Global Printed Circuit Board Market Size, Growth & Revenue 2024-2034

Global Printed Circuit Board Market is segmented by Product Type (Rigid Printed Circuit Board, Flexible Printed Circuit Board, Rigid-Flex Printed Circuit Board, High-Density Interconnect (HDI) PCB, Ceramic Printed Circuit Board), Application (Consumer Electronics, Automotive Electronics, Industrial Electronics, Healthcare Devices, Telecommunications Equipment), End-Use Industry (Automotive, Consumer Electronics, Healthcare, Industrial Manufacturing), Distribution Channel (Direct Sales, Distributor Sales, Online Channels), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

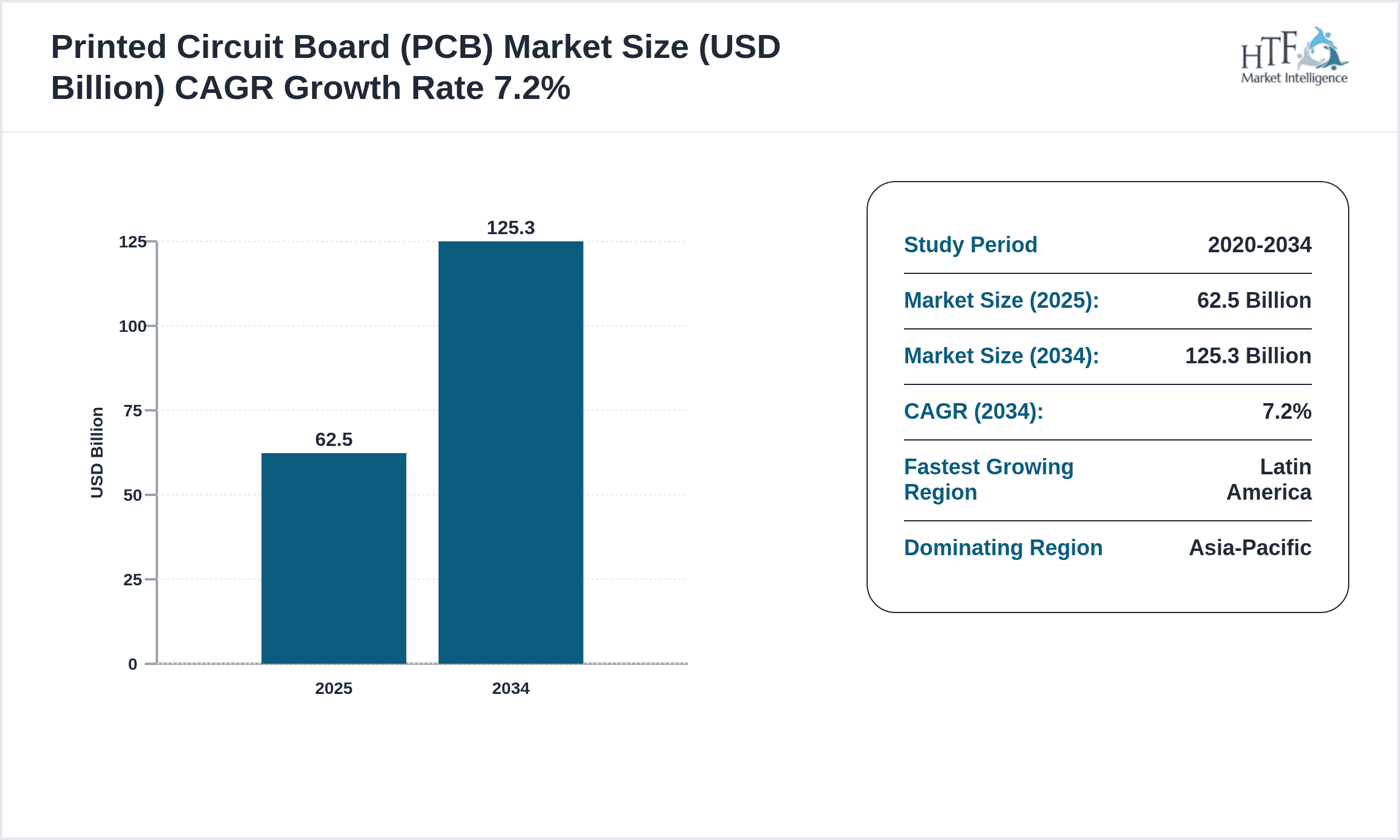

- •The global Printed Circuit Board (PCB) market is a fundamental segment of the electronics manufacturing industry, encompassing the production and application of diverse PCB types such as rigid, flexible, rigid-flex, HDI, and ceramic PCBs. These boards serve as the backbone for electrical connectivity and mechanical support in a wide array of devices including consumer electronics, automotive systems, healthcare equipment, telecommunications infrastructure, and industrial machinery. This market spans raw material procurement, manufacturing technologies, and assembly processes, reflecting advancements in miniaturization, increased device complexity, and evolving application demands. The market is shaped by rapid technological innovations such as IoT adoption, 5G deployment, and automotive electrification, driving increased PCB sophistication and volume globally. Environmental regulations and materials sustainability are also influencing production methods, while regional dynamics highlight Asia-Pacific's dominance due to extensive electronics manufacturing hubs. Forecasts project robust growth through 2034, supported by expanding end-use sectors and continuous innovation in PCB design and manufacturing technologies.

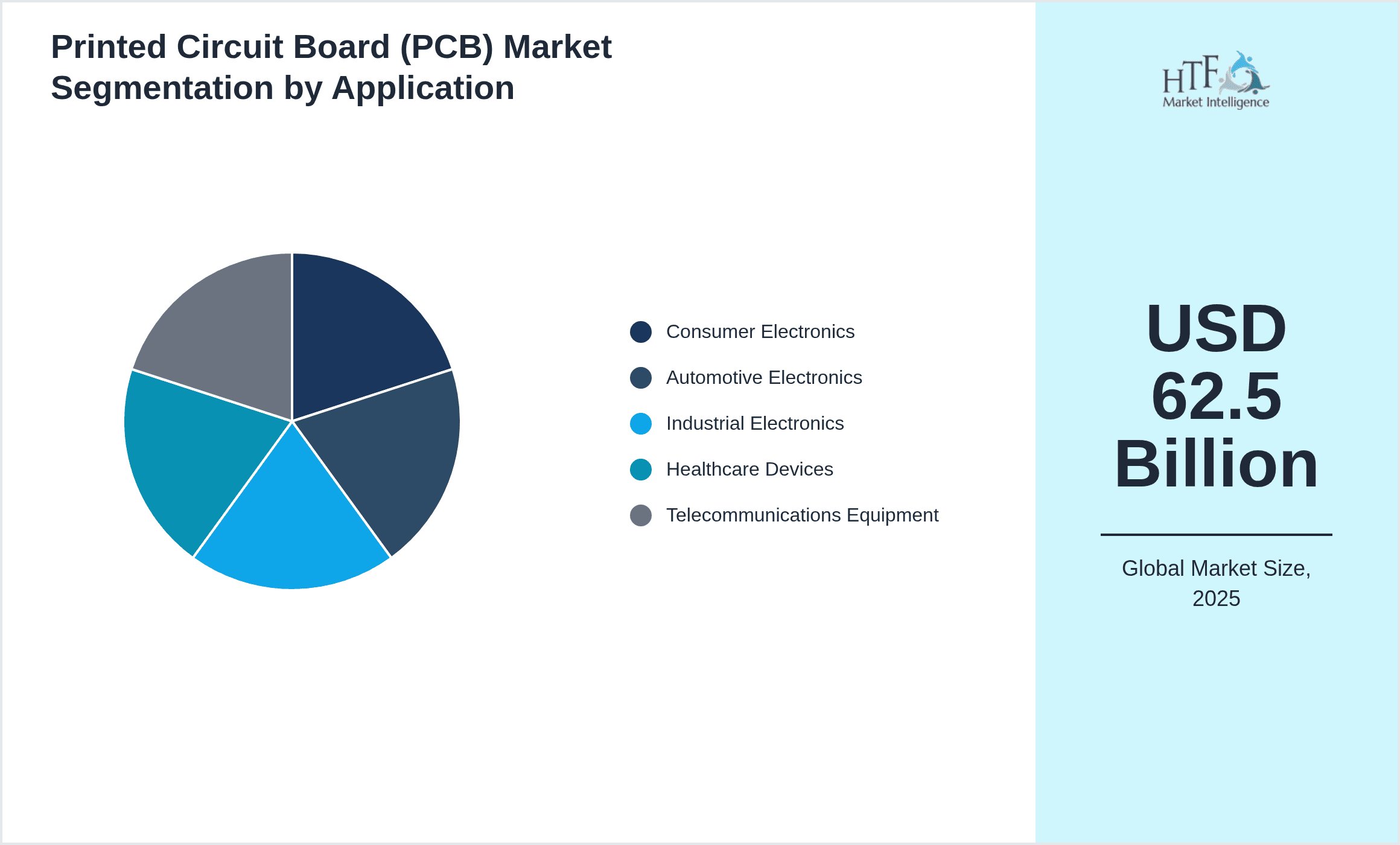

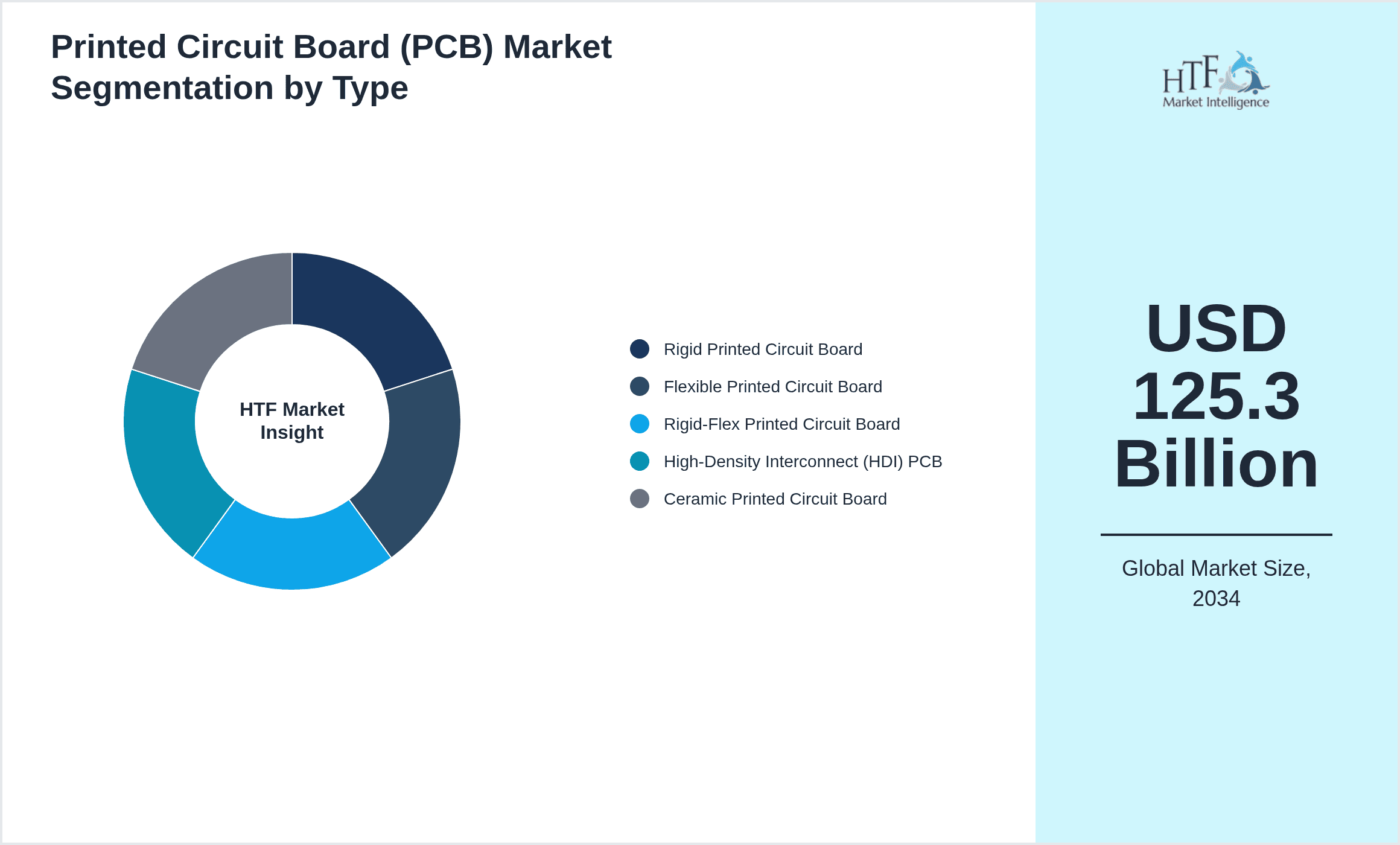

- •Key market highlights include a base market size of USD 62.5 Billion in 2024, expected to nearly double to USD 125.3 Billion by 2034, exhibiting a compound annual growth rate (CAGR) of 7.2%. The Asia-Pacific region leads market share, driven by manufacturing capacity and consumer electronics demand, while Latin America emerges as the fastest-growing region due to expanding industrialization and infrastructure investments. Rigid PCBs dominate the product landscape, accounting for the largest share, yet flexible PCBs show the fastest growth fueled by wearable devices and flexible electronics trends. Application-wise, consumer electronics remain the largest segment, followed by automotive PCBs, reflecting the rise in electric vehicles and advanced driver-assistance systems. Year-over-year growth rates align with the CAGR, indicating a steady expansion trajectory supported by innovation and diversified end-use adoption.

- •The market offers significant value propositions for electronics manufacturers, component suppliers, and end-user industries by enabling enhanced device performance, miniaturization, and reliability. Strategic importance is underscored by its role in supporting emerging technologies including IoT, 5G communications, automotive electrification, and medical instrumentation. Stakeholders benefit from continuous advancements in PCB materials and fabrication technologies that improve thermal management, signal integrity, and mechanical flexibility. Additionally, the market's evolution fosters opportunities for technological collaboration, capacity expansion, and entry into emerging regional markets. The PCB market's resilience and adaptability underpin its criticality in the global electronics value chain, making it essential for sustaining innovation across multiple industry verticals and meeting growing consumer demands worldwide.

Competitive Landscape

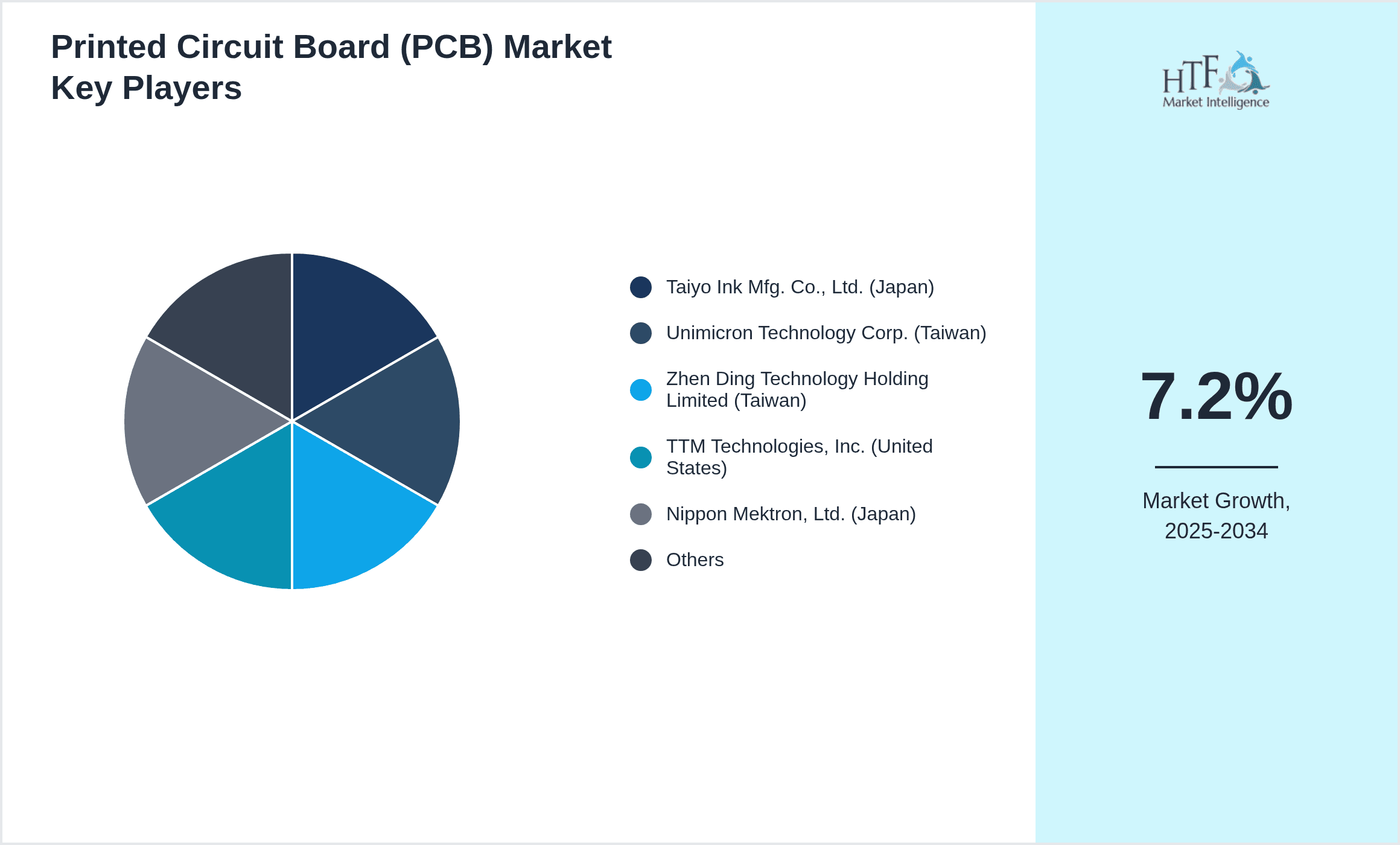

The global Printed Circuit Board market is highly competitive, characterized by a mix of large multinational manufacturers and specialized regional players. Market leaders continuously invest in R&D to innovate high-density interconnect (HDI) technologies, flexible and rigid-flex PCBs, and advanced materials to meet evolving end-user demands. Competitive strategies focus on product differentiation through enhanced performance, reducing manufacturing costs via automation, and expanding global footprint through strategic partnerships and acquisitions. Pricing pressures are moderated by the necessity for quality and reliability in critical applications such as automotive and healthcare. The rivalry intensifies as companies strive for technological leadership, compliance with environmental standards, and faster time-to-market. Distribution channels and after-sales services also influence competitive positioning. Emerging players leverage niche applications and regional cost advantages, while established firms focus on integrated supply chain solutions. Future competition is expected to be driven by digitalization of manufacturing, sustainability imperatives, and expansion into emerging markets.

Prominent Players in Printed Circuit Board Market

- •Taiyo Ink Mfg. Co., Ltd. (Japan)

- •Unimicron Technology Corp. (Taiwan)

- •Zhen Ding Technology Holding Limited (Taiwan)

- •TTM Technologies, Inc. (United States)

- •Nippon Mektron, Ltd. (Japan)

- •Compeq Manufacturing Co., Ltd. (Taiwan)

- •Ibiden Co., Ltd. (Japan)

- •AT&S Austria Technologie & Systemtechnik AG (Austria)

- •Meiko Electronics Co., Ltd. (Japan)

- •Shennan Circuits Company Limited (China)

- •Tripod Technology Corporation (Taiwan)

- •Multek Corporation (Taiwan)

- •Young Poong Group (South Korea)

- •Kinsus Interconnect Technology Corp. (Taiwan)

- •Simmtech Co., Ltd. (South Korea)

- •Sunwoda Electronic Co., Ltd. (China)

- •Meiko Electronics Co., Ltd. (Japan)

- •Flex Ltd. (United States)

- •Nanya PCB Co., Ltd. (Taiwan)

- •LG Innotek Co., Ltd. (South Korea)

- •Samsung Electro-Mechanics Co., Ltd. (South Korea)

- •HannStar Board Corporation (Taiwan)

- •Viasystems Group, Inc. (United States)

- •TT Electronics plc (United Kingdom)

- •Isola Group (United States)

Market Breakdown

- •By Product Type

- ◦Rigid Printed Circuit Board

- ◦Flexible Printed Circuit Board

- ◦Rigid-Flex Printed Circuit Board

- ◦High-Density Interconnect (HDI) PCB

- ◦Ceramic Printed Circuit Board

- •By Application

- ◦Consumer Electronics

- ◦Automotive Electronics

- ◦Industrial Electronics

- ◦Healthcare Devices

- ◦Telecommunications Equipment

- •By End-Use Industry

- ◦Automotive

- ◦Consumer Electronics

- ◦Healthcare

- ◦Industrial Manufacturing

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributor Sales

- ◦Online Channels

Growth Dynamics

- •The global PCB market growth is driven primarily by increasing demand for consumer electronics, automotive electrification, and industrial automation. The proliferation of smartphones, tablets, and wearable devices necessitates sophisticated PCBs, especially flexible and HDI types, which support miniaturization and complex circuitry. Furthermore, the automotive sector’s shift towards electric vehicles (EVs) and advanced driver-assistance systems (ADAS) significantly boosts PCB adoption due to the need for reliable, high-performance circuits. Industrial applications, including robotics and factory automation, also propel market expansion by integrating advanced PCBs for enhanced functionality and durability. This growth is complemented by advancements in 5G technology, which require high-frequency and high-density PCBs for infrastructure equipment. Additionally, rising investments in healthcare electronics, such as diagnostic and monitoring devices, contribute to sustained demand. Regional manufacturing hubs in Asia-Pacific further facilitate market scaling through cost efficiencies and capacity expansion, consolidating the market’s robust growth trajectory.

- •Emerging trends in the PCB market include the adoption of environmentally sustainable materials and processes, driven by stricter global regulations and corporate social responsibility initiatives. The integration of Industry 4.0 technologies such as automation, AI-powered quality control, and digital twins enhances manufacturing precision and reduces defects. Flexible and rigid-flex PCBs gain prominence as consumer and industrial devices demand greater form factor adaptability and reliability under mechanical stress. The rise of IoT ecosystems accelerates the need for specialized PCBs with enhanced signal integrity and low power consumption. Moreover, the transition to 5G networks stimulates demand for PCBs capable of supporting higher frequencies and data rates, challenging manufacturers to innovate materials and design techniques. Collaborative industry ecosystems and strategic partnerships also emerge to foster innovation and supply chain resilience. These trends collectively reshape the PCB market landscape, driving competitive differentiation and technological advancement.

- •Market restraints include the volatility of raw material prices such as copper and specialty laminates, which impact manufacturing costs and pricing strategies. Complex manufacturing processes for advanced PCBs, including HDI and flexible types, require significant capital investment and technical expertise, limiting entry for smaller players. Supply chain disruptions, exacerbated by geopolitical tensions and global pandemics, pose challenges in material availability and lead times, affecting production schedules. Environmental regulations targeting hazardous substances and waste management increase compliance costs and necessitate process adjustments. Additionally, intense competition and pricing pressures constrain profit margins, particularly in commoditized PCB segments. Variability in demand across end-use industries, influenced by economic cycles and technology adoption rates, also creates market uncertainties. These factors collectively restrain rapid expansion and require manufacturers to optimize operations and innovate to sustain competitiveness.

- •The global PCB market presents multiple opportunities, including expansion into emerging markets where industrialization and electronics adoption accelerate. The growing electric vehicle market offers significant potential for specialized PCBs designed for high reliability and thermal management. Development of next-generation PCBs incorporating advanced materials such as organic substrates and higher layer counts facilitates entry into high-performance computing and 5G infrastructure segments. Increasing demand for wearable and flexible electronics opens avenues for flexible and rigid-flex PCB manufacturers to innovate and capture niche markets. Strategic collaborations between material suppliers, manufacturers, and end-users enable co-development of customized solutions, enhancing value propositions. Additionally, investments in automation and smart manufacturing improve operational efficiencies, enabling competitive pricing and faster time-to-market. These opportunities encourage diversification and technological advancement, positioning market participants for sustainable growth amid evolving industry dynamics.

- •Key challenges in the PCB market include managing the complexity of rapidly evolving technologies, which demand continuous R&D investment and skilled workforce development. The high initial capital expenditure for advanced manufacturing equipment and facilities restricts scalability for smaller firms and intensifies competition among established players. Environmental compliance imposes additional operational constraints, requiring manufacturers to adapt processes and materials to meet stringent standards. Supply chain vulnerabilities, particularly for critical raw materials and components, expose manufacturers to risks of production delays and cost escalations. Furthermore, counterfeit PCBs and quality assurance issues pose risks to brand reputation and end-user safety, necessitating robust quality control mechanisms. Price volatility and margin pressures compel firms to balance innovation with cost efficiency. These challenges require strategic planning, technological agility, and collaborative industry efforts to maintain market leadership and ensure sustainable growth.

Market Trends

- •The PCB market is witnessing a significant shift towards sustainable manufacturing practices, with companies adopting eco-friendly materials and reducing hazardous waste in compliance with global environmental regulations. This trend aligns with increasing consumer and regulatory demand for greener electronics and helps mitigate environmental impact while enhancing corporate image.

- •Advancements in flexible and rigid-flex PCB technologies are gaining momentum, driven by the proliferation of wearable devices, foldable smartphones, and medical electronics that require lightweight, bendable, and compact circuit solutions. This adoption facilitates innovation in product design and user experience.

- •The integration of Industry 4.0 within PCB manufacturing is transforming production lines through automation, robotics, and real-time data analytics. These innovations improve yield rates, reduce defects, and shorten lead times, enhancing overall operational efficiency and responsiveness to market demands.

- •5G deployment globally is a strong market catalyst, necessitating PCBs with superior signal integrity, high-frequency performance, and thermal management capabilities. PCB manufacturers are innovating materials and design architectures to meet these stringent technical requirements.

- •Collaborative ecosystems between PCB manufacturers, raw material suppliers, and end-users are evolving to accelerate innovation cycles, improve supply chain resilience, and tailor solutions to specific industry applications, fostering competitive advantages and market responsiveness.

- •Market segmentation is increasingly refined, with companies focusing on customized PCB solutions for niche applications such as electric vehicles, aerospace, and healthcare to capture higher value and reduce commoditization risks.

- •Digital twin technology and virtual prototyping in PCB design are gaining traction, enabling manufacturers to optimize layouts and performance prior to physical production, thereby reducing development time and costs.

Market Opportunities

- •Emerging economies in Latin America and the Middle East & Africa present untapped markets with growing demand for consumer electronics and industrial automation, offering PCB manufacturers opportunities for geographic expansion and localized production facilities. Targeting these regions can yield substantial growth through adaptation to local market needs and cost-effective manufacturing.

- •The electric vehicle (EV) market’s rapid expansion creates demand for specialized PCBs with enhanced thermal management and reliability features, enabling suppliers to innovate and develop tailored products for automotive electronics and battery management systems. This vertical offers lucrative long-term growth potential.

- •Increasing adoption of flexible and wearable electronics invites PCB manufacturers to invest in R&D focused on flexible and rigid-flex technologies, tapping into growing consumer segments such as health monitoring devices and smart textiles. This technological advancement facilitates entry into high-growth niches.

- •Strategic partnerships and joint ventures with technology providers and end-users enable co-creation of customized PCB solutions, improving market responsiveness and fostering innovation. Such collaborations can reduce time-to-market and enhance competitive positioning.

- •Investment in Industry 4.0 and smart manufacturing technologies presents opportunities to optimize production efficiency, reduce costs, and improve quality control, enabling PCB companies to enhance profitability and deliver superior customer value in a competitive landscape.

- •Expansion into high-frequency PCB segments supporting 5G infrastructure and advanced computing offers avenues for product portfolio diversification and higher-margin revenues, aligning with future technology trends and infrastructure investments globally.

- •Growing demand for environmentally compliant and lead-free PCBs creates opportunities for manufacturers to differentiate through sustainable product offerings, aligning with regulatory trends and consumer preferences toward green electronics.

Market Challenges

- •The PCB industry faces challenges from raw material price volatility, particularly copper and specialty laminates, which directly impact production costs and pricing strategies, creating financial uncertainty for manufacturers and limiting margin expansion capabilities.

- •High capital requirements for advanced manufacturing equipment and stringent process controls limit the entry of new players and restrict the scalability of smaller firms, contributing to market consolidation and intensifying competition among established manufacturers.

- •Environmental regulations such as RoHS and REACH impose continuous compliance demands, requiring manufacturers to invest in updated equipment and processes, increasing operational costs and complexity in global supply chains.

- •Supply chain disruptions, including logistics challenges and geopolitical tensions, affect the timely availability of raw materials and components, leading to production delays and increased costs, impacting customer satisfaction and contractual obligations.

- •The proliferation of counterfeit PCBs in the market undermines brand integrity and poses risks to end-user safety, necessitating robust quality assurance protocols and traceability systems to maintain market trust and compliance.

- •Rapid technological evolution requires continuous R&D investments and skilled workforce development, creating challenges in maintaining innovation pipelines and adapting to shifting industry standards and customer expectations.

- •Price competition, especially in commoditized PCB segments, pressures profitability and compels manufacturers to balance cost reduction efforts with maintaining product quality and technological differentiation.

Regulatory Framework

- •Between 2019 and 2024, the global PCB market has been increasingly influenced by environmental regulations such as the Restriction of Hazardous Substances Directive (RoHS) and Registration, Evaluation, Authorization and Restriction of Chemicals (REACH), mandating reductions in hazardous materials to ensure safe manufacturing and disposal. Compliance involves adherence to strict substance limits and reporting requirements, impacting materials selection and production processes globally.

- •Safety standards including IPC-2221 and IPC-6012 have been updated to incorporate new quality and reliability requirements, guiding manufacturers in design and fabrication to ensure durability and performance, particularly for high-reliability sectors like automotive and healthcare electronics.

- •Data security and intellectual property regulations have gained prominence, compelling PCB manufacturers to implement secure handling of design files and proprietary information to prevent counterfeiting and unauthorized production, thus protecting innovation and market position.

- •Regional mandates such as China’s RoHS 2 and the European Union’s Green Deal have introduced stricter environmental compliance frameworks, influencing raw material sourcing and waste management practices, with timelines set for gradual enforcement through 2025 and beyond.

- •Government incentives promoting green manufacturing and technology upgrades have emerged in several regions, offering subsidies and tax benefits to PCB producers adopting sustainable practices and advanced production technologies, fostering industry modernization.

Market Intelligence

- •15th March 2024, Unimicron Technology Corp. launched a new series of advanced HDI PCBs designed for 5G infrastructure applications featuring enhanced signal integrity and thermal dissipation capabilities. This product aims to address the growing demand for high-frequency, high-density circuits in telecommunications, positioning Unimicron as a key supplier in next-generation network deployment. The launch is expected to strengthen Unimicron’s market share in the rapidly expanding 5G segment and support global infrastructure build-out efforts. Source: Company press release

- •8th November 2023, TTM Technologies announced the expansion of its manufacturing facility in Mexico to increase production capacity for automotive PCBs catering to electric vehicles. The investment includes automation upgrades and quality control enhancements to meet stringent automotive standards and rising EV demand. This strategic expansion supports TTM’s objective to capitalize on the automotive electronics growth and diversify its geographic production footprint. The move is anticipated to improve supply chain resilience and reduce lead times for North American customers. Source: Industry publication

- •22nd July 2024, AT&S Austria Technologie & Systemtechnik AG introduced a new environmentally friendly PCB substrate material with reduced halogen content and improved recyclability. This innovation aligns with increasing regulatory pressure and customer demand for sustainable electronics components. The new material delivers comparable electrical performance while significantly lowering environmental impact during production and disposal. AT&S aims to leverage this advancement to gain a competitive edge in green electronics manufacturing and meet evolving market requirements. Source: Company website

- •3rd February 2025, Nippon Mektron, Ltd. completed a strategic collaboration with a leading wearable device manufacturer to co-develop flexible PCBs with enhanced bendability and durability for next-generation health monitoring products. This partnership accelerates innovation in flexible electronics and expands Nippon Mektron’s presence in the growing wearable market. The collaboration focuses on optimizing materials and manufacturing processes to support complex designs and high-volume production. Source: Official press release

Regional Outlook

The Asia-Pacific currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Latin America is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 62.5 Billion |

| Forecast Year Market Size | USD 125.3 Billion |

| CAGR | 7.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by Product Type (Rigid Printed Circuit Board, Flexible Printed Circuit Board, Rigid-Flex Printed Circuit Board, High-Density Interconnect (HDI) PCB, Ceramic Printed Circuit Board), Application (Consumer Electronics, Automotive Electronics, Industrial Electronics, Healthcare Devices, Telecommunications Equipment), End-Use Industry (Automotive, Consumer Electronics, Healthcare, Industrial Manufacturing), Distribution Channel (Direct Sales, Distributor Sales, Online Channels) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Taiyo Ink Mfg. Co., Ltd. (Japan), Unimicron Technology Corp. (Taiwan), Zhen Ding Technology Holding Limited (Taiwan), TTM Technologies, Inc. (United States), Nippon Mektron, Ltd. (Japan), Compeq Manufacturing Co., Ltd. (Taiwan), Ibiden Co., Ltd. (Japan), AT&S Austria Technologie & Systemtechnik AG (Austria), Meiko Electronics Co., Ltd. (Japan), Shennan Circuits Company Limited (China), Tripod Technology Corporation (Taiwan), Multek Corporation (Taiwan), Young Poong Group (South Korea), Kinsus Interconnect Technology Corp. (Taiwan), Simmtech Co., Ltd. (South Korea), Sunwoda Electronic Co., Ltd. (China), Meiko Electronics Co., Ltd. (Japan), Flex Ltd. (United States), Nanya PCB Co., Ltd. (Taiwan), LG Innotek Co., Ltd. (South Korea), Samsung Electro-Mechanics Co., Ltd. (South Korea), HannStar Board Corporation (Taiwan), Viasystems Group, Inc. (United States), TT Electronics plc (United Kingdom), Isola Group (United States) |

Global Printed Circuit Board Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.