Global Railway Infrastructure Equipments Market Size, Growth & Revenue 2024-2034

Global Railway Infrastructure Equipments Market is segmented by Product Type (Track Components (rails, sleepers, fasteners), Signaling Equipment (interlocking systems, train control), Electrification Equipment (overhead lines, transformers), Communication Systems (radio, fiber optics), Maintenance Tools (inspection, repair equipment)), Application (Track Construction & Maintenance, Signaling & Telecommunications, Electrification Systems, Station Infrastructure, Rolling Stock Maintenance), End-Use Industry (Passenger Rail, Freight Rail, Urban Transit Systems, High-Speed Rail), Distribution Channel (Direct Sales, Distributors & Dealers, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Railway Infrastructure Equipments Market comprises a comprehensive portfolio of products and technologies essential for the construction, operation, and maintenance of railway networks across continents. This market includes critical components such as track components (rails, sleepers, fasteners), signaling and telecommunications systems for train control and safety, electrification equipment enabling the shift to electric-powered trains, communication systems for operational coordination, and specialized maintenance tools. It serves a wide range of applications including track construction and maintenance, station infrastructure development, and rolling stock upkeep. The industry is characterized by continuous modernization efforts, driven by growing demand for efficient public transit, freight transport expansion, and government investments in sustainable infrastructure. Innovations such as digital signaling, IoT-enabled maintenance, and green electrification technologies are transforming the landscape. The market’s scope spans multiple global regions, addressing diverse regulatory environments and infrastructure maturity levels, making it vital for transportation and economic development worldwide.

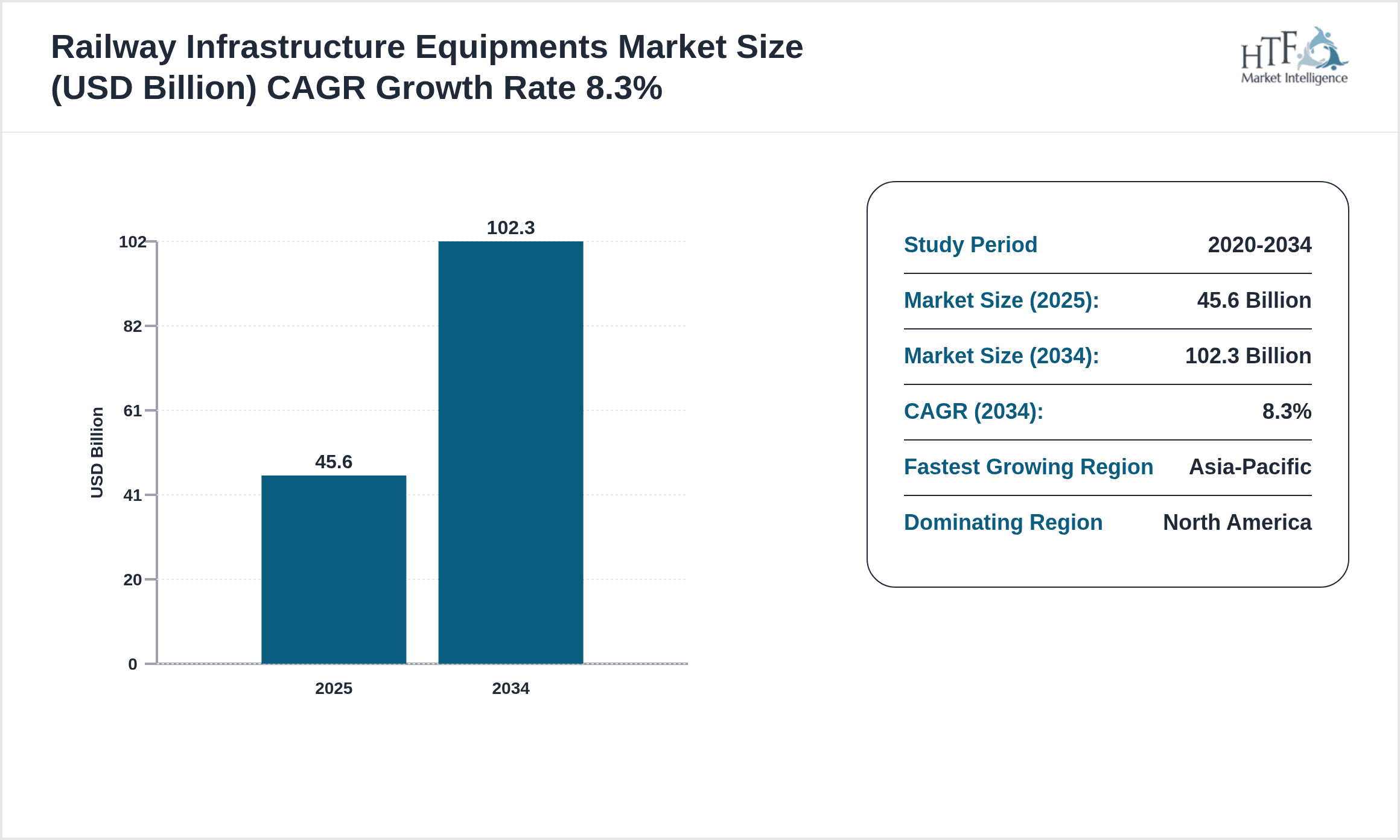

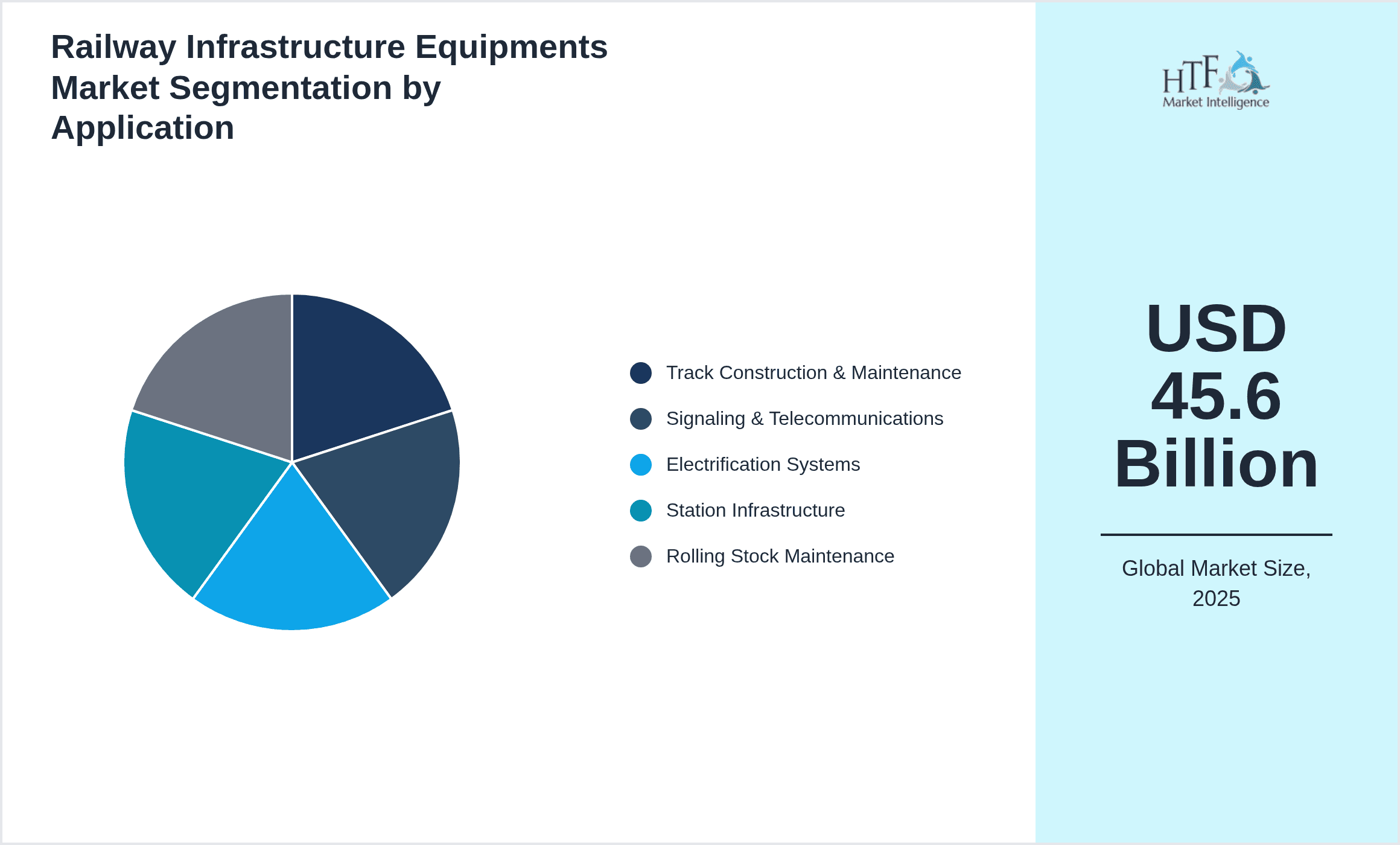

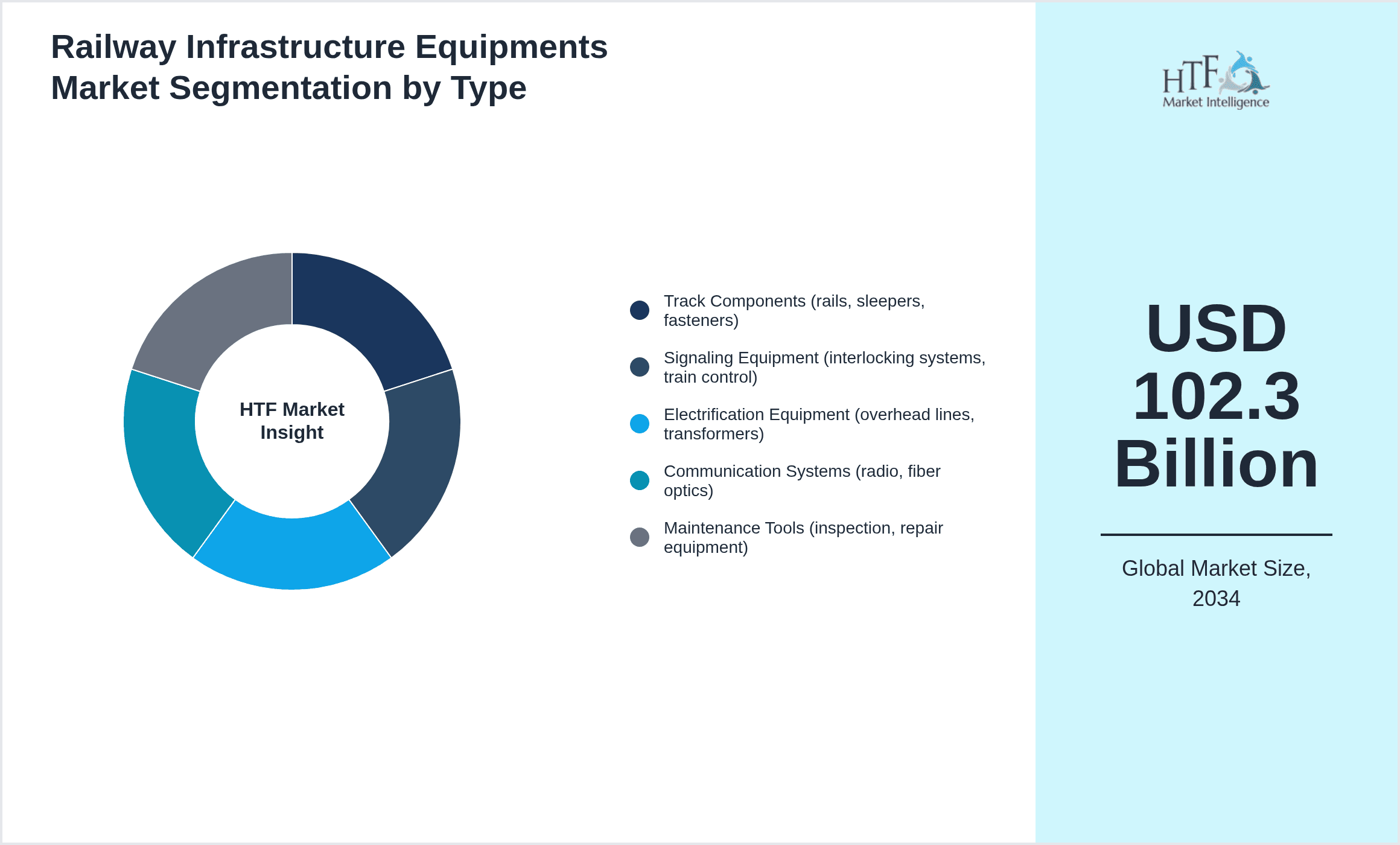

- •Key market highlights reveal a strong base market size of USD 45.6 Billion in 2024, projected to expand to USD 102.3 Billion by 2034, reflecting a robust CAGR of 8.3%. The North American region currently dominates due to its advanced rail infrastructure and substantial investments, while Asia-Pacific shows the fastest growth driven by rapid urbanization and rail network expansions. Track Components remain the leading product type owing to their fundamental role in rail operations, whereas Electrification Equipment emerges as the fastest-growing segment fueled by the shift towards electric mobility. Applications such as Track Construction & Maintenance hold the largest market share given ongoing infrastructure upgrades, with Signaling & Telecommunications also growing rapidly due to digital transformation initiatives.

- •This market offers significant value propositions to stakeholders including railway operators, infrastructure developers, equipment manufacturers, and governments. The strategic importance lies in enabling safer, more efficient, and environmentally sustainable rail transport solutions that support economic growth and connectivity. Investments in advanced railway equipment help reduce operational costs, enhance network capacity, and meet stringent safety and environmental standards. Furthermore, the market supports the global transition to green transportation, thereby aligning with sustainability goals. Consequently, players benefit from expanding opportunities in emerging economies and upgrading aging infrastructure in developed regions, positioning the Railway Infrastructure Equipments Market as a critical sector in the global transportation ecosystem.

Competitive Landscape

The global Railway Infrastructure Equipments Market is intensely competitive and marked by continuous innovation and strategic collaborations. Market players pursue differentiation through technological advancements such as digital signaling solutions, IoT-enabled maintenance systems, and energy-efficient electrification equipment. Competition is driven by the need to secure large infrastructure contracts, foster long-term partnerships with railway operators, and expand geographically into fast-growing regions like Asia-Pacific and Latin America. Companies adopt varied strategies including mergers and acquisitions to consolidate market position, invest in R&D for product innovation, and enhance after-sales services. Pricing dynamics are influenced by cost optimization efforts and the demand for high-reliability equipment. Entry barriers include high capital requirements, stringent regulatory compliance, and established customer relationships, which collectively shape the competitive landscape. The focus on sustainable and smart railway solutions is likely to intensify competition, while regional preferences and local manufacturing capabilities add complexity to market rivalry.

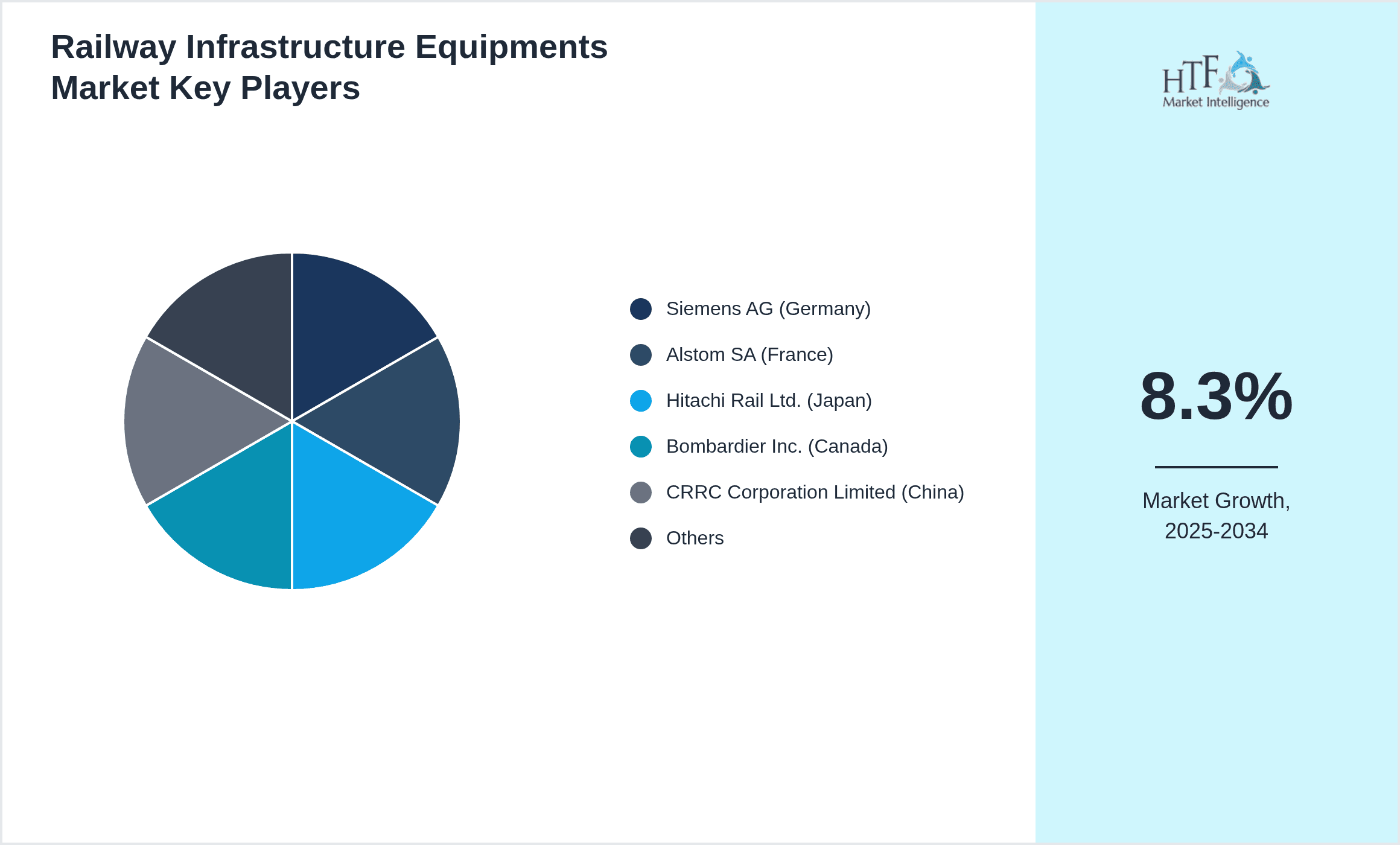

Prominent Players in Railway Infrastructure Equipments Market

- •Siemens AG (Germany)

- •Alstom SA (France)

- •Hitachi Rail Ltd. (Japan)

- •Bombardier Inc. (Canada)

- •CRRC Corporation Limited (China)

- •General Electric Company (United States)

- •Mitsubishi Electric Corporation (Japan)

- •Thales Group (France)

- •Progress Rail Services Corporation (United States)

- •CAF Power & Automation (Spain)

- •Knorr-Bremse AG (Germany)

- •Wabtec Corporation (United States)

- •Toshiba Infrastructure Systems & Solutions Corporation (Japan)

- •Siemens Mobility GmbH (Germany)

- •Alfa Laval AB (Sweden)

- •Larsen & Toubro Limited (India)

- •Kawasaki Heavy Industries, Ltd. (Japan)

- •Hyundai Rotem Company (South Korea)

- •Hitachi Ltd. (Japan)

- •Voestalpine AG (Austria)

- •General Electric Transportation (United States)

- •ABB Ltd. (Switzerland)

- •Siemens Energy (Germany)

- •Schneider Electric SE (France)

- •Bombardier Transportation (Germany)

Market Breakdown

- •By Product Type

- ◦Track Components (rails, sleepers, fasteners)

- ◦Signaling Equipment (interlocking systems, train control)

- ◦Electrification Equipment (overhead lines, transformers)

- ◦Communication Systems (radio, fiber optics)

- ◦Maintenance Tools (inspection, repair equipment)

- •By Application

- ◦Track Construction & Maintenance

- ◦Signaling & Telecommunications

- ◦Electrification Systems

- ◦Station Infrastructure

- ◦Rolling Stock Maintenance

- •By End-Use Industry

- ◦Passenger Rail

- ◦Freight Rail

- ◦Urban Transit Systems

- ◦High-Speed Rail

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Dealers

- ◦Online Platforms

Growth Dynamics

- •Rising demand for sustainable and efficient transportation systems is accelerating investments in railway infrastructure equipment globally. Governments are prioritizing rail modernization projects to reduce carbon emissions and traffic congestion, driving demand for advanced electrification and signaling technologies.

- •Technological advancements such as digital signaling, automated maintenance tools, and IoT-based monitoring are revolutionizing railway infrastructure, enhancing safety and operational efficiency. These innovations encourage stakeholders to upgrade existing equipment and adopt smart solutions.

- •Rapid urbanization and expansion of public transit systems in emerging economies, particularly in Asia-Pacific and Latin America, create significant growth opportunities for railway infrastructure equipment manufacturers.

- •Increasing investments in high-speed rail networks worldwide stimulate demand for specialized track components and electrification systems tailored to high-performance requirements, fostering market growth.

- •Government initiatives focused on infrastructure development and public-private partnerships provide financial support and policy frameworks that facilitate market expansion and innovation adoption.

- •Growing replacement and maintenance needs driven by aging railway infrastructure in developed regions like North America and Europe sustain steady demand for maintenance tools and upgrade equipment.

- •Global emphasis on interoperability and standardization of railway equipment encourages international collaborations and cross-border projects, broadening market reach for key players.

Market Trends

- •The proliferation of digital signaling systems replacing traditional relay-based technologies is a dominant trend, improving train control accuracy and reducing human error. This trend is supported by leading suppliers investing heavily in R&D.

- •Electrification of rail networks is accelerating, driven by environmental regulations and the push to reduce fossil fuel dependence. This shift results in increased demand for overhead catenary systems and power converters.

- •Integration of IoT and predictive maintenance technologies enables real-time asset monitoring, reducing downtime and maintenance costs, a growing trend embraced by rail operators worldwide.

- •Sustainability initiatives encourage use of eco-friendly materials and energy-efficient equipment, influencing product development and procurement decisions across the supply chain.

- •Collaborative ventures between equipment manufacturers and technology firms are rising to develop smart railway solutions, combining expertise in hardware and digital applications.

- •Shift towards modular and standardized components facilitates faster installation and easier maintenance, enhancing overall railway infrastructure efficiency.

- •Expansion of urban transit projects globally, especially metro and light rail systems, is driving demand for specialized infrastructure equipment tailored to urban environments.

Market Opportunities

- •Emerging economies present significant opportunities for railway infrastructure equipment growth due to expanding rail networks and underdeveloped transit systems requiring modernization and new installations.

- •Advancements in green technologies and electrification offer opportunities for equipment manufacturers to develop energy-efficient products that align with global decarbonization goals.

- •Digital transformation in railway operations opens avenues for introducing innovative signaling, communication, and maintenance solutions with enhanced safety and cost benefits.

- •Increasing government funding and policy support for high-speed rail projects create lucrative prospects for specialized infrastructure equipment providers.

- •Collaborations and joint ventures between global and regional players can unlock access to new markets and facilitate technology transfer, expanding business footprints.

- •Development of integrated station infrastructure combining passenger amenities with advanced equipment offers manufacturers novel product development opportunities.

- •Growing emphasis on predictive maintenance and asset management tools creates demand for advanced maintenance tools and software solutions.

Market Challenges

- •High capital expenditure required for railway infrastructure upgrades and new installations can limit investments, especially in developing markets with budget constraints.

- •Complex regulatory requirements and diverse standards across regions impose compliance challenges and increase time-to-market for new equipment.

- •Supply chain disruptions, including raw material shortages and logistics delays, hamper timely delivery and increase production costs for equipment manufacturers.

- •Rapid technological changes require continuous R&D investment, posing risks for companies unable to keep pace with innovation and market demands.

- •Competition from low-cost manufacturers and regional players intensifies pricing pressures and threatens market share of established companies.

- •Skilled labor shortages and technical expertise gaps affect quality and efficiency in railway infrastructure projects.

- •Long project cycles and complex stakeholder coordination delay implementation and affect revenue recognition for equipment suppliers.

Regulatory Framework

- •Between 2019 and 2024, the International Union of Railways (UIC) updated safety standards emphasizing interoperability and digital signaling compliance, requiring manufacturers to align products accordingly.

- •The European Railway Agency enforced stricter environmental regulations from 2020, mandating reductions in emissions and noise pollution associated with railway infrastructure equipment.

- •In 2021, several countries introduced mandatory certification programs for electrification equipment to ensure energy efficiency and safety, impacting product development cycles.

- •North American regulatory bodies implemented enhanced cybersecurity requirements for railway communication systems during 2022-2023, mandating robust data protection measures.

- •Government incentives and subsidies launched globally between 2020 and 2024 support adoption of green railway technologies, promoting investment in electrification and smart infrastructure equipment.

Market Intelligence

- •15th January 2025, Siemens AG launched an advanced digital signaling platform featuring AI-driven predictive analytics aimed at improving train punctuality and safety across European rail networks. This innovation is expected to significantly reduce operational disruptions and maintenance costs, positioning Siemens as a leader in smart railway solutions. Source: Siemens Official Press Release

- •20th March 2025, Alstom SA introduced next-generation electrification equipment capable of supporting ultra-high-speed rail lines with enhanced energy efficiency and reduced maintenance needs. The product is targeted at expanding high-speed rail projects in Asia-Pacific and Europe, addressing growing demand for sustainable transportation infrastructure. Source: Alstom Corporate News

- •12th May 2025, Hitachi Rail Ltd. announced a strategic partnership with a leading IoT technology firm to develop integrated maintenance tools that leverage real-time data for predictive asset management. This collaboration aims to optimize railway infrastructure lifecycle costs and enhance safety standards globally. Source: Hitachi Rail Press Release

- •8th July 2025, Bombardier Inc. completed the acquisition of a regional signaling equipment manufacturer to expand its product portfolio and strengthen market presence in Latin America. This move enhances Bombardier’s capability to deliver end-to-end railway infrastructure solutions tailored to emerging markets. Source: Bombardier Corporate Communications

- •Source: Official press releases / Company websites / Industry publications

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45.6 Billion |

| Forecast Year Market Size | USD 102.3 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.9% |

| Scope of Report | Market is segmented by Product Type (Track Components (rails, sleepers, fasteners), Signaling Equipment (interlocking systems, train control), Electrification Equipment (overhead lines, transformers), Communication Systems (radio, fiber optics), Maintenance Tools (inspection, repair equipment)), Application (Track Construction & Maintenance, Signaling & Telecommunications, Electrification Systems, Station Infrastructure, Rolling Stock Maintenance), End-Use Industry (Passenger Rail, Freight Rail, Urban Transit Systems, High-Speed Rail), Distribution Channel (Direct Sales, Distributors & Dealers, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Siemens AG (Germany), Alstom SA (France), Hitachi Rail Ltd. (Japan), Bombardier Inc. (Canada), CRRC Corporation Limited (China), General Electric Company (United States), Mitsubishi Electric Corporation (Japan), Thales Group (France), Progress Rail Services Corporation (United States), CAF Power & Automation (Spain), Knorr-Bremse AG (Germany), Wabtec Corporation (United States), Toshiba Infrastructure Systems & Solutions Corporation (Japan), Siemens Mobility GmbH (Germany), Alfa Laval AB (Sweden), Larsen & Toubro Limited (India), Kawasaki Heavy Industries, Ltd. (Japan), Hyundai Rotem Company (South Korea), Hitachi Ltd. (Japan), Voestalpine AG (Austria), General Electric Transportation (United States), ABB Ltd. (Switzerland), Siemens Energy (Germany), Schneider Electric SE (France), Bombardier Transportation (Germany) |

Global Railway Infrastructure Equipments Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.