Global Styrene-Acrylonitrile Resin Market - Outlook 2020-2034

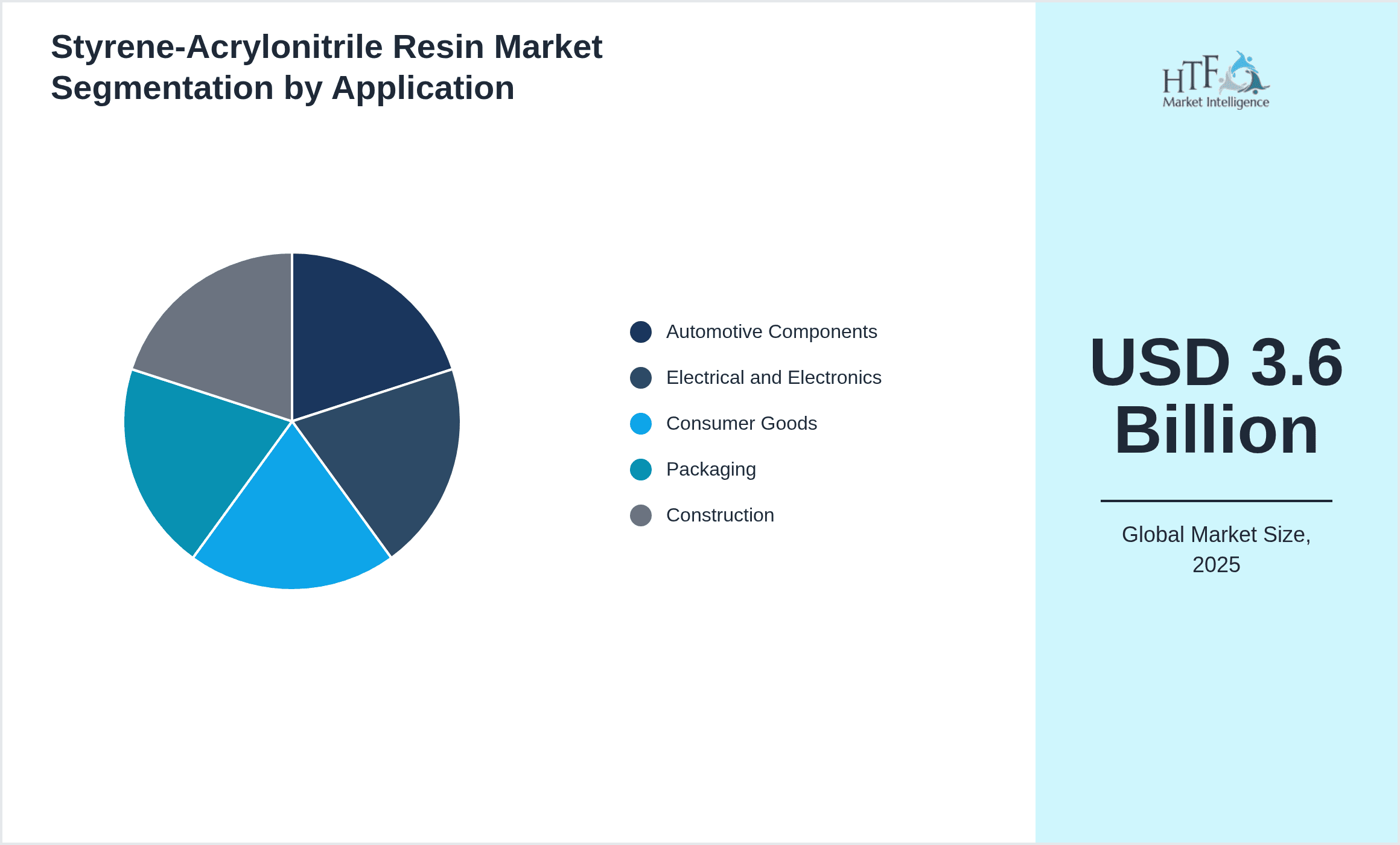

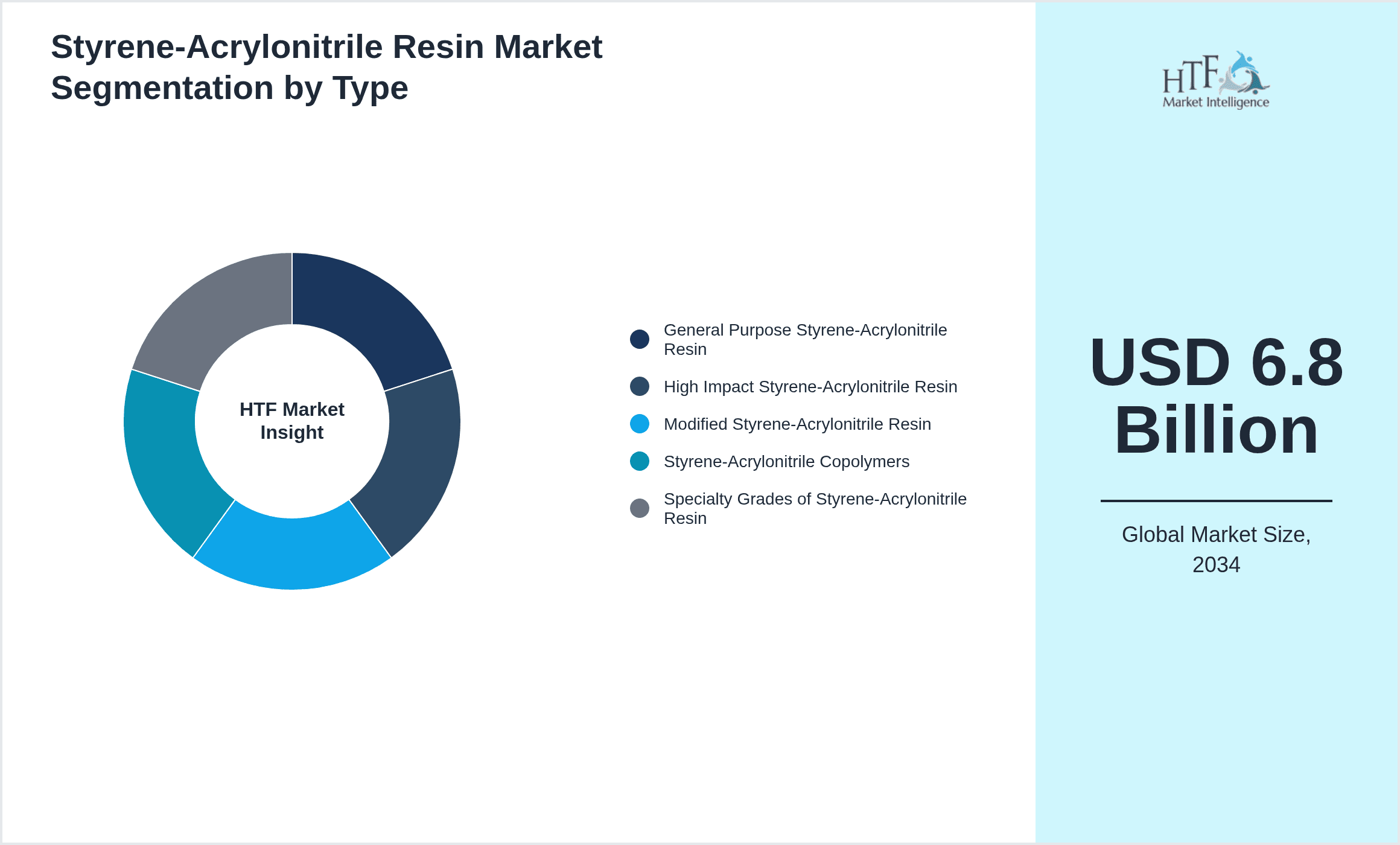

Global Styrene-Acrylonitrile Resin Market is segmented by Product Type (General Purpose Styrene-Acrylonitrile Resin, High Impact Styrene-Acrylonitrile Resin, Modified Styrene-Acrylonitrile Resin, Styrene-Acrylonitrile Copolymers, Specialty Grades of Styrene-Acrylonitrile Resin), Application (Automotive Components, Electrical and Electronics, Consumer Goods, Packaging, Construction), End-Use Industry (Automotive Industry, Electrical & Electronics Industry, Packaging Industry, Construction Industry), Distribution Channel (Direct Sales, Distributors, Online Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

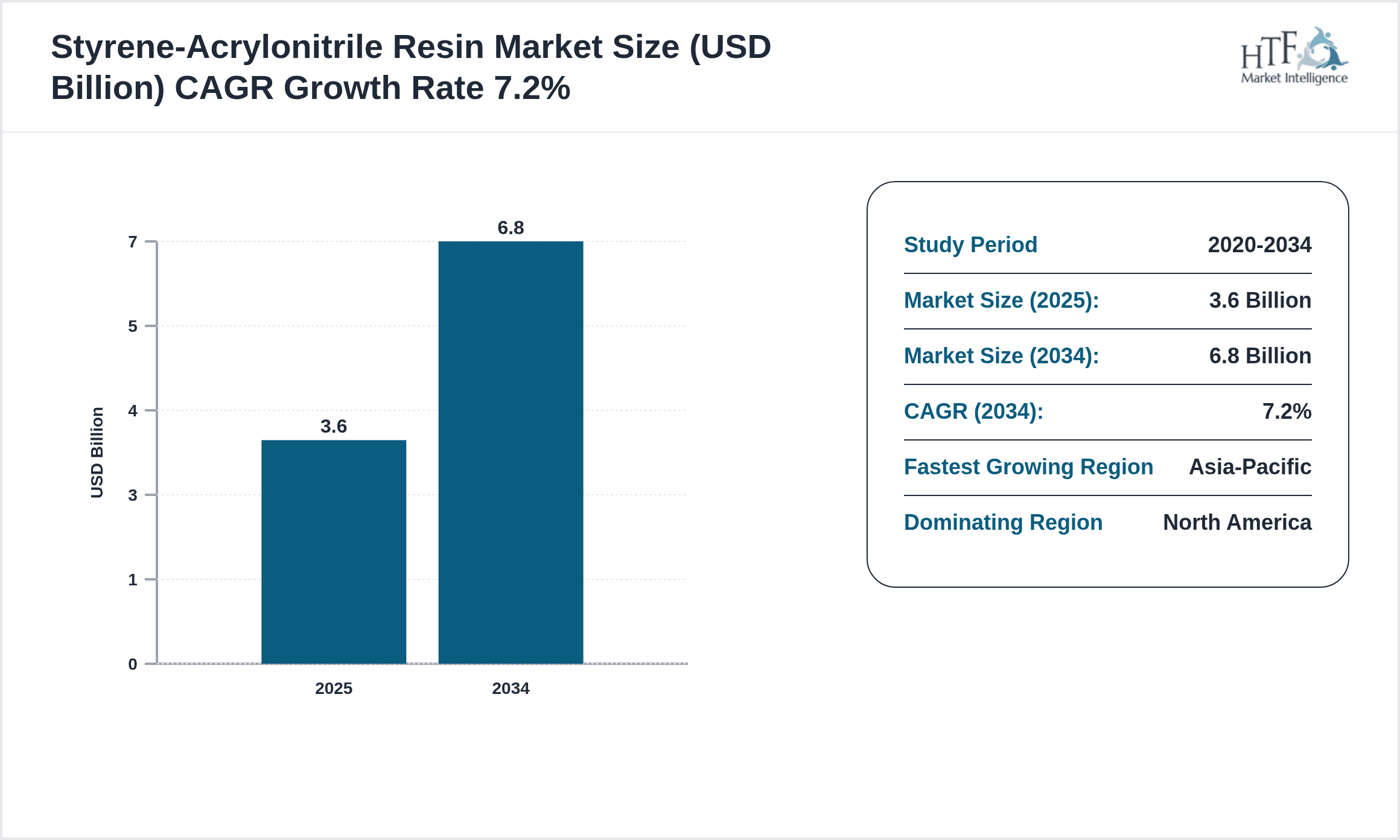

The Global Styrene-Acrylonitrile Resin (SAN) market is a dynamic and rapidly evolving sector characterized by the production and utilization of SAN copolymers which combine styrene and acrylonitrile monomers. These resins exhibit remarkable properties including high chemical resistance, clarity, dimensional stability, and mechanical strength, which make them indispensable in various end-use industries such as automotive, electrical and electronics, packaging, construction, and consumer goods. The SAN resin market is segmented by product type including general purpose SAN, high impact SAN, modified SAN, copolymers, and specialty grades, each tailored to meet specific industry requirements. The applications span automotive components like instrument panels, electrical housings, consumer appliance parts, and packaging materials, reflecting broad market adoption. Geographically, the market sees dominance from North America due to technological advancements and established industrial infrastructure, while Asia-Pacific is emerging as the fastest growing region driven by rapid industrialization and expanding automotive and electronics sectors. Market growth is propelled by increased demand for lightweight and durable materials, stringent regulatory standards, and innovation in polymer modification. The market faces challenges such as raw material price volatility and environmental regulations but holds promising opportunities in emerging economies and specialty resin development. Comprehensive analysis covers market size, competitive landscape, trends, drivers, challenges, regulatory frameworks, and future outlook through 2034, providing stakeholders with actionable insights to navigate the evolving global SAN resin market.

Competitive Landscape

The competitive environment in the Global Styrene-Acrylonitrile Resin market is characterized by intense rivalry among established multinational chemical manufacturers and regional producers. Companies leverage strategies such as product innovation, capacity expansion, strategic partnerships, and mergers and acquisitions to strengthen their market position and cater to evolving customer demands. Innovation in high-performance and modified SAN resins is a key differentiator, enabling players to address niche applications and regulatory requirements. Pricing strategies are influenced by raw material costs and competitive pressure, while companies focus on optimizing their distribution channels to enhance market penetration. The market also experiences competition based on sustainability initiatives, with several players investing in eco-friendly production processes and recyclable resin technologies. Regional competition is notable, especially with Asia-Pacific players expanding capacity to serve the fast-growing markets. Barriers to entry include high capital investment, complex regulatory compliance, and established brand loyalty. Future trends indicate an increased emphasis on technological collaboration and digitalization to optimize supply chains and customer engagement, which will further intensify the competitive landscape.

Key Participants in Styrene-Acrylonitrile Resin Market

- •Trinseo (United States)

- •INEOS Styrolution Group GmbH (Germany)

- •Chi Mei Corporation (Taiwan)

- •LG Chem Ltd. (South Korea)

- •SABIC (Saudi Arabia)

- •Dow Inc. (United States)

- •BASF SE (Germany)

- •Mitsubishi Chemical Holdings Corporation (Japan)

- •LG Polymers (India)

- •Formosa Plastics Corporation (Taiwan)

- •Covestro AG (Germany)

- •Asahi Kasei Corporation (Japan)

- •Sumitomo Chemical Co., Ltd. (Japan)

- •Sabic Innovative Plastics (Saudi Arabia)

- •Westlake Chemical Corporation (United States)

- •Styron LLC (United States)

- •LG Household & Health Care Ltd. (South Korea)

- •Sinopec Corporation (China)

- •Formosa Chemicals & Fibre Corporation (Taiwan)

- •Borealis AG (Austria)

- •INEOS Group Holdings S.A. (Switzerland)

- •ExxonMobil Chemical (United States)

- •Reliance Industries Limited (India)

- •PetroChina Company Limited (China)

- •TotalEnergies SE (France)

Market Breakdown

- •By Product Type

- ◦General Purpose Styrene-Acrylonitrile Resin

- ◦High Impact Styrene-Acrylonitrile Resin

- ◦Modified Styrene-Acrylonitrile Resin

- ◦Styrene-Acrylonitrile Copolymers

- ◦Specialty Grades of Styrene-Acrylonitrile Resin

- •By Application

- ◦Automotive Components

- ◦Electrical and Electronics

- ◦Consumer Goods

- ◦Packaging

- ◦Construction

- •By End-Use Industry

- ◦Automotive Industry

- ◦Electrical & Electronics Industry

- ◦Packaging Industry

- ◦Construction Industry

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Sales

Growth Dynamics

The global Styrene-Acrylonitrile Resin market is driven by increasing demand for lightweight and durable materials across automotive and electrical sectors, which helps manufacturers reduce vehicle weight and improve energy efficiency. Advancements in polymer modification technologies have enabled the development of specialty SAN grades with enhanced impact resistance and thermal stability, expanding application scope. Growing consumer preference for high-performance packaging materials due to their superior clarity and barrier properties is further fueling market expansion. Regulatory initiatives promoting sustainable and recyclable materials are encouraging innovation in eco-friendly SAN resins. Additionally, rapid industrialization in Asia-Pacific is accelerating market growth as manufacturers invest in advanced production facilities to meet rising demand. Furthermore, the adoption of SAN resins in emerging sectors such as medical devices and consumer electronics underpins the growth trajectory. Overall, these factors collectively contribute to robust CAGR and sustained market momentum through the forecast period.

Market Trends

The Styrene-Acrylonitrile Resin market is witnessing a trend towards the development of bio-based and sustainable SAN resins to address environmental concerns and regulatory pressures. Companies are increasingly focusing on enhancing the mechanical and thermal properties of SAN through copolymerization and blending with other polymers to create hybrid materials tailored for specific industry applications. Digitalization of supply chains and adoption of Industry 4.0 technologies are improving operational efficiencies and responsiveness to market demands. Strategic collaborations between resin manufacturers and end-use industries are becoming common to co-develop customized solutions. Additionally, the growing penetration of electric vehicles is driving demand for SAN resins with superior electrical insulation properties. These trends underscore the market's shift towards innovation-driven growth and sustainability-focused product portfolios.

Market Opportunities

Emerging markets in Asia-Pacific and Latin America offer significant growth opportunities for Styrene-Acrylonitrile Resin manufacturers due to expanding automotive and electronics manufacturing bases. The rising demand for lightweight materials in electric vehicles and renewable energy equipment presents avenues for specialty SAN resin development. Increasing consumer awareness about sustainability is driving the adoption of recyclable and bio-based SAN resins, opening new product development pathways. The growing construction sector, particularly in developing regions, requires durable and cost-effective materials, making SAN an attractive option. Furthermore, expanding applications in medical devices and packaging sectors provide untapped markets. Strategic investments in R&D and capacity expansion in these regions can enable companies to capitalize on these opportunities effectively.

Market Challenges

The global Styrene-Acrylonitrile Resin market faces challenges including volatility in raw material prices, particularly styrene and acrylonitrile monomers, which affects production costs and pricing strategies. Stringent environmental regulations related to chemical manufacturing and disposal impose compliance burdens and necessitate investment in cleaner technologies. The presence of alternative polymer materials such as ABS and polycarbonate poses competitive pressure, limiting market share expansion. Additionally, supply chain disruptions and fluctuating demand cycles create operational uncertainties. Achieving product differentiation in a market with several established players requires continuous innovation and significant R&D expenditure. Furthermore, end-user industries' increasing focus on circular economy principles demands recyclable and sustainable material solutions, challenging traditional SAN resin formulations.

Regulatory Framework

Between 2020 and 2025, several key regulations have shaped the Styrene-Acrylonitrile Resin market globally. The European Union’s REACH regulation mandates strict registration, evaluation, authorization, and restriction of chemicals including styrene and acrylonitrile, enforcing rigorous compliance and reporting standards that impact manufacturing processes. In North America, the Toxic Substances Control Act (TSCA) has been updated to enhance oversight of chemical substances, requiring detailed risk assessments and safety data submission from resin producers. Environmental protection policies such as the U.S. EPA’s regulations on volatile organic compounds (VOCs) emissions have driven the adoption of cleaner production techniques. Additionally, regulations promoting sustainability and waste management, including plastic recycling directives in the EU and extended producer responsibility (EPR) schemes in Asia-Pacific, have influenced product development towards recyclable SAN resins. Country-specific mandates in China emphasize pollution control and chemical safety, further tightening market standards. These regulatory frameworks collectively foster market transparency, environmental responsibility, and innovation in safer, sustainable resin products.

Market Intelligence

- •15th January 2025, Trinseo launched a new line of bio-based Styrene-Acrylonitrile Resins designed for enhanced sustainability and performance in automotive and packaging applications. The new product range offers up to 30% bio-content, maintaining mechanical strength and clarity while reducing carbon footprint. This launch targets increasing demand for eco-friendly materials amid tightening environmental regulations globally. Trinseo aims to strengthen its leadership in the specialty resin segment and meet growing customer requirements for sustainable polymers. Source: Official Trinseo Press Release

- •10th March 2025, INEOS Styrolution announced the integration of advanced digital manufacturing technologies at its global SAN production sites to optimize process efficiency and reduce waste. The initiative includes IoT-based monitoring systems and AI-driven analytics to enhance quality control and supply chain responsiveness. This strategic move supports the company’s commitment to operational excellence and sustainability, improving product consistency and reducing production costs. Source: INEOS Styrolution Corporate Website

- •22nd May 2025, BASF SE unveiled a collaborative project with automotive OEMs focusing on developing high-impact modified SAN resins for electric vehicle components. The partnership combines BASF’s polymer expertise with OEM design requirements to create lightweight, durable parts that meet stringent safety standards. This initiative is expected to accelerate market adoption of SAN resins in EV manufacturing, driven by increasing electrification trends worldwide. Source: BASF Annual Report 2025

- •5th August 2025, Mitsubishi Chemical Holdings Corporation completed the acquisition of a regional SAN resin producer in Southeast Asia, expanding its production capacity and strengthening its foothold in emerging markets. This acquisition enables Mitsubishi Chemical to leverage local market knowledge and respond effectively to rising demand in the region. The deal enhances the company’s portfolio with specialty SAN grades tailored for diverse applications. Source: Mitsubishi Chemical Press Release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.6 Billion |

| Forecast Year Market Size | USD 6.8 Billion |

| CAGR | 7.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by Product Type (General Purpose Styrene-Acrylonitrile Resin, High Impact Styrene-Acrylonitrile Resin, Modified Styrene-Acrylonitrile Resin, Styrene-Acrylonitrile Copolymers, Specialty Grades of Styrene-Acrylonitrile Resin), Application (Automotive Components, Electrical and Electronics, Consumer Goods, Packaging, Construction), End-Use Industry (Automotive Industry, Electrical & Electronics Industry, Packaging Industry, Construction Industry), Distribution Channel (Direct Sales, Distributors, Online Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Emerging markets in Asia-Pacific and Latin America offer significant growth opportunities for Styrene-Acrylonitrile Resin manufacturers due to expanding automotive and electronics manufacturing bases. The rising demand for lightweight materials in electric vehicles and renewable energy equipment presents avenues for specialty SAN resin development. Increasing consumer awareness about sustainability is driving the adoption of recyclable and bio-based SAN resins, opening new product development pathways. The growing construction sector, particularly in developing regions, requires durable and cost-effective materials, making SAN an attractive option. Furthermore, expanding applications in medical devices and packaging sectors provide untapped markets. Strategic investments in R&D and capacity expansion in these regions can enable companies to capitalize on these opportunities effectively. |

Global Styrene-Acrylonitrile Resin Market - Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.