Global Supercapacitor Materials Market Size, Growth & Revenue 2025-2034

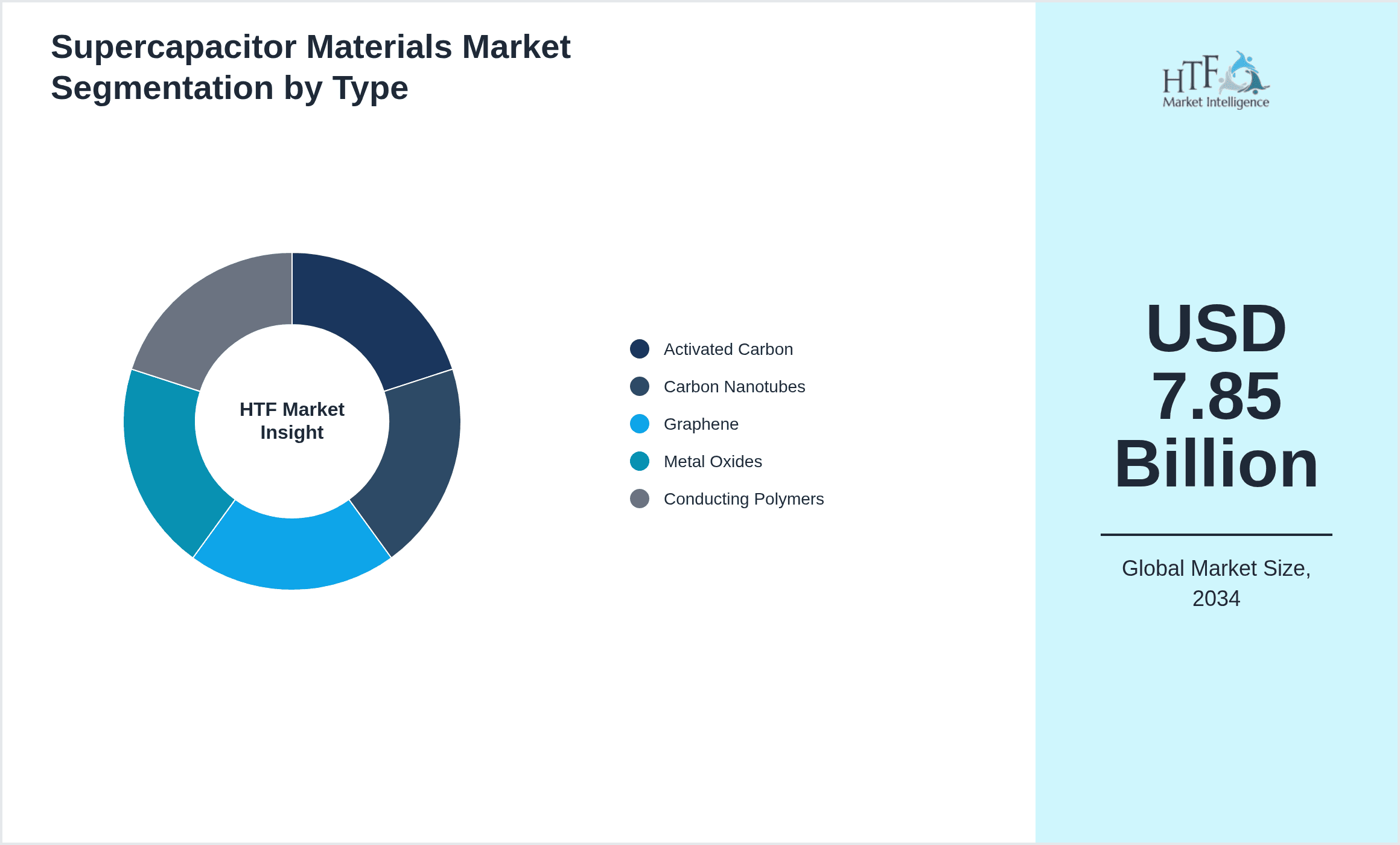

Global Supercapacitor Materials Market is segmented by Product Type (Activated Carbon, Carbon Nanotubes, Graphene, Metal Oxides, Conducting Polymers), Application (Energy Storage, Automotive, Consumer Electronics, Industrial Equipment, Renewable Energy), End-Use Industry (Automotive, Electronics, Energy & Power, Industrial), Distribution Channel (Direct Sales, Distributors, Online Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global supercapacitor materials market is defined by the production and utilization of advanced materials critical to the development of supercapacitors, devices that offer superior power density and longevity compared to traditional batteries. This market includes key material types such as activated carbon, carbon nanotubes, graphene, metal oxides, and conducting polymers, which are essential for enhancing supercapacitor performance. The applications span energy storage systems, automotive sectors including electric and hybrid vehicles, consumer electronics, industrial machinery, and renewable energy infrastructures. The value chain integrates raw material sourcing, cutting-edge research, manufacturing, and final integration into devices, reflecting the industry's interdisciplinary nature. Increasing demand for rapid charging energy storage solutions, coupled with the global shift towards sustainable and renewable energy technologies, propels market expansion. Technological innovations in nanomaterials and conductive polymers have significantly improved supercapacitor efficiency and reduced costs. Regional market dynamics vary, with North America leading in technological adoption, Asia-Pacific exhibiting the fastest growth due to industrialization and electrification trends, and Europe focusing on regulatory compliance and green energy initiatives. These factors collectively establish the supercapacitor materials market as a critical component of the evolving global energy landscape.

- •Market highlights include a base year market size of USD 2.45 Billion in 2025, forecasting robust growth to USD 7.85 Billion by 2034, reflecting a CAGR of 13.1%. The year-on-year growth rate stands at approximately 12.5%, fueled by rising demand from automotive and renewable energy sectors. Dominance by North America is underpinned by advanced R&D infrastructure and significant investments in electric vehicle technologies. Asia-Pacific’s rapid industrial expansion and government incentives contribute to its status as the fastest-growing region. Activated carbon remains the leading product type due to its cost-effectiveness and widespread availability, while graphene is poised as the fastest-growing material, driven by superior conductivity and increased research focus.

- •The value proposition for stakeholders lies in the strategic importance of supercapacitor materials in achieving energy efficiency, reducing carbon emissions, and enabling next-generation electronic and automotive technologies. Manufacturers benefit from expanding application domains and technological advancements, while end-users gain from enhanced device performance and sustainability. This market supports critical infrastructure development, including grid stabilization and electric mobility, positioning it as a vital contributor to the global green energy transition.

Competitive Landscape

The global supercapacitor materials market features a competitive environment characterized by rapid innovation, intense R&D investments, and strategic collaborations. Market players focus on developing proprietary materials with enhanced electrochemical properties to gain differentiation. Competitive strategies include joint ventures, mergers and acquisitions, and partnerships aimed at expanding technological capabilities and geographic reach. Pricing strategies vary with material type and purity, influencing adoption across different applications. Distribution channels are diversified, including direct sales to manufacturers and through intermediaries, ensuring broad market penetration. Market entry barriers exist due to high technical expertise requirements and significant capital investments. Regional competition is influenced by the availability of raw materials and manufacturing infrastructure, with Asia-Pacific emerging as a key innovation hub. Future trends suggest increased integration of AI and machine learning in material development, further intensifying competition and accelerating market evolution.

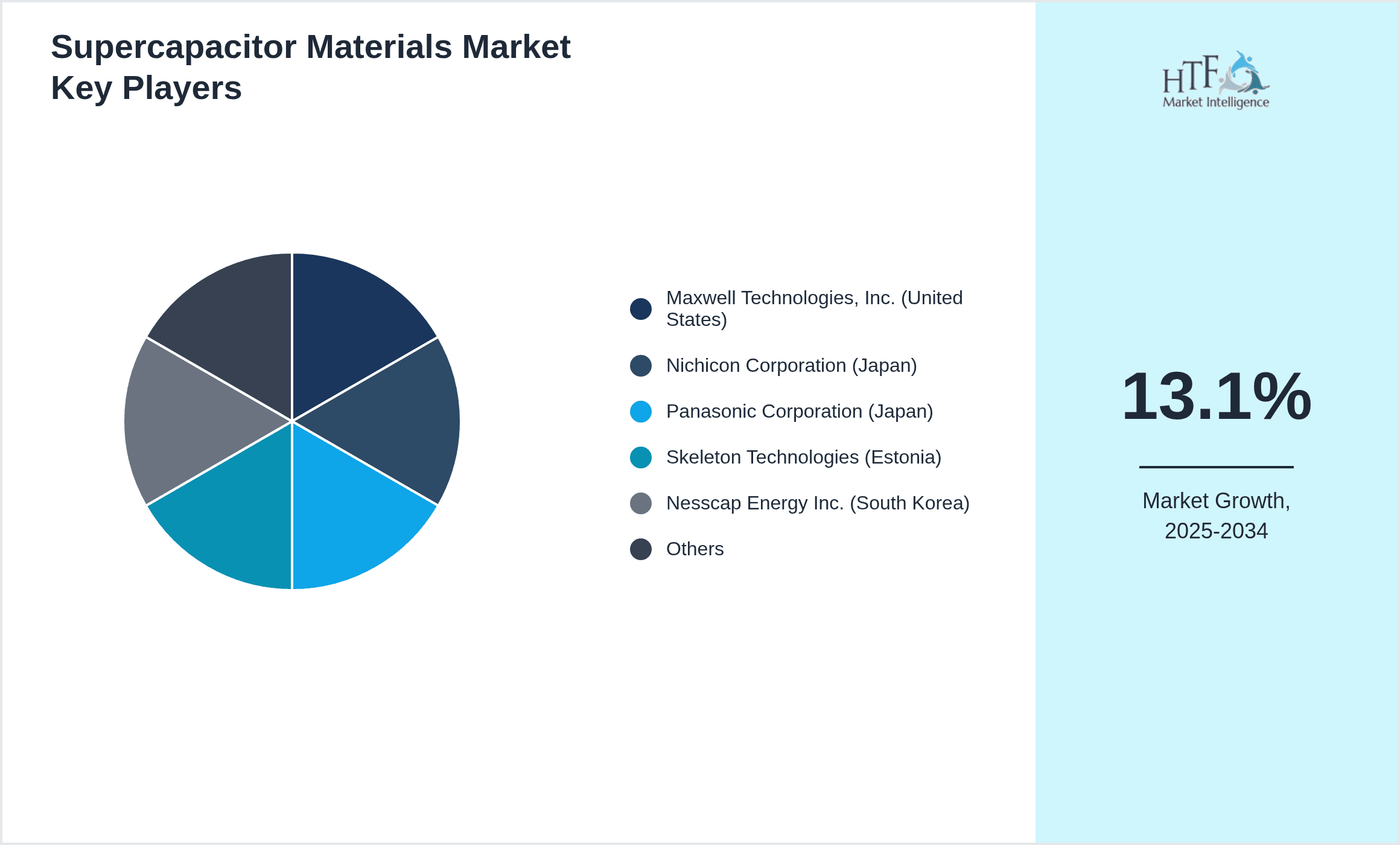

Leading Companies in Supercapacitor Materials Market

- •Maxwell Technologies, Inc. (United States)

- •Nichicon Corporation (Japan)

- •Panasonic Corporation (Japan)

- •Skeleton Technologies (Estonia)

- •Nesscap Energy Inc. (South Korea)

- •LS Mtron Ltd. (South Korea)

- •Furukawa Electric Co., Ltd. (Japan)

- •Ioxus, Inc. (United States)

- •Elna Co., Ltd. (Japan)

- •Jiangsu Topband Battery Co., Ltd. (China)

- •Seiko Instruments Inc. (Japan)

- •Panax Etec (South Korea)

- •Maxwell Technologies (United States)

- •Active Materials Corporation (United States)

- •Cap-XX Limited (Australia)

- •Avogy, Inc. (United States)

- •LSIS Co., Ltd. (South Korea)

- •Eaton Corporation (United States)

- •Cymbet Corporation (United States)

- •Tadiran Batteries GmbH (Germany)

- •Murata Manufacturing Co., Ltd. (Japan)

- •Elithion, Inc. (United States)

- •LS Battery (South Korea)

- •KEMET Corporation (United States)

- •Henan Yuhua Carbon Co., Ltd. (China)

Market Breakdown

- •By Product Type

- ◦Activated Carbon

- ◦Carbon Nanotubes

- ◦Graphene

- ◦Metal Oxides

- ◦Conducting Polymers

- •By Application

- ◦Energy Storage

- ◦Automotive

- ◦Consumer Electronics

- ◦Industrial Equipment

- ◦Renewable Energy

- •By End-Use Industry

- ◦Automotive

- ◦Electronics

- ◦Energy & Power

- ◦Industrial

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Sales

Growth Dynamics

- •Rising demand for electric vehicles accelerates the need for efficient supercapacitor materials that deliver rapid charging and high power density, with companies investing heavily in R&D to improve material performance and durability.

- •Advancements in nanotechnology and material science, particularly in graphene and carbon nanotubes, enable enhanced conductivity and capacitance, driving innovation and expanding application areas for supercapacitors.

- •Government policies promoting renewable energy integration and grid stability increase adoption of supercapacitors in energy storage systems, thus expanding the market for advanced materials.

- •Growing consumer electronics market demands miniaturized, high-performance energy storage solutions, which fuels the development and commercialization of novel supercapacitor materials.

- •Investment in sustainable and eco-friendly materials encourages the shift towards conducting polymers and metal oxides, which offer environmental benefits alongside technical advantages.

- •Strategic collaborations between material suppliers and device manufacturers accelerate market penetration and foster innovation, enhancing competitive advantages for early adopters.

- •Increasing industrial automation and demand for uninterrupted power supplies boost the need for reliable supercapacitor materials across diverse sectors such as manufacturing and telecommunications.

Market Trends

- •Integration of graphene-based materials in supercapacitors is gaining traction due to their exceptional electrical and mechanical properties, leading to enhanced energy density and lifecycle improvements.

- •Hybrid supercapacitors combining batteries and capacitors are emerging, requiring innovative materials that can optimize energy and power balance for diverse applications.

- •Sustainability trends drive research into bio-derived and eco-friendly supercapacitor materials, aligning with global environmental policies and consumer preferences.

- •Digitalization and IoT proliferation increase demand for compact, efficient energy storage materials to support connected devices and smart systems.

- •Collaborative innovation ecosystems involving academia, industry, and government agencies accelerate material development and commercialization cycles in the supercapacitor sector.

- •Customization of supercapacitor materials for specific end-use applications, such as automotive or industrial machinery, enhances product differentiation and market segmentation.

- •Emerging markets in Asia-Pacific are adopting advanced supercapacitor technologies rapidly, driven by infrastructural modernization and electrification initiatives.

Market Opportunities

- •Expanding electric vehicle market presents significant opportunities for supercapacitor materials that improve charge times and vehicle efficiency, with potential for large-scale adoption globally.

- •Untapped applications in renewable energy storage systems offer growth prospects for materials that can enhance grid stability and energy management capabilities.

- •Investment in nanomaterial research and scalable manufacturing processes can unlock new material innovations, reducing costs and improving accessibility for diverse markets.

- •Geographical expansion into emerging economies with growing industrialization and energy infrastructure development provides avenues for market growth.

- •Collaborations and strategic partnerships between material producers and technology firms can accelerate product development and market penetration.

- •Development of customized supercapacitor materials for specific industry needs, such as aerospace or healthcare, can create niche market segments with high margins.

- •Government incentives and funding for green technologies boost the adoption of advanced supercapacitor materials, supporting sustainability goals and market expansion.

Market Challenges

- •High production costs of advanced materials like graphene and carbon nanotubes limit widespread adoption, particularly in price-sensitive markets and applications.

- •Technical challenges in scaling up manufacturing processes while maintaining material quality and consistency pose significant barriers to market growth.

- •Competition from alternative energy storage technologies, such as lithium-ion batteries, creates market pressure and necessitates continuous innovation in supercapacitor materials.

- •Regulatory uncertainties and varying standards across regions complicate market entry and compliance efforts for manufacturers and suppliers.

- •Limited availability of raw materials and supply chain disruptions impact production schedules and cost structures adversely.

- •Environmental concerns related to material disposal and recycling require development of sustainable and circular economy approaches within the industry.

- •Talent shortage in specialized material science and nanotechnology fields restrains the pace of innovation and commercialization.

Regulatory Framework

- •The European Union’s Restriction of Hazardous Substances Directive (RoHS) enforced between 2020 and 2025 mandates strict limits on hazardous materials in supercapacitor production, driving manufacturers to adopt safer substances and comply with environmental standards.

- •The United States Environmental Protection Agency’s (EPA) Clean Energy Incentives Program launched in 2023 incentivizes the use of sustainable energy storage materials, impacting market dynamics by encouraging green innovations in supercapacitor materials.

- •China’s National Development and Reform Commission introduced regulations in 2021 focused on promoting clean energy technologies, including guidelines for material sourcing and environmental compliance in supercapacitor manufacturing.

- •Japan’s Ministry of Economy, Trade and Industry (METI) established operational guidelines in 2024 to standardize performance and safety requirements for supercapacitor materials, enhancing market transparency and consumer trust.

- •The International Electrotechnical Commission (IEC) updated standards in 2022 for supercapacitor testing and certification, facilitating global harmonization and enabling smoother cross-border trade and adoption.

Market Intelligence

- •15th January 2025, Maxwell Technologies, Inc. announced the launch of a new graphene-enhanced supercapacitor material designed to significantly increase energy density and reduce charge times. This innovation targets electric vehicle manufacturers and renewable energy storage providers. The new material incorporates proprietary synthesis techniques that improve conductivity and lifecycle stability, positioning Maxwell as a market leader in advanced supercapacitor materials. Strategic partnerships are planned to accelerate commercialization and scale manufacturing capacity. Source: Official Maxwell Technologies Press Release

- •30th March 2025, Skeleton Technologies introduced an innovative carbon nanotube-based material with superior capacitance and thermal stability. The product aims to serve high-performance automotive applications and industrial equipment requiring reliable energy storage under extreme conditions. This launch reflects the company's commitment to pushing the boundaries of material science to meet evolving market demands. Collaborative research agreements with European automotive OEMs were also announced to integrate this technology into next-generation electric vehicles. Source: Skeleton Technologies Corporate Website

- •18th June 2025, Panasonic Corporation revealed a strategic partnership with a leading graphene manufacturer to develop scalable production methods for graphene-based supercapacitor materials. This collaboration focuses on reducing costs and enhancing material quality for consumer electronics and renewable energy applications. The initiative aligns with Panasonic’s sustainability goals and aims to capture a larger share of the growing global market. Joint R&D efforts are expected to yield commercial products by late 2026. Source: Panasonic Newsroom

- •10th September 2025, Nesscap Energy Inc. completed the acquisition of a specialty conducting polymers manufacturer to strengthen its material portfolio and enhance supercapacitor performance. This acquisition expands Nesscap’s technological capabilities and market reach, particularly in Asia-Pacific and North America. The combined entity will leverage synergies in R&D and production to accelerate innovation cycles and reduce time-to-market for new materials. This move exemplifies the ongoing consolidation trend in the supercapacitor materials sector. Source: Nesscap Energy Official Announcement

- •Source: Official press releases, company websites, industry publications

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 2.45 Billion |

| Forecast Year Market Size | USD 7.85 Billion |

| CAGR | 13.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.5% |

| Scope of Report | Market is segmented by Product Type (Activated Carbon, Carbon Nanotubes, Graphene, Metal Oxides, Conducting Polymers), Application (Energy Storage, Automotive, Consumer Electronics, Industrial Equipment, Renewable Energy), End-Use Industry (Automotive, Electronics, Energy & Power, Industrial), Distribution Channel (Direct Sales, Distributors, Online Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Maxwell Technologies, Inc. (United States), Nichicon Corporation (Japan), Panasonic Corporation (Japan), Skeleton Technologies (Estonia), Nesscap Energy Inc. (South Korea), LS Mtron Ltd. (South Korea), Furukawa Electric Co., Ltd. (Japan), Ioxus, Inc. (United States), Elna Co., Ltd. (Japan), Jiangsu Topband Battery Co., Ltd. (China), Seiko Instruments Inc. (Japan), Panax Etec (South Korea), Maxwell Technologies (United States), Active Materials Corporation (United States), Cap-XX Limited (Australia), Avogy, Inc. (United States), LSIS Co., Ltd. (South Korea), Eaton Corporation (United States), Cymbet Corporation (United States), Tadiran Batteries GmbH (Germany), Murata Manufacturing Co., Ltd. (Japan), Elithion, Inc. (United States), LS Battery (South Korea), KEMET Corporation (United States), Henan Yuhua Carbon Co., Ltd. (China) |

Global Supercapacitor Materials Market Size, Growth & Revenue 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.