Automobile Die Casting Mould Market Market - Global Industry Size & Growth Analysis 2020-2033

Global Automobile Die Casting Mould Market Market is segmented by Application (Automotive, Aerospace, Machinery), Type (Aluminum, Zinc, Magnesium), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

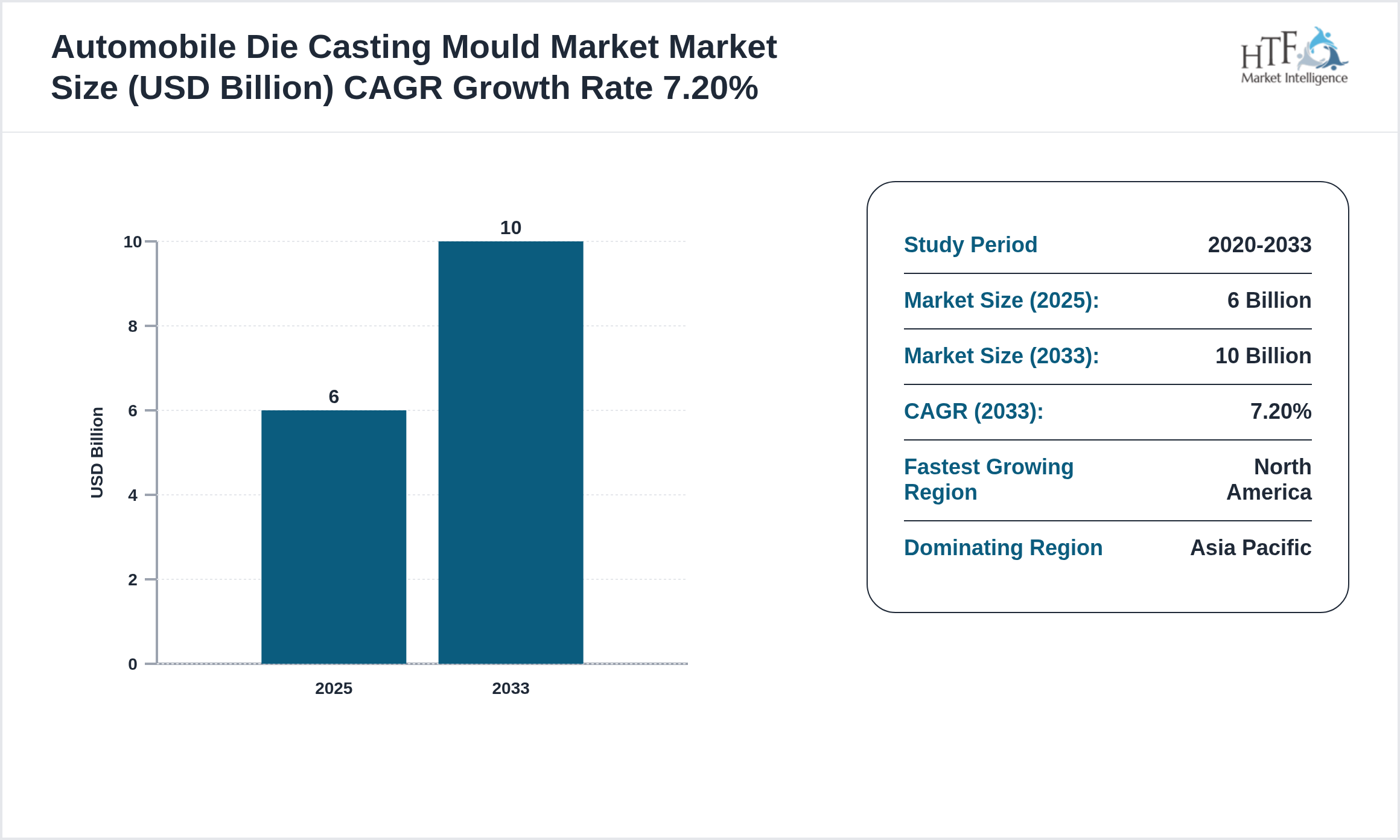

The Automobile Die Casting Mould Market is at USD 6 billion in 2025 and is expected to reach 10 billion by 2033. The Automobile Die Casting Mould Market is driven by increasing demand in end-use industries, technological advancements, research and development (R&D), economic growth, and global trade.

Automobile die casting moulds (dies) are precision-engineered tooling used to produce high-volume metal castings — typically aluminum magnesium and zinc alloy components — for engine transmission structural and body parts; dies must withstand high thermal and mechanical stresses and are designed for dimensional accuracy surface finish and efficient die-casting cycle times.

Source: HTF Market Intelligence (HTF MI)

Competitive landscape

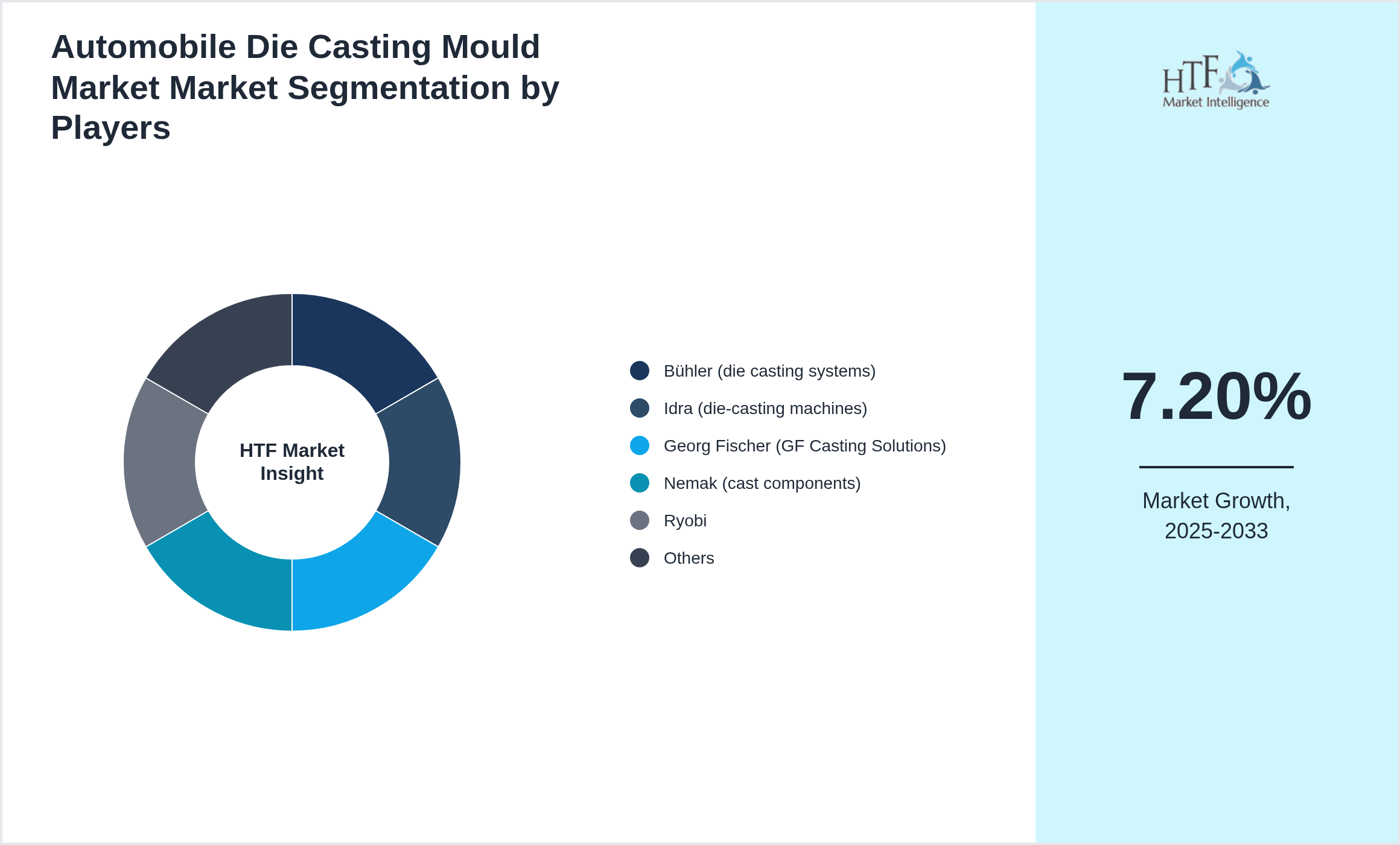

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach:

- • Bühler (die casting systems)

- • Idra (die-casting machines)

- • Georg Fischer (GF Casting Solutions)

- • Nemak (cast components)

- • Ryobi

- • Aisin Seiki (tooling adjacencies)

- • Magna International (casting div)

- • Nemak

- • Dalian Machine Works (China)

- • Endurance Technologies (India)

- • LKM

- • LKQ (aftermarket)

- • KSPG (formerly Kolbenschmidt)

- • Shilong Toolings

- • Magotteaux (adj).

Market Drivers:

Challenge Factor:

Opportunities:

Important Trend:

Regulatory Framework

- • Die casting moulds and tooling are regulated under industrial safety

- • materials handling

- • and workplace ergonomics standards

- • Compliance with ISO tooling standards

- • local machinery safety rules

- • and environmental regulations for die-casting operations is required.

Regional Insight

The Asia Pacific leads the market share, largely due to rising consumption, a growing population, and strong economic momentum that boosts demand. In contrast, the North America is emerging as the fastest-growing area, driven by rapid infrastructure development, the expansion of industrial sectors, and heightened consumer demand, making it a critical factor for future market growth. The regions covered in the report are

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

Regional Analysis

- • Asia-Pacific leads due to large automotive OEM and component manufacturing hubs

- • Europe and North America maintain demand for high-precision and lightweighting tooling

- • Growth follows aluminum die-casting adoption for ICE and EV platforms.

Market Segmentation

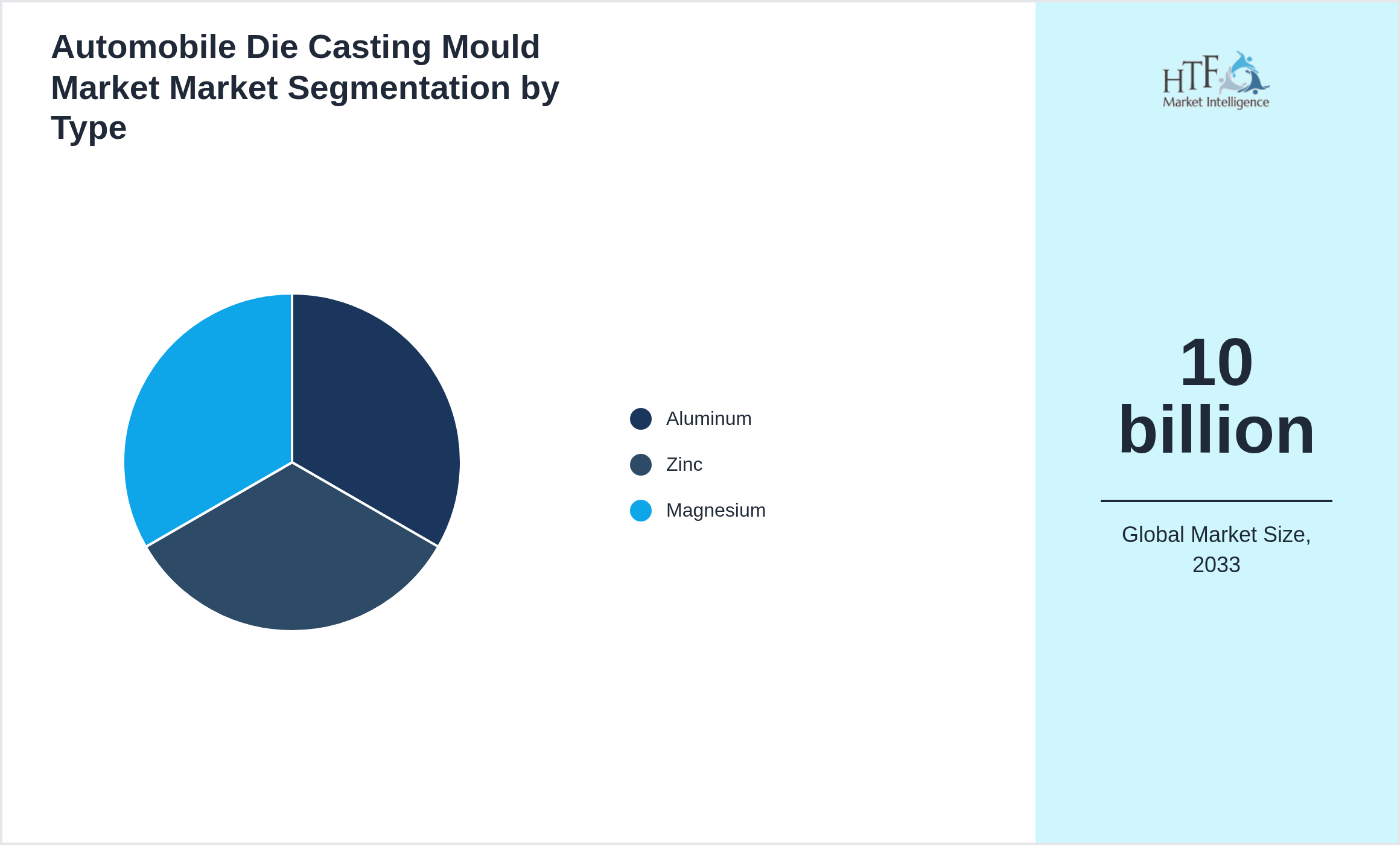

Segmentation by Type

- • Aluminum

- • Zinc

- • Magnesium

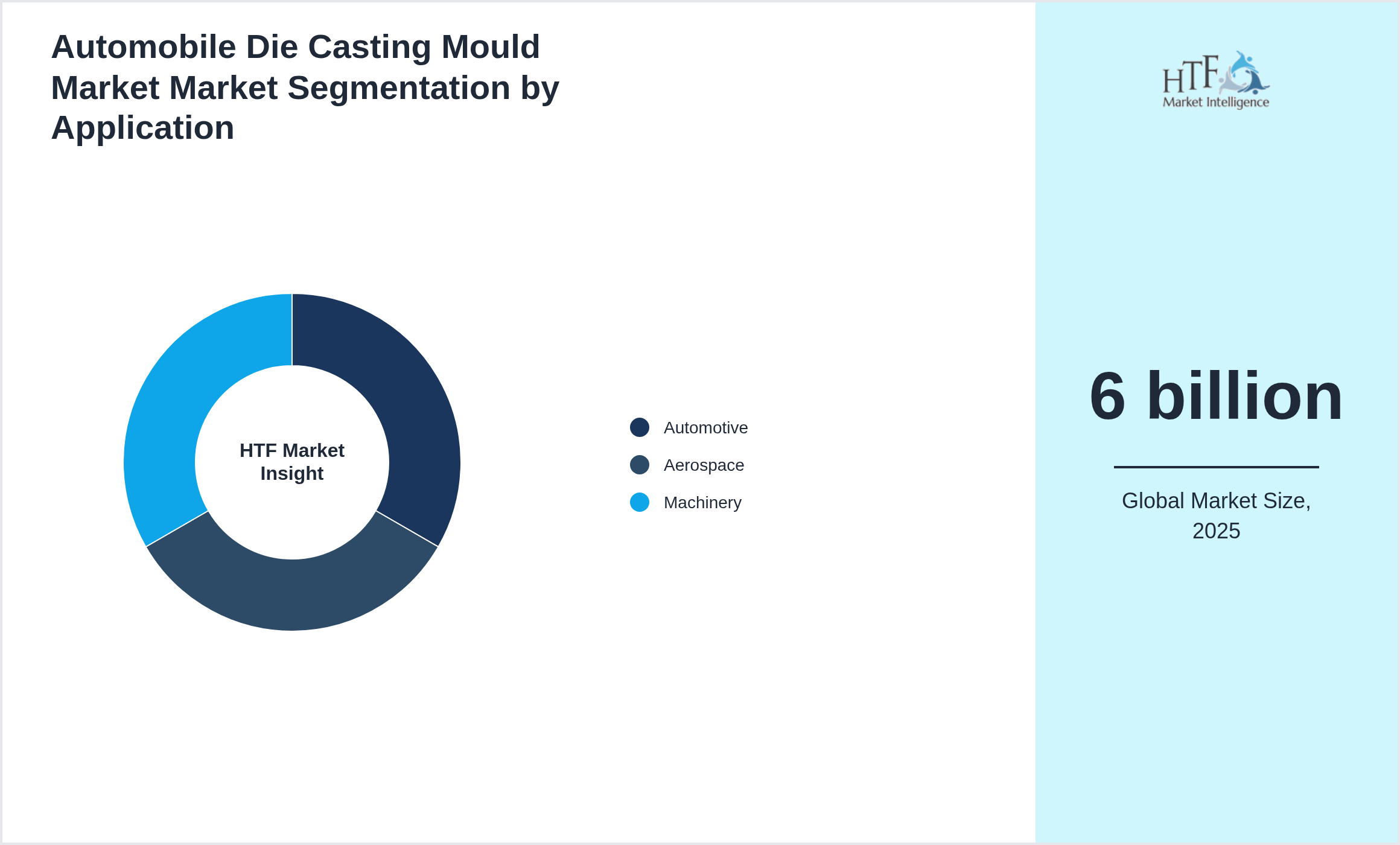

Segmentation by Application

- • Automotive

- • Aerospace

- • Machinery

Key Development Activities

Market Entropy

- • From 2022 to 2024 the automobile die casting mould market showed moderate entropy as OEM demand fluctuated with vehicle production cycles and electrification trends

- • Toolmakers competed on lead time cavity precision and thermal management capabilities

- • Regional mould makers in Asia expanded capacity while Tier-1 suppliers pushed for tighter integration and quicker design iterations.

Merger & Acquisition

- • Between 2023 and 2025 M&A activity included acquisitions of specialist mould shops by large tool and die groups to capture automotive contracts

- • Strategic deals aimed to combine rapid prototyping hardened tool coatings and captive machining capacity

- • Several consolidations focused on geographic reach into EV manufacturing hubs.

Regulatory Landscape

- • Die casting moulds and tooling are regulated under industrial safety

- • materials handling

- • and workplace ergonomics standards

- • Compliance with ISO tooling standards

- • local machinery safety rules

- • and environmental regulations for die-casting operations is required.

Patent Analysis

- • Patent filings emphasize conformal cooling

- • high-wear tool steels

- • and additive-manufactured mold inserts

- • Innovations include internal cooling channels via AM

- • coatings for reduced sticking

- • and modular mold architectures

- • The focus is on cycle time

- • part quality

- • and tool life

Investment and Funding Scenario

- • Investment is capital-intensive with funding for AM tooling

- • hardening equipment

- • and simulation software

- • Funding flows from OEMs and Tier-1 suppliers seeking faster cycles and lighter parts

- • M&A consolidates tooling houses or acquires AM capability to shorten lead times

Report Details

| Report Features | Details |

| Base Year | 2025 |

| Based Year Market Size (2025) | 6 billion |

| Historical Period | 2020 to 2025 |

| CAGR (2025 to 2033) | 7.20% |

| Forecast Period | 2026 to 2033 |

| Forecasted Period Market Size (2033) | 10 billion |

| Scope of the Report | Aluminum, Zinc, Magnesium, Automotive, Aerospace, Machinery |

| Companies Covered | Bühler (die casting systems), Idra (die-casting machines), Georg Fischer (GF Casting Solutions), Nemak (cast components), Ryobi, Aisin Seiki (tooling adjacencies), Magna International (casting div), Nemak, Dalian Machine Works (China), Endurance Technologies (India), LKM, LKQ (aftermarket), KSPG (formerly Kolbenschmidt), Shilong Toolings, Magotteaux (adj). |

| Customization Scope | 15% Free Customization |

| Delivery Format | PDF and Excel through Email |

Research Methodology

The research methodology involves several key steps to ensure comprehensive and accurate insights. First, the objectives of the research are clearly defined, focusing on aspects such as market size, growth trends, and competitive dynamics. Data collection is conducted through both primary and secondary methods. Primary research includes interviews with industry experts, surveys, and focus groups to gather firsthand information, while secondary research involves analyzing existing reports, government publications, and company filings.

The collected data is then subjected to rigorous analysis, with quantitative methods used to evaluate market size and trends and qualitative methods applied to understand industry dynamics and consumer behavior. Findings are compiled into a detailed report featuring key insights, data visualizations, and strategic recommendations. Validation is achieved through data verification and peer reviews to ensure accuracy.

Finally, the research concludes with actionable insights and recommendations, along with suggestions for future studies to address emerging trends and gaps. This methodology provides a structured approach to understanding the {keywords} and guiding strategic decisions.