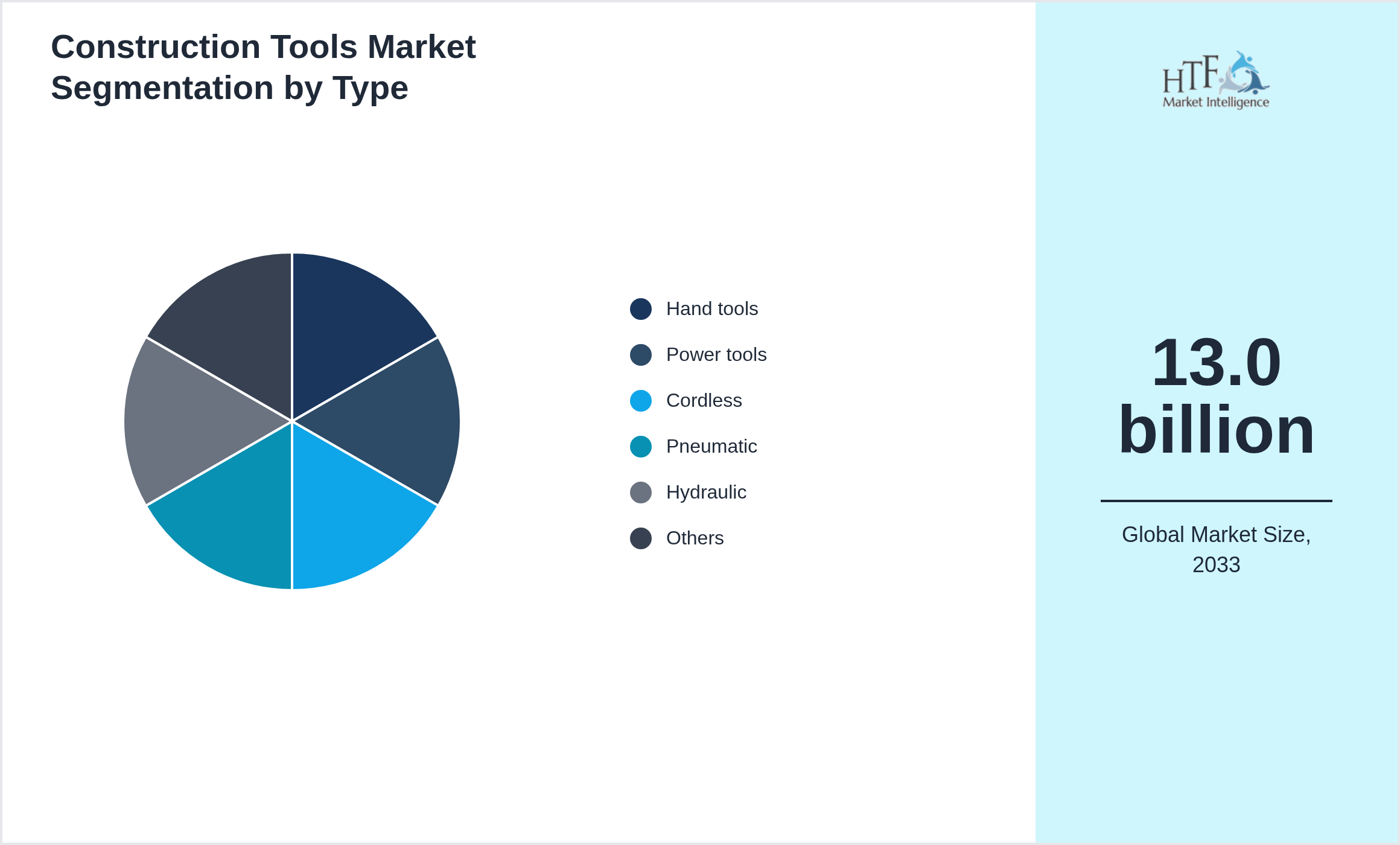

Segmentation by Type

- • Hand tools

- • Power tools

- • Cordless

- • Pneumatic

- • Hydraulic

- • Measuring

- • Fastening

- • Cutting

Segmentation by Application

- • Building

- • Civil works

- • Renovation

- • Workshop

- • Woodworking

- • Metalworking

- • DIY

- • Industrial

![Construction Tools Market trend by end use applications [Building, Civil works, Renovation, Workshop, Woodworking, Metalworking, DIY, Industrial]](https://htf-insight.s3.us-east-1.amazonaws.com/generated-charts/chart-pie-and-donut-chart-application-4402974-na-1768822411563-1768822414705-aa695e09d6cfcd9e.png)

Market Entropy

- • In Aug 2025 construction tools focused on ruggedness and productivity. Infrastructure spending and urban development projects sustained market expansion

Merger & Acquisition

- • In May 2023 a construction equipment company acquired a construction tools manufacturer. The deal expanded heavy-use tools for infrastructure projects.

Regulatory Landscape

- • Regulatory frameworks are evolving toward stricter emissions limits enhanced product certification and supply chain transparency. Compliance costs are rising but harmonization across regions improves market access and reduces long-term regulatory uncertainty

Patent Analysis

- • Patent filings emphasize performance reliability energy efficiency and modular design. Companies use IP portfolios to support licensing and partnerships. Asia leads filing quantity while North America and Europe dominate strategic patent monetization

Investment and Funding Scenario

- • Investment activity favors long-term stability over rapid expansion. Institutional investors support regulation-aligned assets while corporates invest in automation localization and technology upgrades to protect margins and competitiveness

Competitive Innovation Radar

- • The market remains moderately competitive with pressure on pricing and differentiation. Leaders rely on technology leadership and scale while regional players compete on responsiveness and cost efficiency through localized operations

The Top-Down and Bottom-Up Approaches

The top-down approach begins with a broad theory or hypothesis and breaks it down into specific components for testing. This structured, deductive process involves developing a theory, creating hypotheses, collecting and analyzing data, and drawing conclusions. It is particularly useful when there is substantial theoretical knowledge, but it can be rigid and may overlook new phenomena.

Conversely, the bottom-up approach starts with specific data or observations, from which broader generalizations and theories are developed. This inductive process involves collecting detailed data, analyzing it for patterns, developing hypotheses, formulating theories, and validating them with additional data. While this approach is flexible and encourages the discovery of new phenomena, it can be time-consuming and less structured.

Swot and Pestel Analysis

SWOT Analysis

A SWOT analysis evaluates a company’s internal strengths and weaknesses, as well as external opportunities and threats. This Construction Tools analysis helps businesses identify their competitive advantages, address internal challenges, and seize external opportunities while mitigating potential risks. It is performed to gain a comprehensive understanding of the organization's position in the market, align strategies with its strengths, and effectively navigate competitive landscapes.

PESTEL Analysis

Political, economic, social, technological, environmental, and legal factors impacting the business environment. This analysis helps organizations anticipate external changes, adapt strategies to macroeconomic trends, and ensure compliance with regulatory requirements. It is crucial for understanding the external forces that could influence business operations and for planning long-term strategies that align with evolving market conditions.

Report Infographics:

| Report Features | Details |

| Base Year | 2024 |

| Based Year Market Size 2024 | 7.5 billion |

| Historical Period | 2020 |

| CAGR (2024 to 2033) | 6.90% |

| Forecast Period | 2033 |

| Forecasted Period Market Size (2033) | 13.0 billion |

| Scope of the Report | By Type, By Application, By Sales Channel, By Region |

| Quantitative Units |

Revenue in USD million/billion, volume in kilotons, and CAGR from 2024 to 2033 |

| Companies Covered | Bosch (DE), DeWalt (US), Makita (JP), Hilti (CH), Stanley (US), Snap-on (US), Festool (DE), Apex (US), Milwaukee (US), Black+Decker (US), Ryobi (JP), Metabo (DE), Fein (DE), Dremel (US), Proxxon (DE), Atlas Copco (SE), Wurth (DE), Ingersoll Rand (US), Sandvik (SE), SKF (SE), Porter-Cable (US), Norton (US), Craftsman (US), Foredom (US) |

| Customization Scope | 15% Free Customization (For example)

Want to Buy Specific Sections of This Report?

|

| Delivery Format | PDF and Excel through Email |

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.