Global Home Audio Systems Market Scope & Changing Dynamics 2024-2033

Global Home Audio Systems Market is segmented by Application (Entertainment, Gaming, Music Streaming, Smart Home, Events), Type (Soundbars, Home Theater, Smart Speakers, Wireless Speakers, Hi-Fi Systems), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Industry Overview

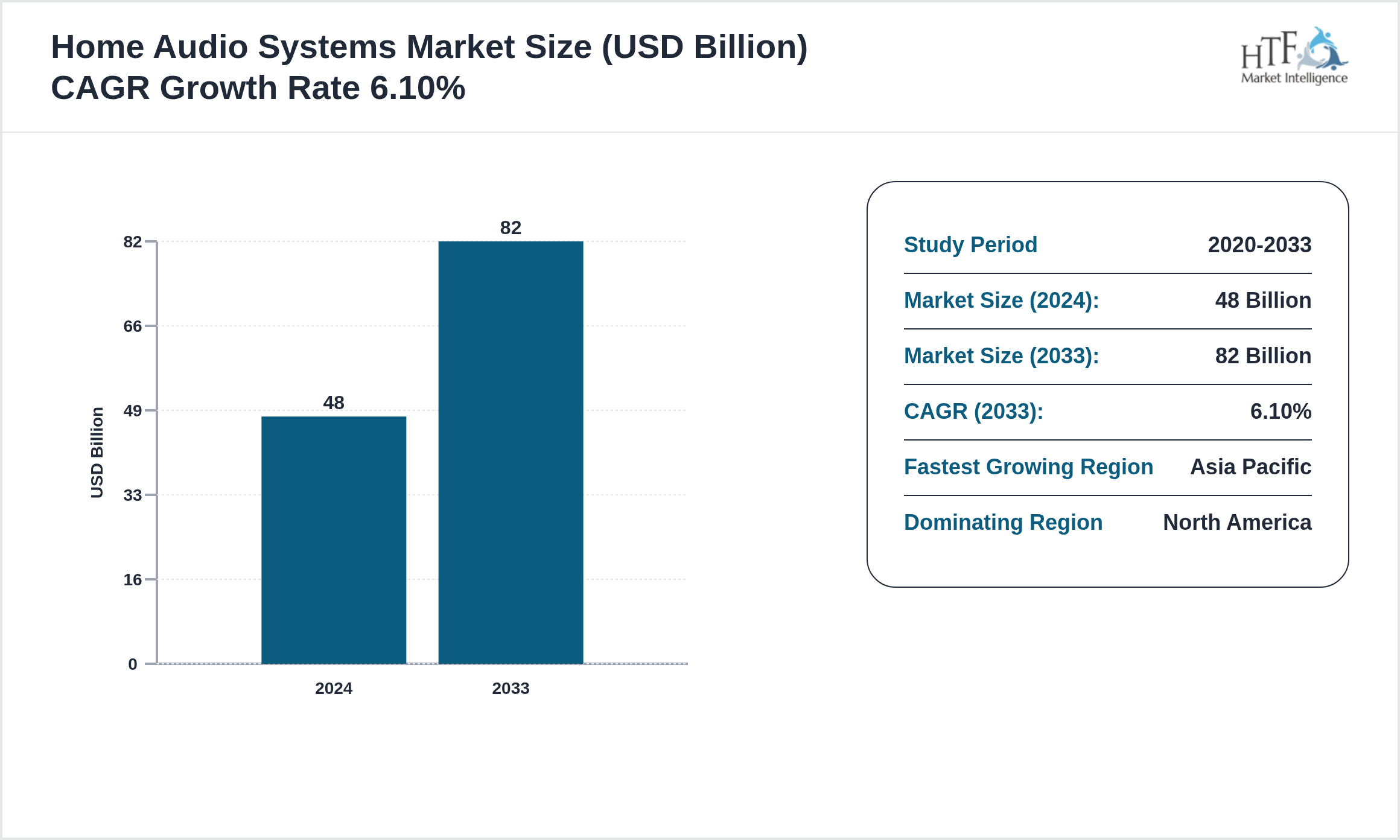

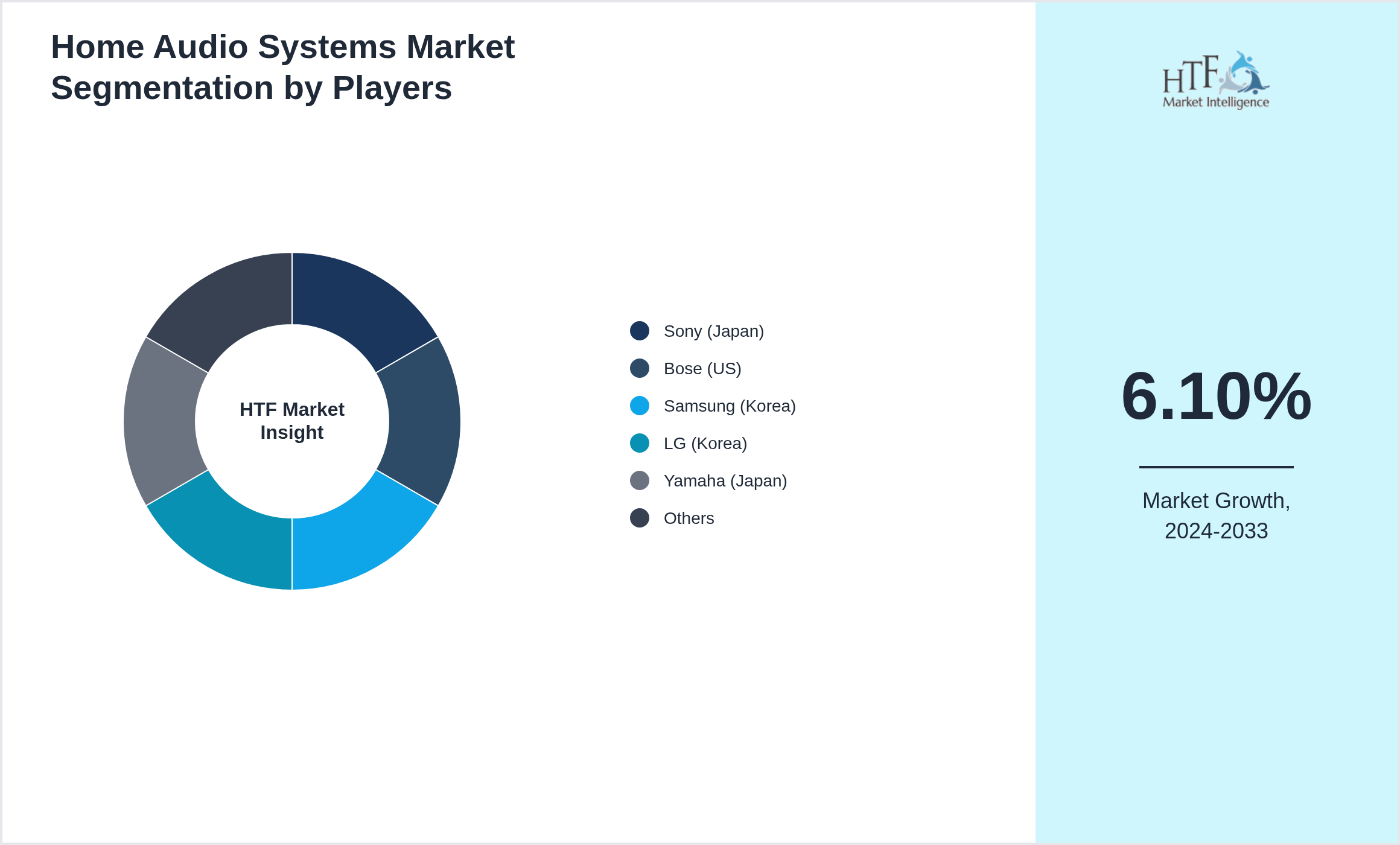

The Home Audio Systems market is expected to reach 82 billion by 2033 and is growing at a CAGR of6.10% between 2024 and 2033.

Home audio systems include smart speakers, soundbars, multi-room setups, and high-fidelity audio equipment designed for immersive home entertainment.

Source: HTF Market Intelligence (HTF MI)

Market Size & Forecast

Market Segmentation

Selecting segmentation criteria in Sony (Japan), Bose (US), Samsung (Korea), LG (Korea), Yamaha (Japan), JBL (US), Harman (US), Sonos (US), Philips (Netherlands), Panasonic (Japan), Denon (Japan), Polk Audio (US), Marshall (UK), Sennheiser (Germany), Pioneer (Japan) involves several key steps. Researchers begin by defining their objectives, such as understanding consumer behavior or identifying market opportunities. They then gather relevant data on demographics, psychographics, and buying behavior. Next, they identify segmentation variables like age, location, lifestyle, and purchase patterns. Using analytical tools, they analyze the data to find distinct market segments and evaluate their attractiveness based on size, growth potential, and alignment with business goals. Detailed profiles are created for each segment, and the most promising ones are selected for targeting. Finally, tailored marketing strategies are developed, and the performance of these strategies is monitored and adjusted as needed. This process ensures that segmentation effectively identifies valuable market opportunities and aligns with strategic goals.

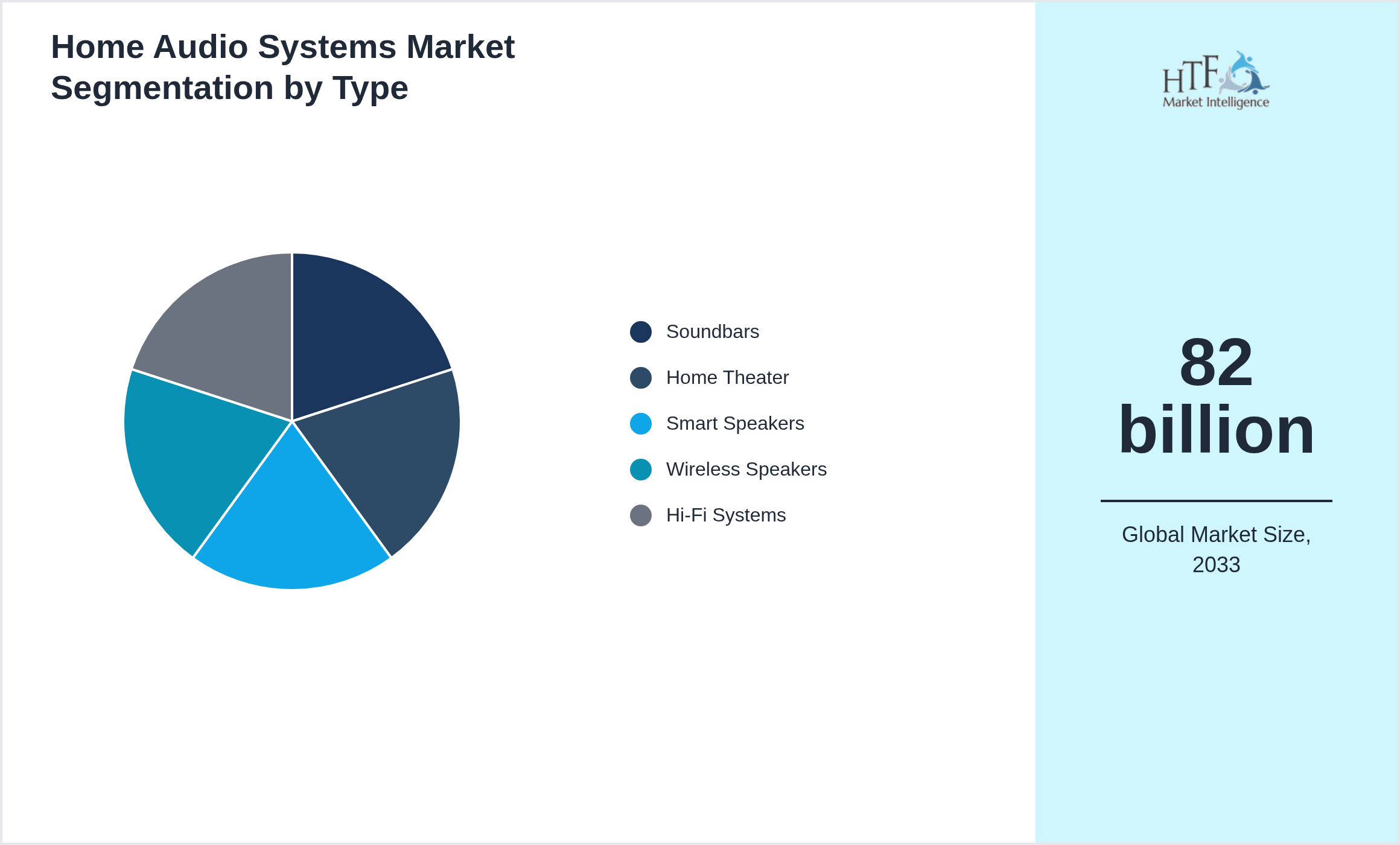

Segmentation by Type

- • Soundbars

- • Home Theater

- • Smart Speakers

- • Wireless Speakers

- • Hi-Fi Systems

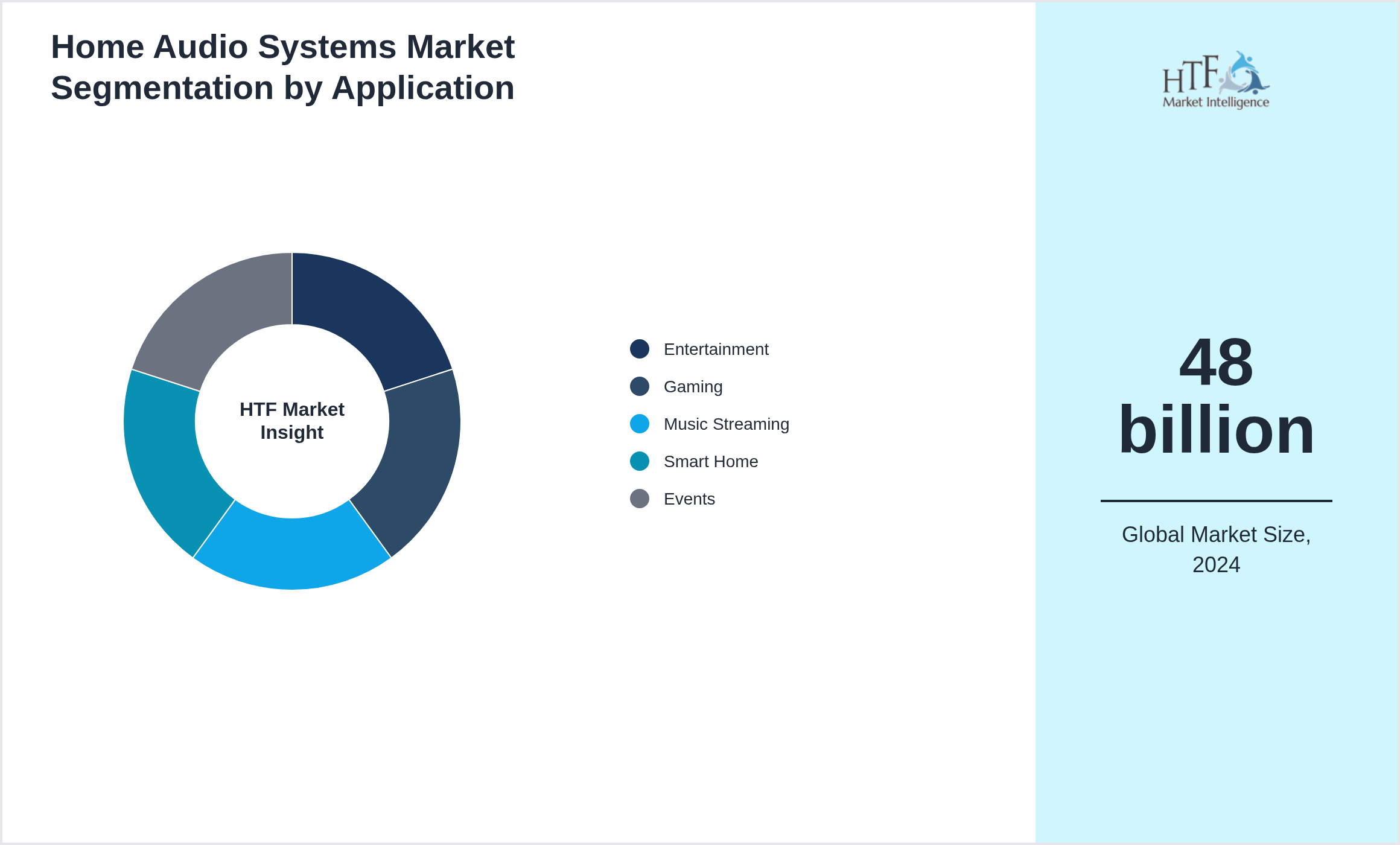

Segmentation by Application

- • Entertainment

- • Gaming

- • Music Streaming

- • Smart Home

- • Events

Home Audio Systems Market Dynamics

TheHome Audio Systems is driven by factors such as increasing demand in end-use industries, technological advancements, research and development (R&D), economic growth, and increasing global trade.

Influencing Trend:

- • Dolby Atmos

- • voice assistants

- • compact designs

- • and wireless multi-room systems dominate trends.

- • Streaming growth

- • smart homes

- • premium entertainment demand

- • and wireless tech drive growth.

- • Price sensitivity

- • commoditization

- • and intense brand competition remain challenges.

- • Emerging markets

- • premium upgrades

- • and smart speaker convergence offer opportunities.

Regional Insight

The North Americaregion holds a dominant market share, primarily driven by growing consumption patterns, a rising population, and robust economic activity that fuels market demand. Meanwhile, the Asia Pacific Region is experiencing the fastest growth, propelled by increasing infrastructure developments, expanding industrial activities, and a surge in consumer demand, positioning it as a key driver for future market expansion.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

- • NA/EU drive premium audio; APAC dominates mass-market Bluetooth and smart speakers; MEA/LATAM rising with home-entertainment adoption.

Key Players

The companies highlighted in this profile were selected based on insights from primary experts and an evaluation of their market penetration, product offerings, and geographical reach:

- • Sony (Japan)

- • Bose (US)

- • Samsung (Korea)

- • LG (Korea)

- • Yamaha (Japan)

- • JBL (US)

- • Harman (US)

- • Sonos (US)

- • Philips (Netherlands)

- • Panasonic (Japan)

- • Denon (Japan)

- • Polk Audio (US)

- • Marshall (UK)

- • Sennheiser (Germany)

- • Pioneer (Japan)

Regulatory Framework

The regulatory framework for the Home Audio Systems ensures product safety, fair competition, and consumer protection. It encompasses setting standards for product quality and safety, enforcing truthful advertising and labeling, and implementing environmental sustainability practices. Regulations include robust procedures for product recalls, data protection, and anti-competitive practices, while also overseeing import/export controls and intellectual property rights. Regulatory bodies enforce these rules through inspections and penalties, and consumer education programs help individuals make informed decisions. This framework aims to protect consumers, promote fair market conditions, and encourage ethical business practices.

- • Regulated via acoustic output safety wireless certification EMC energy efficiency and material compliance.

Competitive Insights

The key players in the Home Audio Systems are intensifying their focus on research and development (R&D) activities to innovate and stay competitive. Major companies, such as Sony (Japan), Bose (US), Samsung (Korea), LG (Korea), Yamaha (Japan), JBL (US), Harman (US), Sonos (US), Philips (Netherlands), Panasonic (Japan), Denon (Japan), Polk Audio (US), Marshall (UK), Sennheiser (Germany), Pioneer (Japan), are heavily investing in R&D to develop new products and improve existing ones. This strategic emphasis on innovation is driving significant advancements in product formulation and the introduction of sustainable and eco-friendly products.

In addition to R&D and acquisitions, there is a notable shift towards green investments among key players in the consumer goods industry. Companies are increasingly committing resources to sustainable practices and the development of environmentally friendly products. This green investment is in response to growing consumer demand for sustainable solutions and stringent environmental regulations. By prioritizing sustainability, these companies are not only contributing to environmental protection but also positioning themselves as leaders in the green movement, thereby fueling market growth.

Merger Acquisition

- • In Aug 2024

Patent Analysis

- • Patents in spatial audio beamforming acoustic tuning algorithms speaker designs and embedded voice assistants.

Investment and Funding Scenario

- • Funding from smart-home vendors audio brands and consumer-AI players.

Market Entropy

- • Jul 2025 – AudioSphere partnered with streaming providers to launch home audio systems with spatial sound engines and voice-adaptive tuning.

Report Infographics:

| Report Features | Details |

| Base Year | 2024 |

| Based Year Market Size 2024 | 48 billion |

| Historical Period Market Size 2020 | USD Million ZZ |

| CAGR (2024 to 2033) | 6.10% |

| Forecast Period | 2024 to2033 |

| Forecasted Period Market Size 2033 | 82 billion |

| Scope of the Report | Soundbars, Home Theater, Smart Speakers, Wireless Speakers, Hi-Fi Systems, Entertainment, Gaming, Music Streaming, Smart Home, Events |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Year-on-Year Growth | 7.40% |

| Companies Covered | Sony (Japan), Bose (US), Samsung (Korea), LG (Korea), Yamaha (Japan), JBL (US), Harman (US), Sonos (US), Philips (Netherlands), Panasonic (Japan), Denon (Japan), Polk Audio (US), Marshall (UK), Sennheiser (Germany), Pioneer (Japan) |

| Customization Scope | 15% Free Customization (For EG) |

| Delivery Format | PDF and Excel through Email

Want to Buy Specific Sections of This Report?

|

Research Methodology

The research methodology for the consumer goods industry involves several key steps to ensure comprehensive and actionable insights. First, the research objectives are clearly defined, focusing on aspects like consumer behavior, market opportunities, competitive dynamics, or regulatory impacts. A thorough literature review follows, drawing from academic journals, industry reports, government publications, and market analyses to establish a knowledge base and identify research gaps. Data collection encompasses both primary methods, such as surveys, interviews, and focus groups with consumers and industry experts, and secondary methods, including analysis of market reports, government data, and industry publications. Quantitative data is analyzed using statistical tools to identify patterns and market segments, while qualitative data from interviews and focus groups is examined to extract key themes and insights.

The market is then segmented based on demographics, psychographics, geography, and purchasing behavior, and competitive analysis is conducted to evaluate key players' strategies and strengths. Trend analysis identifies current and emerging industry trends. Findings are compiled into a detailed report with data visualizations and strategic recommendations. The research is validated and refined through cross-checking and expert feedback, and a framework for continuous monitoring is established to keep the research current and relevant.