Anodized Aluminium Market - Global Industry Size & Growth Analysis 2020-2033

Global Anodized Aluminium Market is segmented by Application (Aerospace parts, Automotive components, Electronics housings, Consumer goods, Architectural aluminum, Medical devices, Defense hardware, Industrial machinery), Type (Sulfuric anodizing, Hard anodizing, Chromic anodizing, Boric-sulfuric, Phosphoric anodizing, Plasma electrolytic oxidation, Color anodizing, Sealed AAO), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

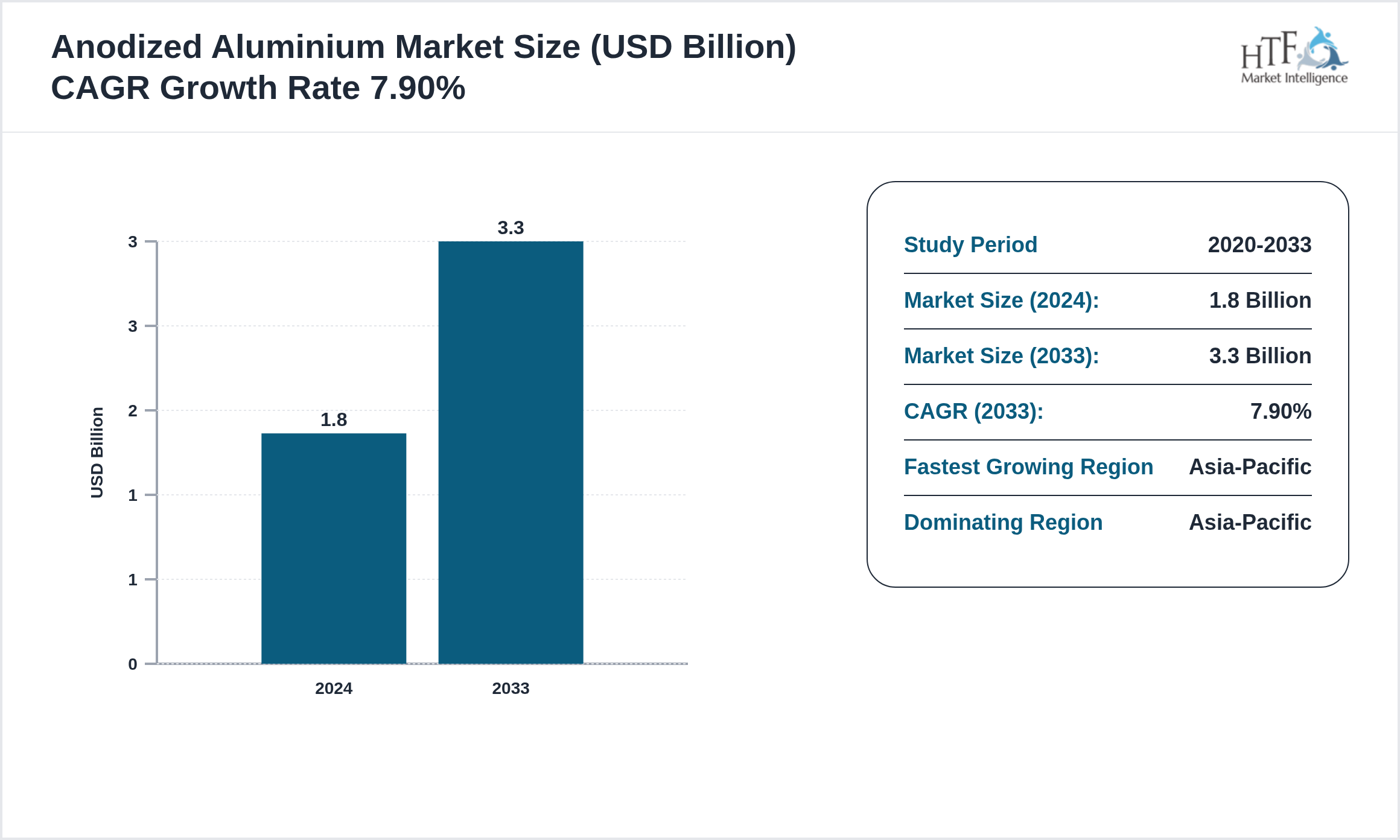

The Anodized Aluminium is at USD 1.8 billion in 2024 and is expected to reach 3.3 billion by 2033. The Anodized Aluminium is driven by increasing demand in end-use industries, technological advancements, research and development (R&D), economic growth, and global trade.

Anodized aluminium is aluminum that has undergone an electrochemical process to thicken its natural oxide layer. This enhances corrosion resistance surface hardness and aesthetic appearance. Anodized aluminium is widely used in construction electronics automotive and consumer products. The process allows for coloring and improves durability while maintaining lightweight properties

Source: HTF Market Intelligence (HTF MI)

Competitive landscape

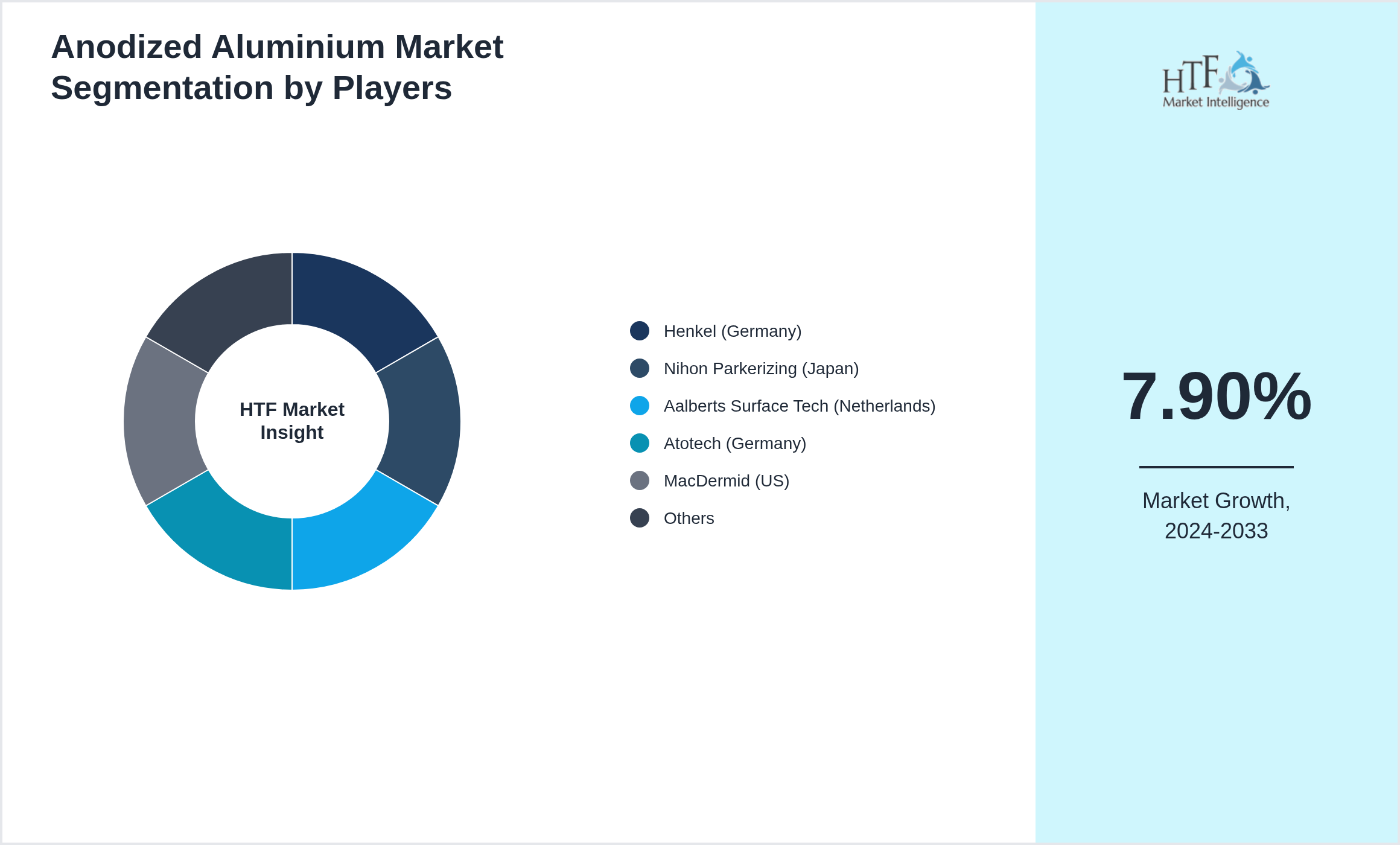

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach:

- • Henkel (Germany)

- • Nihon Parkerizing (Japan)

- • Aalberts Surface Tech (Netherlands)

- • Atotech (Germany)

- • MacDermid (US)

- • Okuno Chemical (Japan)

- • Chemetall/BASF (Germany)

- • Tufram (US)

- • Pioneer Metal Finishing (US)

- • Bodycote (UK)

- • KANIGEN (Canada)

- • Electrochemical Products (US)

- • Anoplate (US)

- • Aludine (France)

- • Coventya (France)

What are the Key Growth Drivers of the Anodized Aluminium Market?

What Risks could Impact the future of the Anodized Aluminium Market?

What Untapped Segments of Anodized Aluminium Market offer the Greatest Growth Potential?

What are the Key Trends in Anodized Aluminium Market to Watch through 2033?

Regulatory Framework

- • Regulatory focus is shifting toward lifecycle compliance environmental disclosures and product traceability. Authorities are enforcing stricter safety audits labeling rules and digital compliance systems while incentive programs promote localization decarbonization and technology modernization

Regional Insight

The Asia-Pacific leads the market share, largely due to rising consumption, a growing population, and strong economic momentum that boosts demand. In contrast, the Asia-Pacific is emerging as the fastest-growing area, driven by rapid infrastructure development, the expansion of industrial sectors, and heightened consumer demand, making it a critical factor for future market growth. The regions covered in the report are

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

Regional Analysis

- • Asia-Pacific accounts for the largest growth share due to expanding manufacturing capacity cost advantages and rapid urban development. North America remains innovation-led with strong enterprise demand while Europe focuses on efficiency compliance-driven upgrades and cross-border industrial collaboration

Market Segmentation

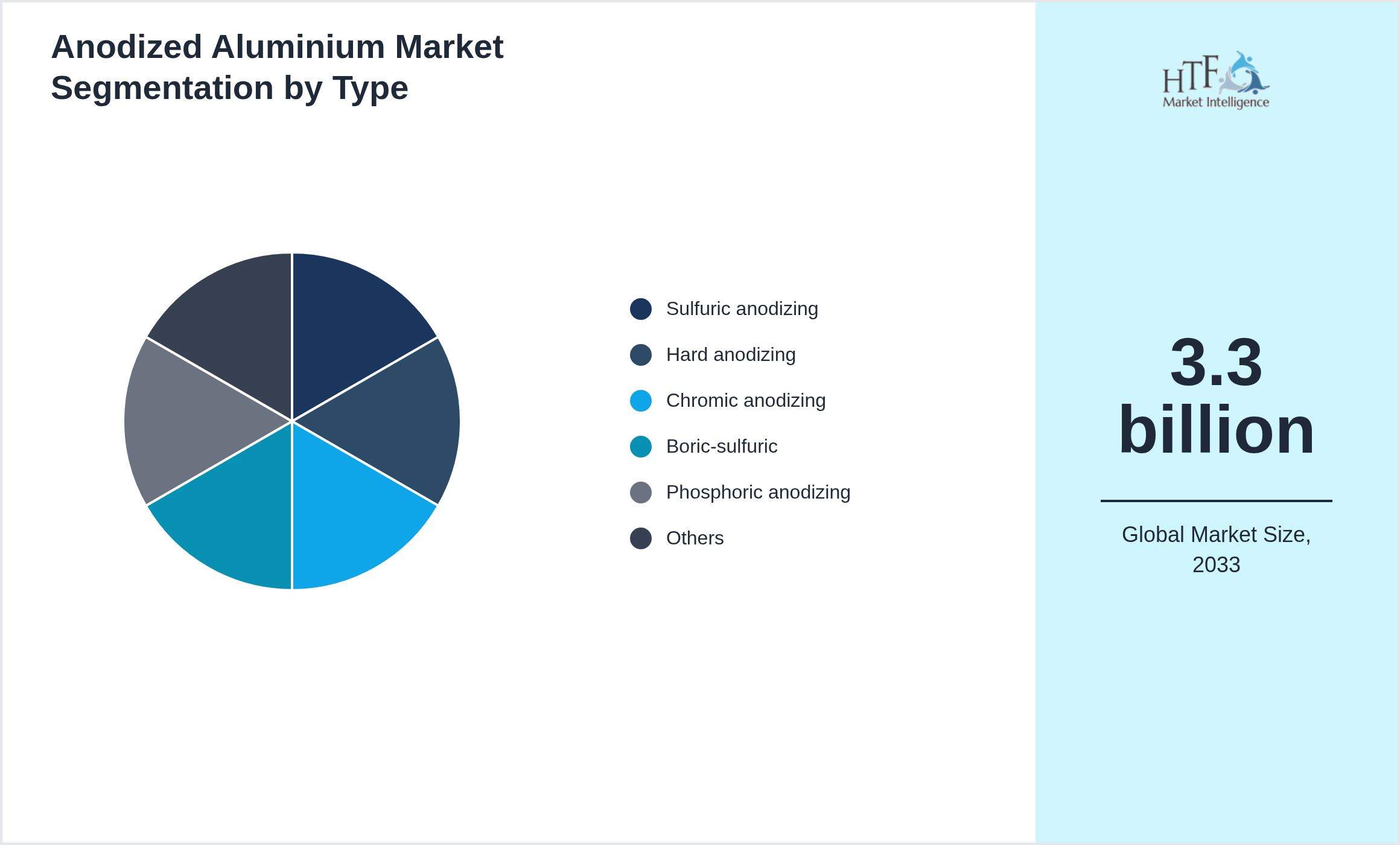

Segmentation by Type

- • Sulfuric anodizing

- • Hard anodizing

- • Chromic anodizing

- • Boric-sulfuric

- • Phosphoric anodizing

- • Plasma electrolytic oxidation

- • Color anodizing

- • Sealed AAO

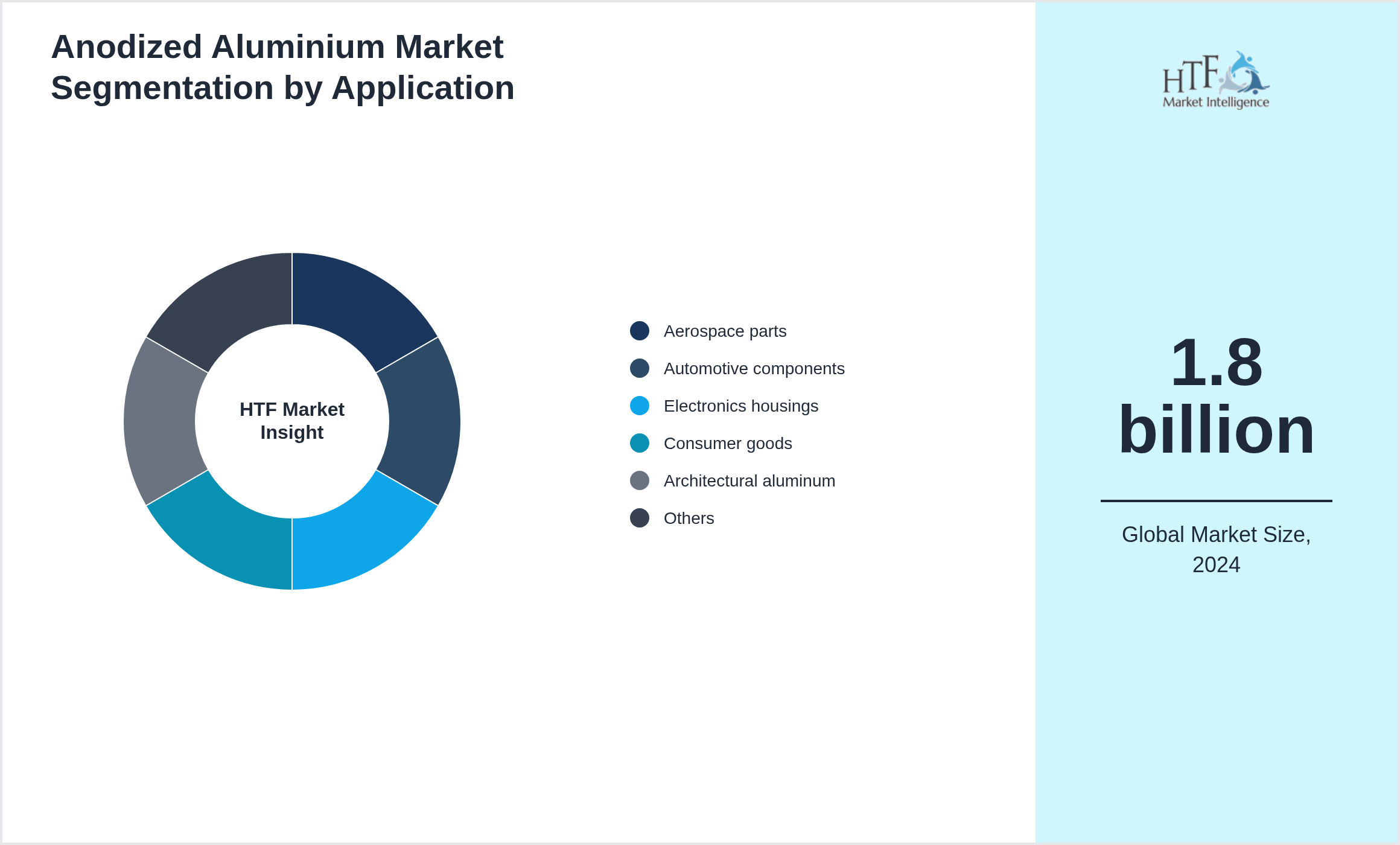

Segmentation by Application

- • Aerospace parts

- • Automotive components

- • Electronics housings

- • Consumer goods

- • Architectural aluminum

- • Medical devices

- • Defense hardware

- • Industrial machinery

Key Development Activities

Market Entropy

- • In Mar 2025 anodized aluminium demand grew across automotive electronics and construction due to corrosion resistance and aesthetic durability

Merger & Acquisition

- • In May 2024 an aluminum processing firm acquired an anodizing facility to strengthen architectural and automotive applications

Regulatory Landscape

- • Regulatory focus is shifting toward lifecycle compliance environmental disclosures and product traceability. Authorities are enforcing stricter safety audits labeling rules and digital compliance systems while incentive programs promote localization decarbonization and technology modernization

Patent Analysis

- • Patent filings emphasize next-generation materials smart process controls and performance enhancement technologies. Large enterprises hold core patents while startups focus on application-level innovation. China and South Korea show strong filing momentum with the US leading in patent citations

Investment and Funding Scenario

- • Capital inflow is supported by strategic investors sovereign funds and industrial partnerships. Funding targets capacity expansion digital transformation and sustainability initiatives. Early-stage funding is active in Asia while North America attracts late-stage and technology commercialization investments

Report Details

| Report Features | Details |

| Base Year | 2024 |

| Based Year Market Size (2024) | 1.8 billion |

| Historical Period | 2020 to 2024 |

| CAGR (2024 to 2033) | 7.90% |

| Forecast Period | 2026 to 2033 |

| Forecasted Period Market Size (2033) | 3.3 billion |

| Scope of the Report | Sulfuric anodizing, Hard anodizing, Chromic anodizing, Boric-sulfuric, Phosphoric anodizing, Plasma electrolytic oxidation, Color anodizing, Sealed AAO, Aerospace parts, Automotive components, Electronics housings, Consumer goods, Architectural aluminum, Medical devices, Defense hardware, Industrial machinery |

| Companies Covered | Henkel (Germany), Nihon Parkerizing (Japan), Aalberts Surface Tech (Netherlands), Atotech (Germany), MacDermid (US), Okuno Chemical (Japan), Chemetall/BASF (Germany), Tufram (US), Pioneer Metal Finishing (US), Bodycote (UK), KANIGEN (Canada), Electrochemical Products (US), Anoplate (US), Aludine (France), Coventya (France) |

| Customization Scope | 15% Free Customization |

| Delivery Format | PDF and Excel through Email |

Research Methodology

The research methodology involves several key steps to ensure comprehensive and accurate insights. First, the objectives of the research are clearly defined, focusing on aspects such as market size, growth trends, and competitive dynamics. Data collection is conducted through both primary and secondary methods. Primary research includes interviews with industry experts, surveys, and focus groups to gather firsthand information, while secondary research involves analyzing existing reports, government publications, and company filings.

The collected data is then subjected to rigorous analysis, with quantitative methods used to evaluate market size and trends and qualitative methods applied to understand industry dynamics and consumer behavior. Findings are compiled into a detailed report featuring key insights, data visualizations, and strategic recommendations. Validation is achieved through data verification and peer reviews to ensure accuracy.

Finally, the research concludes with actionable insights and recommendations, along with suggestions for future studies to address emerging trends and gaps. This methodology provides a structured approach to understanding the {keywords} and guiding strategic decisions.

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.