Global Industrial Gears Market Size, Growth & Revenue 2025-2034

Global Industrial Gears Market is segmented by Product Type (Helical Gears, Bevel Gears, Worm Gears, Spur Gears, Planetary Gears), Application (Material Handling, Automotive, Mining, Power Generation, Construction), End-Use Industry (Manufacturing, Automotive & Transportation, Energy & Utilities, Construction & Infrastructure), Distribution Channel (Direct Sales, Industrial Distributors, Aftermarket & Service Providers), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Industrial Gears market is a critical segment within the manufacturing and industrial machinery sectors, involving the production and application of various gear types designed to transmit mechanical power efficiently. This market includes a broad spectrum of gear variants such as helical, bevel, worm, spur, and planetary gears, which find extensive use across industries like automotive, material handling, mining, power generation, and construction. The value chain encompasses raw material suppliers, precision gear manufacturers, distributors, and aftermarket service providers, each contributing to the overall market ecosystem. Industrial gears are pivotal in ensuring machinery performance, durability, and operational efficiency, with advances in manufacturing technologies such as CNC machining and heat treatment improving gear quality and lifespan. The market is influenced by rising industrial automation, the need for energy-efficient systems, and increasing infrastructure development worldwide. However, challenges such as fluctuating raw material prices, high production costs, and stringent quality standards require continuous innovation and strategic investments. The market outlook from 2025 to 2034 indicates steady growth driven by expanding end-use sectors, technological advancements, and increasing demand from emerging economies, positioning industrial gears as a cornerstone for modern industrial applications globally.

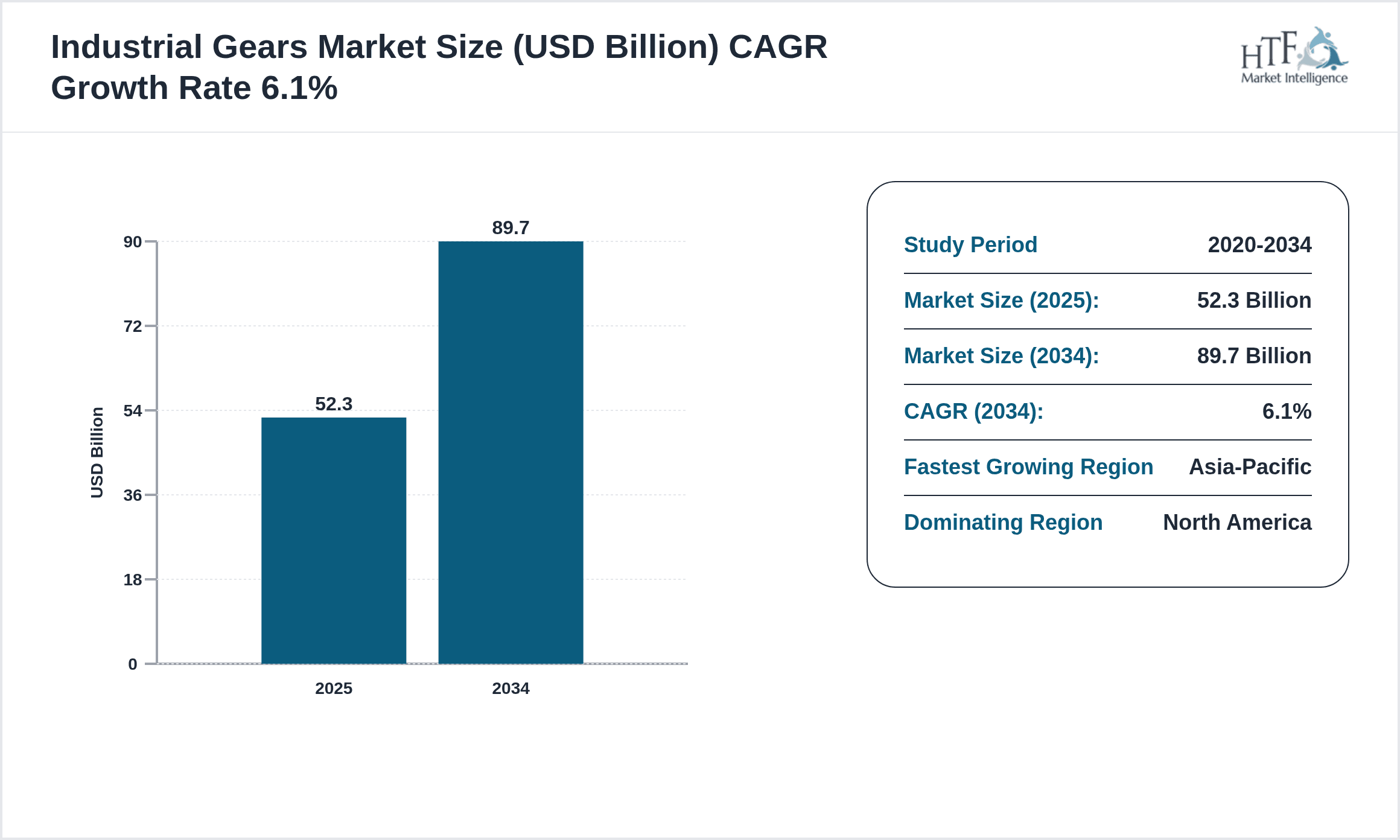

- •Key market highlights include a base market size of USD 52.3 Billion in 2025, projected to reach USD 89.7 Billion by 2034, reflecting a compound annual growth rate (CAGR) of 6.1%. Year-on-year growth is estimated at approximately 6.0%, underscoring consistent demand expansion. North America currently dominates the market due to its advanced manufacturing capabilities and strong automotive and aerospace sectors, while Asia-Pacific is the fastest growing region propelled by rapid industrialization and infrastructure investments. Helical gears lead the product segment owing to their versatility and efficiency, whereas planetary gears are the fastest growing type, driven by their compactness and high power transmission capacity. These dynamics highlight the evolving landscape shaped by technological innovation and shifting regional demand patterns.

- •The Industrial Gears market holds strategic importance across various industries by enabling efficient power transmission essential for heavy machinery and equipment functionality. For stakeholders including manufacturers, suppliers, and end-users, this market offers opportunities to capitalize on technological advancements, growing industrial automation, and infrastructure development globally. The value proposition lies in delivering high-performance, durable gear solutions that enhance operational efficiency and reduce maintenance costs. As industries seek sustainable and reliable mechanical components, investments in research and development, quality assurance, and supply chain optimization will be critical to capturing market share and driving long-term growth.

Competitive Landscape

The competitive environment of the global Industrial Gears market is characterized by a mix of established multinational corporations and regional manufacturers, each leveraging advanced manufacturing technologies, strategic partnerships, and product innovation to strengthen market positions. Companies focus on differentiating their offerings through enhanced gear durability, precision engineering, and customization to meet specific industry requirements. Mergers and acquisitions serve as key strategies for expanding product portfolios and geographic reach. Pricing strategies balance cost-efficiency with quality assurance, while companies invest in digitalization and automation of production processes to improve operational efficiency. Distribution channels are diversified to include direct sales, industrial distributors, and aftermarket services. The market faces moderate entry barriers due to the technical expertise and capital investment needed for precision gear manufacturing. Regional competition varies with Asia-Pacific witnessing rapid growth fueled by local manufacturers and cost advantages, while North America and Europe emphasize innovation and quality standards. Future trends indicate increasing adoption of smart manufacturing, predictive maintenance, and eco-friendly materials, which will redefine competitive dynamics and create new avenues for growth.

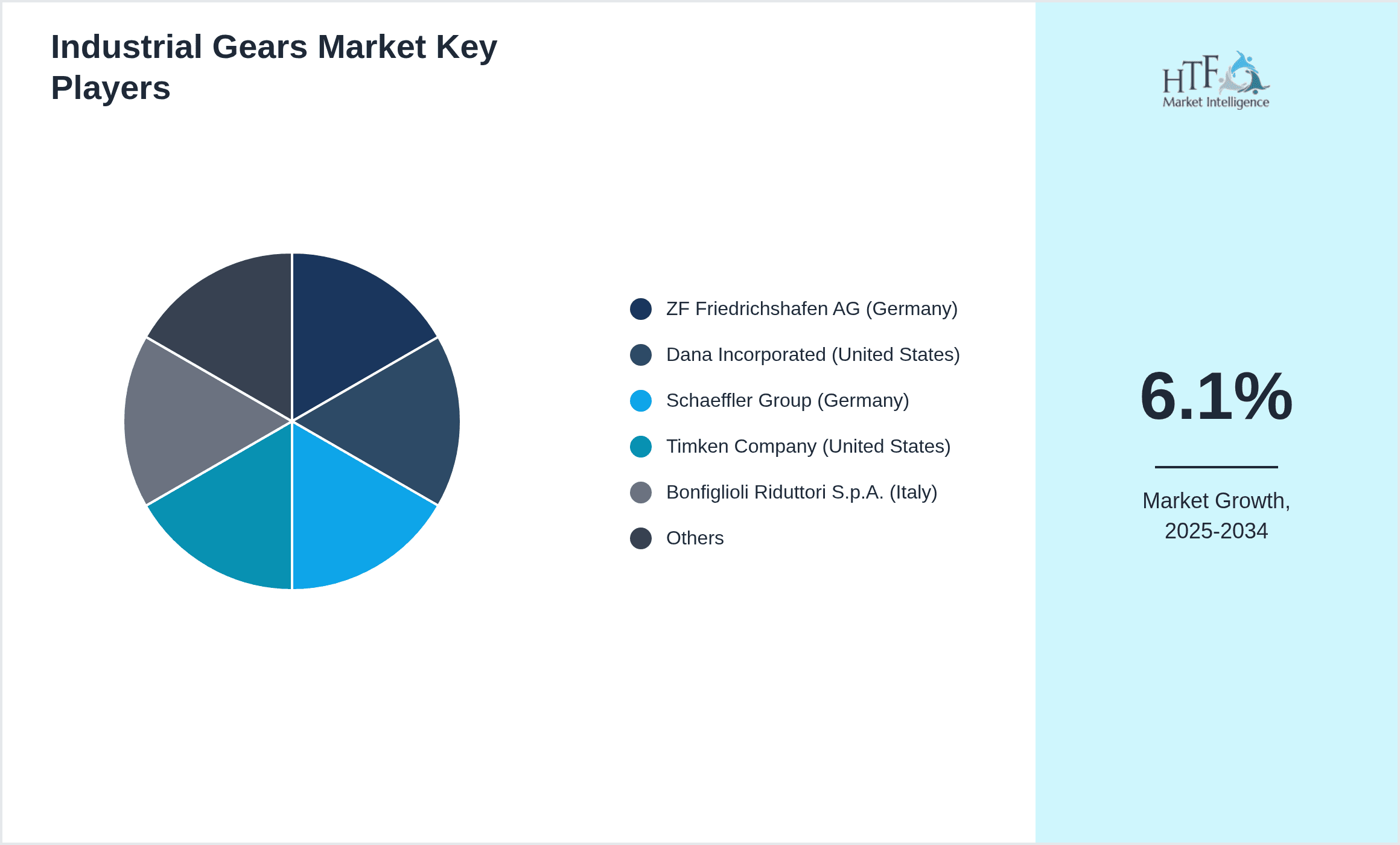

Prominent Players in Industrial Gears Market

- •ZF Friedrichshafen AG (Germany)

- •Dana Incorporated (United States)

- •Schaeffler Group (Germany)

- •Timken Company (United States)

- •Bonfiglioli Riduttori S.p.A. (Italy)

- •SEW-Eurodrive GmbH & Co KG (Germany)

- •Rotork plc (United Kingdom)

- •Meritor, Inc. (United States)

- •Nabtesco Corporation (Japan)

- •Nord Drivesystems (Germany)

- •Flender GmbH (Germany)

- •Brevini Power Transmission S.p.A. (Italy)

- •Gates Corporation (United States)

- •ABB Ltd (Switzerland)

- •WEG S.A. (Brazil)

- •KHK Gears (Japan)

- •Rexnord Corporation (United States)

- •Hitachi Industrial Equipment Systems Co., Ltd. (Japan)

- •NORD Drivesystems GmbH & Co. KG (Germany)

- •Bonfiglioli Engineering S.p.A. (Italy)

- •KTR Systems GmbH (Germany)

- •Mitsubishi Heavy Industries (Japan)

- •Altra Industrial Motion Corp. (United States)

- •Sumitomo Heavy Industries (Japan)

- •Harmonic Drive AG (Germany)

Market Breakdown

- •By Product Type

- ◦Helical Gears

- ◦Bevel Gears

- ◦Worm Gears

- ◦Spur Gears

- ◦Planetary Gears

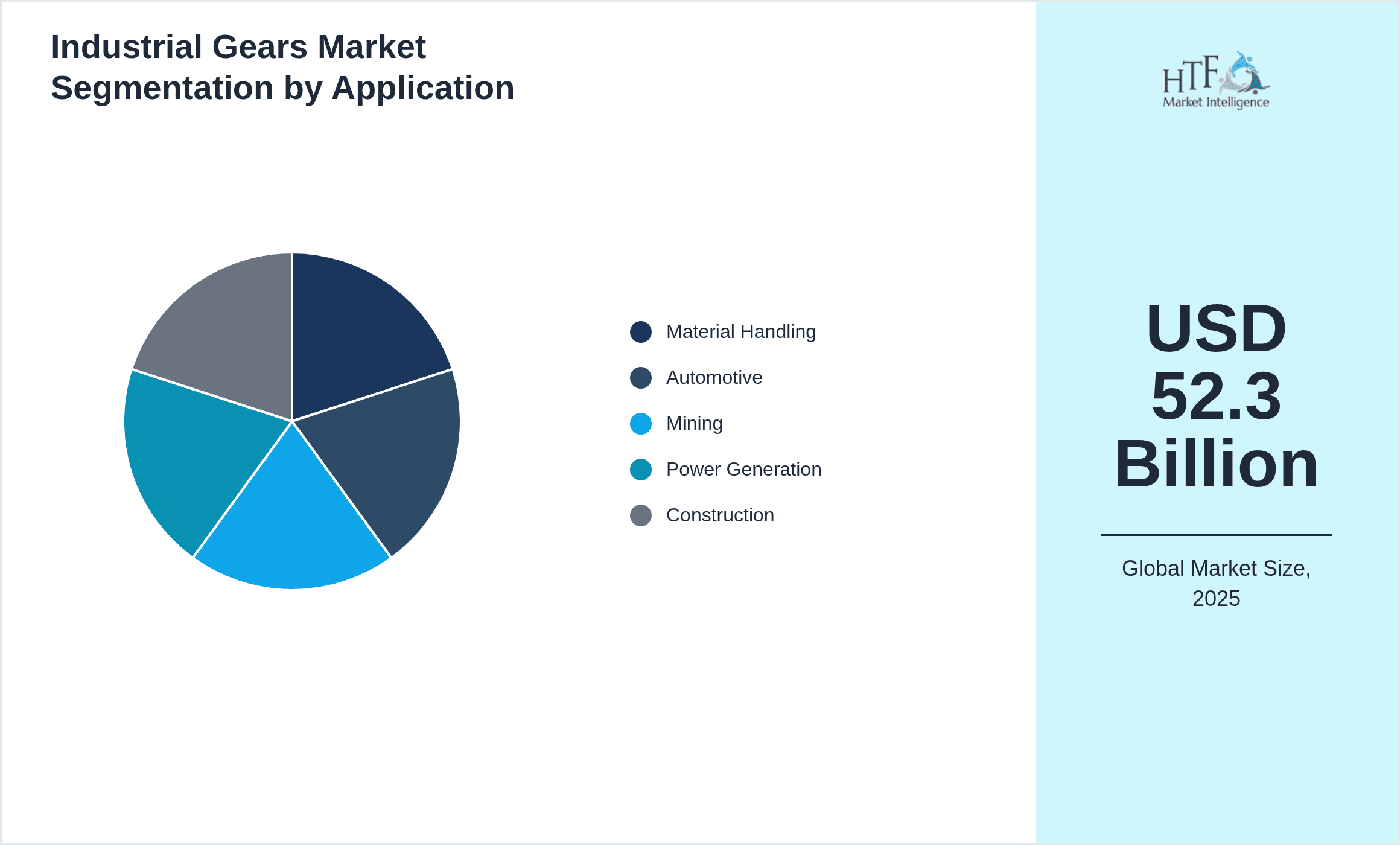

- •By Application

- ◦Material Handling

- ◦Automotive

- ◦Mining

- ◦Power Generation

- ◦Construction

- •By End-Use Industry

- ◦Manufacturing

- ◦Automotive & Transportation

- ◦Energy & Utilities

- ◦Construction & Infrastructure

- •By Distribution Channel

- ◦Direct Sales

- ◦Industrial Distributors

- ◦Aftermarket & Service Providers

Growth Dynamics

- •Increasing industrial automation is a primary growth driver, with the demand for precise and durable gears rising to support automated machinery and robotics. This trend is evident in automotive manufacturing and material handling sectors, where efficiency and reliability are critical.

- •Expansion of infrastructure projects globally, especially in emerging economies, fuels demand for industrial gears used in construction and power generation equipment, driving market growth significantly.

- •Technological advancements such as the integration of advanced materials and surface treatment processes enhance gear performance and longevity, attracting end users seeking to minimize downtime and maintenance costs.

- •Rising investments in renewable energy projects bolster the market, as gears are integral components in wind turbines and other sustainable energy machinery, fostering new growth avenues.

- •Growing adoption of planetary gears in compact and high torque applications supports market expansion, driven by their superior power density and efficiency in automotive and aerospace industries.

- •Increasing demand from the mining sector due to rising commodity demand leads to greater use of heavy-duty gears capable of withstanding harsh operating conditions, contributing to market growth.

- •Government initiatives promoting advanced manufacturing technologies and industrial modernization further stimulate market dynamics, encouraging innovation and capacity expansion.

Market Trends

- •The shift towards lightweight and high-strength materials in gear manufacturing is gaining momentum, enabling improved efficiency and reduced energy consumption in end-use applications.

- •Digitalization and Industry 4.0 adoption are influencing gear production processes, with smart manufacturing techniques allowing real-time quality monitoring and predictive maintenance.

- •Collaborative partnerships between gear manufacturers and end-user industries are becoming common to co-develop customized solutions tailored to specific operational challenges.

- •Sustainability considerations are driving demand for eco-friendly production methods and recyclable materials in gear manufacturing, aligning with global environmental regulations.

- •The rise in electric vehicle production is shifting gear design requirements towards quieter and more efficient transmissions, influencing product innovation in the automotive segment.

- •Emerging markets in Asia-Pacific are witnessing rapid adoption of industrial gears due to increasing manufacturing activities, infrastructure development, and favorable government policies.

- •Advancements in additive manufacturing (3D printing) are starting to influence prototype development and small-batch gear production, reducing lead times and costs.

Market Opportunities

- •Expanding the application of planetary gears in renewable energy and aerospace sectors presents significant growth potential due to their compact size and high torque capabilities.

- •Untapped markets in Latin America and Middle East & Africa offer opportunities for industrial gear manufacturers to establish presence through localized production and partnerships.

- •Investment in R&D focused on lightweight and wear-resistant materials can lead to innovative products with enhanced performance, opening new market segments.

- •Integration of IoT and sensor technologies in gears for predictive maintenance and performance monitoring can create value-added service offerings and competitive differentiation.

- •Collaborations with OEMs to develop customized gear solutions tailored for electric and autonomous vehicles can drive market expansion in emerging mobility sectors.

- •Growth in the aftermarket services segment, including repair and refurbishment of industrial gears, offers recurring revenue streams and customer retention opportunities.

- •Adoption of sustainable manufacturing practices aligned with global environmental standards can enhance brand reputation and attract eco-conscious clients.

Market Challenges

- •Fluctuations in raw material prices, particularly steel and alloy components, create cost pressures that challenge profitability and price stability for manufacturers.

- •High precision manufacturing requirements and quality standards demand significant capital investment, limiting entry for smaller players and increasing production costs.

- •Intense competition from regional manufacturers, especially in Asia-Pacific, pressures established players to innovate and optimize cost structures continuously.

- •Supply chain disruptions and logistical challenges, exacerbated by global events, pose risks to timely delivery and inventory management.

- •Regulatory compliance related to environmental and safety standards requires ongoing adaptation and can increase operational complexity and costs.

- •Technological obsolescence risk as newer transmission technologies emerge, necessitating continuous R&D investment to maintain market relevance.

- •Skilled labor shortages in precision engineering fields can hamper manufacturing efficiency and innovation capabilities.

Regulatory Framework

- •The Machinery Directive 2006/42/EC implemented across Europe mandates stringent safety and performance standards for mechanical components including industrial gears, ensuring operational safety since 2020, impacting manufacturers’ compliance obligations.

- •ISO 9001:2015 quality management standards adopted globally require gear manufacturers to maintain rigorous quality assurance processes, influencing production protocols and customer trust.

- •The REACH regulation in the European Union, effective since 2021, governs the use of chemical substances in manufacturing, affecting material selection and environmental compliance in gear production.

- •U.S. Environmental Protection Agency (EPA) regulations on emissions and waste management, enforced between 2020-2025, require manufacturers to adopt eco-friendly processes and reduce environmental impact.

- •China’s GB/T standards for gear manufacturing, updated in 2023, set comprehensive requirements for gear dimensions, materials, and heat treatment, driving quality improvements in the Asia-Pacific region.

Market Intelligence

- •15th March 2025, ZF Friedrichshafen AG launched a new line of lightweight helical gears designed for electric vehicles, featuring advanced alloy materials that reduce weight by 20% while maintaining strength. This innovation targets the growing EV market, aiming to improve transmission efficiency and support longer vehicle range. The product integrates seamlessly with existing drivetrain architectures, underscoring ZF’s commitment to sustainable mobility solutions. Source: Official ZF Press Release.

- •22nd July 2025, Dana Incorporated introduced an IoT-enabled planetary gear system equipped with sensors for real-time condition monitoring and predictive maintenance. The system is designed for industrial automation applications, enabling clients to reduce downtime and optimize operational efficiency through data-driven insights. This launch represents a strategic move to integrate digital technologies with mechanical components, enhancing value proposition and aftersales services. Source: Dana Corporate Website.

- •10th November 2025, Timken Company announced a strategic partnership with a leading renewable energy firm to supply custom bevel gears for next-generation wind turbines. This collaboration focuses on developing durable, high-performance gears capable of withstanding harsh offshore environments. The initiative aligns with global trends towards clean energy and positions Timken as a key supplier in the renewable sector. Source: Industry Publication - Renewable Energy News.

- •5th February 2025, SEW-Eurodrive GmbH & Co KG completed the acquisition of a regional gear manufacturer in Southeast Asia, expanding its footprint in the fast-growing Asia-Pacific market. The acquisition enables SEW-Eurodrive to enhance local manufacturing capabilities and better serve the increasing demand for industrial gears in the region. This strategic move complements SEW-Eurodrive’s global growth strategy and strengthens its competitive position. Source: SEW-Eurodrive Official Announcement.

- •Source: Official press releases, Corporate websites, Industry publications.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 52.3 Billion |

| Forecast Year Market Size | USD 89.7 Billion |

| CAGR | 6.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6% |

| Scope of Report | Market is segmented by Product Type (Helical Gears, Bevel Gears, Worm Gears, Spur Gears, Planetary Gears), Application (Material Handling, Automotive, Mining, Power Generation, Construction), End-Use Industry (Manufacturing, Automotive & Transportation, Energy & Utilities, Construction & Infrastructure), Distribution Channel (Direct Sales, Industrial Distributors, Aftermarket & Service Providers) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | ZF Friedrichshafen AG (Germany), Dana Incorporated (United States), Schaeffler Group (Germany), Timken Company (United States), Bonfiglioli Riduttori S.p.A. (Italy), SEW-Eurodrive GmbH & Co KG (Germany), Rotork plc (United Kingdom), Meritor, Inc. (United States), Nabtesco Corporation (Japan), Nord Drivesystems (Germany), Flender GmbH (Germany), Brevini Power Transmission S.p.A. (Italy), Gates Corporation (United States), ABB Ltd (Switzerland), WEG S.A. (Brazil), KHK Gears (Japan), Rexnord Corporation (United States), Hitachi Industrial Equipment Systems Co., Ltd. (Japan), NORD Drivesystems GmbH & Co. KG (Germany), Bonfiglioli Engineering S.p.A. (Italy), KTR Systems GmbH (Germany), Mitsubishi Heavy Industries (Japan), Altra Industrial Motion Corp. (United States), Sumitomo Heavy Industries (Japan), Harmonic Drive AG (Germany) |

Global Industrial Gears Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.