Global Debt Collection Services Market Size, Growth & Revenue 2024-2034

Global Debt Collection Services Market is segmented by Product Type (In-house Collection Services, Third-party Collection Agencies, Debt Purchase Services, Legal Collection Services, Early-stage Collection Services), Application (Consumer Debt Collection, Commercial Debt Collection, Healthcare Debt Collection, Government Debt Collection, Utility Debt Collection), End-Use Industry (Banking & Financial Services, Healthcare, Government & Public Sector, Utilities & Telecom), Distribution Channel (Direct Collection, Outsourced Collection, Digital Collection Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Debt Collection Services Market is a critical segment of the financial services industry focused on recovering overdue payments from consumers, businesses, and government entities. It includes a variety of service types such as in-house collection teams, outsourced third-party agencies, debt purchasing firms, legal collection services, and early-stage collection specialists. The market serves multiple application areas including consumer loans, commercial credit, healthcare billing, government receivables, and utility payments. Increasing debt volumes due to economic cycles, credit expansions, and rising delinquencies have expanded market scope significantly. Technological advancements, including AI-powered analytics and automated communication, have transformed collection methodologies to enhance efficiency and compliance. The market operates within stringent regulatory frameworks to protect consumer rights while maximizing recovery rates. Stakeholders range from financial institutions and service providers to regulators and consumers, underscoring the sector’s profound impact on global financial stability and credit ecosystems. Continuous innovation and regulatory adaptation remain key drivers shaping the market landscape over the forecast period.

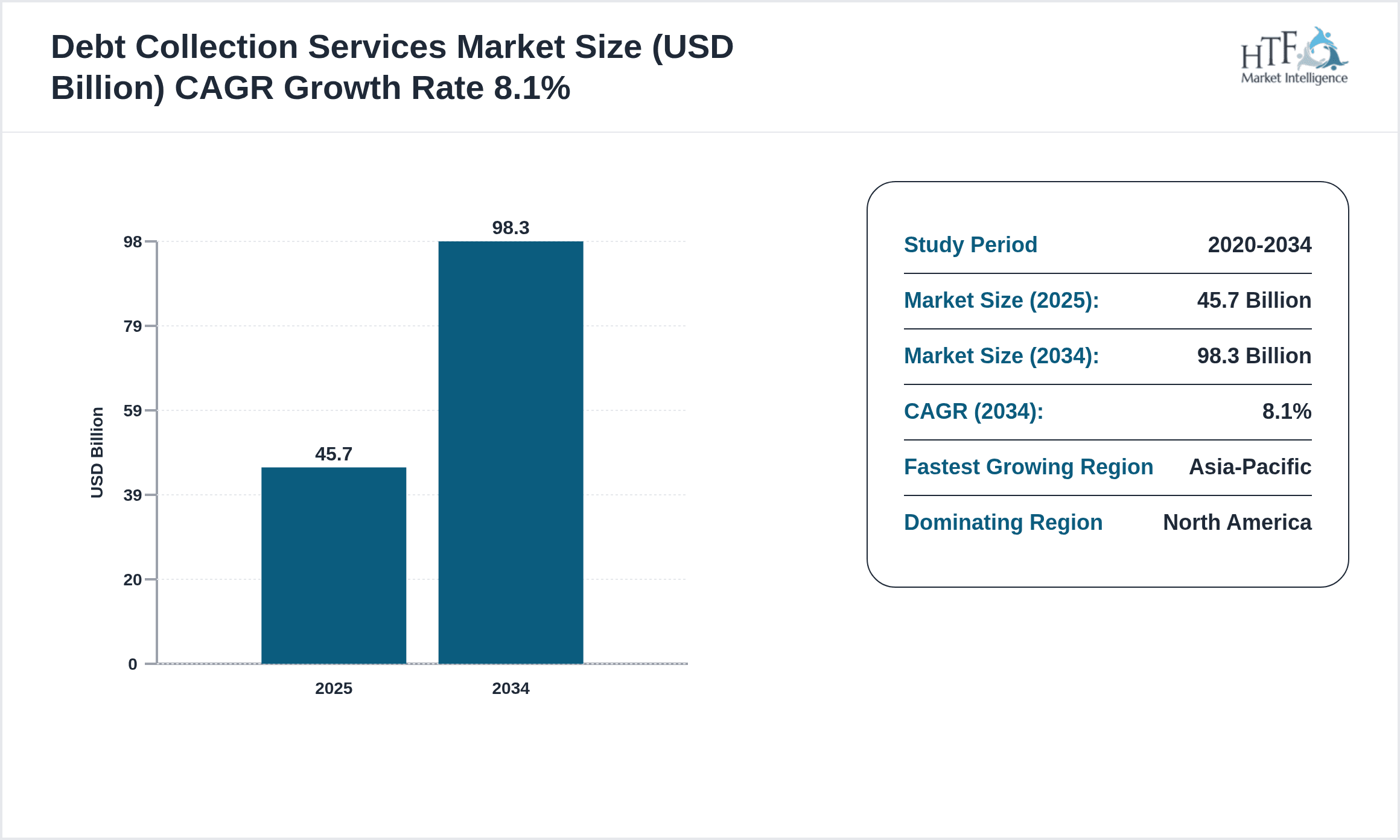

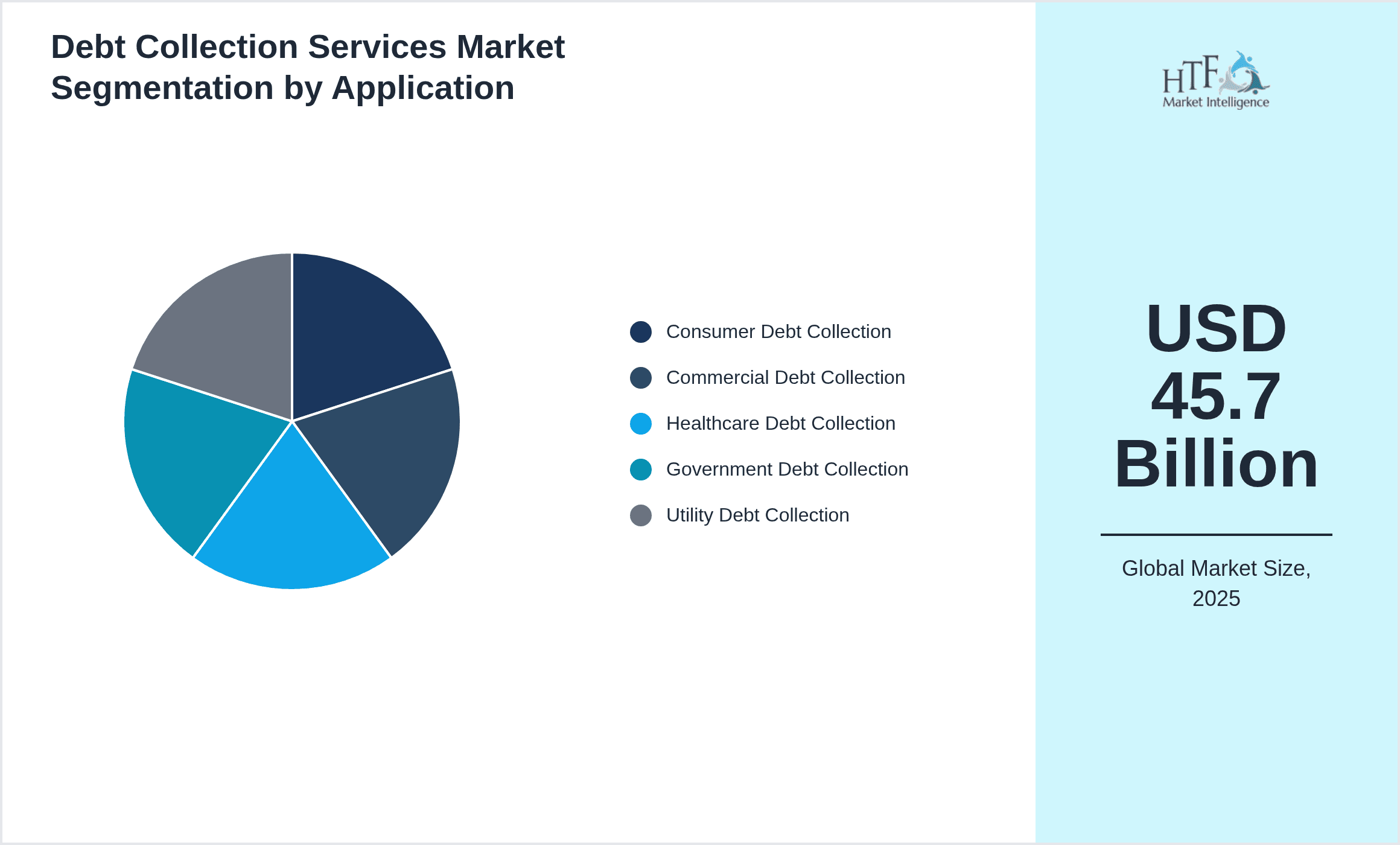

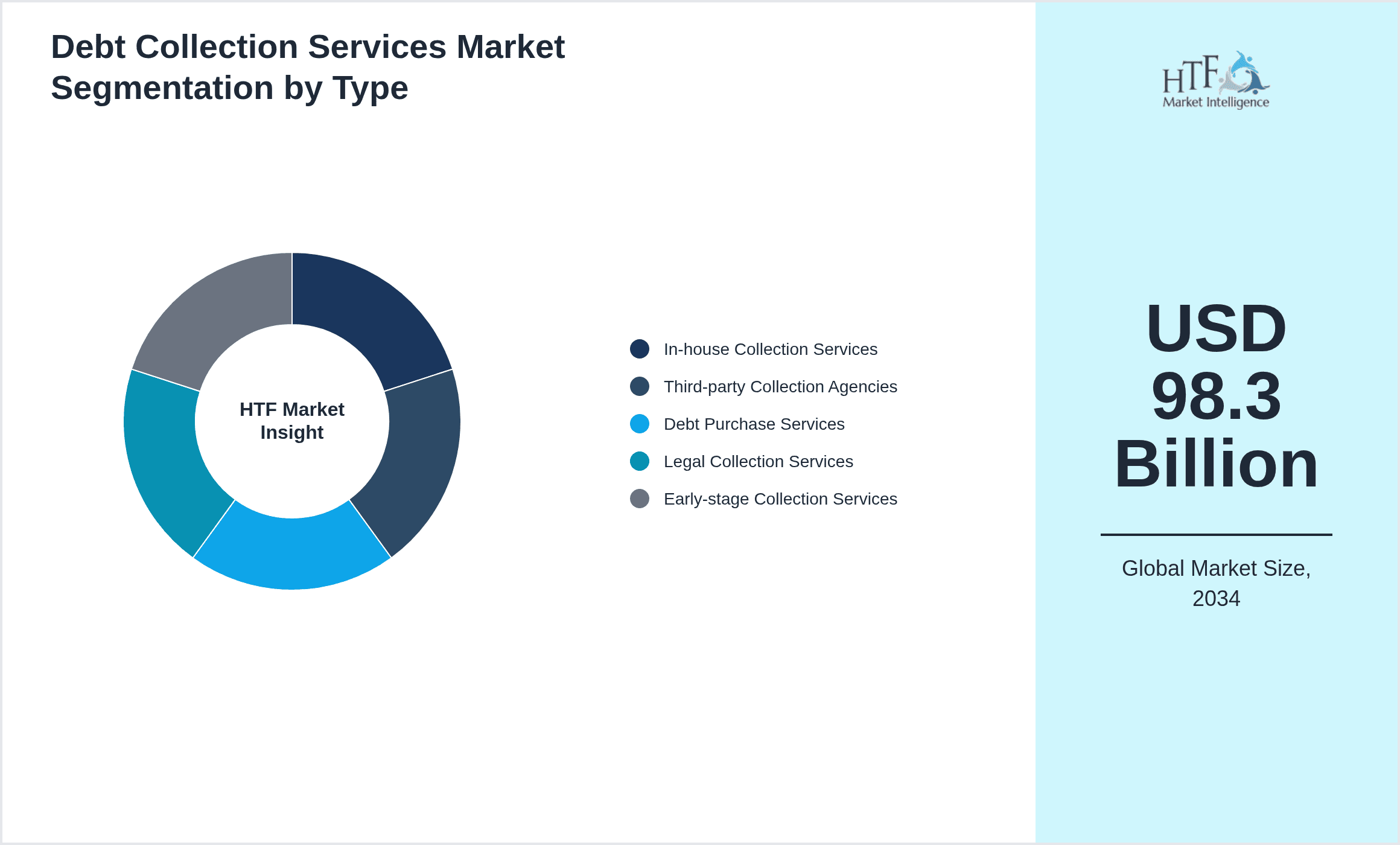

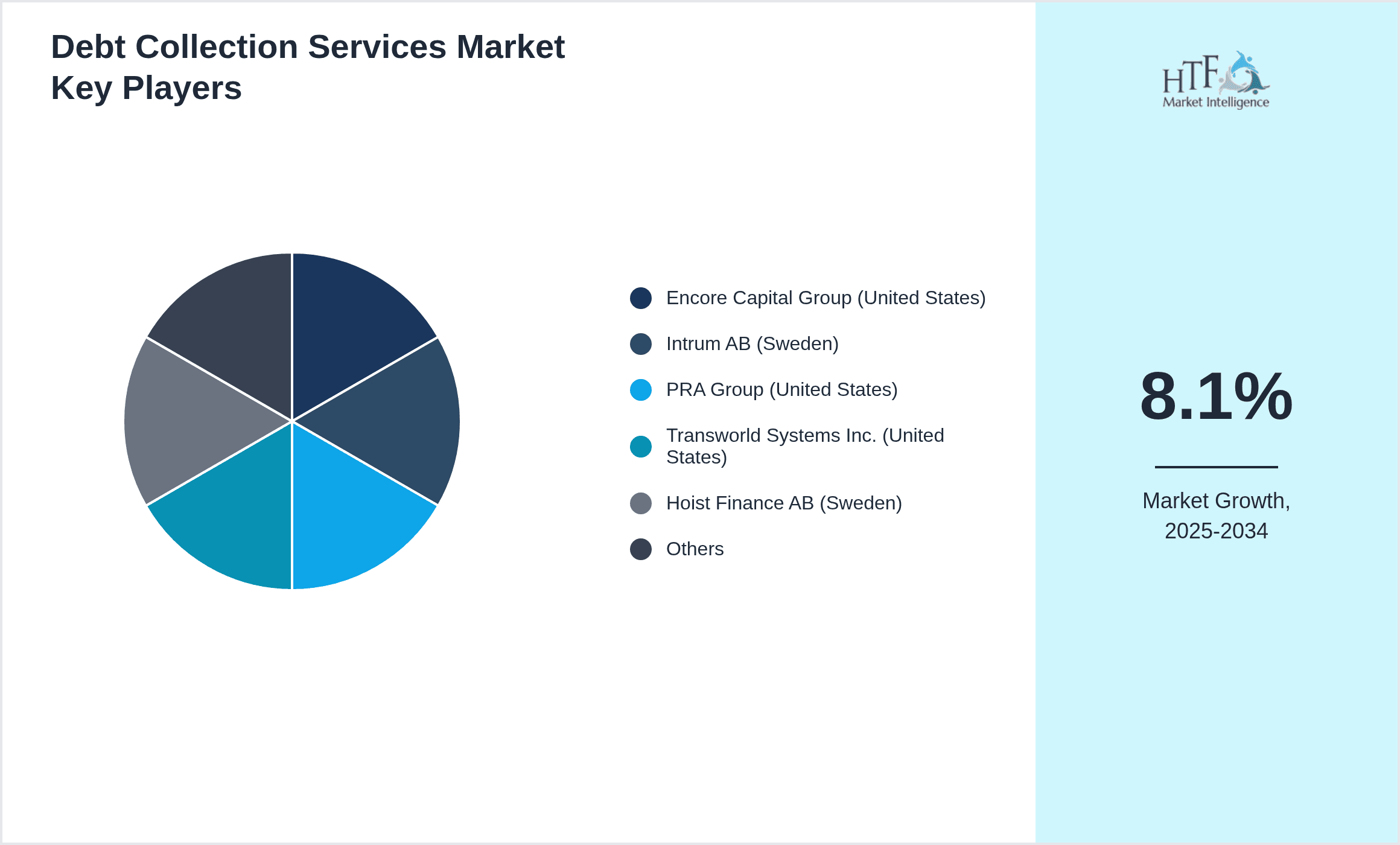

- •Key market highlights include a robust forecast CAGR of 8.1% from 2024 to 2034, with market size expected to reach USD 98.3 Billion by 2034 from USD 45.7 Billion in 2024. North America currently dominates the market due to mature financial sectors and advanced regulatory environments, while Asia-Pacific is poised as the fastest growing region driven by increasing credit penetration and rising consumer debt. Third-party collection services lead the product type segment, reflecting increasing outsourcing trends, whereas debt purchase services exhibit the highest growth rate owing to aggressive debt acquisition strategies. Consumer and commercial debt applications form the largest segments, supported by growing delinquencies and expanding credit portfolios globally. These dynamics highlight the market’s significant growth potential and evolving competitive landscape.

- •The debt collection services market offers substantial value propositions through improved cash flow management, risk mitigation, and operational efficiency for financial institutions and creditors. Enhanced collection processes reduce non-performing asset ratios and support credit availability, contributing to overall economic health. For third-party agencies and technology providers, the market presents opportunities for innovation-driven differentiation and geographic expansion. Additionally, compliance with evolving regulations ensures sustainable growth while protecting consumer rights. This strategic importance extends across banking, healthcare, utilities, government sectors, and more, making debt collection services indispensable for managing credit risks in an increasingly digital and credit-dependent global economy.

Competitive Landscape

The global debt collection services market is characterized by intense competition among a diverse range of players including multinational agencies, specialized regional firms, and emerging technology-driven startups. Market leaders leverage strong client relationships, extensive geographic coverage, and compliance expertise to maintain dominance. Innovation is a key competitive strategy, with companies investing heavily in AI, machine learning, and automated communication tools to enhance recovery rates and reduce operational costs. Strategic partnerships and mergers are common to expand service portfolios and market reach. Pricing strategies vary from performance-based models to fixed fees, depending on client preferences and regulatory constraints. Furthermore, differentiation is achieved through specialized services such as healthcare collections and government receivables management. The competitive environment also reflects regional regulatory variations, prompting tailored approaches in local markets. Overall, market rivalry drives continuous improvement in service quality, efficiency, and technological adoption, positioning the sector for sustained growth and evolving competitive dynamics.

Leading Companies in Debt Collection Services Market

- •Encore Capital Group (United States)

- •Intrum AB (Sweden)

- •PRA Group (United States)

- •Transworld Systems Inc. (United States)

- •Hoist Finance AB (Sweden)

- •Coface (France)

- •Arrow Global Group (United Kingdom)

- •B2Holding ASA (Norway)

- •Kirkland & Ellis LLP (United States)

- •MCM Capital Group (United States)

- •Sherman Financial Group (United States)

- •Creditreform AG (Germany)

- •Cerved Group (Italy)

- •Capita PLC (United Kingdom)

- •Serrala Group (Germany)

- •EOS Group (Germany)

- •Convergent Outsourcing, Inc. (United States)

- •GC Services (United States)

- •Asta Funding, Inc. (United States)

- •FICO (United States)

- •Recova Debt Recovery (United Kingdom)

- •Collective Asset Recovery, LLC (United States)

- •Atradius Collections (Netherlands)

- •Dun & Bradstreet (United States)

- •TransUnion (United States)

Market Breakdown

- •By Product Type

- ◦In-house Collection Services

- ◦Third-party Collection Agencies

- ◦Debt Purchase Services

- ◦Legal Collection Services

- ◦Early-stage Collection Services

- •By Application

- ◦Consumer Debt Collection

- ◦Commercial Debt Collection

- ◦Healthcare Debt Collection

- ◦Government Debt Collection

- ◦Utility Debt Collection

- •By End-Use Industry

- ◦Banking & Financial Services

- ◦Healthcare

- ◦Government & Public Sector

- ◦Utilities & Telecom

- •By Distribution Channel

- ◦Direct Collection

- ◦Outsourced Collection

- ◦Digital Collection Platforms

Growth Dynamics

- •Rising global consumer and commercial debt levels, driven by economic expansion and increased credit accessibility, fuel demand for debt collection services. Financial institutions seek efficient recovery mechanisms to manage credit risk and non-performing assets.

- •Technological advancements such as AI-powered analytics, automated communication tools, and digital payment platforms enhance collection efficiency and compliance, attracting widespread adoption among service providers and creditors.

- •Regulatory frameworks emphasizing consumer protection and transparent collection practices compel service providers to innovate and adopt compliant strategies, thereby fostering market growth.

- •Outsourcing trends continue to rise as organizations prefer third-party specialists with expertise and technology capabilities to improve recovery rates and reduce operational costs.

- •Expansion of financial services in emerging markets, particularly in Asia-Pacific and Latin America, introduces new customer segments and increases demand for localized debt collection solutions.

- •Growing integration of analytics and data-driven decision-making supports better debtor profiling, leading to more effective collection strategies and improved portfolio performance.

- •Collaborations between debt collection agencies and fintech firms facilitate innovative service offerings and access to advanced technologies, propelling market momentum.

Market Trends

- •Adoption of AI and machine learning algorithms has become mainstream, enabling predictive analytics and personalized debtor engagement, thereby improving collection success rates significantly.

- •Digital transformation through mobile and online platforms allows debtors to engage in self-service collections, enhancing customer experience and reducing agency workload.

- •Sustainability and ethical debt collection practices gain prominence, with agencies emphasizing regulatory compliance and transparent communication to maintain brand reputation.

- •Integration of omnichannel communication including SMS, email, and voice calls ensures more flexible and debtor-friendly contact strategies, increasing responsiveness.

- •Increased use of blockchain technology for secure data sharing and transaction tracking enhances transparency and trust in debt recovery processes.

- •Collaborative ecosystems among creditors, collection agencies, and technology providers foster innovation and streamlined operations across the value chain.

- •Focus on data privacy and cybersecurity strengthens as regulatory bodies impose stricter guidelines, prompting investments in secure IT infrastructure.

Market Opportunities

- •Emerging markets present vast untapped potential due to increasing credit penetration and rising debt levels, creating opportunities for market entrants and expansion of existing players.

- •Investment in AI and automation technologies offers opportunities to develop innovative, cost-effective solutions that improve collection outcomes and customer satisfaction.

- •Expansion of services into niche sectors such as healthcare and government debt collection allows firms to diversify revenue streams and specialize in high-demand areas.

- •Strategic partnerships between traditional collection agencies and fintech companies facilitate development of integrated platforms, enhancing market reach and service capabilities.

- •Regulatory changes encouraging transparent and ethical debt collection practices create openings for compliant service providers to differentiate and capture market share.

- •Development of omnichannel and self-service digital platforms enables debt collectors to engage customers effectively, improving recovery rates and operational efficiency.

- •Growing demand for data analytics and credit risk management services opens avenues for value-added offerings beyond traditional collection activities.

Market Challenges

- •Stringent regulatory environments across multiple jurisdictions impose compliance burdens and operational constraints on debt collection agencies, impacting profitability and agility.

- •High competition and market fragmentation lead to pricing pressures and require continuous innovation to maintain competitive advantage and client retention.

- •Consumer resistance and negative perceptions of debt collection practices challenge agencies to balance effective recovery with maintaining customer relationships and brand reputation.

- •Data privacy concerns and cybersecurity risks necessitate significant investments in secure infrastructure and protocols to safeguard sensitive debtor information.

- •Rapid technological change demands continuous upskilling and capital expenditure for agencies to stay current and competitive in the market.

- •Legal complexities and varying enforcement mechanisms across countries complicate cross-border debt collection activities and limit global scalability.

- •Economic downturns and unforeseen events, such as pandemics, can increase default rates but simultaneously reduce the ability of debtors to repay, impacting collection success.

Regulatory Framework

- •Between 2019 and 2024, key regulations such as the EU’s General Data Protection Regulation (GDPR) and the U.S. Fair Debt Collection Practices Act (FDCPA) enforcement have tightened compliance requirements, mandating transparent and ethical collection procedures. These regulations enforce data privacy, restrict abusive collection tactics, and require clear communication with debtors, significantly influencing market practices.

- •Regulators have introduced enforcement mechanisms including higher penalties, mandatory licensing of collection agencies, and consumer complaint redressal systems to ensure adherence and protect debtor rights. These mechanisms affect operational costs and necessitate robust compliance frameworks within agencies.

- •Safety standards for electronic communications and data handling have been established, addressing cybersecurity and fraud prevention, thereby shaping technology investments and operational protocols in the market.

- •Country-specific mandates require localized compliance, such as the U.K.’s Financial Conduct Authority (FCA) regulations and Australia’s Australian Competition and Consumer Commission (ACCC) guidelines, each with unique timelines and operational impacts for market participants.

- •Government initiatives promoting financial literacy and responsible lending indirectly affect debt collection by influencing borrower behavior and delinquency rates, providing a proactive approach to market stability.

Market Intelligence

- •15th January 2025, Encore Capital Group launched an AI-driven debt collection platform integrating predictive analytics and automated communication channels to enhance recovery efficiency and reduce operational costs. The platform targets financial institutions globally, offering advanced debtor segmentation and real-time reporting to improve decision-making and compliance adherence. This innovation positions Encore as a technology leader in the debt collection services market, driving competitive advantage through enhanced service delivery and client satisfaction. The launch reflects broader industry trends towards digital transformation and automation.

- •20th March 2025, Intrum AB announced a strategic partnership with a leading fintech firm to develop blockchain-based secure data exchange solutions for debt collection processes. This initiative aims to improve transparency, reduce fraud risk, and streamline cross-border debt recovery operations. The collaboration enhances Intrum’s technological capabilities and aligns with increasing regulatory demands for data security and consumer protection. It is expected to set new industry standards and open new market opportunities, particularly in the Asia-Pacific region.

- •5th June 2025, PRA Group completed the acquisition of a regional debt purchasing firm specializing in healthcare receivables. This move expands PRA’s portfolio and geographic footprint, allowing deeper penetration into the growing healthcare debt segment. The acquisition strengthens PRA’s position in key markets and provides access to proprietary data analytics tools, enhancing collection strategies. The deal underscores the ongoing consolidation trend within the debt collection services market aimed at achieving scale and operational synergies.

- •12th September 2025, Transworld Systems Inc. launched a cloud-based digital self-service portal enabling consumers to manage and settle debts online with flexible payment options. The platform incorporates AI chatbots for personalized support and complies with evolving regulatory standards for fair debt collection. This digital initiative improves customer engagement and reduces agency workload, enhancing overall recovery rates. It represents Transworld’s commitment to innovation and customer-centric service models in the competitive debt collection market.

- •Source: Official press releases and company websites

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45.7 Billion |

| Forecast Year Market Size | USD 98.3 Billion |

| CAGR | 8.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.8% |

| Scope of Report | Market is segmented by Product Type (In-house Collection Services, Third-party Collection Agencies, Debt Purchase Services, Legal Collection Services, Early-stage Collection Services), Application (Consumer Debt Collection, Commercial Debt Collection, Healthcare Debt Collection, Government Debt Collection, Utility Debt Collection), End-Use Industry (Banking & Financial Services, Healthcare, Government & Public Sector, Utilities & Telecom), Distribution Channel (Direct Collection, Outsourced Collection, Digital Collection Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Encore Capital Group (United States), Intrum AB (Sweden), PRA Group (United States), Transworld Systems Inc. (United States), Hoist Finance AB (Sweden) |

Global Debt Collection Services Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.