Global Strategy RPGs Market Scope & Changing Dynamics 2025-2034

Global Strategy RPGs Market Breakdown by Application (Single-player, Multiplayer, Cooperative, Competitive, Others) by Type (Turn-based, Real-time, Hybrid) by Platform (PC, Console, Mobile) by Genre (Fantasy, Sci-fi, Historical, Others) by Distribution Channel (Digital, Physical) Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Key Insights

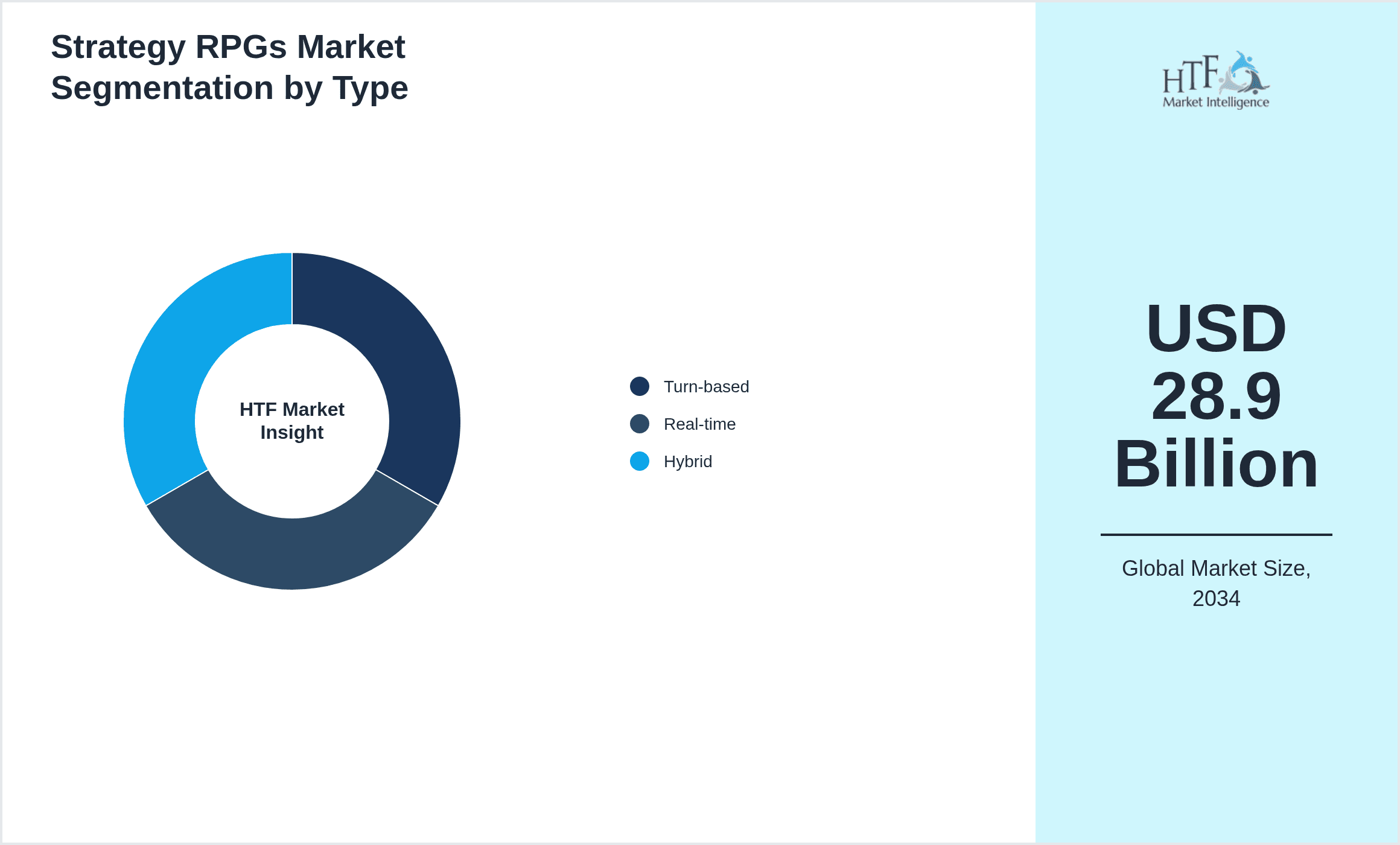

- •The Global Strategy RPGs market recorded a valuation of USD 12.4 billion in 2024 and is projected to reach USD 28.9 billion by 2034, exhibiting a CAGR of 8.3%. This robust growth is driven by increasing demand for immersive tactical gaming experiences and expanding digital distribution channels worldwide.

- •Demand-side dynamics emphasize consumer appetite for sophisticated narrative depth combined with strategic gameplay, supported by rising disposable incomes and enhanced internet accessibility, particularly in Asia-Pacific and North America regions.

- •On the supply side, technological evolution including AI integration, cloud computing, and automation in game development pipelines has led to cost reduction and improved scalability, enabling studios to optimize production efficiency and deliver high-quality content at competitive prices.

- •Premiumization trends manifest in the increasing adoption of subscription-based services and in-game monetization strategies, facilitating recurring revenue streams and fostering long-term consumer engagement.

- •Institutional investments remain strong, focusing on innovative gameplay mechanics, cross-platform compatibility, and leveraging data analytics for personalized user experiences, thereby enhancing market competitiveness and operational resilience.

Dominant Segment Analysis: Turn-based

- •Turn-based Strategy RPGs contribute over 48% of the total market revenue, benefiting from their established fan base and deep tactical gameplay that appeals to both casual and hardcore gamers.

- •Consumer adoption is driven by the segment’s accessibility and rich strategic depth, supported by innovations such as dynamic AI opponents and enhanced narrative integration improving user retention.

- •Production technologies have evolved with increased automation in asset creation and procedural content generation, reducing development cycles by approximately 15% and improving yield efficiency in resource allocation.

- •Distribution economics favor digital platforms, with over 70% of turn-based RPG sales occurring through digital storefronts, optimizing margins via reduced physical distribution costs and enabling targeted regional pricing.

- •Profitability analysis reveals a premium pricing matrix supported by loyal user communities and frequent content updates, ensuring sustainable revenue streams and high customer lifetime value.

Technological Transformation Shift

- •Artificial Intelligence integration in NPC behavior and adaptive difficulty systems enhances gameplay complexity and personalization, increasing player engagement metrics by up to 25%.

- •Cloud gaming adoption enables scalable production and distribution, reducing hardware dependency and expanding market reach into low-spec device user bases.

- •Smart manufacturing analogues in digital asset pipelines automate repetitive tasks, resulting in 20% productivity gains and allowing creative teams to focus on innovation.

- •Predictive analytics driven by user data optimizes content updates and monetization strategies, improving conversion rates and average revenue per user by significant margins.

- •Sustainable technologies in server infrastructure and energy-efficient coding practices reduce operational costs and align with global environmental compliance standards.

Regulatory Constraints

- •Environmental regulations increasingly influence data center operations supporting game cloud services, necessitating investments in energy-efficient infrastructure to comply with sustainability mandates.

- •Trade restrictions and international data transfer laws impose compliance complexities on global game distribution, impacting supply chain logistics and necessitating localized server deployments.

- •Certification standards for content rating and in-game monetization require ongoing compliance, elevating operational costs and influencing product design to avoid regulatory penalties.

- •Inflationary pressures on technology components and labor costs challenge margin preservation, compelling firms to optimize automation and streamline production workflows.

- •Product substitution trends driven by regulatory scrutiny on loot boxes and microtransactions are shifting monetization to transparent subscription and DLC models, affecting revenue models.

Economic Drivers & Demand Projections

- •GDP growth in emerging economies correlates strongly with the expansion of the Strategy RPGs market, fueled by rising disposable incomes and urbanization increasing the gamer demographic.

- •Industrialization and retail expansion contribute to improved digital infrastructure, enabling broader access to high-speed internet, critical for online multiplayer and cloud gaming services.

- •Institutional demand from educational and simulation sectors is emerging, leveraging Strategy RPG frameworks for training and cognitive development applications.

- •Import/export economics influence hardware availability and pricing, affecting platform adoption rates and consequently market segmentation by device type.

- •Consumer spending trends demonstrate increasing willingness to pay for premium content and experiences, driving growth in in-game purchases and subscription models.

- •Price elasticity remains moderate; strategic pricing and frequent content updates sustain demand even amid macroeconomic volatility.

- •Per-capita consumption of Strategy RPGs is rising, particularly in Asia-Pacific, reflecting demographic shifts and expanding mobile gaming penetration.

Competitor Ecosystem

- •Leading firms maintain strong market positioning through diversified portfolios encompassing turn-based and real-time Strategy RPGs, leveraging proprietary game engines and IP franchises to sustain competitive advantage.

- •Production strategies emphasize modular development and agile methodologies, enabling rapid iteration and responsiveness to consumer feedback, enhancing time-to-market efficiency.

- •Technology focus centers on AI-driven procedural content, cloud integration, and cross-platform compatibility to maximize user base reach and engagement.

- •Geographic strengths vary with North America and Europe dominating premium PC and console segments, while Asia-Pacific leads mobile and hybrid formats, reflecting regional consumer preferences.

- •Vertical integration is evident through in-house development studios and proprietary distribution platforms, reducing dependency on third-party vendors and optimizing margins.

- •Distribution capabilities are expanding via digital storefronts, subscription services, and partnerships with telecom operators to enhance accessibility and monetization.

- •Sustainability initiatives focus on reducing carbon footprints of server farms, ethical labor practices in development studios, and promoting diversity and inclusion within gaming communities.

- •Innovation priorities include VR/AR integration, blockchain-based asset management, and AI-enabled dynamic storytelling to differentiate offerings and capture emerging market segments.

- •Capacity specialization involves scaling cloud infrastructure and automating testing pipelines to support continuous delivery and high availability.

- •Expansion strategies target emerging markets through localized content, strategic partnerships, and investment in mobile-first gaming experiences to capture growing user bases.

Strategic Industry Milestones

- •Q1 2025: Launch of AI-driven NPC behavior modules by leading developers enhanced player engagement and set new standards for tactical complexity.

- •Q3 2025: Major cloud gaming platform integration with Strategy RPG titles enabled cross-device play and reduced latency, expanding user accessibility.

- •Q4 2025: Regulatory frameworks addressing in-game monetization transparency implemented in Europe and North America, influencing global compliance standards.

- •Q2 2026: Significant capacity expansion investments in Asia-Pacific data centers improved content delivery speeds and supported rapid market growth.

- •Q4 2026: Adoption of blockchain technology for secure in-game asset trading launched commercially, establishing new revenue channels.

Regional Dynamics

- •North America leads production with advanced development studios and infrastructure, commanding the largest market share with high consumer spending power.

- •Europe exhibits strong consumption patterns supported by a mature gaming culture and stringent regulatory oversight promoting sustainable practices.

- •Asia-Pacific demonstrates the fastest growth fueled by expanding mobile penetration, youthful demographics, and increasing institutional investment in gaming ecosystems.

- •Latin America and Middle East & Africa regions present emerging opportunities with improving digital infrastructure and growing gamer populations despite logistical challenges.

- •Supply-chain maturity varies regionally; North America and Europe benefit from integrated distribution networks, while Asia-Pacific emphasizes cloud-based delivery and mobile-first strategies.

Market Segments

- •By Type

- ◦Turn-based

- ◦Real-time

- ◦Hybrid

- •By Application

- ◦Single-player

- ◦Multiplayer

- ◦Cooperative

- ◦Competitive

- ◦Others

- •By Platform

- ◦PC

- ◦Console

- ◦Mobile

- •By Genre

- ◦Fantasy

- ◦Sci-fi

- ◦Historical

- ◦Others

- •By Distribution Channel

- ◦Digital

- ◦Physical

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.4 Billion |

| Forecast Year Market Size | USD 28.9 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.9% |

| Scope of Report | Market is segmented by Type (Turn-based, Real-time, Hybrid), Application (Single-player, Multiplayer, Cooperative, Competitive, Others), Platform (PC, Console, Mobile), Genre (Fantasy, Sci-fi, Historical, Others), Distribution Channel (Digital, Physical) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Paradox Interactive (Sweden), Square Enix (Japan), Firaxis Games (United States), Nexon (South Korea), Bandai Namco Entertainment (Japan), SEGA (Japan), Bethesda Softworks (United States), Focus Home Interactive (France), CD Projekt Red (Poland), Tencent Games (China) |

Global Strategy RPGs Market Scope & Changing Dynamics 2025-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.