North America CRM Software Market Size, Growth & Revenue 2024-2034

North America CRM Software Market is segmented by Type (Cloud-Based CRM, On-Premise CRM, Hybrid CRM, Mobile CRM, AI-Driven CRM), Application (Sales Force Automation, Customer Service Management, Marketing Automation, Analytics, Social CRM), End-User Industry (Retail, Banking, Financial Services and Insurance (BFSI), Healthcare, Manufacturing, Information Technology), Distribution Channel (Direct Sales, Channel Partners, Online Marketplaces), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

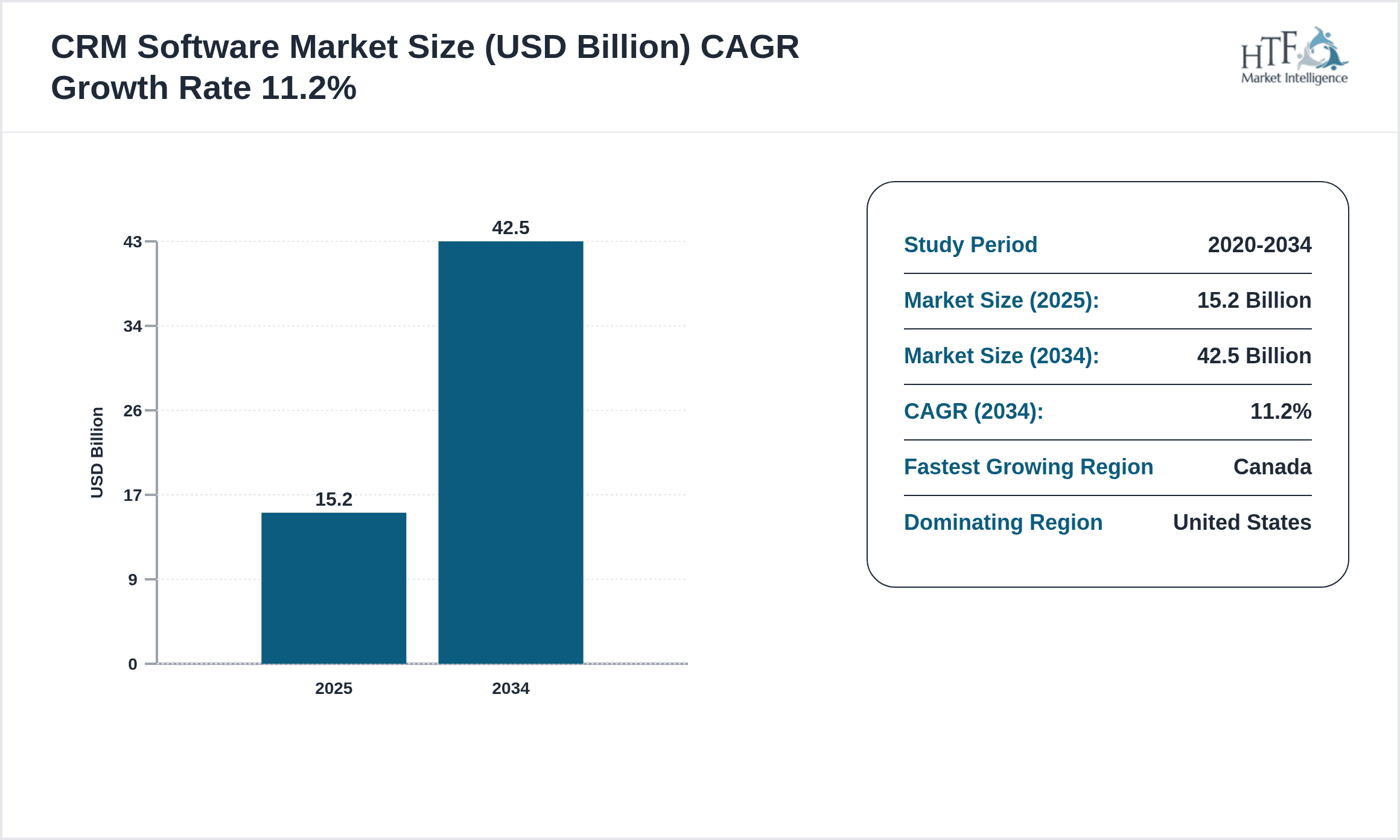

- •The North America CRM Software market represents a dynamic and rapidly evolving segment of the broader enterprise software industry, focused on tools that facilitate customer relationship management. Encompassing cloud-based, on-premise, hybrid, mobile, and AI-driven solutions, it serves a wide spectrum of applications including sales force automation, customer service management, marketing automation, analytics, and social CRM. This market is characterized by increasing digital transformation efforts across industries such as retail, financial services, healthcare, and manufacturing, driving the adoption of sophisticated CRM platforms that enhance customer engagement and operational efficiency. The market scope extends to software vendors, system integrators, and service providers delivering solutions that integrate advanced analytics, artificial intelligence, and omnichannel engagement capabilities. The growing emphasis on personalized customer experiences, data-driven decision-making, and seamless omnichannel interactions underscores the strategic importance of CRM software in North America’s competitive business landscape. Forecasts indicate a robust compound annual growth rate of over 11% through 2034, fueled by cloud migration, AI integration, and expanding small to mid-sized business adoption.

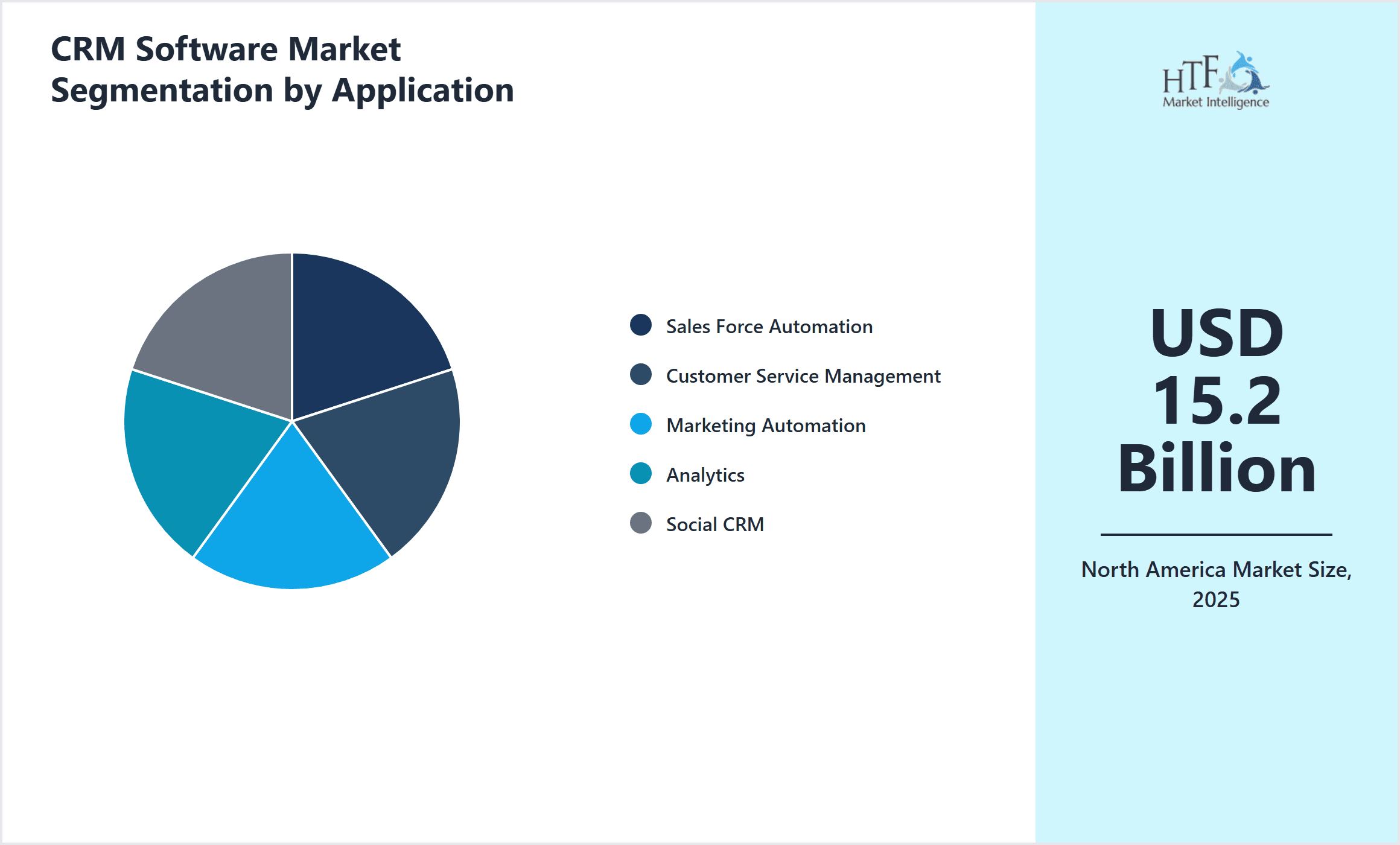

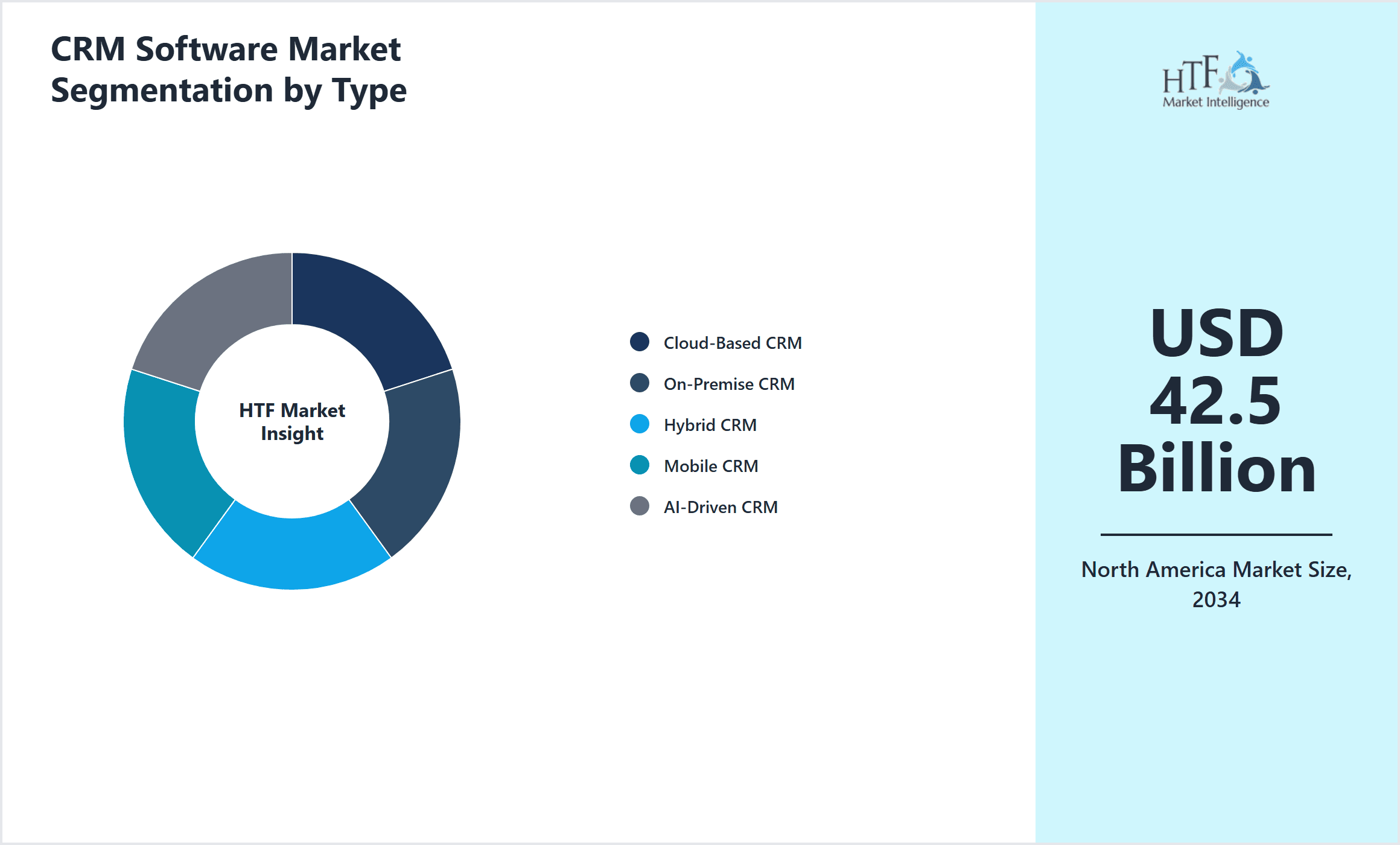

- •Key market highlights include a base market size of USD 15.2 billion in 2024, projected to reach USD 42.5 billion by 2034, reflecting a CAGR of 11.2%. Cloud-based CRM leads the product segment due to scalability and cost benefits, while AI-driven CRM is the fastest-growing type, propelled by predictive analytics and automation. Sales force automation dominates application share, closely followed by customer service management, driven by increased demand for customer retention and satisfaction solutions. The United States holds the dominant market share within North America, with Canada emerging as the fastest-growing country due to rising digital adoption and supportive government initiatives. Market growth is also supported by increasing integration of CRM with other enterprise systems and rising investments in customer experience management technologies.

- •The strategic importance of the North America CRM Software market lies in its role as a critical enabler of customer-centric business transformation. By leveraging CRM platforms, organizations can streamline sales pipelines, personalize marketing efforts, and optimize customer service operations, thereby driving revenue growth and competitive differentiation. The market’s rapid evolution, fueled by technological advancements and shifting customer expectations, presents significant value propositions for software vendors, channel partners, and end-users. Enterprises across verticals benefit from enhanced data insights, improved operational agility, and stronger customer loyalty. As businesses increasingly prioritize digital engagement and data-driven strategies, the CRM software market in North America is poised to remain a pivotal component of enterprise technology stacks, offering sustained growth opportunities through innovation and expanding adoption.

Competitive Landscape

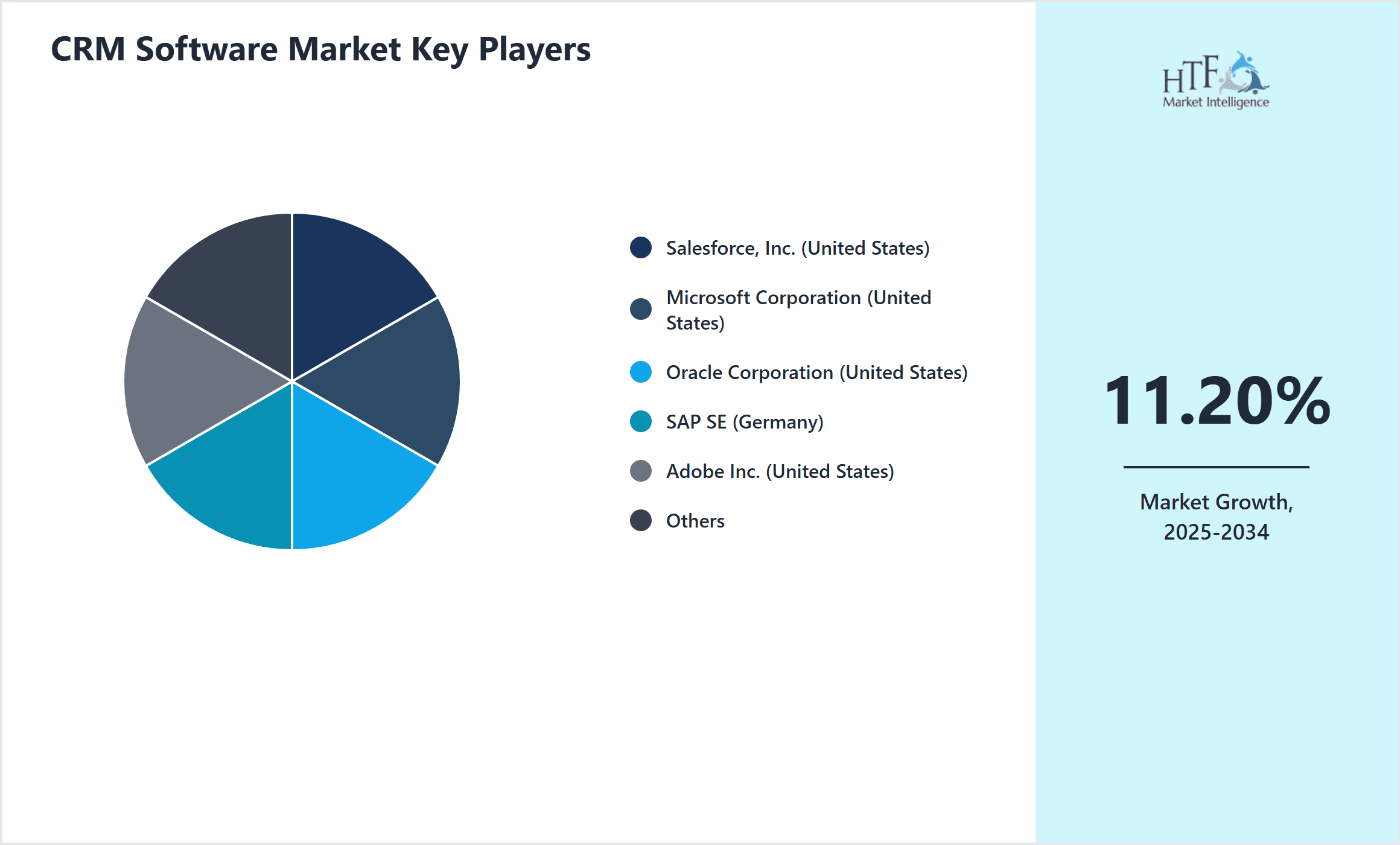

The North America CRM Software market features intense competition characterized by rapid innovation, aggressive pricing strategies, and strategic partnerships. Market players compete by enhancing product capabilities, integrating emerging technologies such as AI and machine learning, and expanding cloud offerings. Established vendors focus on comprehensive platform ecosystems, while niche players differentiate through specialized solutions or vertical-specific functionalities. Competitive dynamics are further influenced by mergers and acquisitions, enabling companies to broaden their portfolios and geographic reach. Pricing models vary from subscription-based SaaS to traditional licensing, impacting customer acquisition and retention. Innovation in user experience, mobile accessibility, and integration with third-party applications remains a key differentiator. Strategic alliances with consulting firms and cloud service providers strengthen market positioning. Overall, rivalry propels continuous product development and customer-centric enhancements, shaping a market environment that demands agility, customer focus, and technological leadership.

Leading Companies in CRM Software Market

- •Salesforce, Inc. (United States)

- •Microsoft Corporation (United States)

- •Oracle Corporation (United States)

- •SAP SE (Germany)

- •Adobe Inc. (United States)

- •HubSpot, Inc. (United States)

- •Zoho Corporation (United States)

- •Freshworks Inc. (United States)

- •SugarCRM Inc. (United States)

- •Pegasystems Inc. (United States)

- •Infor Inc. (United States)

- •Nimble LLC (United States)

- •Zendesk, Inc. (United States)

- •Creatio (United States)

- •Insightly, Inc. (United States)

- •SalesLoft (United States)

- •Pipedrive (United States)

- •Microsoft Dynamics 365 (United States)

- •Oracle NetSuite (United States)

- •SAP Customer Experience (Germany)

- •ActiveCampaign (United States)

- •Copper CRM (United States)

- •Vtiger (United States)

- •Zendesk Sell (United States)

- •Oracle CRM On Demand (United States)

Market Breakdown

- •By Type

- ◦Cloud-Based CRM

- ◦On-Premise CRM

- ◦Hybrid CRM

- ◦Mobile CRM

- ◦AI-Driven CRM

- •By Application

- ◦Sales Force Automation

- ◦Customer Service Management

- ◦Marketing Automation

- ◦Analytics

- ◦Social CRM

- •By End-User Industry

- ◦Retail

- ◦Banking, Financial Services and Insurance (BFSI)

- ◦Healthcare

- ◦Manufacturing

- ◦Information Technology

- •By Distribution Channel

- ◦Direct Sales

- ◦Channel Partners

- ◦Online Marketplaces

Growth Dynamics

The North America CRM Software market is propelled by rapid digital transformation initiatives across industries, accelerating cloud adoption and driving demand for scalable, flexible CRM solutions. Organizations seek to enhance customer engagement and operational efficiency by integrating AI-powered automation and predictive analytics, which streamline sales and marketing workflows. The surge in mobile workforce and remote working necessitates mobile-accessible CRM platforms, further broadening market reach. Increasing investments from SMEs alongside large enterprises expand the user base, while rising competition compels vendors to innovate continuously. Moreover, data-driven decision-making and personalized customer experience strategies fuel CRM adoption, enabling businesses to improve retention and lifetime value. Government incentives for digital innovation and cybersecurity also contribute to growth, positioning CRM software as an essential tool for business resilience and agility in North America’s competitive landscape.

Market Trends

A prominent trend in the North America CRM Software market is the integration of artificial intelligence and machine learning to enable smarter customer insights and predictive sales forecasting. Vendors increasingly offer AI-driven CRM functionalities such as chatbots and sentiment analysis, enhancing automation and customer engagement. Another trend is the shift towards cloud-native CRM solutions, which offer improved scalability, lower upfront costs, and faster deployment compared to traditional on-premise systems. The rise of mobile CRM applications supports remote and field sales teams, reflecting evolving workforce dynamics. Additionally, growing adoption of omnichannel CRM strategies enables seamless, personalized experiences across social media, email, and direct contact. Strategic partnerships between CRM providers and cloud infrastructure companies are also shaping innovation, enabling better interoperability and data integration across enterprise systems.

Market Opportunities

Significant opportunities exist in expanding CRM adoption among small and medium-sized enterprises (SMEs) in North America, where digital transformation is still accelerating. Vendors can capitalize on delivering cost-effective, modular CRM solutions tailored to SME needs, fostering broader market penetration. The growing importance of AI and machine learning offers avenues for innovation in predictive analytics and customer personalization. Additionally, integrating CRM with emerging technologies such as Internet of Things (IoT) and blockchain could unlock new use cases and enhance data security. Expansion of CRM solutions into untapped verticals like healthcare and manufacturing presents further growth potential. Strategic collaborations with cloud service providers and technology partners can facilitate scalable, integrated offerings. Furthermore, increasing regulatory focus on data privacy and compliance opens opportunities for CRM solutions designed with robust security and governance features, meeting evolving customer and legal requirements.

Market Challenges

Despite robust growth, the North America CRM Software market faces challenges including data privacy concerns and compliance with stringent regulations such as GDPR and CCPA, which complicate data management practices. Integration of CRM systems with legacy enterprise applications remains complex and costly, limiting adoption especially among smaller organizations. High implementation and customization costs, coupled with the need for skilled personnel to manage CRM platforms, pose barriers to market entry for some companies. Market fragmentation with numerous vendors and overlapping offerings creates customer confusion and intensifies competition. Additionally, resistance to change within organizations, particularly among sales and service teams accustomed to traditional processes, slows CRM deployment and utilization. The rapid pace of technological evolution demands continuous upgrades, placing pressure on vendors and users to invest in training and system updates, which can impact overall ROI and user satisfaction.

Regulatory Framework

Between 2019 and 2024, North America CRM Software vendors and users have navigated evolving regulatory landscapes focusing on data privacy and cybersecurity. Key regulations include the California Consumer Privacy Act (CCPA) enacted in 2020, which mandates transparency, consumer rights over personal data, and stringent data handling protocols impacting CRM data management. At the federal level, increasing scrutiny on data protection practices has led to enhanced guidelines for software vendors to ensure compliance with privacy laws. Industry-specific regulations in healthcare (HIPAA) and financial services (GLBA) impose additional requirements for CRM solutions handling sensitive customer data. Vendors have adapted by integrating privacy-by-design principles and robust encryption features. Regulatory frameworks also encourage adoption of certifications and standards to assure data security, influencing product development and market entry strategies. These evolving policies shape CRM market dynamics by emphasizing data governance, compliance support, and secure customer engagement tools.

Market Intelligence

On 15th March 2024, Salesforce, Inc. launched its new Einstein GPT, an AI-powered CRM enhancement designed to automate customer interactions and deliver predictive insights across sales and service functions. This innovation leverages natural language processing to generate personalized communications and streamline workflows, significantly boosting user productivity and customer engagement. The launch positions Salesforce to lead in AI-driven CRM solutions, addressing growing demand for intelligent automation among North American enterprises. On 10th October 2023, Microsoft Corporation expanded its Dynamics 365 capabilities with integrated AI models and enhanced analytics features, enabling deeper customer insights and improved decision-making. These strategic enhancements reflect a broader industry trend of embedding advanced AI technologies to differentiate CRM offerings and address complex customer needs across industries.

Mergers and Acquisitions Overview

- •In June 2023, Adobe Inc. acquired Marketo Engage, strengthening its position in the marketing automation segment of the CRM market. This strategic acquisition expanded Adobe's customer experience platform by integrating Marketo’s advanced marketing automation tools, enabling enhanced personalization and campaign management. The deal bolstered Adobe’s cloud-based CRM offerings and facilitated cross-selling opportunities within the North American market. This consolidation reflects ongoing trends where leading CRM vendors seek to broaden capabilities through acquisitions, enhancing competitive advantage and accelerating innovation.

- •In November 2022, Oracle Corporation completed the acquisition of Cerner Corporation, a leading provider of healthcare IT solutions. This acquisition aimed to integrate Cerner’s electronic health records and healthcare CRM capabilities into Oracle’s cloud infrastructure, enhancing its offerings for the healthcare vertical. The deal expanded Oracle’s footprint in the North American healthcare CRM market, enabling more comprehensive data management and patient engagement solutions. The transaction highlights the strategic importance of vertical-specific CRM solutions and cloud adoption trends in the region.

Recent Industry News

- •On 20th January 2025, HubSpot, Inc. announced a major update to its CRM platform with enhanced AI-driven sales forecasting and marketing automation features. These improvements aim to increase forecasting accuracy and automate repetitive marketing tasks, helping businesses optimize customer acquisition and retention strategies. The update responds to growing demand for intelligent CRM tools among North American SMEs. Source: HubSpot Official Press Release

- •On 5th August 2024, Zoho Corporation unveiled Zoho AI, an integrated artificial intelligence assistant embedded within its CRM suite, offering real-time customer sentiment analysis and predictive lead scoring. This innovation enhances user experience and decision-making capabilities, strengthening Zoho’s competitive position in the North American market. Source: Zoho Company News

- •On 12th November 2023, Freshworks Inc. expanded its CRM offering by launching Freshsales Suite, combining sales force automation, marketing automation, and customer support modules in a unified platform. The launch targets mid-market companies seeking integrated CRM solutions to streamline customer engagement. Source: Freshworks Press Release

- •On 28th February 2023, Microsoft Corporation partnered with Adobe to integrate Dynamics 365 CRM with Adobe Experience Cloud, enabling seamless data exchange and enhanced customer journey analytics. This collaboration aims to provide enterprises with comprehensive CRM and marketing capabilities, facilitating personalized customer interactions across channels. Source: Microsoft News Center

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 15.2 Billion |

| Forecast Year Market Size | USD 42.5 Billion |

| CAGR | 11.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.1% |

| Scope of Report | Market is segmented by Type (Cloud-Based CRM, On-Premise CRM, Hybrid CRM, Mobile CRM, AI-Driven CRM), Application (Sales Force Automation, Customer Service Management, Marketing Automation, Analytics, Social CRM), End-User Industry (Retail, Banking, Financial Services and Insurance (BFSI), Healthcare, Manufacturing, Information Technology), Distribution Channel (Direct Sales, Channel Partners, Online Marketplaces) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Salesforce, Inc. (United States), Microsoft Corporation (United States), Oracle Corporation (United States), SAP SE (Germany), Adobe Inc. (United States), HubSpot, Inc. (United States), Zoho Corporation (United States), Freshworks Inc. (United States), SugarCRM Inc. (United States), Pegasystems Inc. (United States), Infor Inc. (United States), Nimble LLC (United States), Zendesk, Inc. (United States), Creatio (United States), Insightly, Inc. (United States), SalesLoft (United States), Pipedrive (United States), Microsoft Dynamics 365 (United States), Oracle NetSuite (United States), SAP Customer Experience (Germany), ActiveCampaign (United States), Copper CRM (United States), Vtiger (United States), Zendesk Sell (United States), Oracle CRM On Demand (United States) |

North America CRM Software Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.