Global Infant Formula Packaging Market Size, Growth & Revenue 2025-2034

Global Infant Formula Packaging Market is segmented by Product Type (Plastic Packaging, Metal Packaging, Glass Packaging, Paper-Based Packaging, Flexible Packaging), Application (Powdered Infant Formula, Liquid Infant Formula, Concentrated Infant Formula, Ready-to-Feed Formula, Specialty Infant Formula), End-Use Industry (Retail, Healthcare Facilities, Online Retail, Foodservice), Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, E-commerce, Pharmacies & Drugstores), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Infant Formula Packaging market represents a vital segment of the food packaging industry, focusing on specialized packaging solutions designed to safeguard the quality and safety of infant formula products. This market spans multiple packaging types such as plastic, metal, glass, paper-based, and flexible materials, each selected based on product form and preservation requirements. Applications include powdered, liquid, concentrated, ready-to-feed, and specialty infant formulas, all demanding packaging that complies with rigorous hygiene and safety regulations. The market is influenced by growing global demand for infant nutrition products driven by rising birth rates, increased parental awareness, and urbanization trends in emerging economies. Innovations in sustainable and smart packaging technologies are reshaping the competitive landscape, enabling manufacturers to meet environmental targets while enhancing consumer convenience and product shelf life. Key market players focus on developing eco-friendly materials and advanced barrier properties to reduce contamination risks and extend freshness. Regional dynamics show North America dominates market share due to high consumer spending and regulatory frameworks, while Asia-Pacific is poised for the fastest growth driven by expanding middle-class populations and increasing formula consumption. The market outlook from 2025 through 2034 forecasts robust growth supported by technological advancements, evolving consumer preferences, and expanding distribution channels including e-commerce. This comprehensive analysis covers market segmentation, growth drivers, challenges, opportunities, and competitive strategies shaping the future of infant formula packaging worldwide.

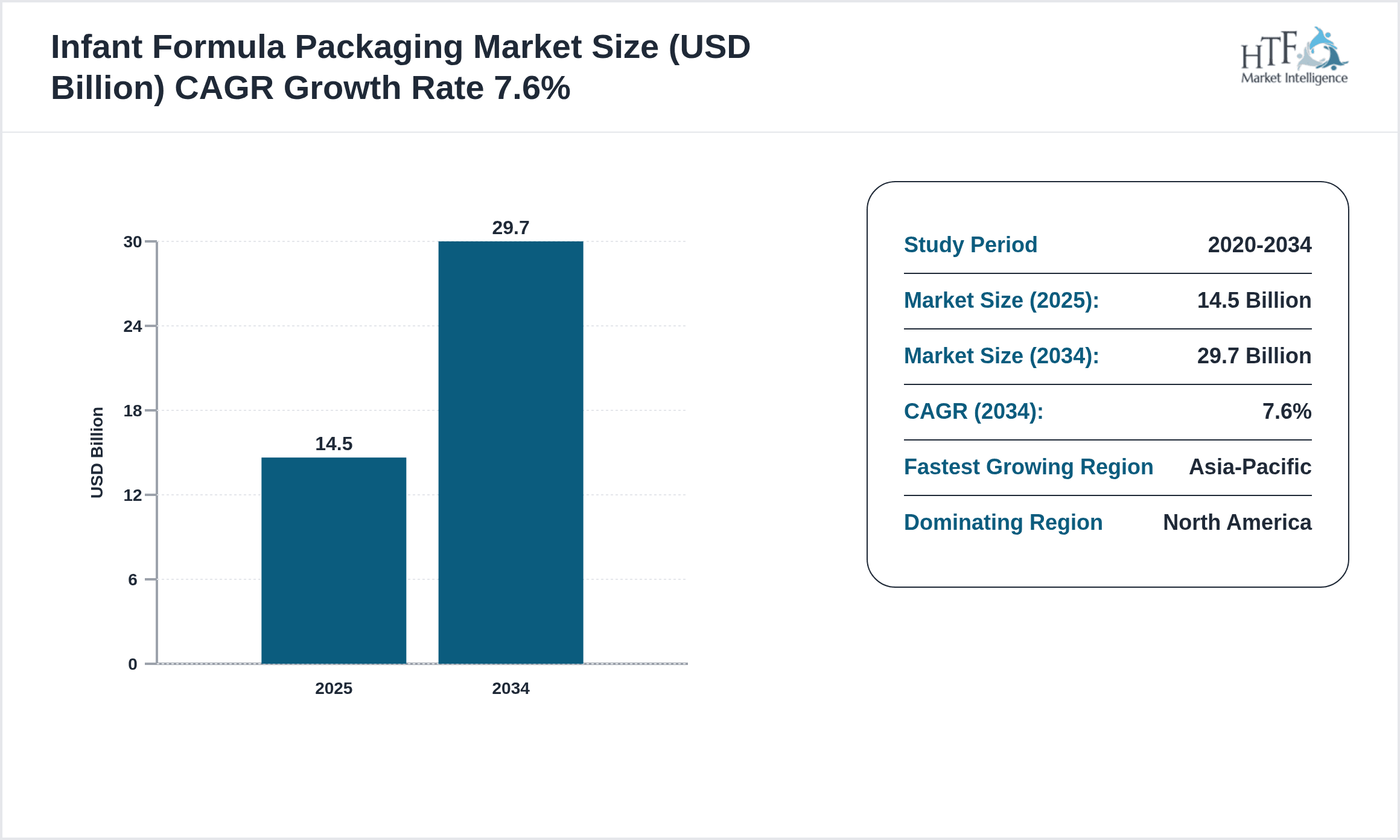

- •Key market highlights include a base market size of USD 14.5 Billion in 2025, projected to reach USD 29.7 Billion by 2034, reflecting a CAGR of 7.6%. The year-on-year growth rate is calculated at 7.3%, indicating strong and steady expansion fueled by sustained demand across all major regions. Plastic packaging remains the leading product type due to its versatility and cost-effectiveness, whereas flexible packaging is identified as the fastest growing segment, attributed to its lightweight, eco-friendly attributes and convenience for caregivers. North America holds dominance in market share owing to mature infrastructure and stringent product safety regulations, while Asia-Pacific leads growth momentum propelled by changing lifestyles and increasing infant nutrition awareness. The market also benefits from rising investments in packaging innovation, sustainable materials, and digitalization of supply chains, enhancing product traceability and consumer engagement.

- •The infant formula packaging market holds strategic importance for stakeholders including manufacturers, retailers, healthcare providers, and regulatory bodies. Packaging innovations directly impact product safety, shelf life, and consumer trust, which are critical in infant nutrition. The value proposition centers on delivering packaging solutions that meet regulatory compliance, ensure product integrity, and support sustainability goals. For manufacturers, this translates into opportunities for differentiation through advanced materials and smart packaging technologies. Retailers benefit from packaging designs that enhance shelf appeal and convenience, while consumers gain from improved usability and safety assurances. Regulatory compliance remains a cornerstone, driving continuous improvements in packaging standards and testing protocols. Overall, the market serves as a key enabler in the infant nutrition value chain, balancing consumer needs with environmental and safety considerations in a competitive global landscape.

Competitive Landscape

The global infant formula packaging market is characterized by intense competition among established multinational corporations and regional players focused on innovation, quality, and sustainability. Market dynamics are shaped by strategic investments in research and development, enabling companies to introduce advanced packaging materials such as biodegradable plastics and multi-layered barriers that enhance product preservation. Competitive strategies include mergers and acquisitions to expand geographic presence and product portfolios, partnerships with raw material suppliers to secure high-quality inputs, and collaborations with infant formula manufacturers to tailor packaging solutions. Pricing strategies are influenced by raw material costs and regulatory compliance expenses, with companies striving to balance affordability and premium quality. Distribution channel optimization, including e-commerce integration, is a key focus area to increase market reach and consumer accessibility. Technological adoption of smart packaging with features like freshness indicators and tamper-evident seals enhances brand differentiation and consumer trust. Market entry barriers such as stringent regulatory requirements and high capital investment limit new entrants, while regional competition varies with North America and Europe emphasizing regulatory compliance and Asia-Pacific focusing on cost-effective innovations. Looking ahead, the competitive landscape will evolve with sustainability mandates and digital transformation shaping product development and go-to-market strategies.

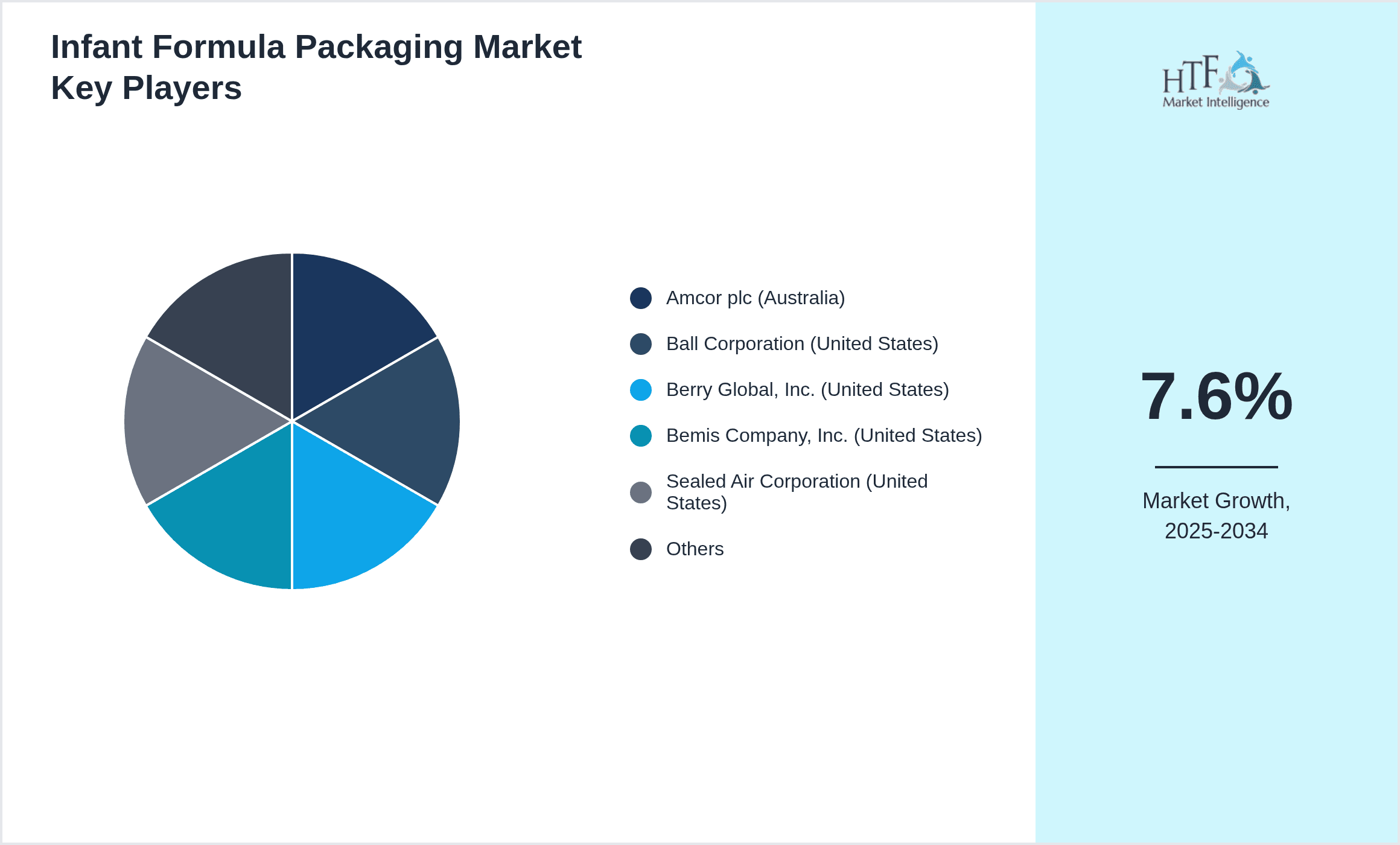

Companies Shaping the Infant Formula Packaging Market

- •Amcor plc (Australia)

- •Ball Corporation (United States)

- •Berry Global, Inc. (United States)

- •Bemis Company, Inc. (United States)

- •Sealed Air Corporation (United States)

- •Sonoco Products Company (United States)

- •Huhtamaki Oyj (Finland)

- •Mondi Group (United Kingdom)

- •WestRock Company (United States)

- •International Paper Company (United States)

- •Coveris Holdings S.A. (Luxembourg)

- •ProAmpac (United States)

- •Smurfit Kappa Group (Ireland)

- •RPC Group Plc (United Kingdom)

- •Tetra Pak International S.A. (Switzerland)

- •Sonoco-Alcore (United States)

- •Graham Packaging Company (United States)

- •Plastipak Packaging, Inc. (United States)

- •Berry Global Group, Inc. (United States)

- •MJS Packaging (United States)

- •Coveris Rigid (United Kingdom)

- •SIG Combibloc Group AG (Switzerland)

- •Bemis Company, Inc. (United States)

- •Huhtamaki Oyj (Finland)

- •AptarGroup, Inc. (United States)

Market Breakdown

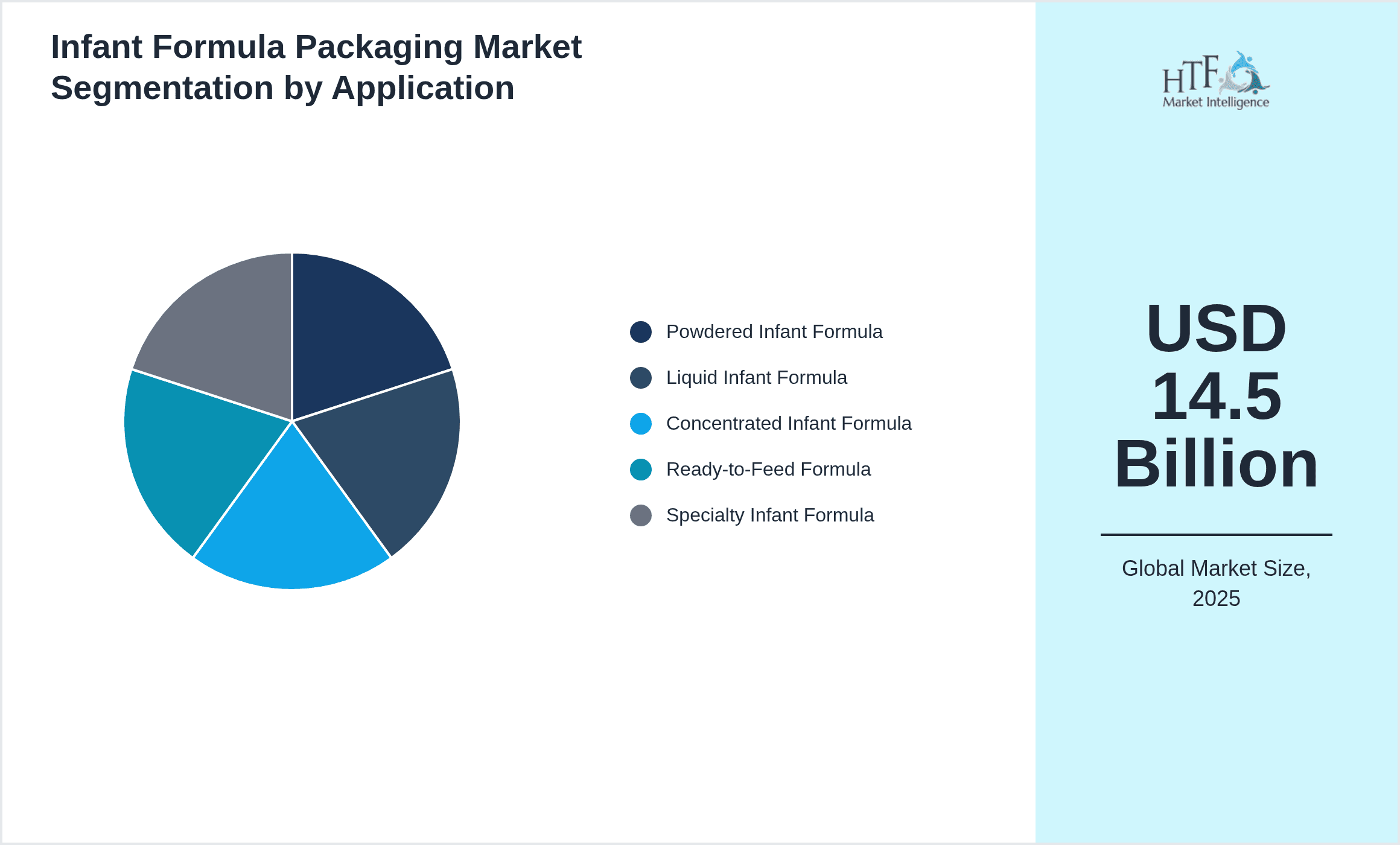

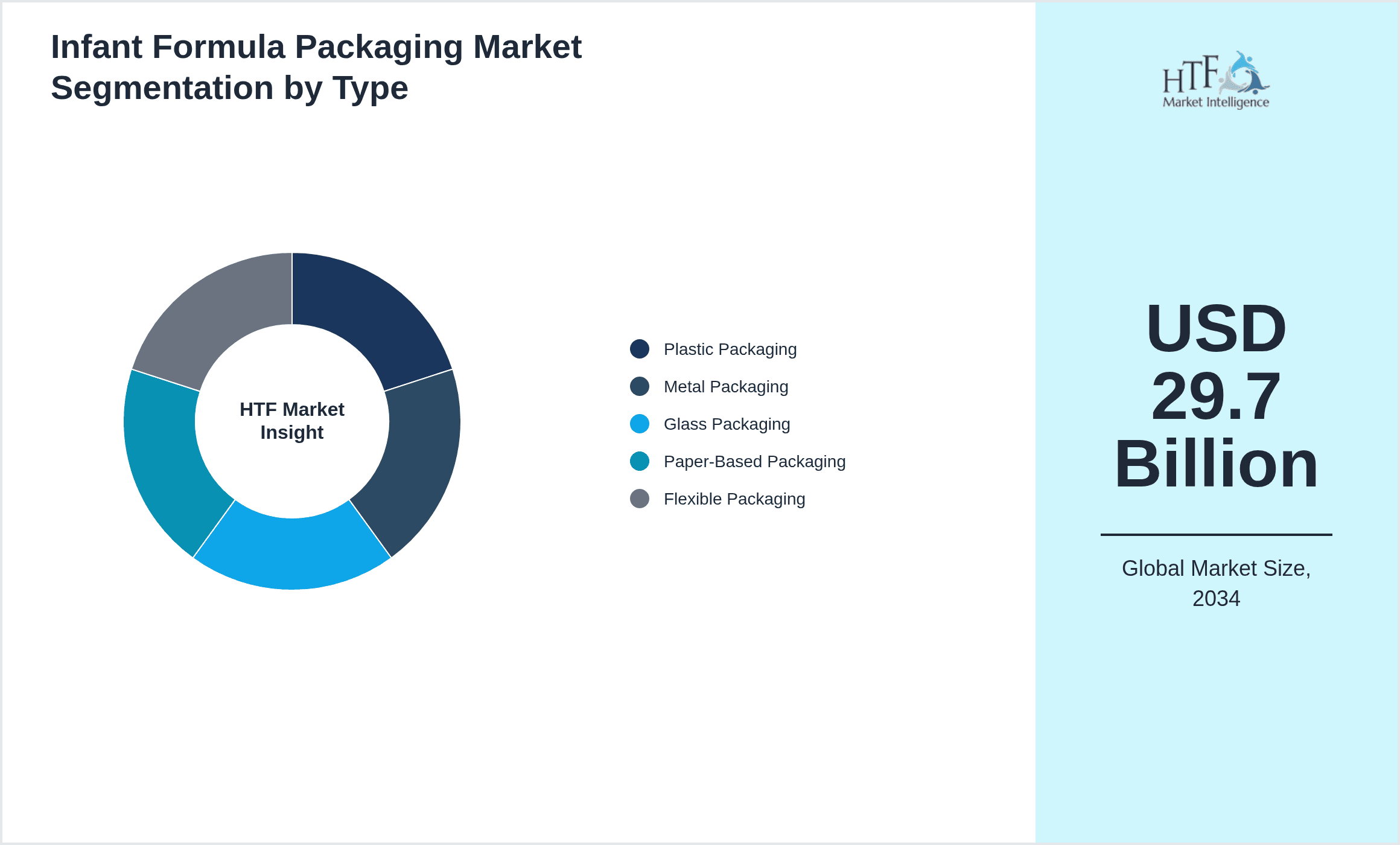

- •By Product Type

- ◦Plastic Packaging

- ◦Metal Packaging

- ◦Glass Packaging

- ◦Paper-Based Packaging

- ◦Flexible Packaging

- •By Application

- ◦Powdered Infant Formula

- ◦Liquid Infant Formula

- ◦Concentrated Infant Formula

- ◦Ready-to-Feed Formula

- ◦Specialty Infant Formula

- •By End-Use Industry

- ◦Retail

- ◦Healthcare Facilities

- ◦Online Retail

- ◦Foodservice

- •By Distribution Channel

- ◦Supermarkets & Hypermarkets

- ◦Specialty Stores

- ◦E-commerce

- ◦Pharmacies & Drugstores

Growth Dynamics

The global infant formula packaging market growth is primarily driven by increasing birth rates and rising awareness about infant nutrition, particularly in developing regions. Urbanization and changing lifestyles have led to heightened demand for convenient and safe packaging solutions, facilitating portability and ease of use for caregivers. Technological advancements in packaging materials, including biodegradable and flexible options, are reducing environmental impacts while enhancing product safety. Additionally, stringent regulatory frameworks globally mandate high standards for infant formula packaging, which encourages manufacturers to innovate continuously. The growth trajectory is further supported by expanding distribution channels, notably e-commerce, which increases product accessibility to a broader demographic. Investments in smart packaging technologies that provide freshness indicators and tamper evidence are gaining traction, boosting consumer confidence and brand loyalty. Furthermore, collaborations between packaging suppliers and infant formula manufacturers are fostering tailored solutions that meet regional consumer preferences and compliance standards. This confluence of demographic, technological, and regulatory factors underpins the robust growth forecast for the infant formula packaging market through 2034.

Market Trends

Sustainability is a dominant trend shaping the infant formula packaging market, with increased adoption of eco-friendly materials such as biodegradable plastics and recyclable paper-based solutions. Leading companies are investing in circular economy initiatives to reduce packaging waste and carbon footprint. Another trend is the integration of smart packaging features including QR codes and freshness sensors, which enhance consumer engagement and product traceability. The rise of e-commerce has prompted the development of packaging designs optimized for shipping durability and convenience. Additionally, premiumization trends are influencing packaging aesthetics and functionality, with a focus on user-friendly designs that facilitate easy storage and handling. Regulatory pressures are driving standardization of packaging materials and safety protocols across regions. Digital printing technologies are gaining popularity, enabling customization and faster time-to-market. These trends collectively contribute to evolving consumer expectations and competitive differentiation in the infant formula packaging industry.

Market Opportunities

Emerging markets in Asia-Pacific and Latin America present significant growth opportunities due to rising disposable incomes, urbanization, and increasing infant formula consumption. There is a growing demand for sustainable packaging solutions that reduce environmental impact without compromising product safety. Innovations in flexible packaging that offer convenience and extended shelf life are gaining traction, opening avenues for product differentiation. Strategic partnerships between packaging manufacturers and infant formula producers can accelerate innovation and market penetration. Additionally, the expansion of e-commerce platforms offers new distribution channels for packaged infant formula products, enabling reach into remote and underserved regions. Investment in smart packaging technologies that enhance consumer interaction and safety compliance also represents a lucrative opportunity. Companies can capitalize on these trends by aligning product development strategies with evolving consumer needs and regulatory requirements, ensuring sustainable and profitable growth in the coming decade.

Market Challenges

The infant formula packaging market faces challenges including stringent regulatory compliance which requires substantial investment in quality assurance and testing protocols, increasing operational costs. Raw material price volatility, particularly for plastics and metals, poses risks to profitability and pricing stability. Environmental concerns and rising consumer demand for sustainable packaging necessitate costly research and development to develop eco-friendly alternatives without compromising product safety. Additionally, complex supply chains and logistics issues, exacerbated by global disruptions such as pandemics, impact timely delivery and inventory management. High competition intensifies pressure on margins, especially in mature markets where differentiation is limited. Furthermore, counterfeit products and packaging fraud pose risks to brand reputation and consumer trust, requiring advanced anti-counterfeiting technologies. Addressing these challenges demands strategic investments in innovation, regulatory expertise, and supply chain resilience to maintain competitive advantage and market growth.

Regulatory Framework

Between 2020 and 2025, regulatory frameworks globally have tightened to ensure the safety and integrity of infant formula packaging. Key regulations include the Food and Drug Administration (FDA) mandates in North America, requiring strict compliance with material safety, labeling, and tamper-evidence standards. The European Union’s Packaging and Packaging Waste Directive (PPWD) emphasizes sustainability and recyclability, influencing packaging design and material selection. Asia-Pacific countries have introduced specific infant formula packaging regulations addressing contamination risks and traceability requirements, such as China's GB standards. These regulations mandate rigorous testing for chemical migration, barrier properties, and product compatibility. Enforcement mechanisms involve periodic audits, certifications, and penalties for non-compliance, prompting manufacturers to adopt advanced quality control systems. Additionally, global initiatives like the United Nations Sustainable Development Goals (SDGs) promote eco-friendly packaging solutions, encouraging industry-wide adoption of biodegradable and recyclable materials. Governments have provided incentives and support programs to facilitate innovation in sustainable packaging, balancing consumer safety with environmental responsibility. Overall, regulatory evolution continues to shape industry practices, driving higher standards and continuous improvement in infant formula packaging.

Market Intelligence

- •15th March 2025, Amcor plc announced the launch of its new biodegradable flexible packaging line specifically designed for powdered infant formula products. This innovative packaging utilizes plant-based materials that comply with global safety standards and offers superior barrier properties to maintain product freshness. Targeting markets in North America and Asia-Pacific, the company aims to reduce environmental impact while meeting rising consumer demand for sustainable solutions. The launch is complemented by strategic investments in manufacturing capacity expansion and collaboration with infant formula producers to customize packaging designs. This initiative positions Amcor as a leader in eco-friendly infant formula packaging, responding to regulatory pressures and shifting market preferences. Source: Amcor Official Press Release

- •10th July 2025, Tetra Pak International S.A. unveiled its latest aseptic packaging technology integrating smart freshness indicators for liquid infant formula applications. The technology uses embedded sensors to monitor product integrity throughout the supply chain, enhancing consumer confidence and reducing waste. This advancement supports Tetra Pak’s commitment to digital transformation and sustainability, enabling real-time quality assurance. The company targets expanding markets in Europe and Latin America, where demand for ready-to-feed formulas is growing rapidly. The innovation is expected to set new industry standards and strengthen Tetra Pak’s competitive positioning. Source: Tetra Pak Press Release

- •5th November 2025, Berry Global, Inc. announced a strategic partnership with a leading infant formula manufacturer to co-develop recyclable plastic packaging solutions. This collaboration focuses on integrating post-consumer recycled materials without compromising packaging performance or safety. The initiative aligns with global sustainability goals and regulatory mandates in North America and Europe. Berry Global plans to leverage its extensive R&D capabilities and supply chain to accelerate commercialization by 2027. This partnership aims to meet growing consumer demand for environmentally responsible packaging while maintaining product integrity. Source: Berry Global Corporate Announcement

- •20th January 2025, Sealed Air Corporation completed the acquisition of a specialty packaging firm specializing in tamper-evident and child-resistant closures for infant formula containers. The acquisition strengthens Sealed Air’s product portfolio and enhances its ability to offer integrated safety solutions. This strategic move supports the company's growth objectives in the infant nutrition packaging sector, particularly in Asia-Pacific and Middle East & Africa regions. The deal is expected to generate synergies through expanded distribution channels and innovation capabilities, reinforcing Sealed Air’s leadership position. Source: Sealed Air Investor Relations

- •Source: Various Official Company Press Releases, Industry Publications, and Regulatory Announcements

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 14.5 Billion |

| Forecast Year Market Size | USD 29.7 Billion |

| CAGR | 7.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.3% |

| Scope of Report | Market is segmented by Product Type (Plastic Packaging, Metal Packaging, Glass Packaging, Paper-Based Packaging, Flexible Packaging), Application (Powdered Infant Formula, Liquid Infant Formula, Concentrated Infant Formula, Ready-to-Feed Formula, Specialty Infant Formula), End-Use Industry (Retail, Healthcare Facilities, Online Retail, Foodservice), Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, E-commerce, Pharmacies & Drugstores) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Amcor plc (Australia), Ball Corporation (United States), Berry Global, Inc. (United States), Bemis Company, Inc. (United States), Sealed Air Corporation (United States), Sonoco Products Company (United States), Huhtamaki Oyj (Finland), Mondi Group (United Kingdom), WestRock Company (United States), International Paper Company (United States), Coveris Holdings S.A. (Luxembourg), ProAmpac (United States), Smurfit Kappa Group (Ireland), RPC Group Plc (United Kingdom), Tetra Pak International S.A. (Switzerland), Sonoco-Alcore (United States), Graham Packaging Company (United States), Plastipak Packaging, Inc. (United States), Berry Global Group, Inc. (United States), MJS Packaging (United States), Coveris Rigid (United Kingdom), SIG Combibloc Group AG (Switzerland), Bemis Company, Inc. (United States), Huhtamaki Oyj (Finland), AptarGroup, Inc. (United States) |

Global Infant Formula Packaging Market Size, Growth & Revenue 2025-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.