Carbon Foam Market Market - Global Size & Outlook 2020-2033

Global Carbon Foam Market Market is segmented by Application (Aerospace, Automotive, Thermal Insulation), Type (Rigid, Flexible), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

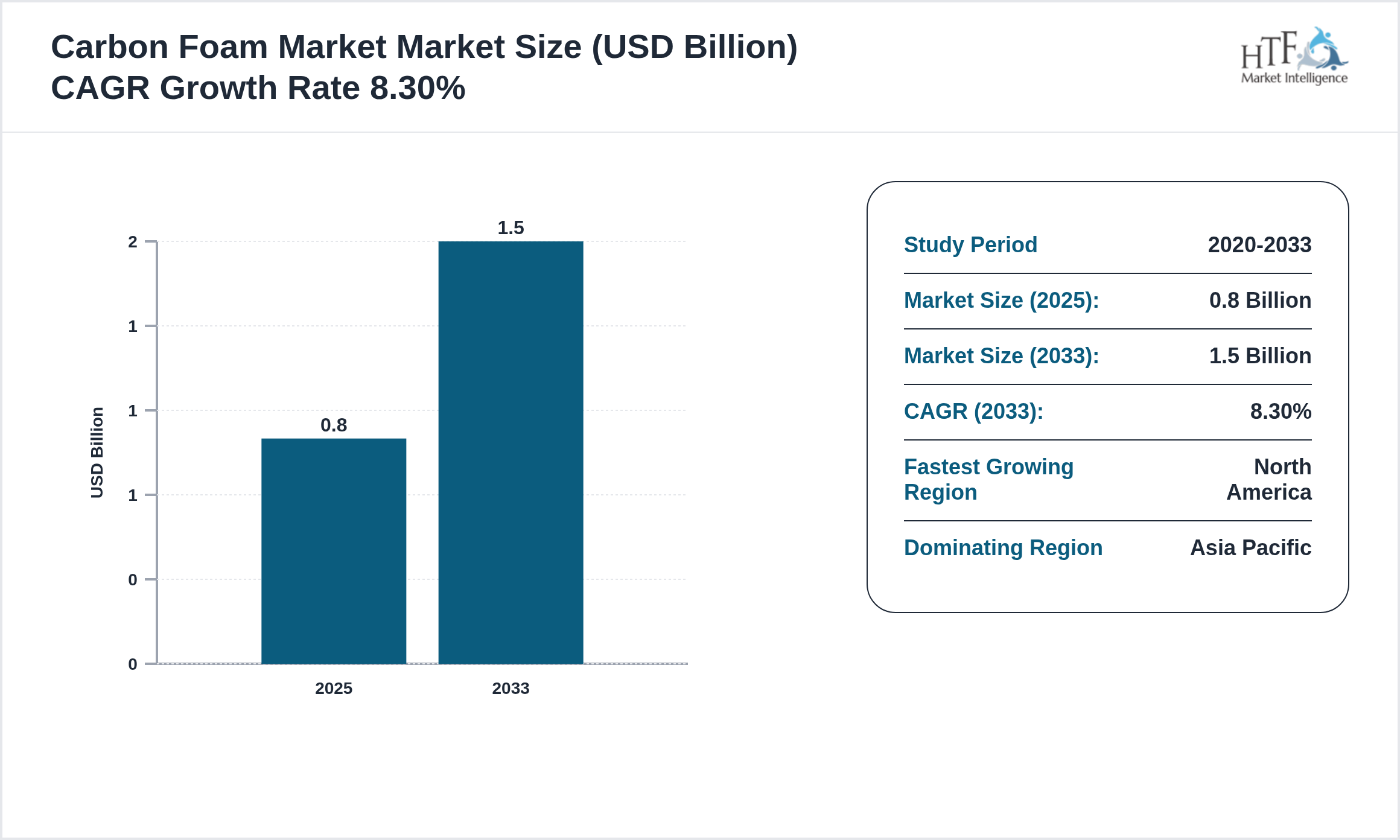

The Carbon Foam Market is at USD 800 million in 2025 and is expected to reach 1.5 billion by 2033. The Carbon Foam Market is driven by increasing demand in end-use industries, technological advancements, research and development (R&D), economic growth, and global trade.

Carbon foam (porous carbonaceous blocks produced from polymer precursors pitch or carbonized resins) is used for thermal management energy-absorbing structures electrodes for advanced batteries and fuel cells and high-temperature insulation; properties include low density high thermal conductivity (depending on structure) tunable porosity and good mechanical strength for lightweight structural uses.

Source: HTF Market Intelligence (HTF MI)

Competitive landscape

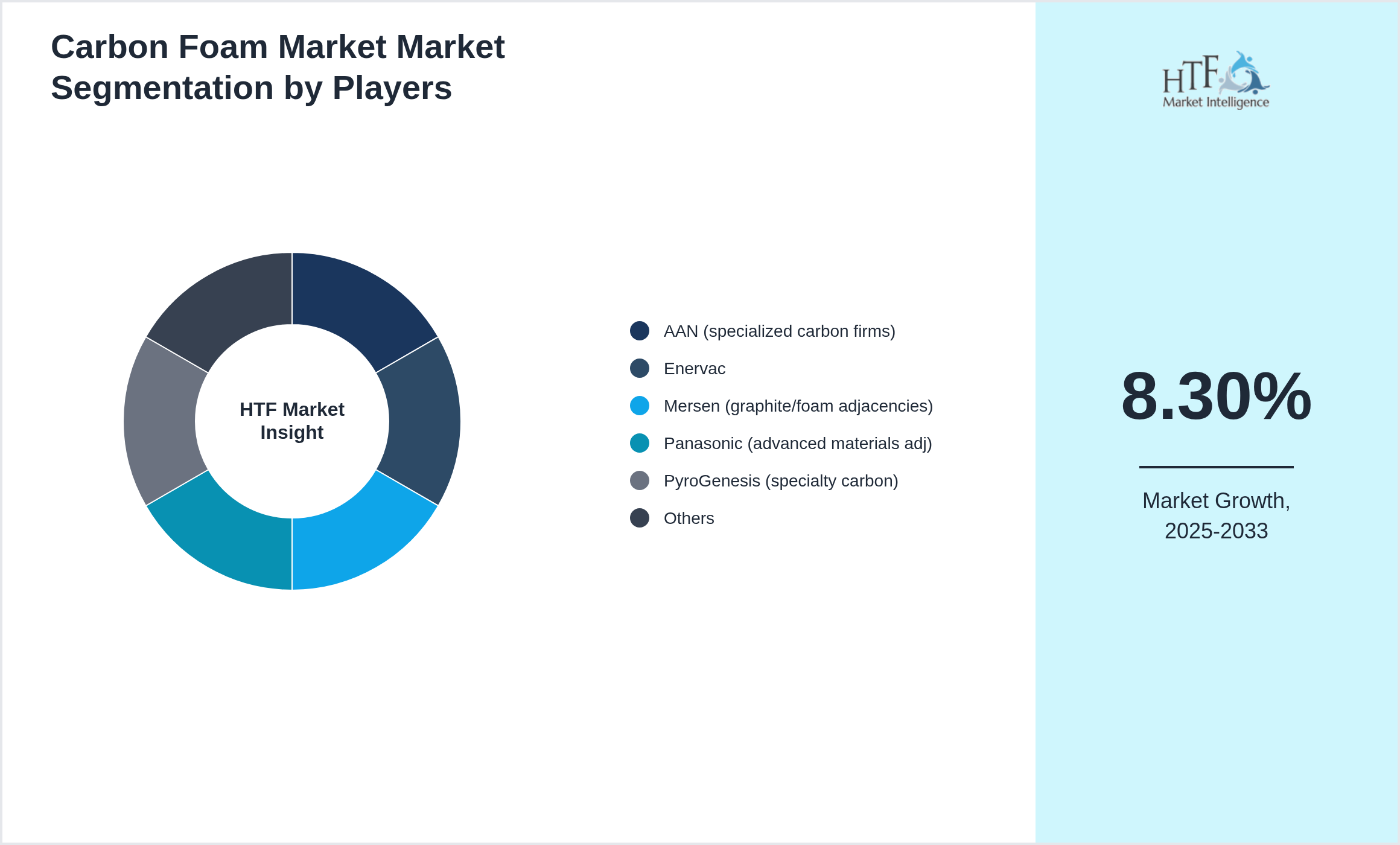

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach:

- • AAN (specialized carbon firms)

- • Enervac

- • Mersen (graphite/foam adjacencies)

- • Panasonic (advanced materials adj)

- • PyroGenesis (specialty carbon)

- • Carbolex

- • ERG (materials)

- • Poco Graphite (graphite foams)

- • ZCarbon

- • Sekisui (adj materials)

- • Nanoshell developers

- • ZGF

- • Graphite India (adj)

- • SGL Carbon (graphite/foam).

What are the Key Growth Drivers of the Carbon Foam Market Market?

What Risks could Impact the future of the Carbon Foam Market Market?

What Untapped Segments of Carbon Foam Market Market offer the Greatest Growth Potential?

What are the Key Trends in Carbon Foam Market Market to Watch through 2033?

Regulatory Framework

- • Carbon foam products are regulated under material safety

- • thermal/fire-performance testing

- • and industrial application standards

- • Compliance with ISO/ASTM material tests

- • REACH (if chemical content relevant)

- • and local industrial safety regulations is required.

Regional Insight

The Asia Pacific leads the market share, largely due to rising consumption, a growing population, and strong economic momentum that boosts demand. In contrast, the North America is emerging as the fastest-growing area, driven by rapid infrastructure development, the expansion of industrial sectors, and heightened consumer demand, making it a critical factor for future market growth. The regions covered in the report are

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

Regional Analysis

- • Asia-Pacific is growing due to industrial and thermal management applications

- • North America and Europe maintain demand in aerospace electronics and filtration

- • Specialty high-performance foam segments expand with R&D.

Market Segmentation

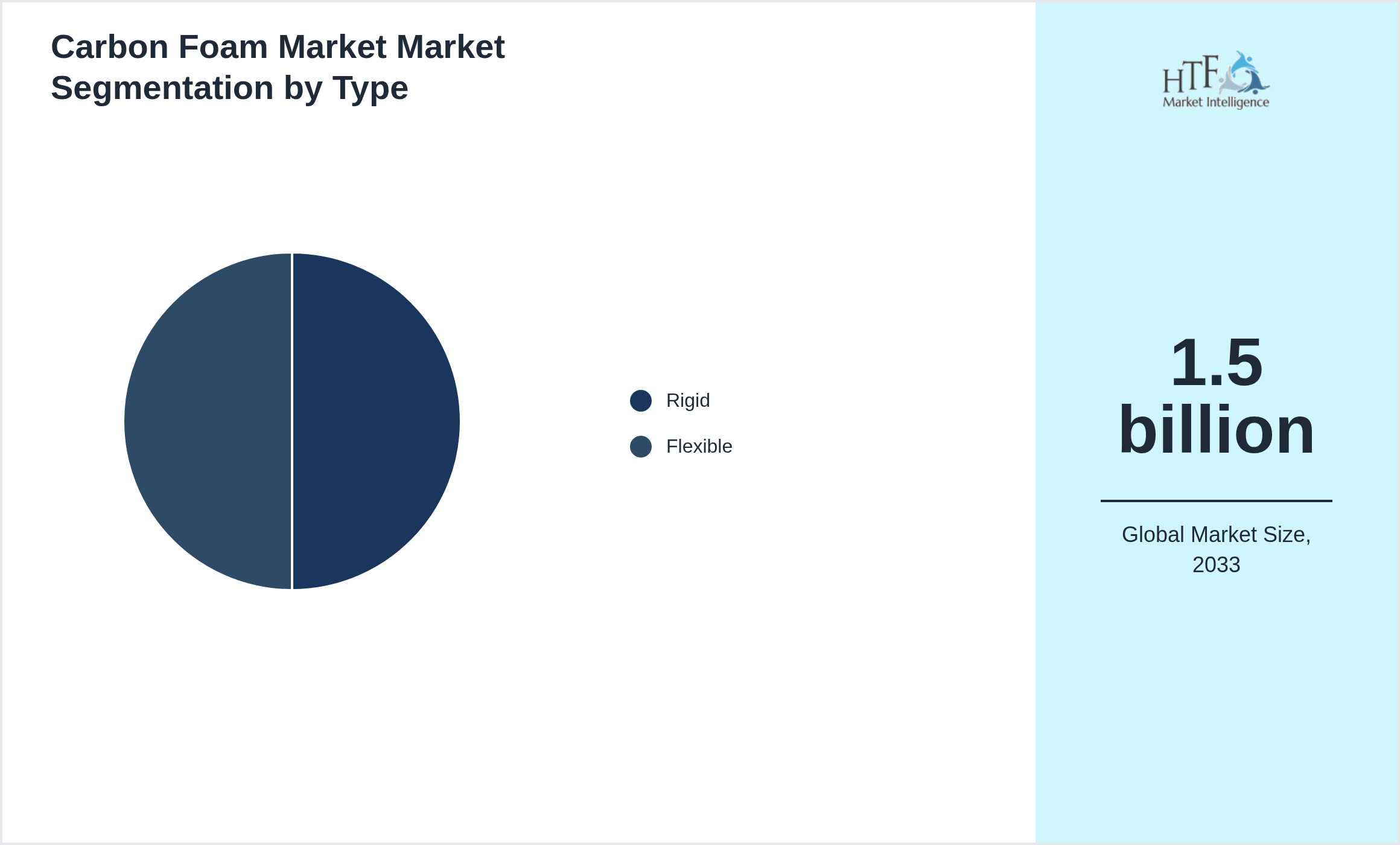

Segmentation by Type

- • Rigid

- • Flexible

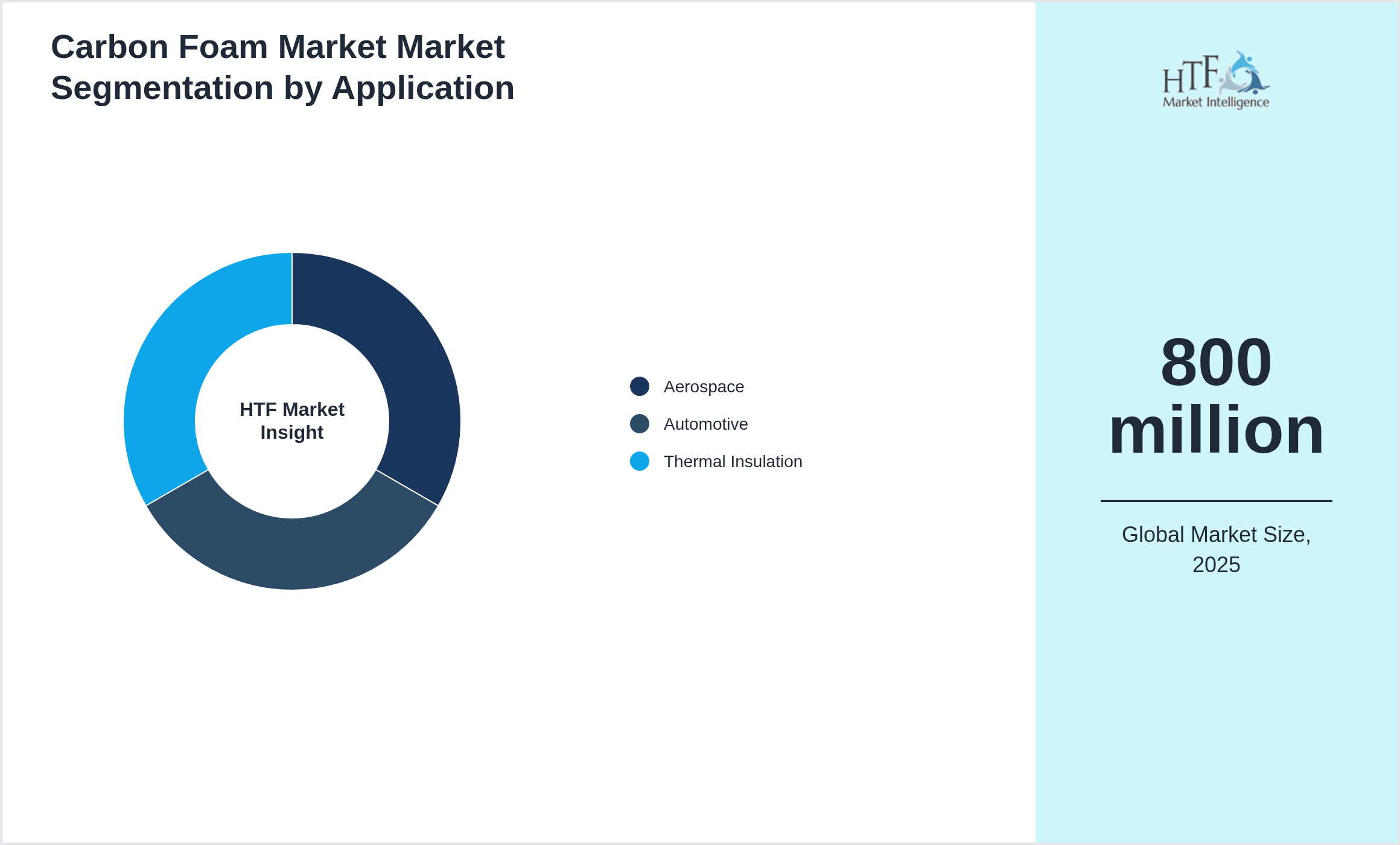

Segmentation by Application

- • Aerospace

- • Automotive

- • Thermal Insulation

Key Development Activities

Market Entropy

- • From 2022 to 2024 the carbon foam market exhibited moderate entropy as niche applications in thermal management aerospace and filtration expanded unevenly

- • Small specialized manufacturers competed on porosity control thermal conductivity and oxidation resistance

- • Qualification cycles for aerospace and energy applications lengthened time-to-revenue and added uncertainty.

Merger & Acquisition

- • Between 2023 and 2025 M&A involved materials firms acquiring carbon foam producers to integrate advanced thermal solutions

- • Strategic purchases targeted IP for processing and high-temperature treatments

- • Consolidation aimed to scale production for industrial and defense qualification programs.

Regulatory Landscape

- • Carbon foam products are regulated under material safety

- • thermal/fire-performance testing

- • and industrial application standards

- • Compliance with ISO/ASTM material tests

- • REACH (if chemical content relevant)

- • and local industrial safety regulations is required.

Patent Analysis

- • Patent filings emphasize porous carbonization routes

- • templating for controlled pore-size

- • and high-temperature stability for insulation/energy applications

- • Innovations include graphene-enhanced foams

- • solvent-free templating

- • and scalable molding techniques

- • The focus is on thermal resistance

- • mechanical strength

- • and consistent pore architecture

Investment and Funding Scenario

- • Investment targets pilot-scale production

- • application validation in batteries/insulation

- • and scale-up of templating processes

- • Funding often comes from strategic industrial partners and grants for advanced materials

- • M&A can fold novel foam tech into larger materials portfolios or application OEMs

Report Details

| Report Features | Details |

| Base Year | 2025 |

| Based Year Market Size (2025) | 800 million |

| Historical Period | 2020 to 2025 |

| CAGR (2025 to 2033) | 8.30% |

| Forecast Period | 2026 to 2033 |

| Forecasted Period Market Size (2033) | 1.5 billion |

| Scope of the Report | Rigid, Flexible, Aerospace, Automotive, Thermal Insulation |

| Companies Covered | AAN (specialized carbon firms), Enervac, Mersen (graphite/foam adjacencies), Panasonic (advanced materials adj), PyroGenesis (specialty carbon), Carbolex, ERG (materials), Poco Graphite (graphite foams), ZCarbon, Sekisui (adj materials), Nanoshell developers, ZGF, Graphite India (adj), SGL Carbon (graphite/foam). |

| Customization Scope | 15% Free Customization |

| Delivery Format | PDF and Excel through Email |

Research Methodology

The research methodology involves several key steps to ensure comprehensive and accurate insights. First, the objectives of the research are clearly defined, focusing on aspects such as market size, growth trends, and competitive dynamics. Data collection is conducted through both primary and secondary methods. Primary research includes interviews with industry experts, surveys, and focus groups to gather firsthand information, while secondary research involves analyzing existing reports, government publications, and company filings.

The collected data is then subjected to rigorous analysis, with quantitative methods used to evaluate market size and trends and qualitative methods applied to understand industry dynamics and consumer behavior. Findings are compiled into a detailed report featuring key insights, data visualizations, and strategic recommendations. Validation is achieved through data verification and peer reviews to ensure accuracy.

Finally, the research concludes with actionable insights and recommendations, along with suggestions for future studies to address emerging trends and gaps. This methodology provides a structured approach to understanding the {keywords} and guiding strategic decisions.

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.