Global Sleepwear Market Size, Growth & Revenue 2024-2034

Global Sleepwear Market is segmented by Type (Cotton Sleepwear, Silk Sleepwear, Synthetic Sleepwear, Wool Sleepwear, Blended Fabrics), Application (Men, Women, Children, Infants, Others), End-Use Industry (Retail Stores, Online Retailers, Specialty Stores, Department Stores), Distribution Channel (Offline Distribution, Online Distribution, Direct Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global sleepwear market represents a dynamic segment of the apparel industry focused on garments designed for sleeping comfort, style, and health benefits. The market includes diverse product types ranging from cotton and silk to synthetic and blended fabrics, catering to men, women, children, and infants. It spans multiple distribution channels including online retail, specialty stores, and department outlets. The industry is characterized by continuous innovation in materials, such as the incorporation of sustainable fabrics and temperature-regulating technologies. Rising consumer focus on wellness and comfort, alongside increasing disposable incomes particularly in emerging economies, has led to robust demand growth worldwide. Key regions driving the market include North America, Europe, and Asia-Pacific, with Asia-Pacific emerging as the fastest growing due to expanding middle-class populations and evolving lifestyle trends. The market also faces challenges such as raw material price fluctuations and stringent regulatory standards on textile safety. Strategic collaborations, product diversification, and expansion into untapped regions offer significant growth prospects through 2034.

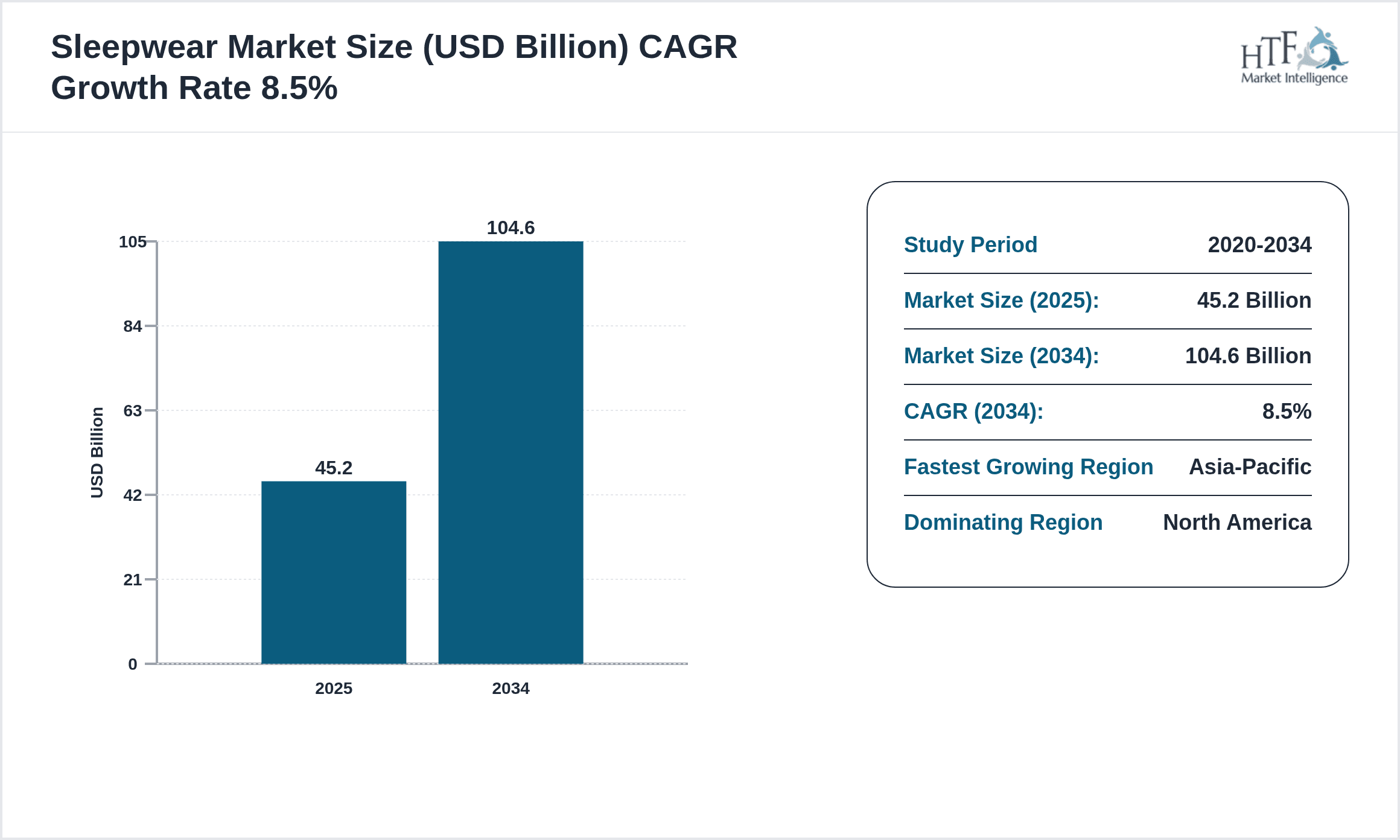

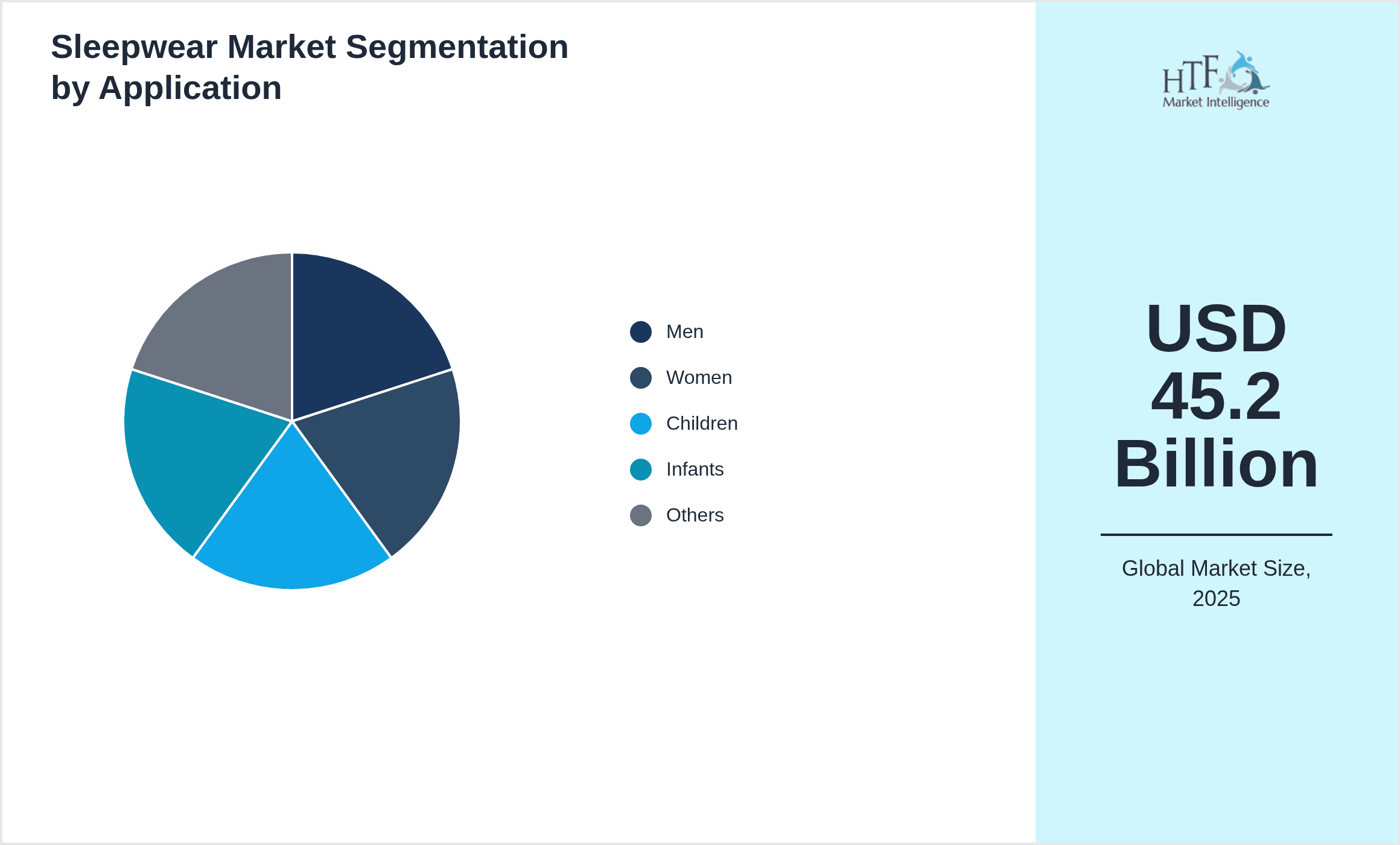

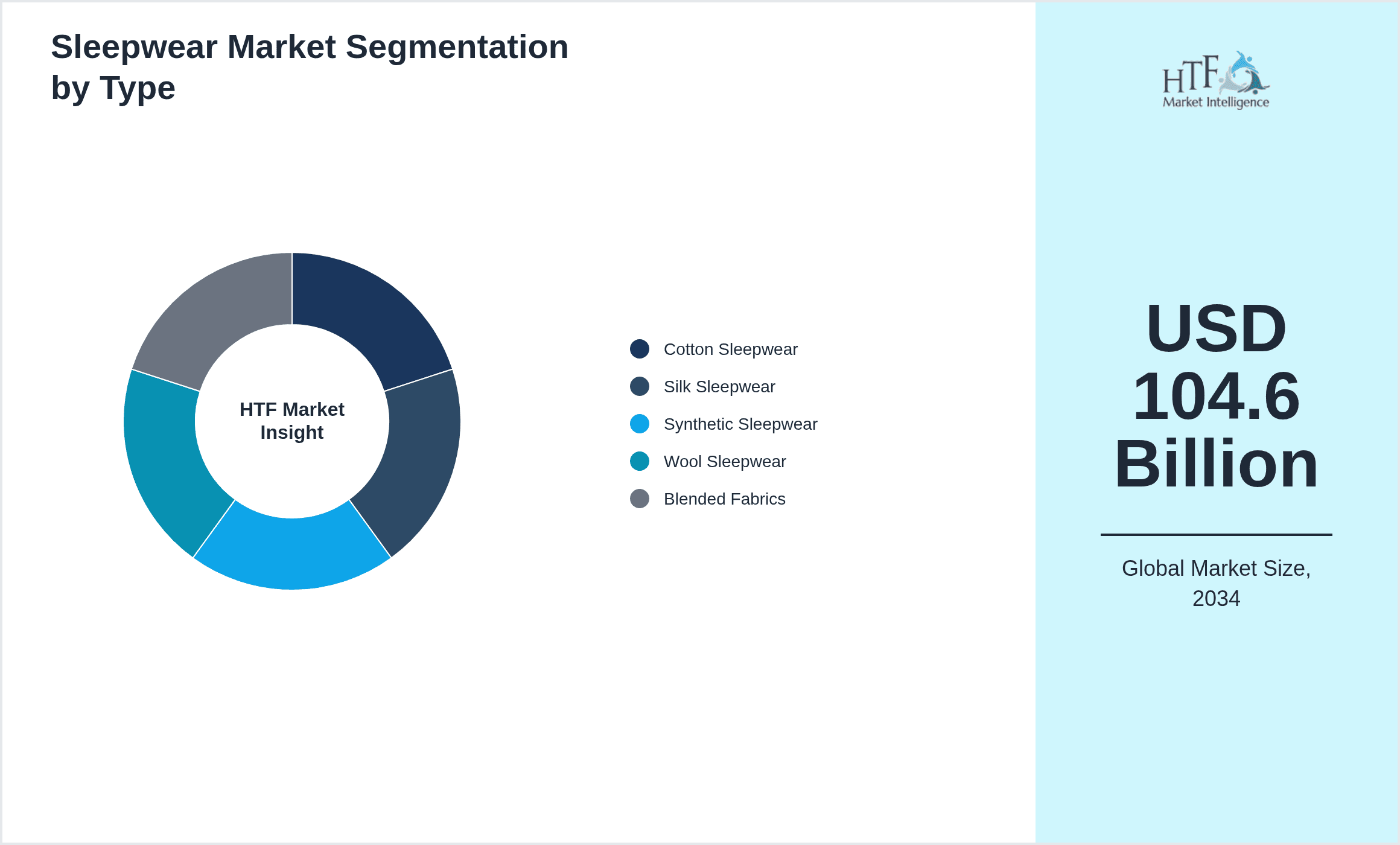

- •Market highlights include a base market size of USD 45.2 Billion in 2024 with an expected growth to USD 104.6 Billion by 2034, reflecting a CAGR of 8.5%. Cotton sleepwear dominates the product segment due to its breathability and comfort, while silk sleepwear is the fastest-growing type driven by luxury and premium consumer segments. Men and women represent the largest applications, with increasing demand for children’s and infant sleepwear. North America holds the largest market share owing to high consumer spending and fashion consciousness, whereas Asia-Pacific exhibits the highest growth rate fueled by urbanization and e-commerce expansion. Key players focus on innovation, sustainability, and omnichannel retailing to capture market share. Year-over-year growth remains positive at approximately 8.2%, signaling strong market momentum.

- •The sleepwear market's strategic importance spans fashion, wellness, and lifestyle industries, offering manufacturers and retailers opportunities to leverage growing consumer preference for comfortable and sustainable apparel. The integration of advanced textile technologies and personalized offerings enhances product differentiation. For stakeholders, this market presents avenues for expansion via digital sales platforms, collaborations with designers, and penetration into emerging markets. Moreover, regulatory emphasis on product safety and environmental compliance ensures quality standards, reinforcing consumer trust. The market’s growth trajectory aligns with broader societal shifts towards health-conscious living and leisure-focused apparel, positioning sleepwear as a vital segment in global apparel portfolios.

Competitive Landscape

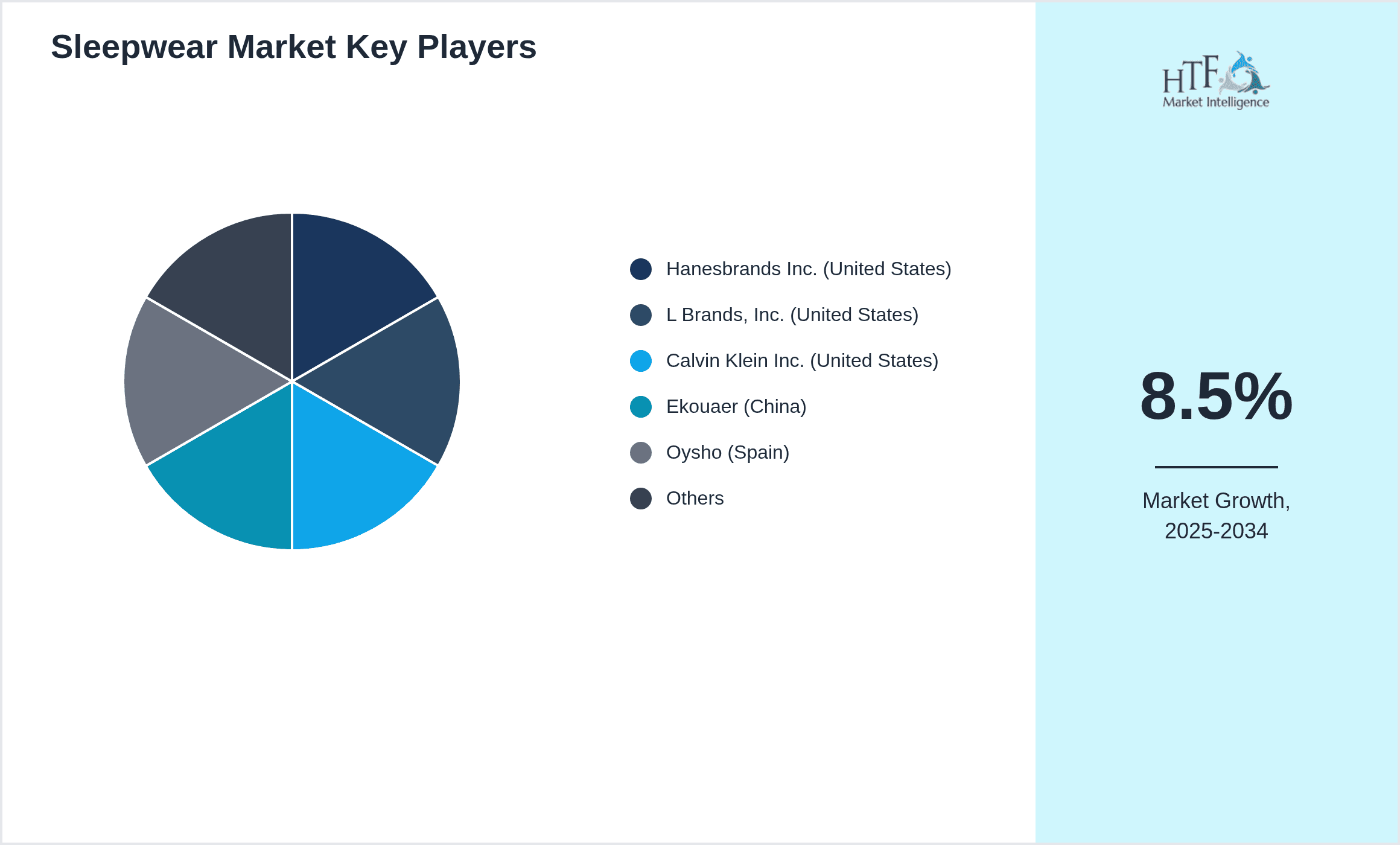

The global sleepwear market competition is characterized by the presence of established multinational corporations and numerous regional players striving for market dominance through innovation, brand equity, and expansive distribution networks. Companies emphasize sustainable fabric development, seamless design integration, and advanced comfort technologies to differentiate their offerings. Strategic investments in digital marketing, omnichannel retailing, and consumer engagement initiatives enhance brand loyalty. Intense rivalry fosters continuous product enhancements and competitive pricing strategies. Mergers and acquisitions are frequent, enabling companies to expand geographic reach and diversify product portfolios. Barriers to entry include high capital requirements and the need for strong supply chain management. Regional competition varies, with North America and Europe focusing on premium products, while Asia-Pacific leverages cost efficiency and rapid urbanization. Future trends suggest increased convergence of fashion and functionality, with personalized and eco-friendly sleepwear gaining prominence in competitive strategies.

Companies Shaping the Sleepwear Market

- •Hanesbrands Inc. (United States)

- •L Brands, Inc. (United States)

- •Calvin Klein Inc. (United States)

- •Ekouaer (China)

- •Oysho (Spain)

- •Gildan Activewear Inc. (Canada)

- •Jockey International, Inc. (United States)

- •H&M Hennes & Mauritz AB (Sweden)

- •Victoria's Secret (United States)

- •Fruit of the Loom, Inc. (United States)

- •Marks & Spencer Group plc (United Kingdom)

- •Uniqlo Co., Ltd. (Japan)

- •Zara (Spain)

- •Target Corporation (United States)

- •Amazon.com, Inc. (United States)

- •Gap Inc. (United States)

- •Intimissimi (Italy)

- •Decathlon S.A. (France)

- •M&S (United Kingdom)

- •Victoria’s Secret & Co. (United States)

- •Next plc (United Kingdom)

- •Abercrombie & Fitch Co. (United States)

- •ASOS plc (United Kingdom)

- •Lululemon Athletica Inc. (Canada)

- •Nike, Inc. (United States)

Market Breakdown

- •By Type

- ◦Cotton Sleepwear

- ◦Silk Sleepwear

- ◦Synthetic Sleepwear

- ◦Wool Sleepwear

- ◦Blended Fabrics

- •By Application

- ◦Men

- ◦Women

- ◦Children

- ◦Infants

- ◦Others

- •By End-Use Industry

- ◦Retail Stores

- ◦Online Retailers

- ◦Specialty Stores

- ◦Department Stores

- •By Distribution Channel

- ◦Offline Distribution

- ◦Online Distribution

- ◦Direct Sales

Growth Dynamics

- •The growing consumer inclination towards comfort and wellness has significantly propelled the demand for breathable and skin-friendly sleepwear fabrics such as cotton, which dominate the market. Rising health awareness has also increased interest in hypoallergenic and organic textile options, expanding market reach among sensitive skin consumers.

- •Technological advancements in textile manufacturing, including moisture-wicking and temperature-regulating fabrics, have enhanced product performance and consumer appeal. These innovations enable companies to cater to diverse climates and individual preferences, thus broadening application scope.

- •The surge in e-commerce platforms and digital marketing has dramatically increased accessibility and consumer engagement worldwide. Online retailing allows brands to target niche segments, customize offerings, and respond swiftly to fashion trends, fostering accelerated market growth.

- •Urbanization and rising disposable incomes in emerging economies, particularly in Asia-Pacific and Latin America, have driven the expansion of the sleepwear market. Consumers in these regions are increasingly adopting western lifestyles, fueling demand for premium and branded sleepwear products.

- •Sustainability trends are influencing product development, with manufacturers investing in eco-friendly materials and ethical sourcing. This shift caters to environmentally conscious consumers, presenting a competitive edge and supporting long-term market expansion.

Market Trends

- •The integration of smart textiles and wearable technology into sleepwear is gaining traction, allowing consumers to monitor sleep quality and regulate body temperature, thus enhancing the functional aspect of sleepwear beyond comfort.

- •Minimalist and gender-neutral sleepwear designs are emerging trends, reflecting changing societal norms and consumer preferences for versatile and inclusive apparel options.

- •Collaborations between fashion designers and sleepwear brands are increasing, resulting in limited edition collections that combine style with comfort, attracting fashion-forward consumers and boosting brand visibility.

- •Sustainability remains a core trend, with increased use of organic cotton, bamboo fibers, and recycled materials, supported by certifications that assure consumers of product authenticity and environmental responsibility.

- •The rise of subscription-based sleepwear services offers consumers curated selections delivered regularly, blending convenience with personalized fashion experiences.

Market Opportunities

- •Expanding into emerging markets with tailored sleepwear collections that address regional climate and cultural preferences opens substantial growth avenues, especially in Asia-Pacific and Latin America.

- •Innovations in sustainable and biodegradable materials provide opportunities to capture environmentally conscious consumer segments and comply with tightening global regulations.

- •Leveraging advanced manufacturing technologies such as 3D knitting and seamless garment construction can reduce production costs and enhance product quality, offering competitive advantage.

- •Developing multifunctional sleepwear that combines loungewear and nightwear addresses consumer demand for versatile apparel, broadening market appeal.

- •Strategic partnerships with e-commerce platforms and influencers enable brands to reach wider audiences and foster brand loyalty through targeted marketing campaigns.

Market Challenges

- •Fluctuating raw material prices, particularly cotton and silk, present cost management challenges for manufacturers, impacting product pricing and profitability.

- •Intense competition from low-cost regional manufacturers exerts pricing pressure on established brands, necessitating continuous innovation and differentiation.

- •Stringent regulations regarding chemical use and product safety in textiles require compliance investments, posing barriers for smaller players entering the market.

- •Seasonal demand fluctuations challenge inventory and supply chain management, requiring agile production planning to avoid overstocking or stockouts.

- •Counterfeit products and unregulated online marketplaces undermine brand reputation and dilute market share, necessitating robust intellectual property protections.

Regulatory Framework

- •Between 2019 and 2024, several countries implemented stricter regulations on textile chemical usage, including limits on azo dyes and formaldehyde, to ensure consumer safety and environmental protection, compelling manufacturers to adopt safer alternatives.

- •The European Union’s REACH regulation update in 2022 mandated enhanced compliance for textile imports, affecting global supply chains and necessitating certification and testing protocols.

- •In North America, the Consumer Product Safety Improvement Act (CPSIA) revisions introduced in 2021 tightened flammability standards for sleepwear, increasing compliance costs but improving product safety.

- •Emerging regulations in Asia-Pacific countries focusing on sustainable manufacturing practices and waste reduction have driven industry-wide adoption of eco-friendly processes and materials since 2023.

- •Government incentives promoting organic cotton cultivation and recycled textiles, particularly in Latin America and Europe, have encouraged sustainable sourcing and innovation in sleepwear production.

Market Intelligence

- •15th January 2025, Hanesbrands Inc. launched a new line of sustainable cotton sleepwear made entirely from organic fibers, targeting eco-conscious consumers across North America and Europe. The collection incorporates moisture-wicking technology and is certified by global organic textile standards, aiming to strengthen Hanesbrands' position in the premium eco-friendly segment. This launch aligns with growing market demand for sustainable sleepwear and enhances the company's brand reputation.

- •10th March 2025, Uniqlo introduced innovative silk-based sleepwear incorporating temperature regulation technology, designed to provide comfort across seasons in Asia-Pacific markets. The product integrates nanotechnology to adjust thermal insulation dynamically, offering enhanced sleep quality. This launch marks Uniqlo's strategic focus on combining technology and traditional fabrics to capture luxury and performance-oriented consumer segments.

- •8th February 2025, Victoria's Secret announced a strategic partnership with a leading textile innovation firm to develop biodegradable sleepwear fabrics, aiming to reduce environmental impact and meet sustainability goals. This move is expected to set new industry benchmarks and attract eco-sensitive millennial and Gen Z consumers worldwide.

- •20th April 2025, Amazon.com, Inc. expanded its private label sleepwear portfolio with personalized sizing options and AI-driven design recommendations, enhancing the online shopping experience. This initiative leverages data analytics to optimize fit and style, positioning Amazon competitively in the digital sleepwear retail space.

- •Source: Official company announcements and industry reports

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45.2 Billion |

| Forecast Year Market Size | USD 104.6 Billion |

| CAGR | 8.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.2% |

| Scope of Report | Market is segmented by Type (Cotton Sleepwear, Silk Sleepwear, Synthetic Sleepwear, Wool Sleepwear, Blended Fabrics), Application (Men, Women, Children, Infants, Others), End-Use Industry (Retail Stores, Online Retailers, Specialty Stores, Department Stores), Distribution Channel (Offline Distribution, Online Distribution, Direct Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Hanesbrands Inc. (United States), L Brands, Inc. (United States), Calvin Klein Inc. (United States), Ekouaer (China), Oysho (Spain), Gildan Activewear Inc. (Canada), Jockey International, Inc. (United States), H&M Hennes & Mauritz AB (Sweden), Victoria's Secret (United States), Fruit of the Loom, Inc. (United States), Marks & Spencer Group plc (United Kingdom), Uniqlo Co., Ltd. (Japan), Zara (Spain), Target Corporation (United States), Amazon.com, Inc. (United States), Gap Inc. (United States), Intimissimi (Italy), Decathlon S.A. (France), M&S (United Kingdom), Victoria’s Secret & Co. (United States), Next plc (United Kingdom), Abercrombie & Fitch Co. (United States), ASOS plc (United Kingdom), Lululemon Athletica Inc. (Canada), Nike, Inc. (United States) |

Global Sleepwear Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.