Table-top Autorefractor Market to See Incredible Expansion

Global Table-top Autorefractor Market is segmented by Application (Eye examination, Vision assessment, Clinical ophthalmology, Refractive error measurement, Pediatric eye screening, Optometry clinics, Hospital eye care), Type (Manual table-top, Semi-automatic, Fully automatic, Portable table-top, Desktop models, LCD display models, Infrared models, Vision screening models, Binocular models, Digital models), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

INDUSTRY OVERVIEW

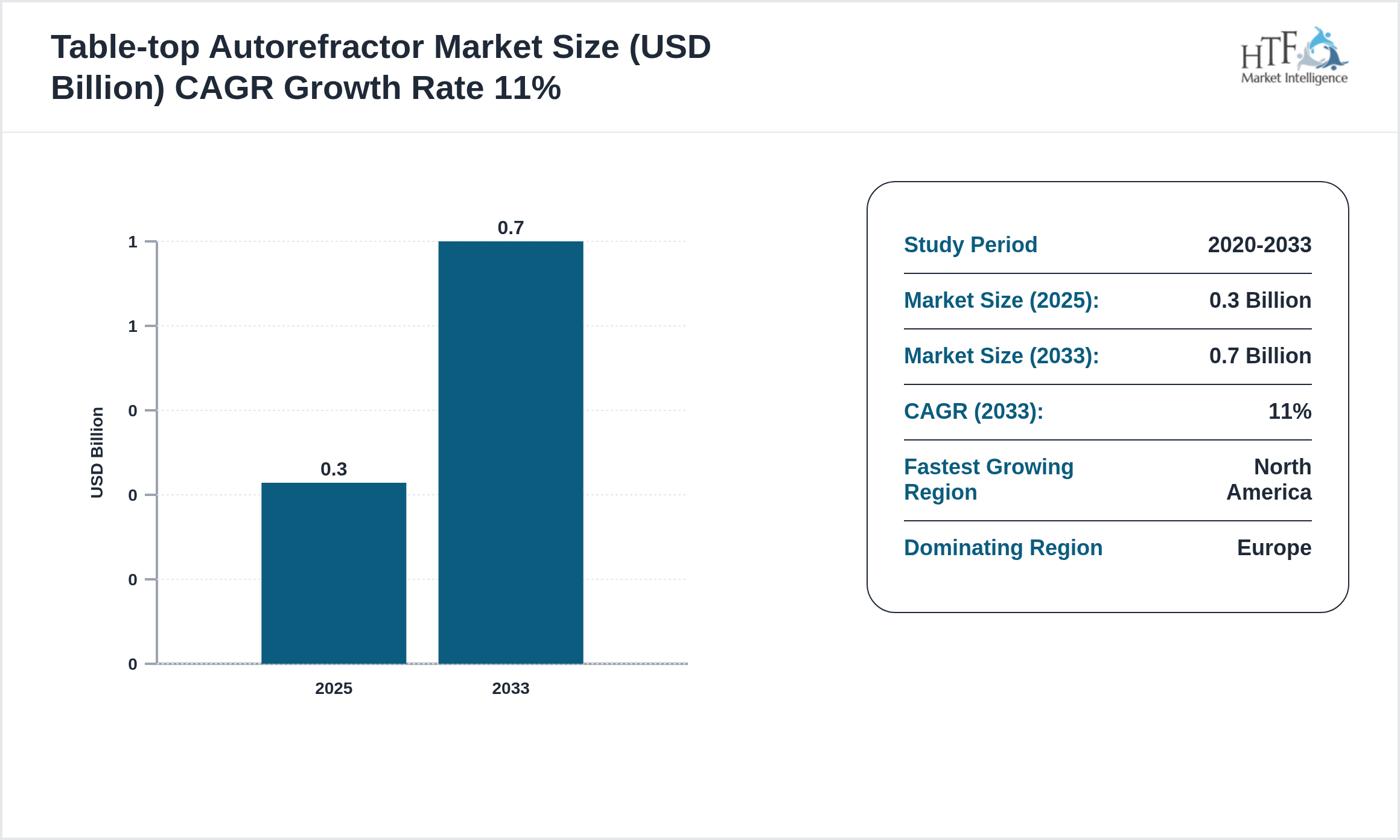

The Table-top Autorefractor is growing at 11% and is expected to reach 700 million by 2033. The below-mentioned are some of the dynamics shaping the Table-top Autorefractor.

Table-top autorefractors are ophthalmic diagnostic instruments that measure refractive errors automatically. Widely used in optometry clinics hospitals and eye-care centers they enable quick and accurate vision correction assessments. Rising prevalence of myopia demand for efficient diagnostic solutions and adoption in emerging markets are key growth drivers.

Source: HTF Market Intelligence (HTF MI)

Understand Key Market Dynamics

Market Dynamics

Market Drivers:

The key drivers in the market include technological advancements, increasing demand by consumers for innovative products, and government-friendly policies.

- • Rising prevalence of refractive errors fuels demand

- • Growing elderly population supports adoption

- • Increasing awareness of eye health boosts market growth

- • Expansion of ophthalmology clinics enhances demand

- • Rising disposable incomes in emerging economies strengthen uptake

Some of the restraints to market growth may include regulatory challenges, high production costs, and disruptions in the supply chain.

- • High equipment costs limit adoption in small practices

- • Stringent regulatory requirements delay product approvals

- • Limited availability of skilled optometrists restricts usage

- • Maintenance and calibration costs hinder adoption

- • Competition from manual refraction methods reduces demand

Among the trending ones are sustainability, digital transformation, and the increasing importance of data analytics.

- • Trend of portable and compact autorefractors gaining popularity

- • Integration with digital health platforms enhances usability

- • Rising adoption in school and community eye screening programs supports demand

- • Growing focus on teleophthalmology fuels adoption

- • Technological innovation in AI-based refraction systems boosts efficiency

These include emerging markets, innovation in product development, and strategic partnerships.

- • Rising demand for vision screening in hospitals and clinics creates opportunities

- • Expanding use in optometry practices supports growth

- • Growing adoption in rural healthcare outreach strengthens demand

- • Technological innovations in autorefractors improve accuracy

- • Expansion of eye-care access in emerging economies fuels growth

Regulation Shaping the Healthcare Industry

The healthcare industry is significantly influenced by a complex framework of regulations designed to ensure patient safety, the efficacy of treatments, and the overall quality of care. Key regulatory areas include drug approval processes, medical device standards, and healthcare data protection. These regulations aim to maintain high standards for clinical practices and safeguard public health.

Get More Details on the Table-top Autorefractor Market Study

SWOT Analysis in the Healthcare Industry

SWOT analysis in the healthcare industry involves a structured assessment of strengths, weaknesses, opportunities, and threats to identify strategic advantages and areas for improvement.

• Strengths: Evaluates internal factors such as advanced technology, skilled personnel, and strong brand reputation. For example, a hospital with cutting-edge medical equipment and specialized staff is considered to have a strong competitive edge.

• Weaknesses: Identifies internal limitations like outdated facilities, regulatory compliance issues, or high operational costs. Weaknesses could include inefficient processes or lack of innovation.

• Opportunities: Assesses external factors that could drive growth, such as emerging medical technologies, expanding markets, or favorable government policies. Opportunities might involve partnerships or new service lines.

• Threats: Examines external challenges such as increasing competition, changing regulations, or economic downturns. Threats might include new entrants with disruptive technologies or stricter regulatory requirements.

Market Segmentation

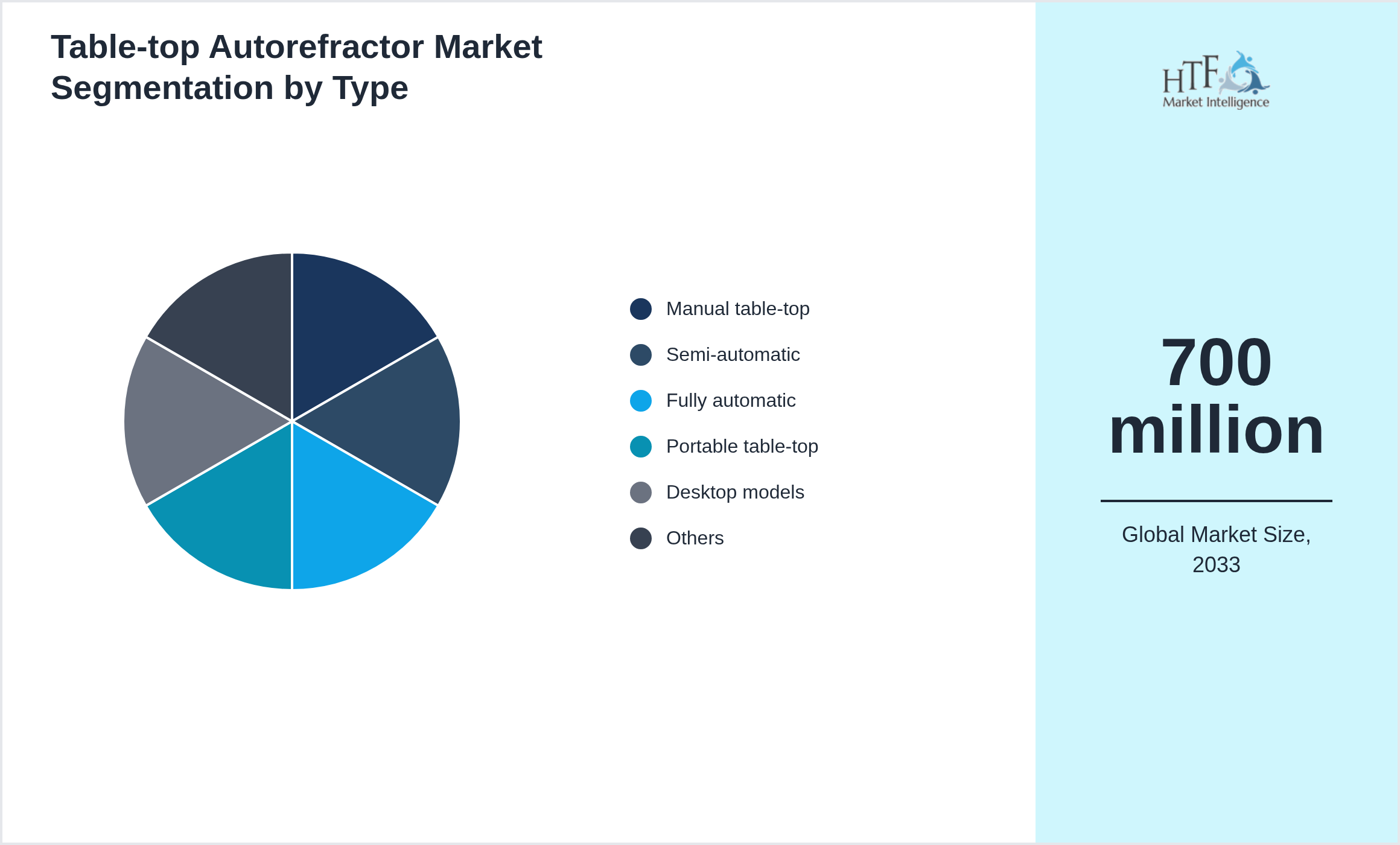

Segmentation by Type

- • Manual table-top

- • Semi-automatic

- • Fully automatic

- • Portable table-top

- • Desktop models

- • LCD display models

- • Infrared models

- • Vision screening models

- • Binocular models

- • Digital models

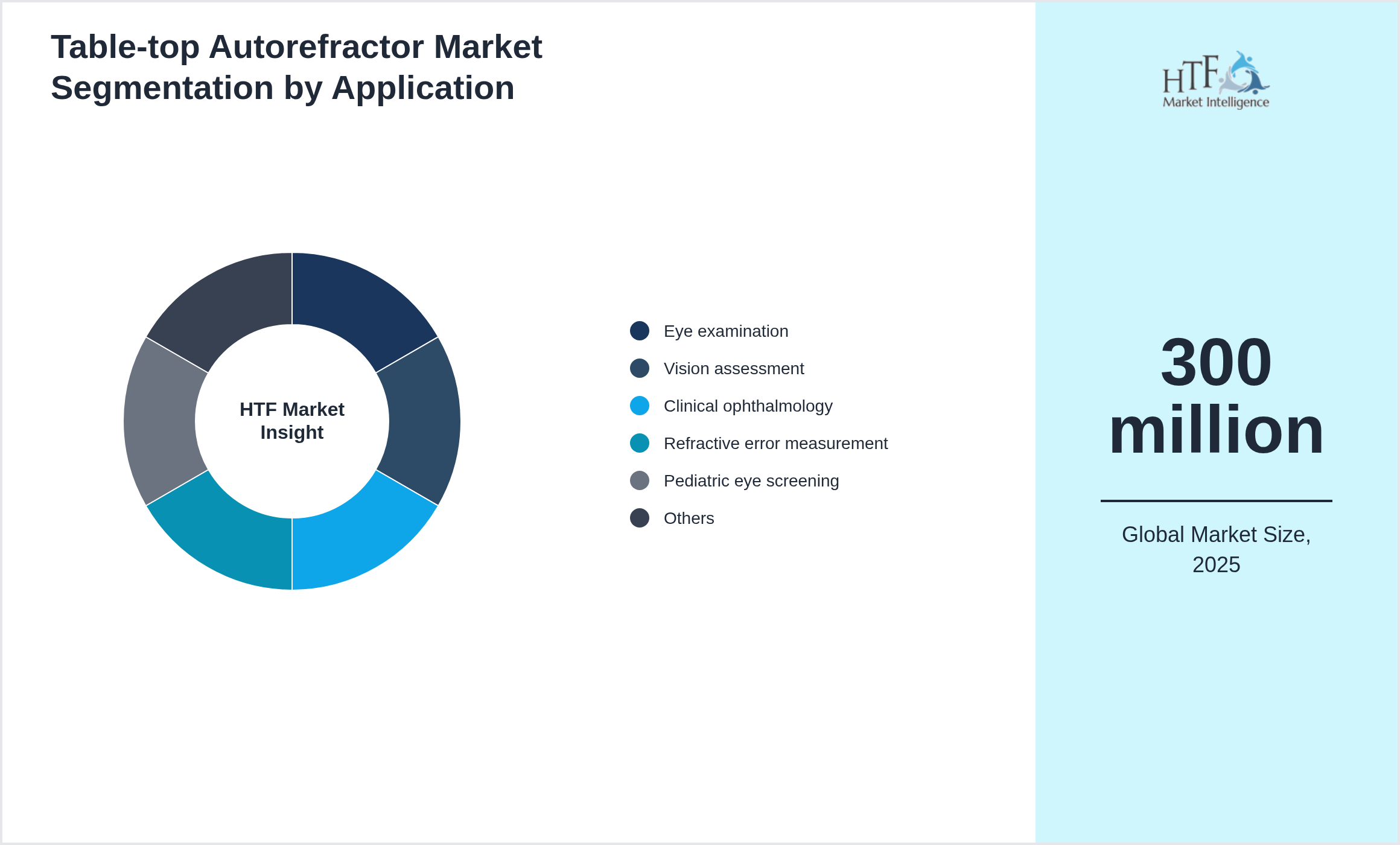

Segmentation by Application

- • Eye examination

- • Vision assessment

- • Clinical ophthalmology

- • Refractive error measurement

- • Pediatric eye screening

- • Optometry clinics

- • Hospital eye care

Regional Outlook

The Europe currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, North America is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth. In our report, we cover a comprehensive analysis of the regions and countries, including

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

The company consistently allocates significant resources to expand its research capabilities, develop new medical technologies, and enhance its pharmaceutical portfolio. Johnson & Johnson's investments in R&D, coupled with strategic acquisitions and partnerships, reinforce its position as a major contributor to advancements in healthcare. This focus on innovation and market expansion underscores the critical importance of the North American region in the global healthcare landscape.

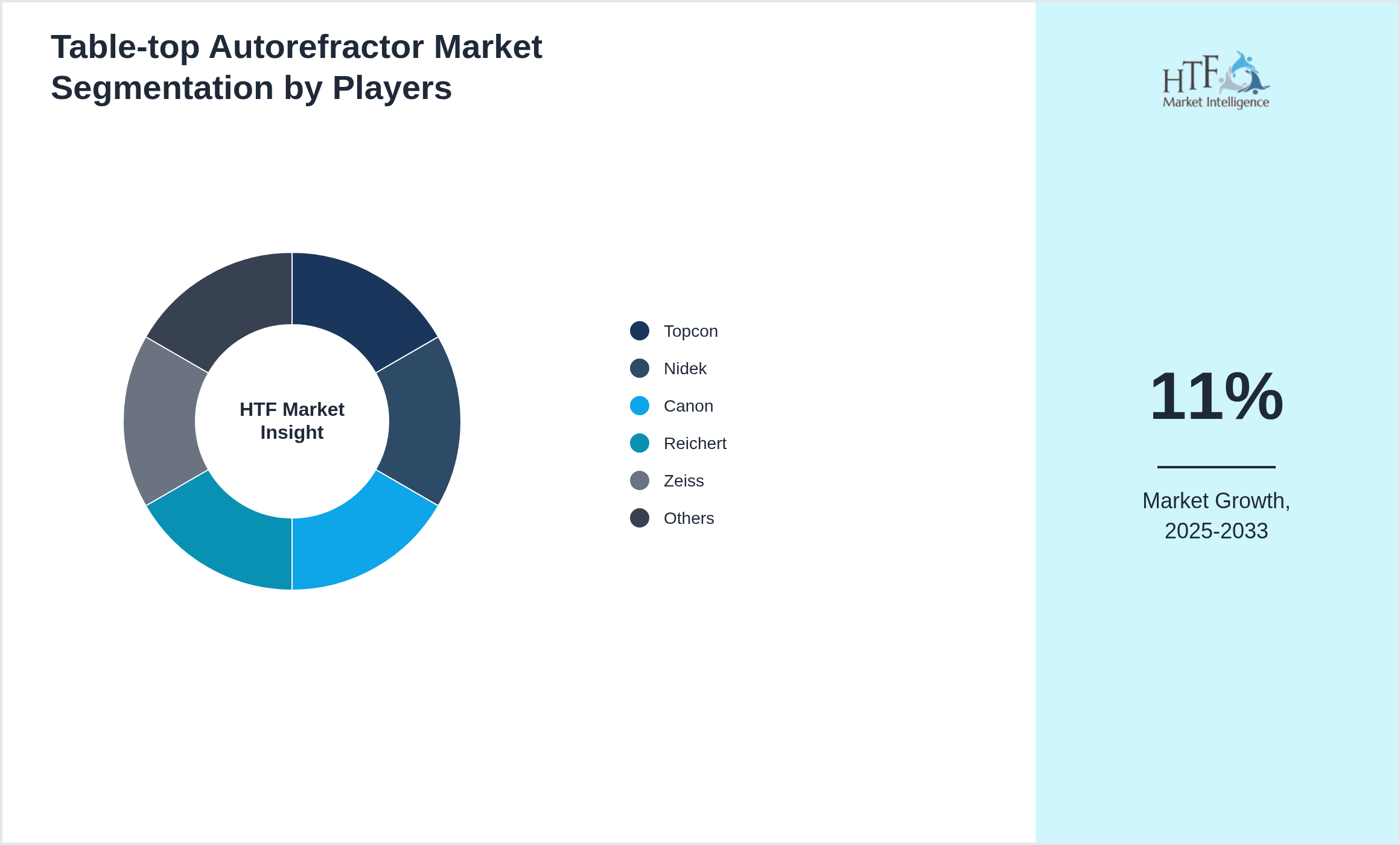

- • Topcon

- • Nidek

- • Canon

- • Reichert

- • Zeiss

- • Huvitz

- • Righton

- • CSO

- • Essilor

- • Marco Ophthalmic

- • Tomey

- • Oculus

- • Optos

- • Takagi

- • Welch Allyn

- • Visionix

- • Grand Seiko

- • Luneau

- • Heidelberg Engineering

- • Coburn

- • Mediworks

Key Development Activities

Regional Analysis

- • North America: Strong demand in optometry clinics and ophthalmic practices for vision screening

- • Europe: High adoption in the UK

- • Germany

- • and France for professional eye care services

- • Asia–Pacific: China and India rapidly adopting autorefractors in clinics and hospitals

- • Latin America: Brazil and Mexico expanding use of diagnostic equipment in eye care

- • Middle East & Africa: GCC countries investing in advanced eye care diagnostic tools

Market Entropy

- • Moderate entropy with steady innovation in optometry devices

- • Smaller startups entered with portable AI-assisted models

Merger & Acquisition

- • In 2023 acquisitions targeted optical device startups

- • In 2024 M&A activity centered on expanding refractive care across Asia-Pacific

- • In 2025 larger diagnostic firms consolidated compact autorefractor suppliers

Regulatory Landscape

- • US: FDA approval for medical devices

- • 510(k) for autorefractors

- • ISO 13485 for manufacturing; EU: CE marking under MDR

- • ISO 13485 for medical equipment

- • EN 14042 for optical instruments; regional certifications for optometric devices in Africa and the Middle East

Investment and Funding Scenario

- • Government healthcare programs are funding vision care infrastructure

- • Venture capital is backing startups producing advanced optical diagnostic tools

- • Private equity is consolidating eye care equipment manufacturers

- • Corporate investors are acquiring ophthalmic technology companies

- • Development agencies are financing vision care and diagnostic infrastructure

Primary and Secondary Research

Primary research involves the collection of original data directly from sources in the healthcare industry. Approaches include the survey of health professionals, interviews with patients, focus groups, and clinical trials. This gives an overview of the current practice, the needs of the patient, and the interest in emerging trends. Firsthand information on the efficacy of new treatments, an assessment of market demand, and insight into changes in regulation can be sought only with primary research.

Secondary Research: This is the investigation of existing information from a variety of sources, which may include industry reports, academic journals, government publications, and market research studies. Alfred secondary research empowers them to understand trends within industries, historical data, and competitive landscapes. It gives a wide view of the market dynamics and validates findings obtained from primary research. By combining both primary and secondary together, health organizations will be empowered to develop comprehensive strategies and make informed decisions based on a strong foundation built on data.

Report Infographics

|

Report Features |

Details |

|

Base Year |

2025 |

|

Based Year Market Size (BASE_YEAR) |

300 million |

|

Historical Period |

2020 to 2025 |

|

CAGR (2025 to 2033) |

11% |

|

Forecast Period |

2025 to 2033 |

|

Forecasted Period Market Size (2033) |

700 million |

|

Scope of the Report |

Manual table-top, Semi-automatic, Fully automatic, Portable table-top, Desktop models, LCD display models, Infrared models, Vision screening models, Binocular models, Digital models, Eye examination, Vision assessment, Clinical ophthalmology, Refractive error measurement, Pediatric eye screening, Optometry clinics, Hospital eye care |

|

Regions Covered |

North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

|

Companies Covered |

Topcon, Nidek, Canon, Reichert, Zeiss, Huvitz, Righton, CSO, Essilor, Marco Ophthalmic, Tomey, Oculus, Optos, Takagi, Welch Allyn, Visionix, Grand Seiko, Luneau, Heidelberg Engineering, Coburn, Mediworks |

|

Customization Scope |

15% Free Customization (For EG) |

|

Delivery Format |

PDF and Excel through Email |