Global Constructional Steel Electrode Market Market Size, Growth & Revenue 2025-2033

Global Constructional Steel Electrode Market Market is segmented by Application (Construction, Manufacturing, Welding), Type (Carbon Steel, Stainless Steel), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

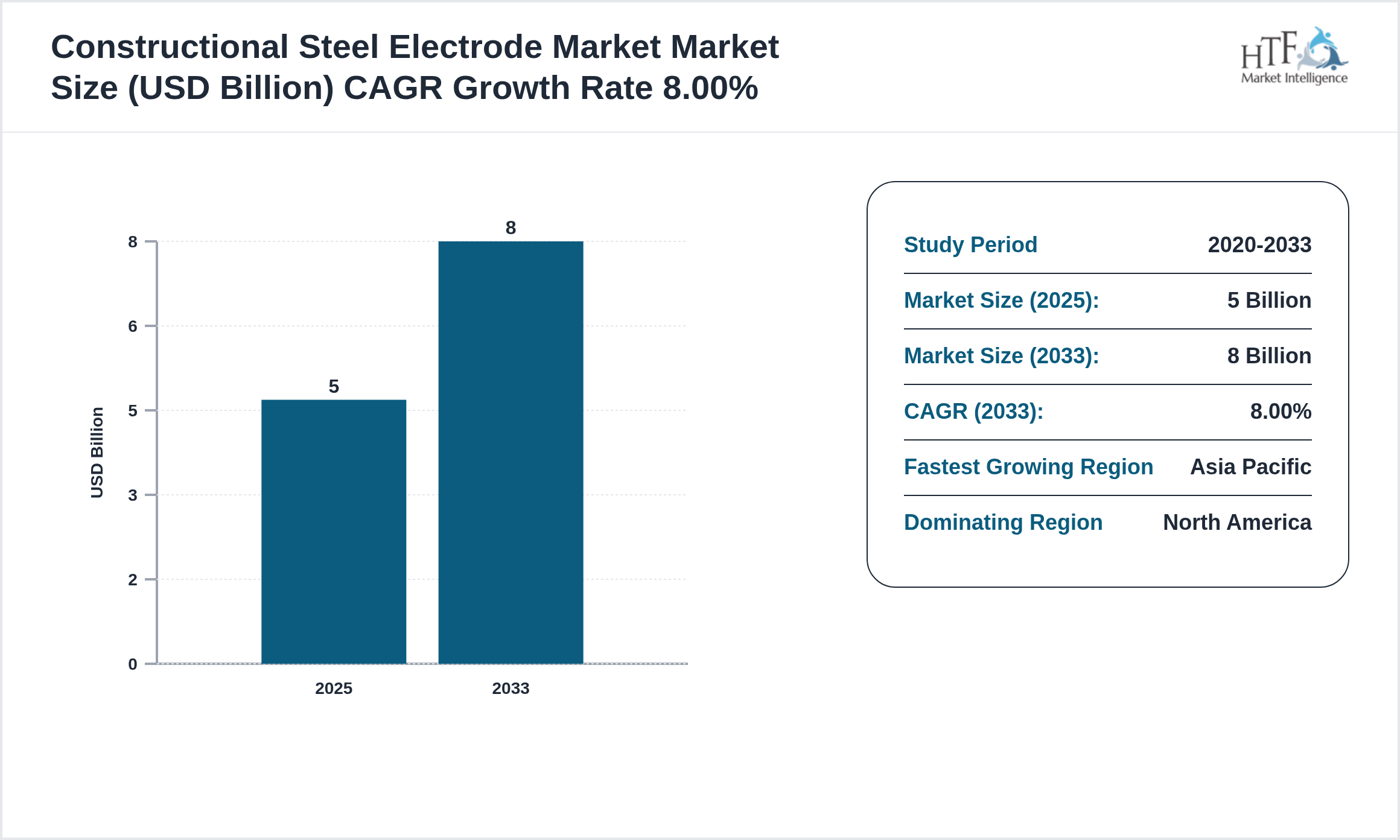

The Constructional Steel Electrode Market market is expected to reach 8 billion by 2033 and is growing at a CAGR of8.00% between 2025 and 2033.

Constructional steel electrodes (welding electrodes for structural steel) include covered stick electrodes (SMAW) flux-cored wires (FCAW) welding rods and electrodes designed for structural welding in construction bridges heavy equipment and pipeline fabrication; electrodes are specified by strength toughness deposit chemistry and suitability for positional welding and outdoor conditions. Requirements include low-hydrogen formulations for crack resistance matching of parent-metal strength and certified consumables for code-compliant construction work under standards like AWS EN and ISO.

Source: HTF Market Intelligence (HTF MI)

Market Size & Forecast

Market Segmentation

Selecting segmentation criteria in Lincoln Electric, ESAB, Bohler Welding (voestalpine), ITW Welding (Arcweld/ Hobart), Kobelco Welding, Jindal Stainless (adj), Nippon Steel (consumables adj), D&H, Shaanxi Xingyuan, Zhangjiagang Jinfeng, Tata Steel (consumables adj), Haynes (specialty), Bekaert (wire), Weldcote Metals (distribution), Faraday Welding, Panasonic Welding Systems (industrial). involves several key steps. Researchers begin by defining their objectives, such as understanding consumer behavior or identifying market opportunities. They then gather relevant data on demographics, psychographics, and buying behavior. Next, they identify segmentation variables like age, location, lifestyle, and purchase patterns. Using analytical tools, they analyze the data to find distinct market segments and evaluate their attractiveness based on size, growth potential, and alignment with business goals. Detailed profiles are created for each segment, and the most promising ones are selected for targeting. Finally, tailored marketing strategies are developed, and the performance of these strategies is monitored and adjusted as needed. This process ensures that segmentation effectively identifies valuable market opportunities and aligns with strategic goals.

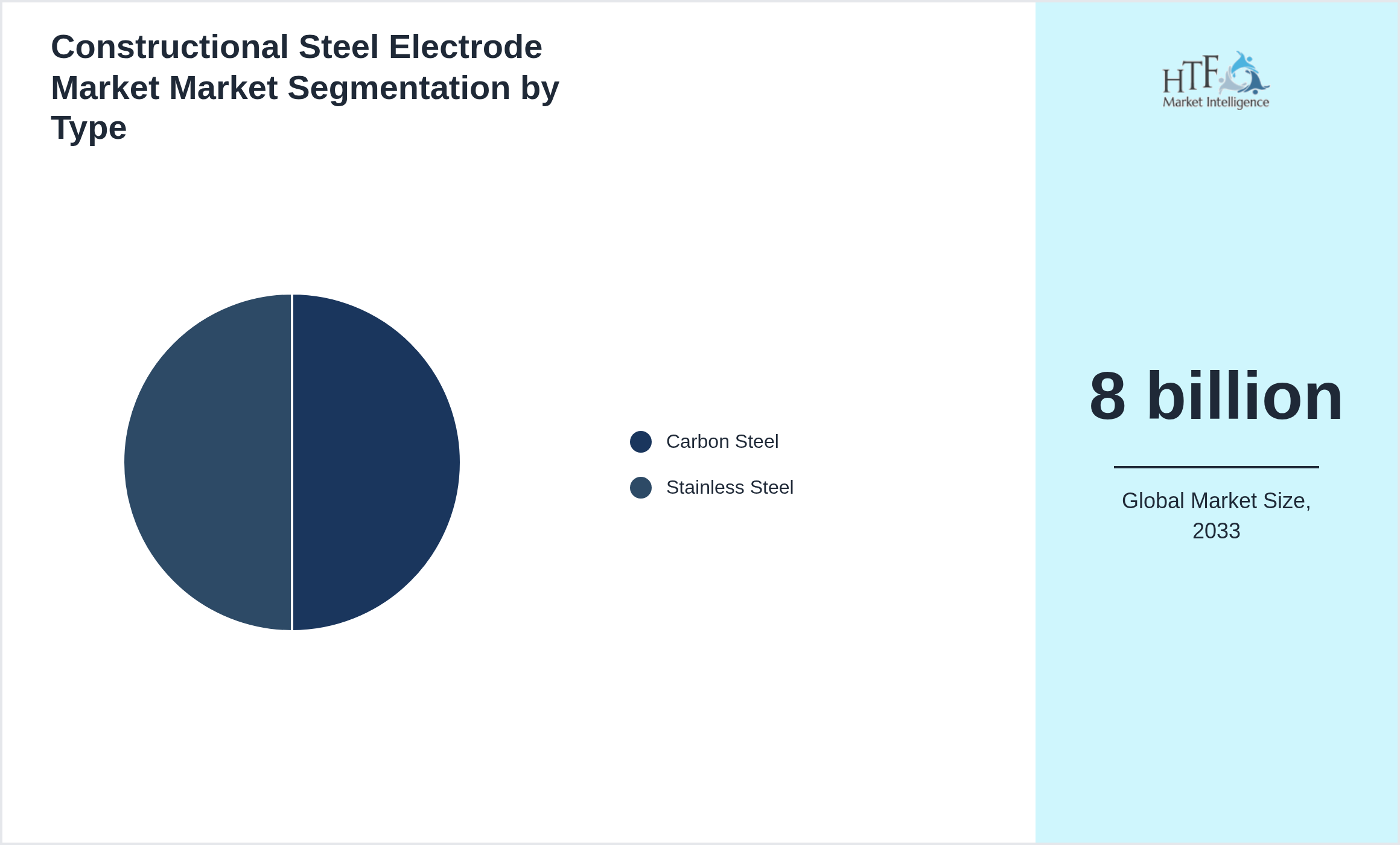

Segmentation by Type

- • Carbon Steel

- • Stainless Steel

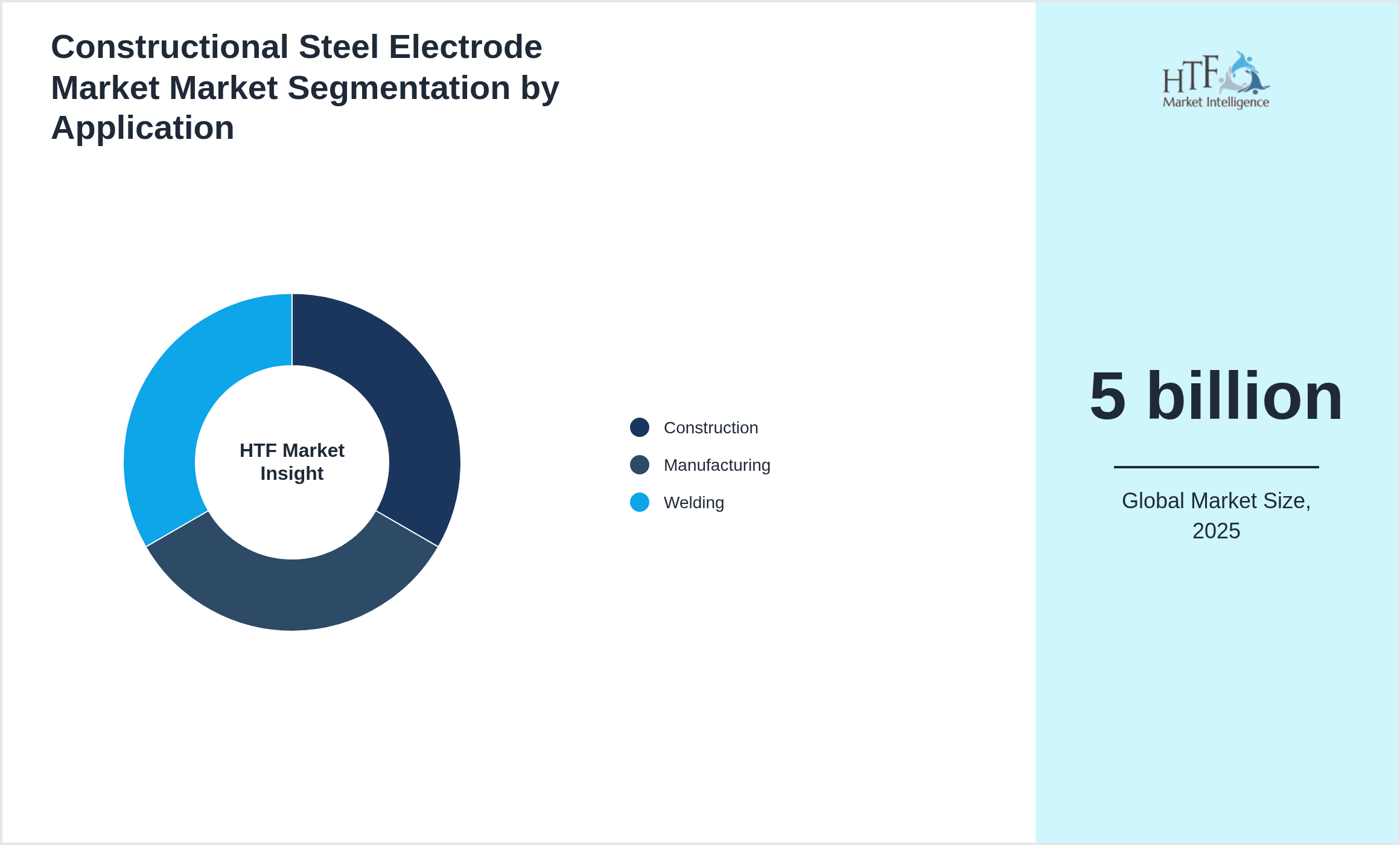

Segmentation by Application

- • Construction

- • Manufacturing

- • Welding

Constructional Steel Electrode Market Market Dynamics

TheConstructional Steel Electrode Market is driven by factors such as increasing demand in end-use industries, technological advancements, research and development (R&D), economic growth, and increasing global trade.

Influencing Trend:

- • Shift toward flux-cored and metal-cored wires for high-productivity construction welding is trending

- • Development of low-splash low-spatter electrode chemistries improves productivity and reduces post-weld cleanup

- • Electrodes tailored for high-strength high-toughness steels and HSLA grades are in demand

- • Robotic and automated welding cell optimization pushes demand for consistent machine-feedable flux formulations

- • Coated electrodes with enhanced storage stability and low-hydrogen characteristics are increasingly specified for field work.

- • Infrastructure investment and construction activity in emerging markets drive demand for structural welding consumables

- • Replacement and maintenance of aging steel infrastructure sustain steady electrode consumption

- • Demand for low-hydrogen high-toughness electrodes grows with stricter structural codes and fatigue-resistant designs

- • Mechanization of welding and higher-throughput construction methods create demand for flux-cored and mechanized consumables

- • Quality-certification and project-level traceability requirements (certified batches) influence procurement.

- • Raw-material volatility for alloying elements and flux components affects pricing and margin for electrode makers

- • Field conditions (moisture) can compromise electrode storage and performance increasing returns and rework cost

- • Qualification to strict structural codes and approvals for large infrastructure projects lengthens sales cycles

- • Competition from low-cost regional manufacturers pressures pricing in commodity segments

- • Labor shortages and mechanization reduce stick electrode usage in some markets shifting demand to wire products requiring different system investments.

- • Supplying certified electrode bundles and onsite welding-consumable logistics to EPC contractors and bridge-builders creates recurring B2B revenue

- • Developing low-hydrogen high-toughness electrode lines for offshore and seismic-prone construction commands premium pricing

- • Partnering with automation integrators to qualify wires/electrodes for robotic welding cells secures OEM-spec channels

- • Providing bundled consumables + training + QC documentation for large construction projects increases stickiness

- • Localized production near major construction hubs reduces logistics cost and supports rapid response.

Regional Insight

The North Americaregion holds a dominant market share, primarily driven by growing consumption patterns, a rising population, and robust economic activity that fuels market demand. Meanwhile, the Asia Pacific Region is experiencing the fastest growth, propelled by increasing infrastructure developments, expanding industrial activities, and a surge in consumer demand, positioning it as a key driver for future market expansion.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

- • North America experiences steady demand for constructional steel electrodes due to ongoing infrastructure repair and industrial construction with the US leading in adoption of advanced welding solutions

- • Europe benefits from sustainable construction projects strict welding quality standards and ongoing transportation network expansions

- • Asia-Pacific dominates global demand fueled by rapid industrialization high-rise construction and government-backed infrastructure investments in countries like China and India

Key Players

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach:

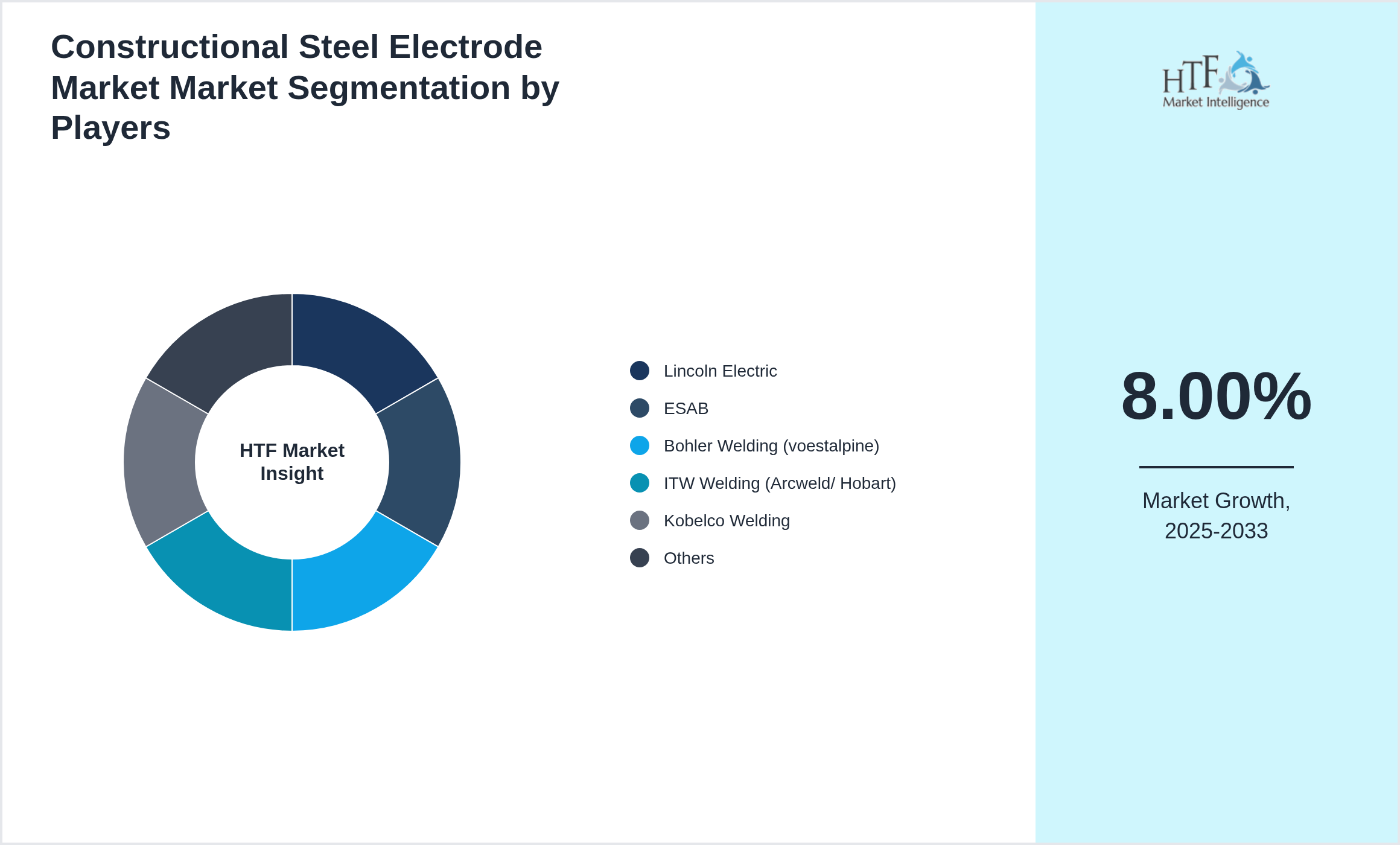

- • Lincoln Electric

- • ESAB

- • Bohler Welding (voestalpine)

- • ITW Welding (Arcweld/ Hobart)

- • Kobelco Welding

- • Jindal Stainless (adj)

- • Nippon Steel (consumables adj)

- • D&H

- • Shaanxi Xingyuan

- • Zhangjiagang Jinfeng

- • Tata Steel (consumables adj)

- • Haynes (specialty)

- • Bekaert (wire)

- • Weldcote Metals (distribution)

- • Faraday Welding

- • Panasonic Welding Systems (industrial).

Regulatory Framework

The regulatory framework for the Constructional Steel Electrode Market ensures product safety, fair competition, and consumer protection. It encompasses setting standards for product quality and safety, enforcing truthful advertising and labeling, and implementing environmental sustainability practices. Regulations include robust procedures for product recalls, data protection, and anti-competitive practices, while also overseeing import/export controls and intellectual property rights. Regulatory bodies enforce these rules through inspections and penalties, and consumer education programs help individuals make informed decisions. This framework aims to protect consumers, promote fair market conditions, and encourage ethical business practices.

- • The constructional steel electrode market is governed by welding safety standards

- • metallurgical quality requirements

- • and occupational hazard regulations

- • In the US

- • AWS (American Welding Society) standards ensure product classification and performance

- • Europe enforces EN ISO 2560 standards for electrode quality and safety

- • Asia-Pacific markets follow both international welding codes and localized construction safety norms

Competitive Insights

The key players in the Constructional Steel Electrode Market are intensifying their focus on research and development (R&D) activities to innovate and stay competitive. Major companies, such as Lincoln Electric, ESAB, Bohler Welding (voestalpine), ITW Welding (Arcweld/ Hobart), Kobelco Welding, Jindal Stainless (adj), Nippon Steel (consumables adj), D&H, Shaanxi Xingyuan, Zhangjiagang Jinfeng, Tata Steel (consumables adj), Haynes (specialty), Bekaert (wire), Weldcote Metals (distribution), Faraday Welding, Panasonic Welding Systems (industrial)., are heavily investing in R&D to develop new products and improve existing ones. This strategic emphasis on innovation is driving significant advancements in product formulation and the introduction of sustainable and eco-friendly products.

In addition to R&D and acquisitions, there is a notable shift towards green investments among key players in the consumer goods industry. Companies are increasingly committing resources to sustainable practices and the development of environmentally friendly products. This green investment is in response to growing consumer demand for sustainable solutions and stringent environmental regulations. By prioritizing sustainability, these companies are not only contributing to environmental protection but also positioning themselves as leaders in the green movement, thereby fueling market growth.

Merger Acquisition

- • Welding conglomerates purchased regional electrode plants to broaden footprints

- • Vertical integration moves secured core wires and fluxes

- • Distributors consolidated to gain national tender leverage

- • Transactions prioritized seismic-grade approvals and automated baking logistics.

Patent Analysis

- • Patent activity focuses on alloy-coated electrodes

- • lower-spatter formulations

- • and coatings that improve weld penetration

- • Innovations include flux chemistries for specific steel grades and low-smoking binders for operator safety

- • The focus is on weld quality

- • operator health

- • and compatibility with automated welding systems

Investment and Funding Scenario

- • Investment is steady from industrial chemical firms and welding groups funding process R&D and automation compatibility trials

- • Funding supports qualification programs with major fabricators and approvals for critical structures

- • M&A consolidates consumable lines or acquires niche electrode chemistries

Market Entropy

- • Entropy was moderate as infrastructure recovery and shipbuilding cycles lifted demand across low-hydrogen and rutile electrodes

- • Local brands competed on weld quality moisture resistance and packaging integrity

- • Price movements followed steel and flux minerals spurring frequent tender re-bids

- • Certification to AWS/EN standards remained a key differentiator

- • .

Report Infographics:

| Report Features | Details |

| Base Year | 2025 |

| Based Year Market Size 2025 | 5 billion |

| Historical Period Market Size 2020 | USD Million ZZ |

| CAGR (2025 to 2033) | 8.00% |

| Forecast Period | 2025 to2033 |

| Forecasted Period Market Size 2033 | 8 billion |

| Scope of the Report | Carbon Steel, Stainless Steel, Construction, Manufacturing, Welding |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Year-on-Year Growth | 7.50% |

| Companies Covered | Lincoln Electric, ESAB, Bohler Welding (voestalpine), ITW Welding (Arcweld/ Hobart), Kobelco Welding, Jindal Stainless (adj), Nippon Steel (consumables adj), D&H, Shaanxi Xingyuan, Zhangjiagang Jinfeng, Tata Steel (consumables adj), Haynes (specialty), Bekaert (wire), Weldcote Metals (distribution), Faraday Welding, Panasonic Welding Systems (industrial). |

| Customization Scope | 15% Free Customization (For EG) |

| Delivery Format | PDF and Excel through Email

Want to Buy Specific Sections of This Report?

|

Research Methodology

The research methodology for the consumer goods industry involves several key steps to ensure comprehensive and actionable insights. First, the research objectives are clearly defined, focusing on aspects like consumer behavior, market opportunities, competitive dynamics, or regulatory impacts. A thorough literature review follows, drawing from academic journals, industry reports, government publications, and market analyses to establish a knowledge base and identify research gaps. Data collection encompasses both primary methods, such as surveys, interviews, and focus groups with consumers and industry experts, and secondary methods, including analysis of market reports, government data, and industry publications. Quantitative data is analyzed using statistical tools to identify patterns and market segments, while qualitative data from interviews and focus groups is examined to extract key themes and insights.

The market is then segmented based on demographics, psychographics, geography, and purchasing behavior, and competitive analysis is conducted to evaluate key players' strategies and strengths. Trend analysis identifies current and emerging industry trends. Findings are compiled into a detailed report with data visualizations and strategic recommendations. The research is validated and refined through cross-checking and expert feedback, and a framework for continuous monitoring is established to keep the research current and relevant.