Global Multilayer PCB Market Size, Growth & Revenue 2025-2034

Global Multilayer PCB Market is segmented by Product Type (Rigid Multilayer PCB, Flexible Multilayer PCB, Rigid-Flex Multilayer PCB, High-Density Interconnect (HDI) PCB, Other Specialty Multilayer PCBs), Application (Consumer Electronics, Automotive, Telecommunications, Industrial Equipment, Healthcare & Medical Devices), End-Use Industry (Electronics Manufacturing, Automotive Industry, Telecom Industry, Healthcare Sector), Distribution Channel (Direct Sales, Authorized Distributors, Online Sales Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

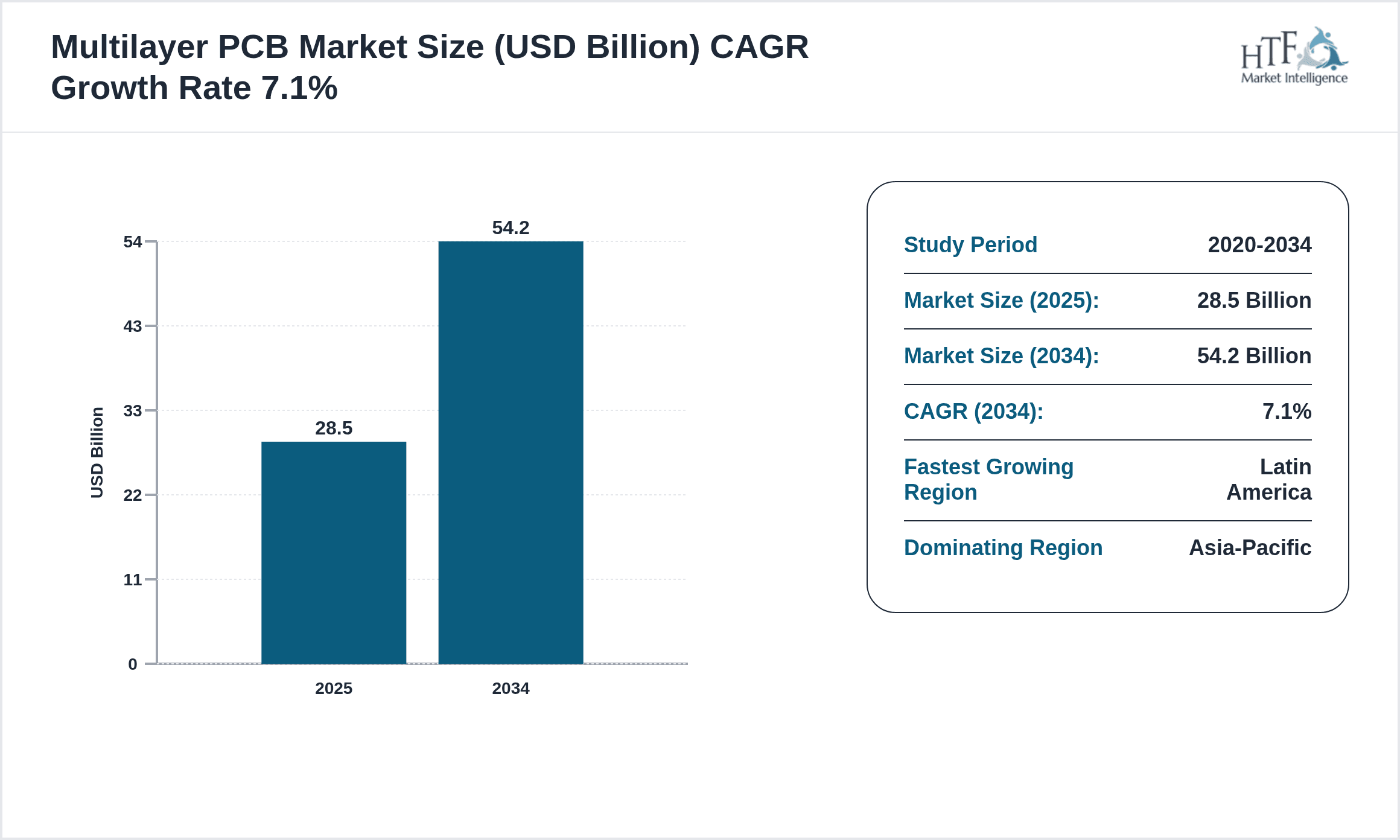

- •The global multilayer PCB market represents a crucial segment in the electronics manufacturing industry, focusing on PCBs with three or more conductive layers to support increasingly complex electronic designs. These multilayer PCBs are integral to miniaturizing devices while enhancing performance, enabling applications across consumer electronics, automotive, telecommunications, industrial equipment, and healthcare sectors. The market's evolution is driven by technological advancements such as HDI and rigid-flex PCBs, which allow greater circuit density and improved electrical performance. Increasing adoption of electric vehicles, 5G telecommunications infrastructure, and IoT devices is fueling demand for sophisticated multilayer PCBs. The market also navigates challenges including high manufacturing costs, technical complexity, and supply chain vulnerabilities. Strategic investments in research and development, coupled with expanding manufacturing capabilities in emerging regions, are anticipated to sustain market growth through 2034. Overall, the market outlook remains positive with a CAGR of 7.1%, reflecting steady expansion supported by innovation and diversification of applications worldwide.

- •Key market highlights include a base market size of USD 28.5 Billion in 2025 expanding to USD 54.2 Billion by 2034, driven by rising demand in Asia-Pacific, which dominates global consumption and production. Latin America is identified as the fastest-growing region, fueled by increasing industrialization and electronics manufacturing. Rigid multilayer PCBs remain the leading product type due to their broad applicability, while rigid-flex multilayer PCBs are witnessing the fastest growth owing to their flexibility and multifunctional use cases. The market’s compound annual growth rate (CAGR) is projected at 7.1%, with a year-on-year growth rate closely aligned at 7.0%. These growth metrics underscore the increasing significance of multilayer PCBs in powering next-generation electronic devices and infrastructure globally.

- •The multilayer PCB market holds strategic importance for stakeholders across industries, providing essential components for high-performance electronics that underpin digital transformation. For manufacturers, the market offers opportunities to leverage advanced materials and manufacturing techniques to meet complex design requirements. For end-users in automotive, telecommunications, and healthcare, multilayer PCBs enable enhanced functionality, reliability, and miniaturization critical to product innovation. Investors and policymakers recognize the market’s role in technological ecosystems, supporting job creation and regional economic growth. As electronics demand escalates globally, multilayer PCBs will continue to be a pivotal technology, driving integration and efficiency across multiple sectors.

Competitive Landscape

The global multilayer PCB market exhibits a highly competitive environment characterized by rapid technological innovation, strategic partnerships, and continuous capacity expansion. Market players focus on differentiating through advanced manufacturing processes such as HDI and rigid-flex technologies, enabling higher layer counts and finer circuit designs. Competitive strategies include mergers and acquisitions to consolidate market presence and expand geographic reach, along with investments in R&D to develop eco-friendly materials and improve production efficiency. Pricing strategies are influenced by raw material costs and supply chain dynamics, with manufacturers optimizing cost structures to maintain profitability. Distribution channels leverage both direct sales and authorized distributors to maximize market penetration. Regional competition varies, with Asia-Pacific dominating production capabilities while Europe and North America emphasize high-value, specialized PCB solutions. Future trends suggest increased collaboration between technology providers and OEMs to accelerate innovation, alongside a focus on sustainability and supply chain resilience shaping the competitive landscape.

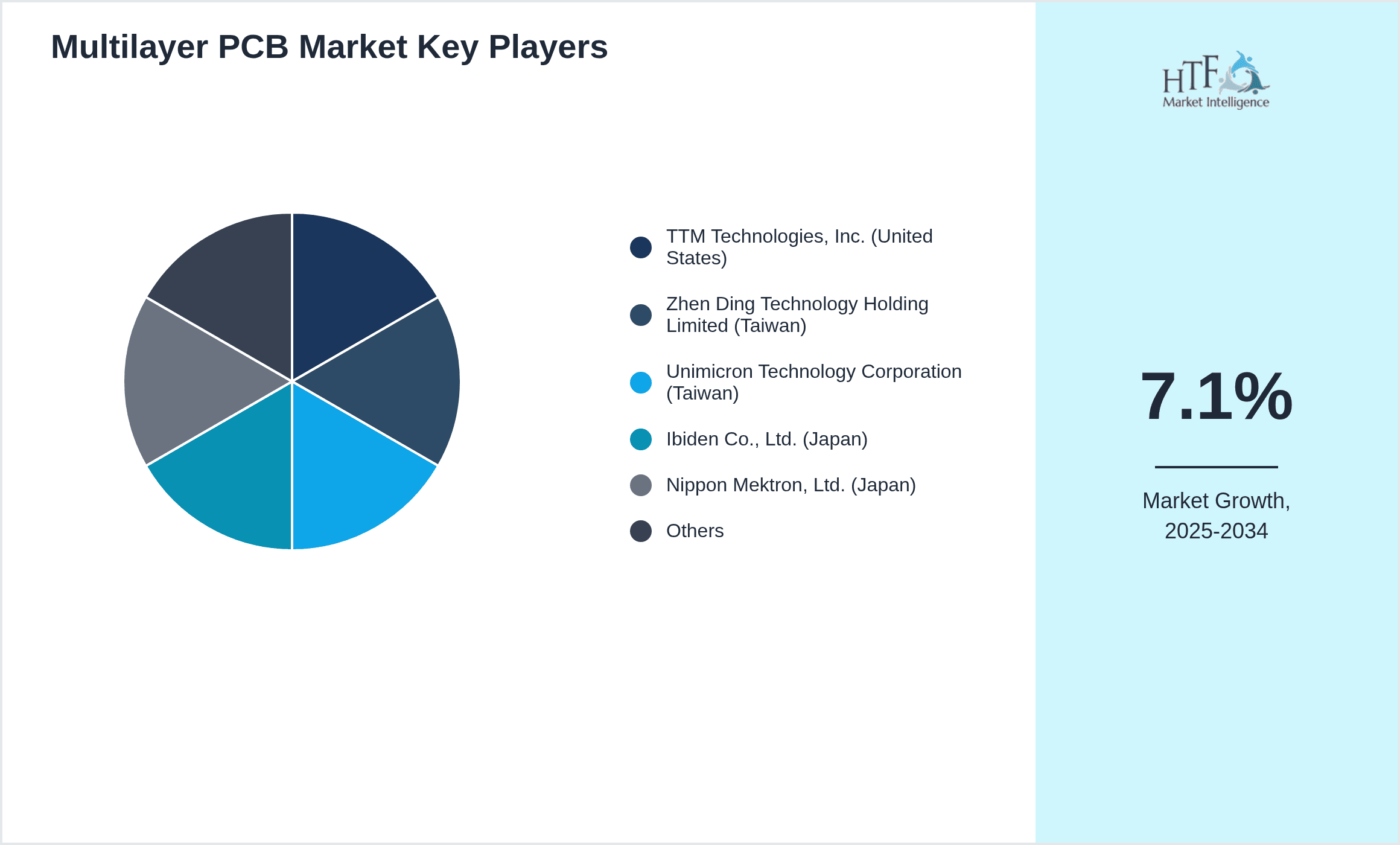

Prominent Players in Multilayer PCB Market

- •TTM Technologies, Inc. (United States)

- •Zhen Ding Technology Holding Limited (Taiwan)

- •Unimicron Technology Corporation (Taiwan)

- •Ibiden Co., Ltd. (Japan)

- •Nippon Mektron, Ltd. (Japan)

- •Samsung Electro-Mechanics Co., Ltd. (South Korea)

- •Compeq Manufacturing Co., Ltd. (Taiwan)

- •Tripod Technology Corporation (Taiwan)

- •Shennan Circuits Company Limited (China)

- •Meiko Electronics Co., Ltd. (Japan)

- •AT&S Austria Technologie & Systemtechnik AG (Austria)

- •Unitech Printed Circuit Board Corporation (Taiwan)

- •Tripod Technology Corporation (Taiwan)

- •TTM Technologies, Inc. (United States)

- •Kinsus Interconnect Technology Corp. (Taiwan)

- •Flex Ltd. (United States)

- •Nanya PCB Corporation (Taiwan)

- •Daeduck GDS Co., Ltd. (South Korea)

- •Viasystems Group, Inc. (United States)

- •Shiyi Technology Co., Ltd. (China)

- •Young Poong Group (South Korea)

- •HannStar Board Corporation (Taiwan)

- •Elite Material Co., Ltd. (Taiwan)

- •Flexium Interconnect, Inc. (Taiwan)

- •Multek Corporation (United States)

Market Breakdown

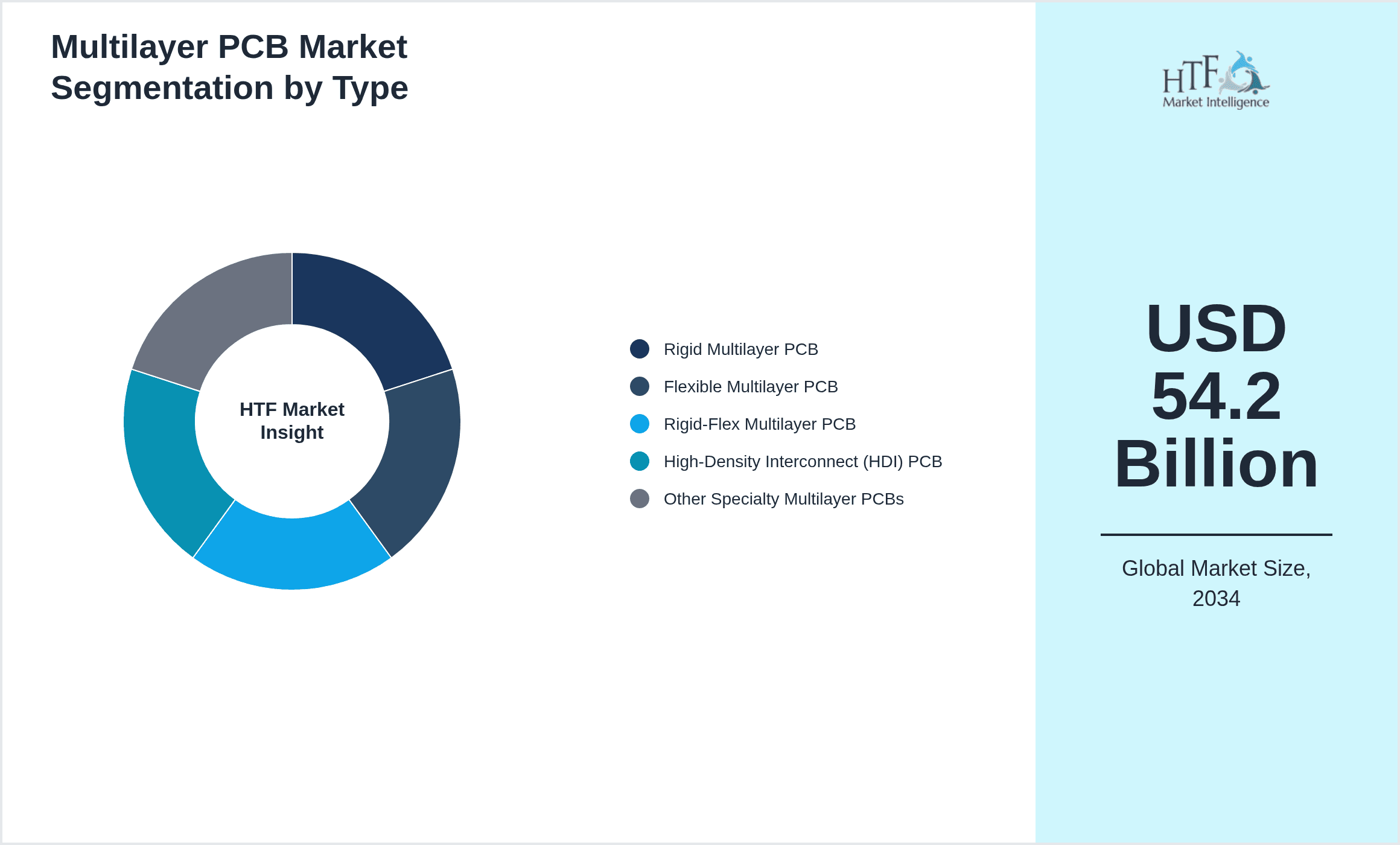

- •By Product Type

- ◦Rigid Multilayer PCB

- ◦Flexible Multilayer PCB

- ◦Rigid-Flex Multilayer PCB

- ◦High-Density Interconnect (HDI) PCB

- ◦Other Specialty Multilayer PCBs

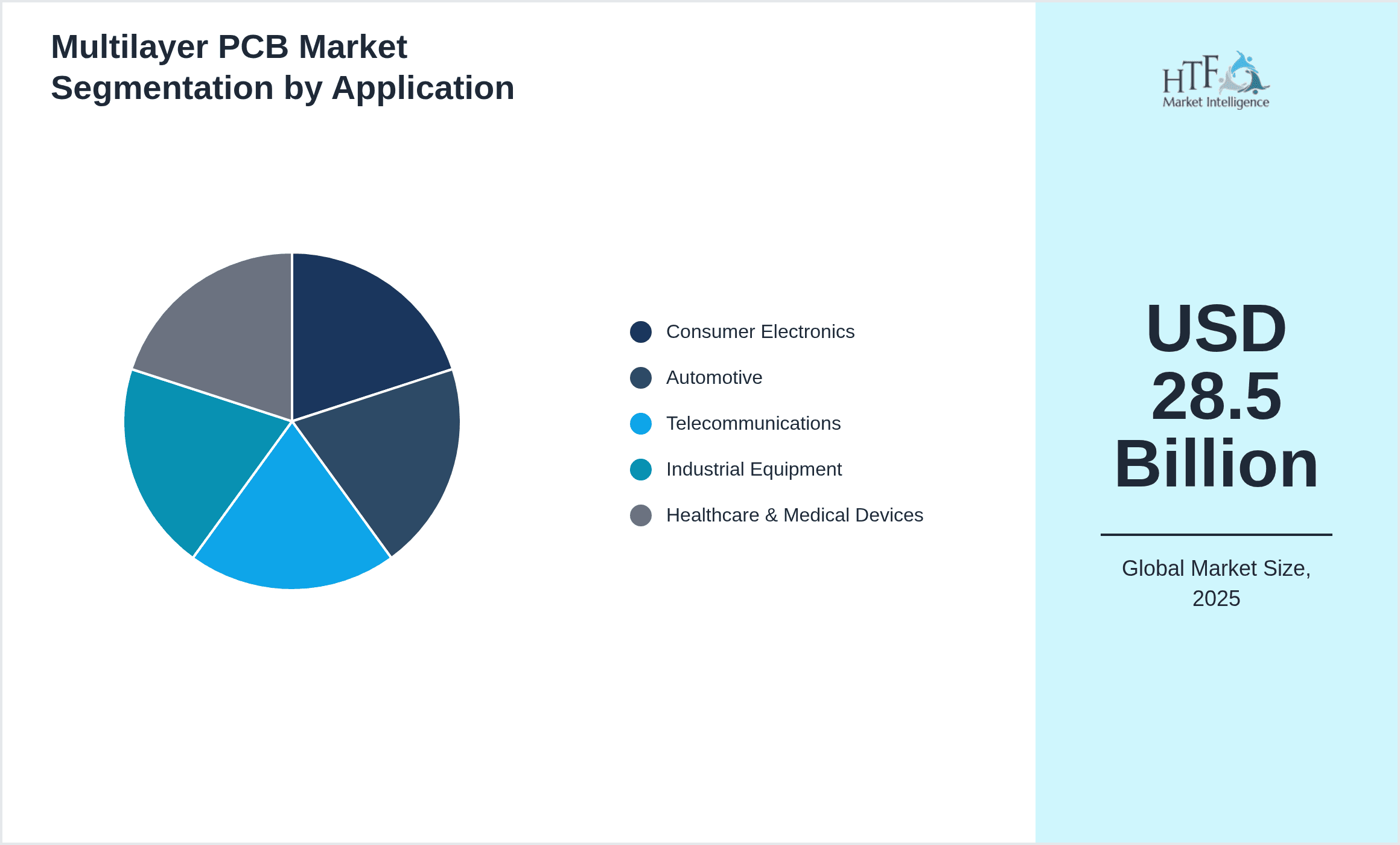

- •By Application

- ◦Consumer Electronics

- ◦Automotive

- ◦Telecommunications

- ◦Industrial Equipment

- ◦Healthcare & Medical Devices

- •By End-Use Industry

- ◦Electronics Manufacturing

- ◦Automotive Industry

- ◦Telecom Industry

- ◦Healthcare Sector

- •By Distribution Channel

- ◦Direct Sales

- ◦Authorized Distributors

- ◦Online Sales Platforms

Growth Dynamics

The global multilayer PCB market is propelled by escalating demand for advanced electronics requiring complex circuitry and higher performance. Automotive electrification and 5G telecommunication infrastructure investments are major contributors, driving the need for multilayer PCBs capable of supporting greater signal integrity and miniaturization. The rise of IoT devices and wearable technology further accelerates market growth by necessitating compact, flexible PCBs. Additionally, advancements in manufacturing technologies such as laser drilling and HDI enable higher layer counts and finer circuit designs, expanding application possibilities. Economic development in emerging markets and growing consumer electronics adoption are sustaining demand, while strategic collaborations and innovations among key players enhance product offerings and market reach. These factors collectively underpin a robust growth trajectory through the forecast period.

Market Trends

A significant trend in the multilayer PCB market is the increased adoption of rigid-flex and HDI PCBs driven by the need for lightweight, compact, and high-performance solutions in sectors like aerospace and medical devices. Sustainability initiatives are prompting manufacturers to develop eco-friendly materials and reduce hazardous substances in PCB fabrication. The integration of automation and Industry 4.0 technologies in PCB manufacturing is enhancing production efficiency and quality control. Moreover, the shift toward electric vehicles has intensified demand for PCBs with high thermal management capabilities. Collaborative R&D efforts between PCB producers and electronics OEMs are fostering innovation in materials and design, enabling customized solutions tailored to complex electronic applications.

Market Opportunities

Emerging markets present significant growth opportunities for multilayer PCB manufacturers, particularly in Latin America and the Middle East & Africa, where industrialization and electronics adoption are accelerating. The expanding electric vehicle market offers avenues for specialized multilayer PCBs with enhanced heat dissipation and durability. Adoption of multilayer PCBs in healthcare for advanced diagnostic and wearable devices is another promising segment. Technological advancements enabling thinner, lighter, and more flexible PCBs open new application fields in consumer electronics and aerospace. Additionally, strategic investments in local manufacturing facilities and supply chain diversification can capitalize on rising regional demand and mitigate geopolitical risks, enhancing market penetration and resilience.

Market Challenges

The multilayer PCB market faces challenges including high manufacturing complexity that requires precision engineering and expensive equipment, limiting entry for new players. Volatility in raw material prices, especially copper and specialty laminates, affects cost structures and profitability. Supply chain disruptions, exacerbated by global geopolitical tensions and logistics constraints, pose risks to timely delivery. Environmental regulations and the need for sustainable materials impose additional compliance costs. Furthermore, intense competition leads to pricing pressure, challenging margins for manufacturers. The shortage of skilled labor and technical expertise in advanced PCB fabrication also hinders capacity expansion. Addressing these challenges requires continuous innovation, supply chain optimization, and regulatory alignment.

Regulatory Framework

Between 2020 and 2025, several key regulations shaped the multilayer PCB market globally, focusing on environmental compliance, safety standards, and trade policies. The Restriction of Hazardous Substances Directive (RoHS) enforced stringent limits on hazardous materials such as lead and mercury, compelling manufacturers to adopt eco-friendly alternatives and revise production processes. The Waste Electrical and Electronic Equipment (WEEE) Directive mandated responsible disposal and recycling, impacting PCB lifecycle management. In North America and Europe, regulations around chemical handling and worker safety were enhanced to reduce occupational hazards in PCB manufacturing. Trade tariffs and export controls introduced in this period affected cross-border supply chains and sourcing strategies. Governments also incentivized investments in local manufacturing to boost resilience and technological capability. Compliance with these regulations ensures sustainable growth and market access across global regions, necessitating ongoing monitoring and adaptation by industry stakeholders.

Market Intelligence

- •15th January 2025, TTM Technologies, Inc. announced the launch of a new series of high-density multilayer rigid-flex PCBs designed for next-generation 5G infrastructure equipment. These PCBs feature enhanced thermal management and signal integrity capabilities, targeting telecommunications OEMs seeking to improve network performance and reliability. The product launch aligns with increasing global deployment of 5G networks and rising demand for compact, high-performance PCBs. TTM's strategic expansion in Asia-Pacific production facilities aims to meet escalating regional demand. This initiative is expected to strengthen the company's market position and support customer innovation efforts. Source: Official TTM Technologies Press Release

- •10th March 2025, Unimicron Technology Corporation introduced advanced eco-friendly multilayer PCB materials compliant with the latest global environmental standards. The new materials reduce hazardous substance content while maintaining excellent electrical performance and mechanical strength. This innovation supports manufacturers' sustainability goals and responds to tightening regulations worldwide. Unimicron's collaboration with leading electronics OEMs aims to accelerate adoption of green PCBs across consumer electronics and automotive sectors. The initiative enhances Unimicron's competitive edge by addressing market demand for environmentally responsible products. Source: Unimicron Corporate Website

- •22nd May 2025, Zhen Ding Technology Holding Limited announced a strategic partnership with a major electric vehicle manufacturer to develop customized multilayer PCBs optimized for battery management systems. This collaboration focuses on integrating thermal management and high-reliability features critical for EV performance and safety. The partnership underscores the growing importance of multilayer PCBs in automotive electrification and promotes joint innovation in design and manufacturing. Zhen Ding's investment in cutting-edge production lines supports scaling to meet automotive sector requirements. The move strengthens market positioning within the EV supply chain and aligns with global sustainability trends. Source: Industry Publication

- •5th August 2025, Ibiden Co., Ltd. completed the acquisition of a European rigid-flex PCB manufacturer, expanding its footprint in the high-growth healthcare and aerospace markets. The acquisition enhances Ibiden's technological capabilities and diversifies its product portfolio with specialized high-reliability PCB solutions. This strategic move aims to leverage synergies in R&D and production efficiency, accelerating innovation and market penetration in Europe and North America. The consolidation reflects ongoing industry trends toward vertical integration and global expansion to meet complex customer demands. The acquisition is expected to drive revenue growth and operational scalability over the forecast horizon. Source: Ibiden Official Announcement

Regional Outlook

The Asia-Pacific currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Latin America is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 28.5 Billion |

| Forecast Year Market Size | USD 54.2 Billion |

| CAGR | 7.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by Product Type (Rigid Multilayer PCB, Flexible Multilayer PCB, Rigid-Flex Multilayer PCB, High-Density Interconnect (HDI) PCB, Other Specialty Multilayer PCBs), Application (Consumer Electronics, Automotive, Telecommunications, Industrial Equipment, Healthcare & Medical Devices), End-Use Industry (Electronics Manufacturing, Automotive Industry, Telecom Industry, Healthcare Sector), Distribution Channel (Direct Sales, Authorized Distributors, Online Sales Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | TTM Technologies, Inc. (United States), Zhen Ding Technology Holding Limited (Taiwan), Unimicron Technology Corporation (Taiwan), Ibiden Co., Ltd. (Japan), Nippon Mektron, Ltd. (Japan), Samsung Electro-Mechanics Co., Ltd. (South Korea), Compeq Manufacturing Co., Ltd. (Taiwan), Tripod Technology Corporation (Taiwan), Shennan Circuits Company Limited (China), Meiko Electronics Co., Ltd. (Japan), AT&S Austria Technologie & Systemtechnik AG (Austria), Unitech Printed Circuit Board Corporation (Taiwan), Tripod Technology Corporation (Taiwan), TTM Technologies, Inc. (United States), Kinsus Interconnect Technology Corp. (Taiwan), Flex Ltd. (United States), Nanya PCB Corporation (Taiwan), Daeduck GDS Co., Ltd. (South Korea), Viasystems Group, Inc. (United States), Shiyi Technology Co., Ltd. (China), Young Poong Group (South Korea), HannStar Board Corporation (Taiwan), Elite Material Co., Ltd. (Taiwan), Flexium Interconnect, Inc. (Taiwan), Multek Corporation (United States) |

Global Multilayer PCB Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.