Global Industrial Vacuums Market Size, Growth & Revenue 2024-2034

Global Industrial Vacuums Market is segmented by Product Type (Wet Industrial Vacuums, Dry Industrial Vacuums, Combination Industrial Vacuums, Pneumatic Industrial Vacuums, Portable Industrial Vacuums), Application (Dust Collection, Liquid Recovery, Material Handling, Environmental Cleanup, Maintenance), End-Use Industry (Manufacturing, Pharmaceutical, Food & Beverage, Chemical & Petrochemical), Distribution Channel (Direct Sales, Distributors & Dealers, Online Retail), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

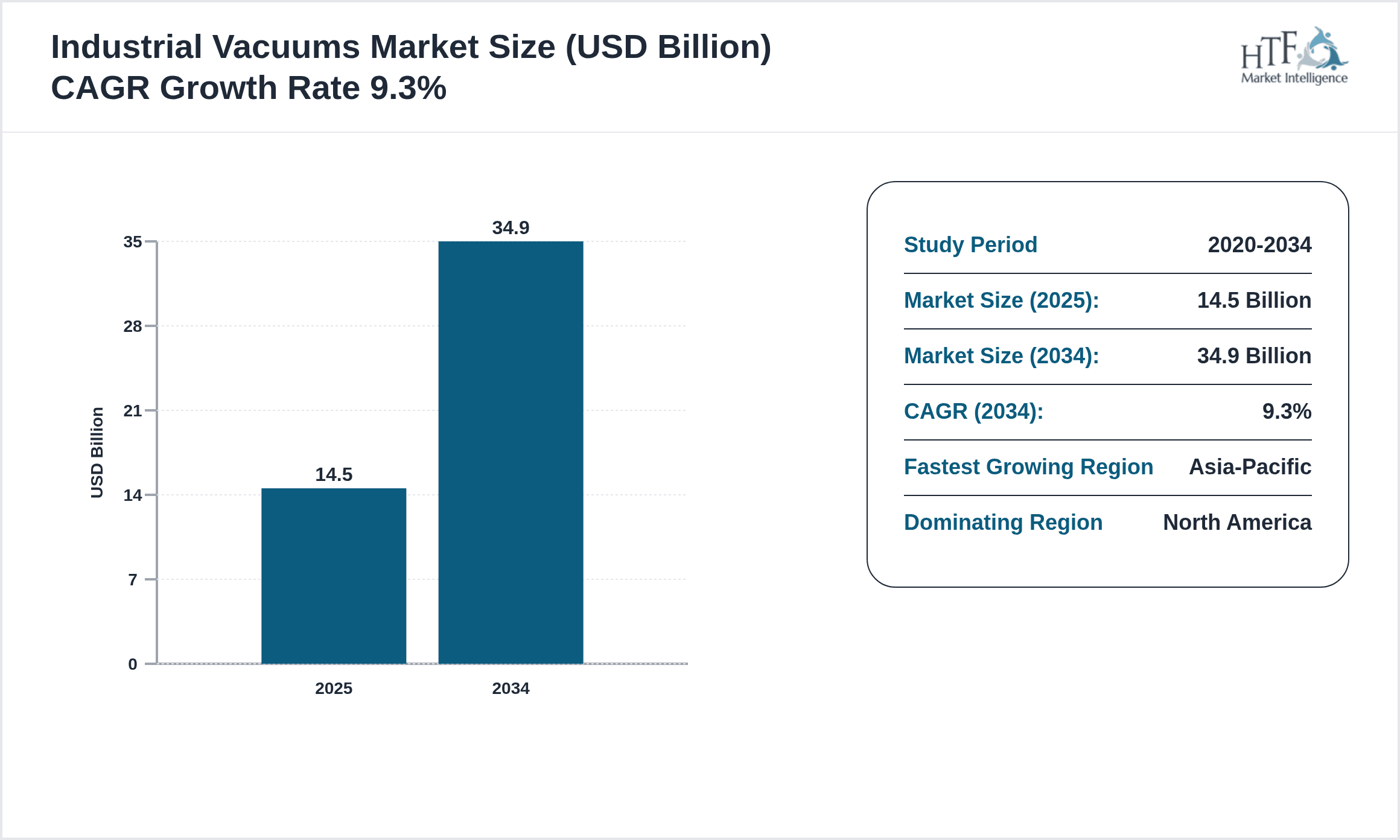

- •The Global Industrial Vacuums Market encompasses a broad range of vacuum technologies tailored for industrial environments, addressing critical needs such as dust collection, liquid recovery, and material handling. These systems are vital for maintaining clean and safe workspaces in sectors like manufacturing, pharmaceuticals, food processing, and environmental services. The market includes wet, dry, combination, pneumatic, and portable vacuum systems, each offering unique benefits aligned with specific industrial applications. Over the forecast period, the market is projected to witness robust growth driven by increasing industrialization, stringent environmental regulations, and rising demand for automation in cleaning operations. Asia-Pacific is emerging as the fastest growing region due to rapid industrial expansion and infrastructure development. North America currently dominates the market owing to advanced manufacturing facilities and high adoption of technologically advanced vacuum solutions. The growing emphasis on workplace safety and environmental sustainability further propels the demand for efficient industrial vacuum systems worldwide. This market report provides an in-depth analysis of segmentation, competitive landscape, growth drivers, challenges, and emerging opportunities, offering strategic insights for stakeholders across the value chain.

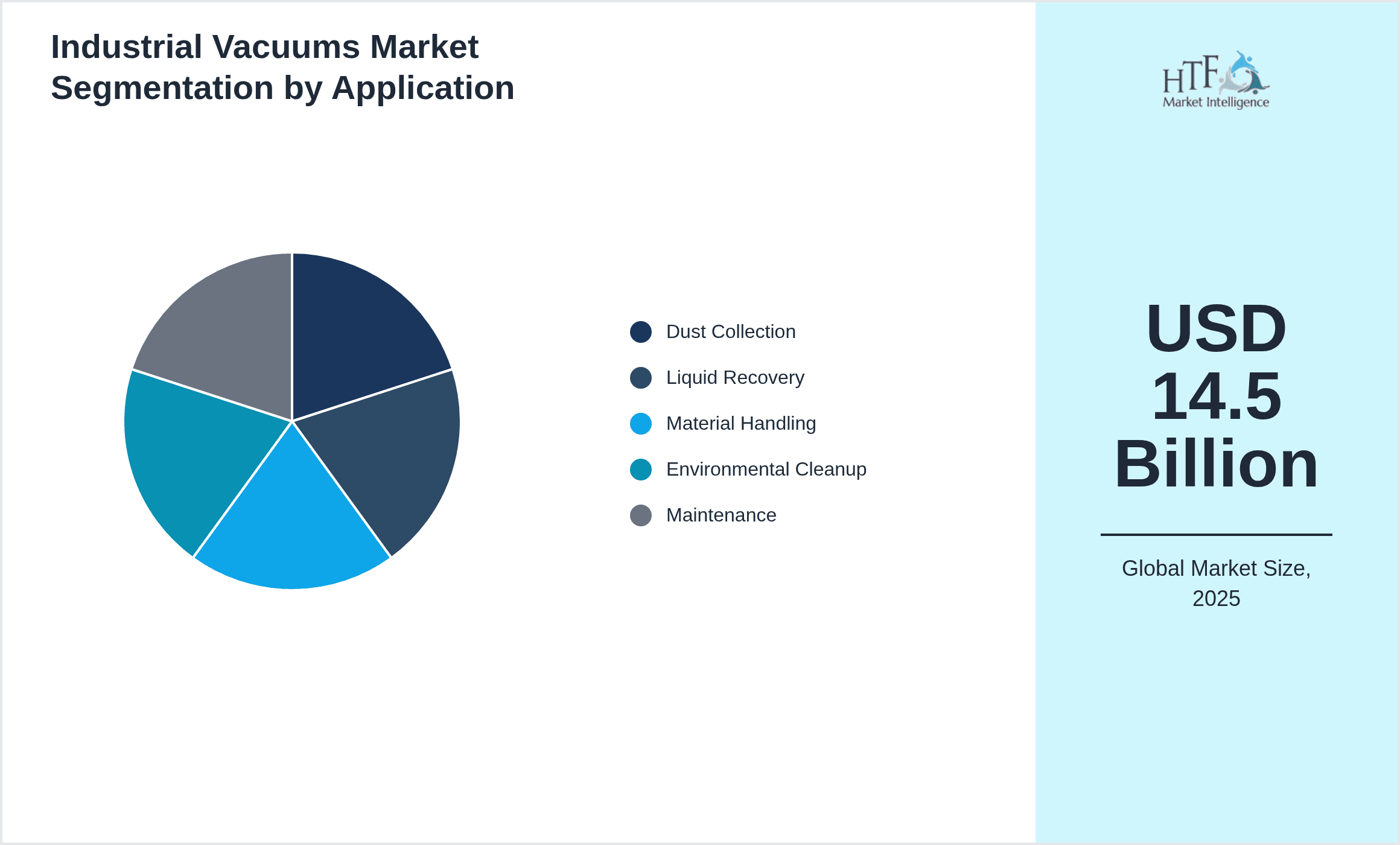

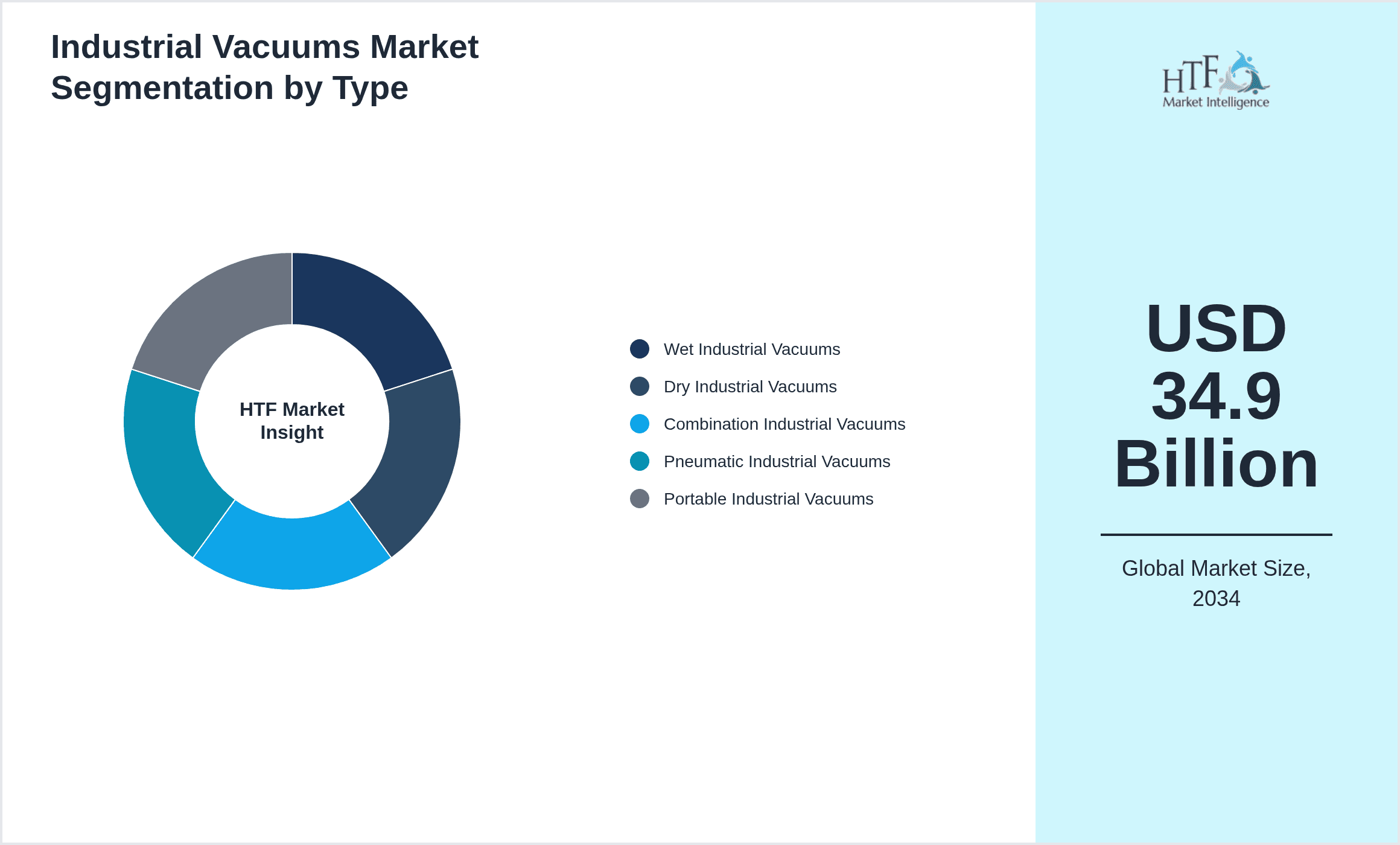

- •Key highlights of the Global Industrial Vacuums Market include a base market valuation of USD 14.5 Billion in 2024 with an anticipated growth to USD 34.9 Billion by 2034, reflecting a compound annual growth rate (CAGR) of 9.3%. Dry Industrial Vacuums currently lead the product segment, supported by their versatility and efficiency in diverse industrial settings. Combination Industrial Vacuums are identified as the fastest growing type segment due to their ability to handle both wet and dry substances, catering to the evolving demands of various industries. Dust Collection remains the dominating application segment, driven by stricter air quality norms and industrial safety mandates. North America holds the largest market share, leveraging mature industrial infrastructure and technological advancements. Asia-Pacific's rapid industrialization and expanding manufacturing base position it as the fastest growing region. The market also benefits from increasing investments in automation and smart vacuum technologies, which are reshaping operational efficiencies and cost-effectiveness across industries worldwide.

- •The Global Industrial Vacuums Market presents a significant value proposition by enhancing industrial cleanliness, operational safety, and environmental compliance. This market is strategically important for manufacturers, environmental service providers, and end-users requiring robust solutions for hazardous material handling and pollution control. Industrial vacuums contribute to minimizing workplace hazards, reducing downtime, and ensuring compliance with regulatory standards, thereby optimizing productivity and reducing operational costs. Stakeholders benefit from technological innovations such as IoT-enabled systems and energy-efficient designs that improve monitoring and maintenance. Furthermore, the market’s expansion aligns with global sustainability goals, promoting eco-friendly industrial practices. The increasing focus on health and safety standards alongside digital transformation initiatives creates ample opportunities for market players to innovate and capture emerging segments. This comprehensive market analysis equips investors, manufacturers, and policy makers with actionable intelligence to navigate competitive dynamics and capitalize on growth trends.

Competitive Landscape

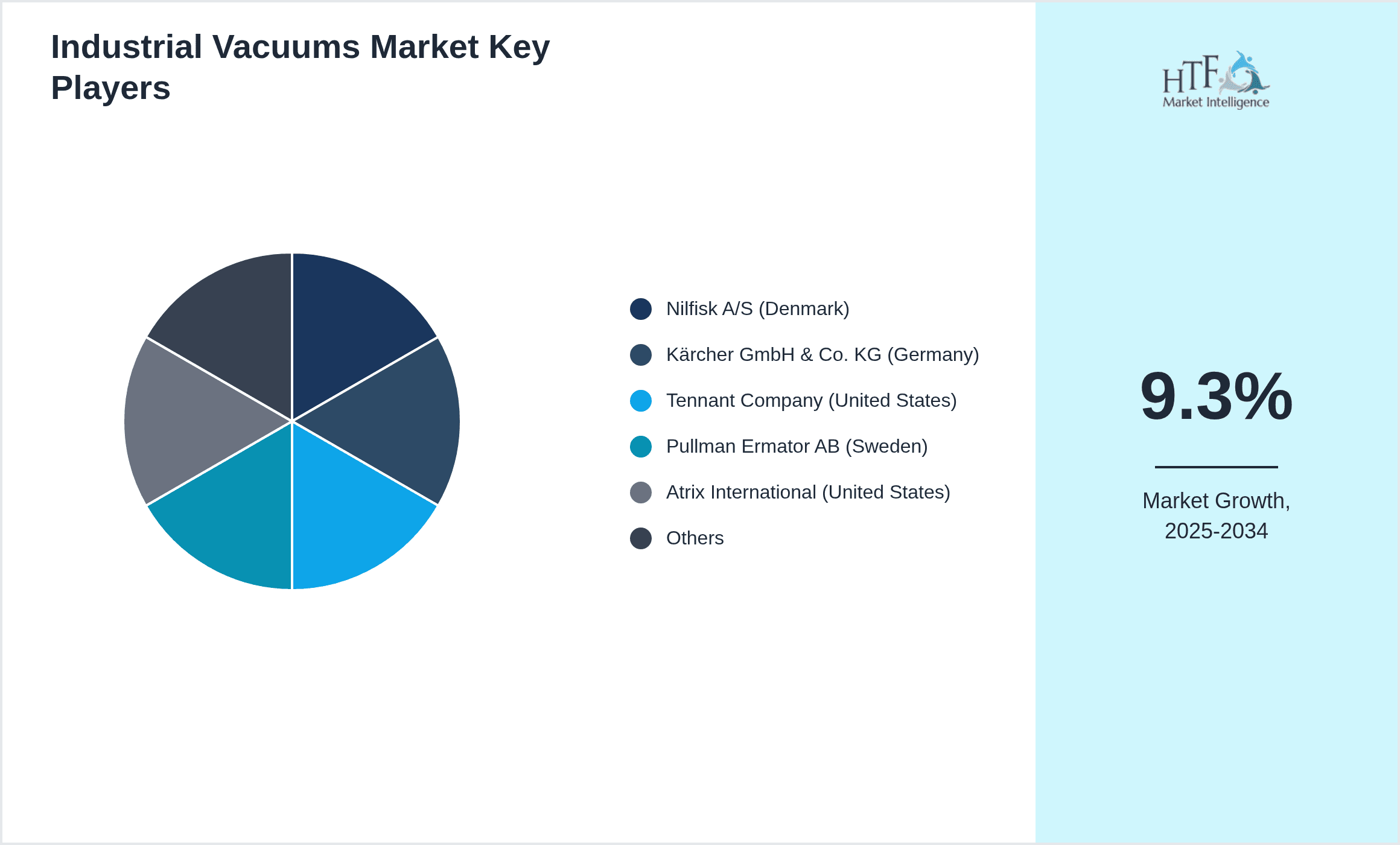

The competitive landscape of the Global Industrial Vacuums Market is characterized by intense rivalry among established multinational corporations and emerging regional players. Market leaders focus on continuous innovation, expanding product portfolios, and strategic partnerships to enhance their market positioning. Emphasis on research and development enables companies to introduce advanced vacuum systems featuring smart technologies, energy efficiency, and compliance with stringent environmental regulations. Competitive strategies include mergers and acquisitions, geographic expansion, and diversification into adjacent industrial cleaning solutions to capture larger market shares. Pricing strategies are balanced with value-added features to maintain profitability while addressing diverse customer needs. Distribution channel optimization and after-sales services are critical for sustaining customer loyalty and differentiating offerings. Regional competition varies, with North America exhibiting mature competitive dynamics and Asia-Pacific showcasing rapidly evolving market entrants. Future trends indicate a shift toward integrated vacuum solutions that combine automation and IoT connectivity, intensifying competition and innovation cycles. Overall, the market's competitive environment drives technological advancements, improved product quality, and enhanced customer engagement.

Companies Shaping the Industrial Vacuums Market

- •Nilfisk A/S (Denmark)

- •Kärcher GmbH & Co. KG (Germany)

- •Tennant Company (United States)

- •Pullman Ermator AB (Sweden)

- •Atrix International (United States)

- •Bosch Industriekraftfahrzeuge GmbH (Germany)

- •MAKITA Corporation (Japan)

- •Gardner Denver Holdings, Inc. (United States)

- •Hako GmbH (Germany)

- •Numatic International Limited (United Kingdom)

- •Ruwac Industriesauger GmbH (Germany)

- •Advance Vacuum Systems, Inc. (United States)

- •Lavorwash Group S.p.A. (Italy)

- •PowerBoss LLC (United States)

- •Pullman-Holt Corporation (United States)

- •Industrias Cleantech S.A. de C.V. (Mexico)

- •Royal Vacuum Company (United States)

- •Sotecma S.L. (Spain)

- •Thomas GmbH (Germany)

- •Nilfisk-Advance (Denmark)

- •Karcher North America (United States)

- •Bissell Homecare, Inc. (United States)

- •SharkNinja Operating LLC (United States)

- •Electrolux AB (Sweden)

- •Dustcontrol AB (Sweden)

Market Breakdown

- •By Product Type

- ◦Wet Industrial Vacuums

- ◦Dry Industrial Vacuums

- ◦Combination Industrial Vacuums

- ◦Pneumatic Industrial Vacuums

- ◦Portable Industrial Vacuums

- •By Application

- ◦Dust Collection

- ◦Liquid Recovery

- ◦Material Handling

- ◦Environmental Cleanup

- ◦Maintenance

- •By End-Use Industry

- ◦Manufacturing

- ◦Pharmaceutical

- ◦Food & Beverage

- ◦Chemical & Petrochemical

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Dealers

- ◦Online Retail

Growth Dynamics

The Global Industrial Vacuums Market is propelled by increasing industrialization and automation across manufacturing and processing sectors. Stringent environmental regulations mandating dust and pollutant control have compelled industries to invest in efficient vacuum systems. The rise in workplace safety awareness further drives adoption as businesses seek to minimize hazards related to dust, chemical spills, and contaminants. Technological advancements such as integration with IoT enable real-time monitoring and predictive maintenance, enhancing operational efficiencies. Additionally, growth in end-use industries like pharmaceuticals and food processing fuels demand for specialized vacuum solutions capable of handling sensitive materials while complying with hygiene standards. Investments in infrastructure development in emerging economies, especially within Asia-Pacific, create a robust market environment. The expanding e-commerce industry also supports growth through increased distribution channels, facilitating broader product accessibility. Collectively, these factors contribute to the steady expansion and dynamic evolution of the industrial vacuums market worldwide.

Market Trends

A significant trend in the industrial vacuums market is the adoption of smart vacuum systems equipped with IoT sensors and automation capabilities. These technologies allow for remote monitoring, predictive maintenance, and operational optimization, reducing downtime and costs. Another prevailing trend is the shift toward energy-efficient vacuum solutions that lower environmental impact and operational expenses, aligning with global sustainability objectives. The increasing integration of vacuum systems with robotics and automated cleaning workflows is revolutionizing industrial maintenance processes, particularly in manufacturing and chemical sectors. Additionally, modular and portable vacuum designs are gaining traction for their ease of use and versatility in varied applications. Companies are also focusing on developing eco-friendly materials and systems compliant with evolving regulations. Collaborative innovations and partnerships aimed at enhancing product capabilities and expanding geographical reach are shaping market dynamics and competitive positioning.

Market Opportunities

Emerging markets in Asia-Pacific and Latin America present substantial growth opportunities due to rapid industrialization and infrastructure development. There is increasing demand for specialized vacuum systems tailored to pharmaceutical and food industries, where hygiene and contamination control are critical. Integration of advanced technologies such as AI and IoT with industrial vacuums opens avenues for product differentiation and enhanced customer value. Expansion in e-commerce and online retail channels provides opportunities for direct consumer engagement and market penetration. Strategic partnerships and acquisitions focusing on innovation and geographic expansion also offer pathways to capitalize on untapped market segments. Furthermore, growing environmental concerns and regulatory pressures create demand for sustainable vacuum solutions, driving research and development investments. Companies that effectively address these facets while ensuring cost-effectiveness and operational efficiency are well-positioned to leverage future market potential.

Market Challenges

The Global Industrial Vacuums Market faces challenges including high initial investment costs for advanced vacuum systems, which may deter small and medium enterprises. Technical limitations related to system customization and integration with existing industrial processes can restrict adoption. Supply chain disruptions and raw material price volatility impact production costs and delivery timelines. Regulatory compliance across diverse international markets requires constant monitoring and adaptation, increasing operational complexity. Competition from low-cost regional manufacturers intensifies pricing pressures. Additionally, lack of awareness about advanced vacuum technologies in emerging economies limits market penetration. Maintenance and operational complexities, especially for high-capacity systems, pose logistical challenges. Addressing these issues requires strategic initiatives focusing on cost optimization, technology standardization, and customer education to sustain growth momentum in the global industrial vacuums market.

Regulatory Framework

Between 2019 and 2024, key regulatory developments affecting the Industrial Vacuums Market have included the enforcement of stricter air quality and workplace safety standards globally. Regulations such as OSHA’s updated dust control guidelines in North America mandate the implementation of high-efficiency vacuum systems to minimize airborne contaminants. The European Union’s REACH regulation enforces chemical safety compliance, impacting vacuum system materials and disposal methods. Environmental mandates in Asia-Pacific, including China’s Air Pollution Prevention and Control Action Plan, require industries to adopt advanced dust collection and liquid recovery technologies. Governments have introduced incentives and subsidies promoting energy-efficient and sustainable industrial equipment, indirectly boosting vacuum system adoption. These evolving regulatory landscapes necessitate continuous product innovation and compliance assurance from manufacturers, influencing market strategies and investment priorities worldwide.

Market Intelligence

- •15th January 2025, Nilfisk A/S launched its latest smart combination industrial vacuum featuring IoT-enabled sensors for real-time monitoring and predictive maintenance, targeting manufacturing and pharmaceutical sectors to enhance operational efficiency and compliance with environmental standards. This innovation positions Nilfisk as a leader in smart industrial cleaning solutions, responding to increasing demand for automation and data-driven asset management. Source: Official press release

- •22nd March 2025, Kärcher GmbH & Co. KG introduced a new energy-efficient dry industrial vacuum system designed to reduce power consumption by 25% while maintaining high suction performance, aligning with global sustainability goals and regulatory requirements in Europe and North America. The product launch underscores Kärcher’s commitment to eco-friendly industrial solutions and market expansion. Source: Company website

- •30th May 2024, Tennant Company announced a strategic partnership with a leading IoT technology provider to integrate advanced connectivity features into its industrial vacuums, enabling customers to leverage predictive analytics and remote diagnostics for improved equipment uptime and maintenance planning. This initiative enhances Tennant’s product portfolio with cutting-edge smart capabilities. Source: Industry publication

- •10th November 2024, Pullman Ermator AB completed the acquisition of a regional vacuum system distributor to strengthen its footprint in the Asia-Pacific market, facilitating broader access to emerging industrial sectors and accelerating growth in high-potential regions. The acquisition aligns with Pullman Ermator’s global expansion strategy and product diversification goals. Source: Company website

- •Source: Various official press releases and industry news sources

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 14.5 Billion |

| Forecast Year Market Size | USD 34.9 Billion |

| CAGR | 9.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9% |

| Scope of Report | Market is segmented by Product Type (Wet Industrial Vacuums, Dry Industrial Vacuums, Combination Industrial Vacuums, Pneumatic Industrial Vacuums, Portable Industrial Vacuums), Application (Dust Collection, Liquid Recovery, Material Handling, Environmental Cleanup, Maintenance), End-Use Industry (Manufacturing, Pharmaceutical, Food & Beverage, Chemical & Petrochemical), Distribution Channel (Direct Sales, Distributors & Dealers, Online Retail) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Nilfisk A/S (Denmark), Kärcher GmbH & Co. KG (Germany), Tennant Company (United States), Pullman Ermator AB (Sweden), Atrix International (United States), Bosch Industriekraftfahrzeuge GmbH (Germany), MAKITA Corporation (Japan), Gardner Denver Holdings, Inc. (United States), Hako GmbH (Germany), Numatic International Limited (United Kingdom), Ruwac Industriesauger GmbH (Germany), Advance Vacuum Systems, Inc. (United States), Lavorwash Group S.p.A. (Italy), PowerBoss LLC (United States), Pullman-Holt Corporation (United States), Industrias Cleantech S.A. de C.V. (Mexico), Royal Vacuum Company (United States), Sotecma S.L. (Spain), Thomas GmbH (Germany), Nilfisk-Advance (Denmark), Karcher North America (United States), Bissell Homecare, Inc. (United States), SharkNinja Operating LLC (United States), Electrolux AB (Sweden), Dustcontrol AB (Sweden) |

Global Industrial Vacuums Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.