Precision Agriculture Systems Market - Global Growth Opportunities 2020-2033

Global Precision Agriculture Systems Market is segmented by Application (Row crops, Specialty crops, Dairy/livestock, Greenhouses, Large farms, Smallholders, Cooperatives), Type (GPS guidance, Variable rate tech, Soil sensors, Drones, Imagery/NDVI, Auto-steer, Yield monitors, Farm management software, IoT gateways, Robotics), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

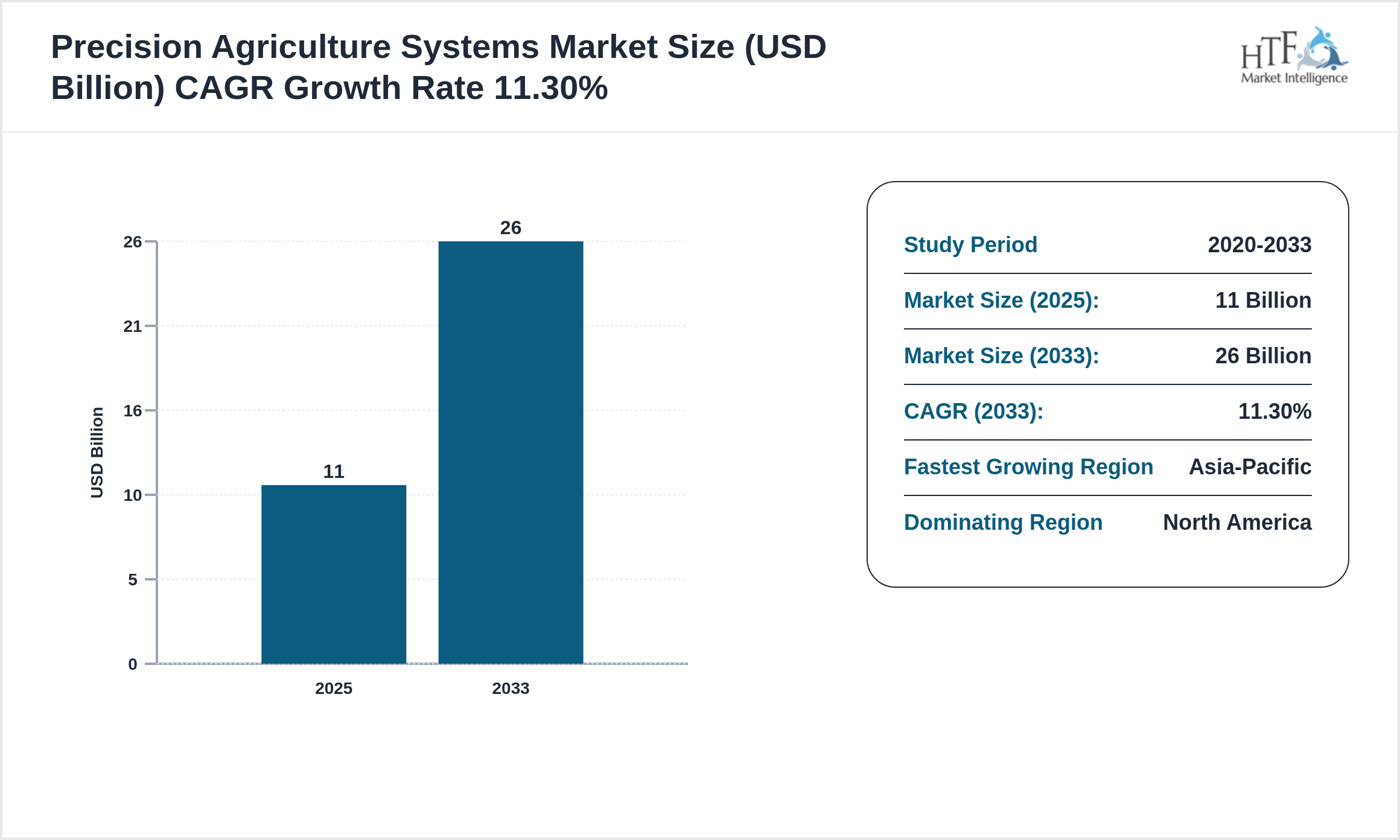

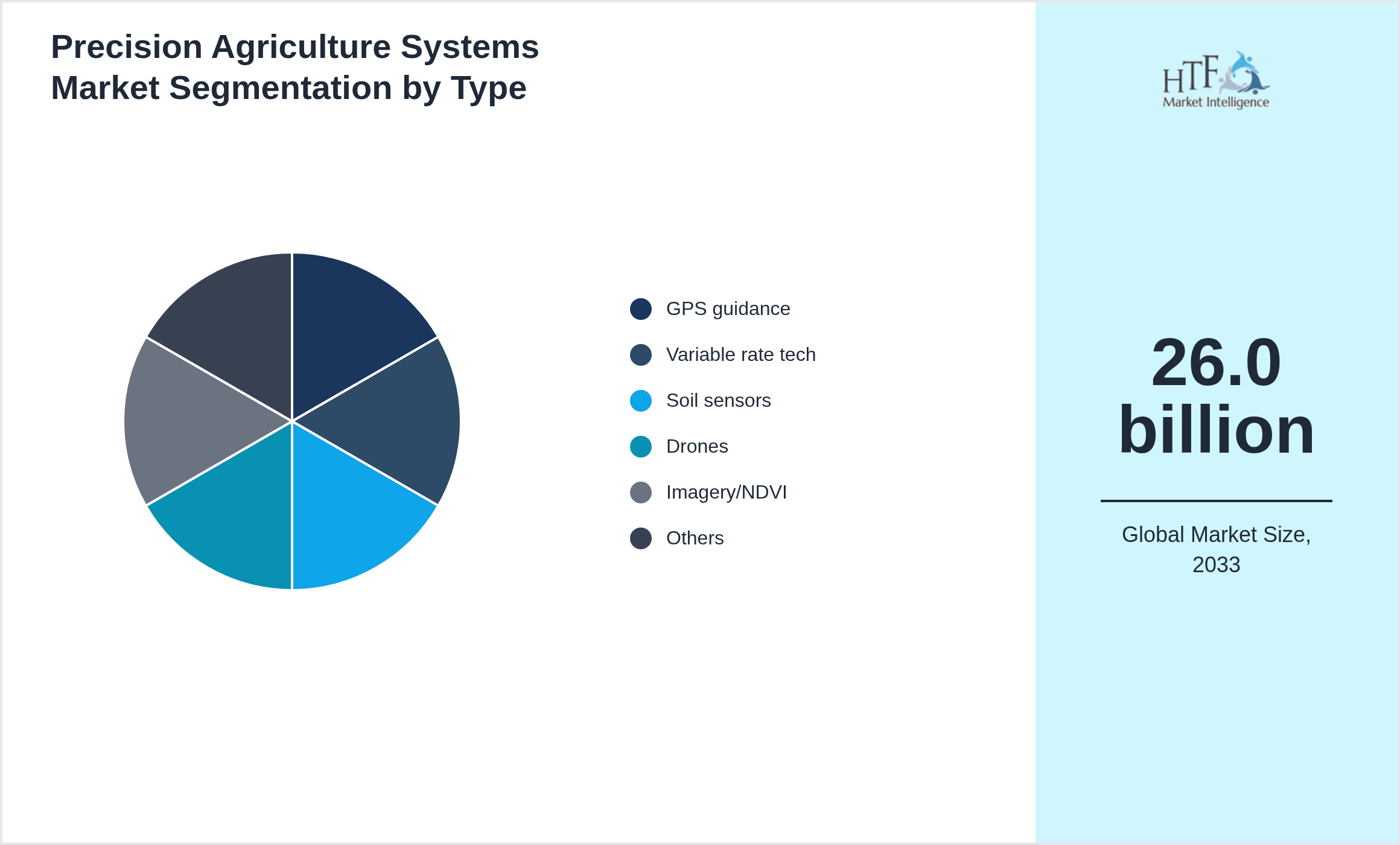

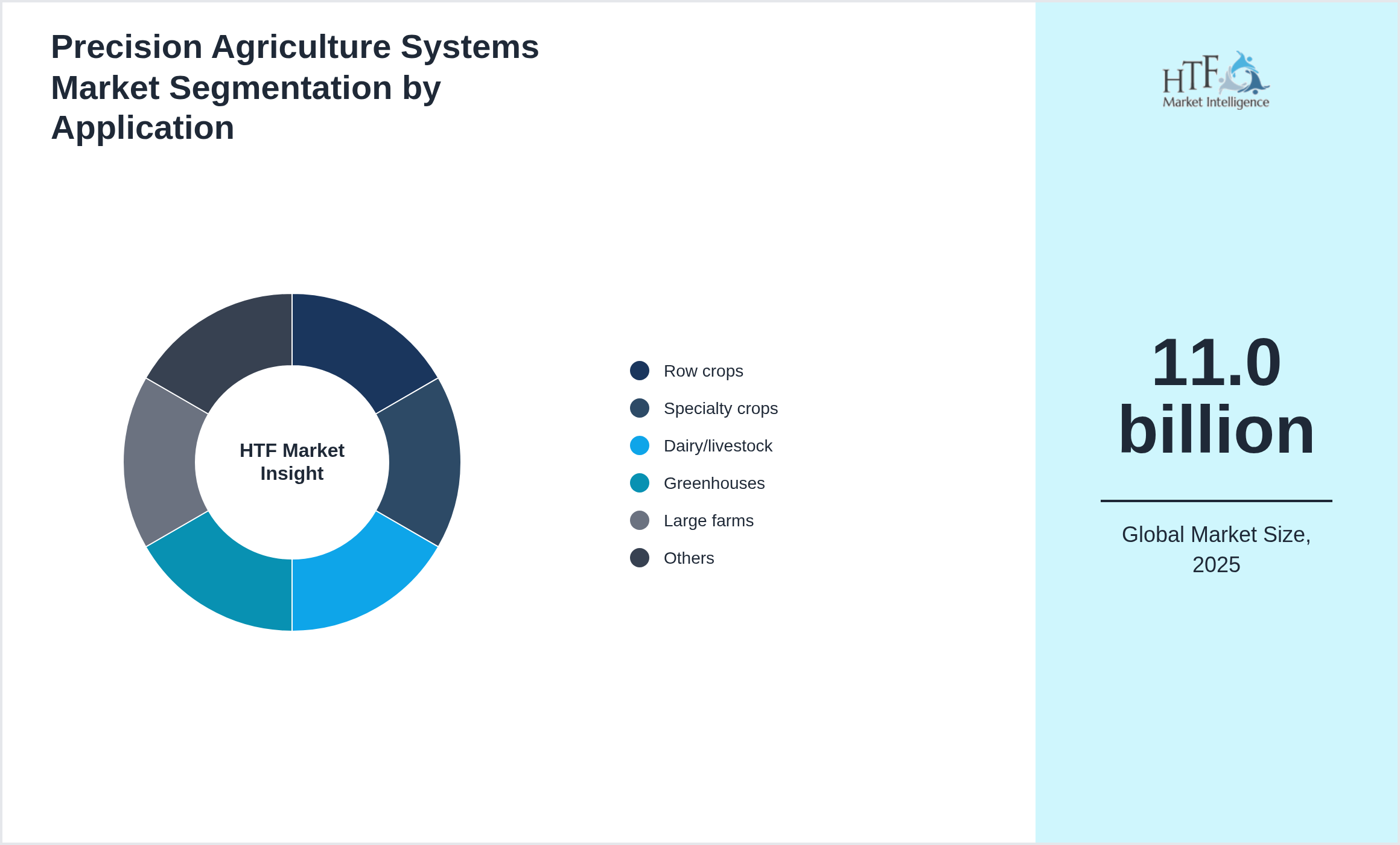

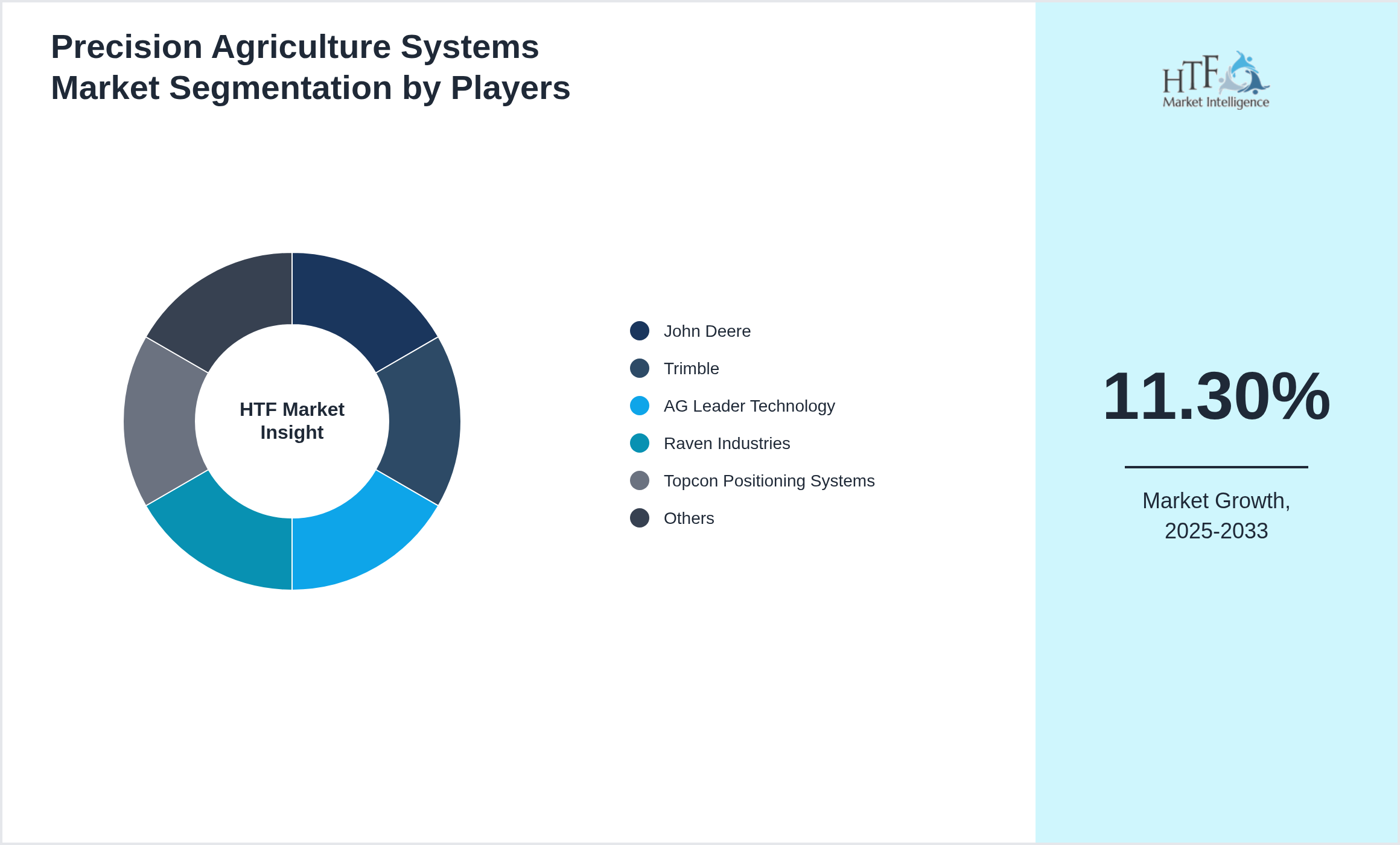

The Precision Agriculture Systems market is expected to reach 26.0 billion by 2033 and is growing at a CAGR of11.30% between 2025 and 2033.

This market involves technologies for data-driven farming including sensors GPS drones and analytics to improve crop yield resource efficiency and sustainability. Rising food demand technological adoption and smart farming initiatives drive growth.

Source: HTF Market Intelligence (HTF MI)

Market Size & Forecast

Market Segmentation

Selecting segmentation criteria in John Deere, Trimble, AG Leader Technology, Raven Industries, Topcon Positioning Systems, AGCO Corporation, Climate FieldView, Bayer CropScience, CNH Industrial, Hexagon Agriculture involves several key steps. Researchers begin by defining their objectives, such as understanding consumer behavior or identifying market opportunities. They then gather relevant data on demographics, psychographics, and buying behavior. Next, they identify segmentation variables like age, location, lifestyle, and purchase patterns. Using analytical tools, they analyze the data to find distinct market segments and evaluate their attractiveness based on size, growth potential, and alignment with business goals. Detailed profiles are created for each segment, and the most promising ones are selected for targeting. Finally, tailored marketing strategies are developed, and the performance of these strategies is monitored and adjusted as needed. This process ensures that segmentation effectively identifies valuable market opportunities and aligns with strategic goals.

Segmentation by Type

- • GPS guidance

- • Variable rate tech

- • Soil sensors

- • Drones

- • Imagery/NDVI

- • Auto-steer

- • Yield monitors

- • Farm management software

- • IoT gateways

- • Robotics

Segmentation by Application

- • Row crops

- • Specialty crops

- • Dairy/livestock

- • Greenhouses

- • Large farms

- • Smallholders

- • Cooperatives

Precision Agriculture Systems Market Dynamics

ThePrecision Agriculture Systems is driven by factors such as increasing demand in end-use industries, technological advancements, research and development (R&D), economic growth, and increasing global trade.

Influencing Trend:

- • IoT-enabled sensors for soil and crop monitoring are trending.

- • Drone-based field analysis is gaining traction.

- • AI-powered predictive analytics for farming decisions is emerging.

- • Variable rate application technologies are becoming standard.

- • Cloud-based farm management systems are increasing.

- • Rising need for increased crop yields is driving adoption.

- • Growth in smart farming technologies is fueling market expansion.

- • Integration with GPS and remote sensing is improving efficiency.

- • Government support for agricultural modernization is boosting sales.

- • Increasing labor shortages in farming are encouraging automation.

- • High initial investment costs can deter adoption.

- • Lack of technical skills among farmers can slow implementation.

- • Data integration challenges across devices can hinder usage.

- • Dependence on stable internet connectivity can limit rural adoption.

- • Climate variability can affect predictive analytics accuracy.

- • Expanding into developing regions with large agricultural sectors offers potential.

- • Partnering with agri-tech startups can boost innovation.

- • Offering affordable subscription models can attract small farmers.

- • Developing all-in-one precision farming platforms can increase adoption.

- • Integrating with e-commerce for farm supplies can enhance value.

Regional Insight

The North Americaregion holds a dominant market share, primarily driven by growing consumption patterns, a rising population, and robust economic activity that fuels market demand. Meanwhile, the Asia-Pacific Region is experiencing the fastest growth, propelled by increasing infrastructure developments, expanding industrial activities, and a surge in consumer demand, positioning it as a key driver for future market expansion.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

- • North America leads with large mechanized farms and RTK/GNSS adoption

- • Europe follows with sustainability and CAP incentives

- • Asia-Pacific grows via yield optimization and smart irrigation.

Key Players

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach:

- • John Deere

- • Trimble

- • AG Leader Technology

- • Raven Industries

- • Topcon Positioning Systems

- • AGCO Corporation

- • Climate FieldView

- • Bayer CropScience

- • CNH Industrial

- • Hexagon Agriculture

Regulatory Framework

The regulatory framework for the Precision Agriculture Systems ensures product safety, fair competition, and consumer protection. It encompasses setting standards for product quality and safety, enforcing truthful advertising and labeling, and implementing environmental sustainability practices. Regulations include robust procedures for product recalls, data protection, and anti-competitive practices, while also overseeing import/export controls and intellectual property rights. Regulatory bodies enforce these rules through inspections and penalties, and consumer education programs help individuals make informed decisions. This framework aims to protect consumers, promote fair market conditions, and encourage ethical business practices.

- • Regulated under spectrum/drone rules

- • data privacy

- • and equipment safety

- • Compliance with aviation/telecom approvals

- • machinery directives

- • and farm data rights frameworks is required.

Competitive Insights

The key players in the Precision Agriculture Systems are intensifying their focus on research and development (R&D) activities to innovate and stay competitive. Major companies, such as John Deere, Trimble, AG Leader Technology, Raven Industries, Topcon Positioning Systems, AGCO Corporation, Climate FieldView, Bayer CropScience, CNH Industrial, Hexagon Agriculture, are heavily investing in R&D to develop new products and improve existing ones. This strategic emphasis on innovation is driving significant advancements in product formulation and the introduction of sustainable and eco-friendly products.

In addition to R&D and acquisitions, there is a notable shift towards green investments among key players in the consumer goods industry. Companies are increasingly committing resources to sustainable practices and the development of environmentally friendly products. This green investment is in response to growing consumer demand for sustainable solutions and stringent environmental regulations. By prioritizing sustainability, these companies are not only contributing to environmental protection but also positioning themselves as leaders in the green movement, thereby fueling market growth.

Merger Acquisition

- • Between 2023 and 2025 M&A activity included agri-tech giants acquiring startups specializing in drone-based crop monitoring

- • Equipment manufacturers purchased software providers to offer integrated solutions

- • Partnerships between agri-data platforms and seed/fertilizer companies expanded value chains

- • Private equity investments scaled precision irrigation technologies

- • Cross-border acquisitions increased global market penetration.

Patent Analysis

- • Patent activity emphasizes multi-sensor fusion

- • RTK-guided actuation

- • and autonomous implement control for variable-rate applications

- • Innovations include plant-health analytics

- • micro-application sprayers

- • and edge-inference for low-latency decisions

- • The focus is on ROI per hectare

- • input reduction

- • and yield optimization

Investment and Funding Scenario

- • Investment is strong from agri-focused VCs

- • strategic input suppliers

- • and equipment OEMs; funding supports pilots

- • sensor fleets

- • and SaaS scaling

- • M&A often pairs analytics firms with equipment OEMs or consolidates precision-application service providers

Market Entropy

- • The Precision Agriculture Systems Market in 2022–2024 displayed medium entropy as GPS-enabled machinery IoT sensors and data analytics platforms competed for farmer adoption

- • Regional growth was strong in North America Europe and parts of Asia-Pacific

- • Vendors differentiated through integration capabilities and ease of use

- • Climate change and sustainability goals drove innovation in precision irrigation and crop monitoring

- • Competitive pricing and government subsidies influenced adoption rates.

Report Infographics:

| Report Features | Details |

| Base Year | 2025 |

| Based Year Market Size 2025 | 11.0 billion |

| Historical Period Market Size 2020 | USD Million ZZ |

| CAGR (2025 to 2033) | 11.30% |

| Forecast Period | 2025 to2033 |

| Forecasted Period Market Size 2033 | 26.0 billion |

| Scope of the Report | GPS guidance, Variable rate tech, Soil sensors, Drones, Imagery/NDVI, Auto-steer, Yield monitors, Farm management software, IoT gateways, Robotics, Row crops, Specialty crops, Dairy/livestock, Greenhouses, Large farms, Smallholders, Cooperatives |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Year-on-Year Growth | 10% |

| Companies Covered | John Deere, Trimble, AG Leader Technology, Raven Industries, Topcon Positioning Systems, AGCO Corporation, Climate FieldView, Bayer CropScience, CNH Industrial, Hexagon Agriculture |

| Customization Scope | 15% Free Customization (For EG) |

| Delivery Format | PDF and Excel through Email

Want to Buy Specific Sections of This Report?

|

Research Methodology

The research methodology for the consumer goods industry involves several key steps to ensure comprehensive and actionable insights. First, the research objectives are clearly defined, focusing on aspects like consumer behavior, market opportunities, competitive dynamics, or regulatory impacts. A thorough literature review follows, drawing from academic journals, industry reports, government publications, and market analyses to establish a knowledge base and identify research gaps. Data collection encompasses both primary methods, such as surveys, interviews, and focus groups with consumers and industry experts, and secondary methods, including analysis of market reports, government data, and industry publications. Quantitative data is analyzed using statistical tools to identify patterns and market segments, while qualitative data from interviews and focus groups is examined to extract key themes and insights.

The market is then segmented based on demographics, psychographics, geography, and purchasing behavior, and competitive analysis is conducted to evaluate key players' strategies and strengths. Trend analysis identifies current and emerging industry trends. Findings are compiled into a detailed report with data visualizations and strategic recommendations. The research is validated and refined through cross-checking and expert feedback, and a framework for continuous monitoring is established to keep the research current and relevant.

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.