Global Industrial Dust Collectors Market Size, Growth & Revenue 2024-2034

Global Industrial Dust Collectors Market is segmented by Product Type (Baghouse Collectors, Cartridge Collectors, Cyclone Collectors, Electrostatic Precipitators, Wet Scrubbers), Application (Metalworking, Pharmaceuticals, Food Processing, Chemicals, Cement), End-Use Industry (Automotive, Manufacturing, Construction, Mining), Distribution Channel (Direct Sales, Distributors, Online Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Industrial Dust Collectors market includes a broad range of dust collection systems designed to remove airborne particulate contaminants from industrial environments. These systems encompass technologies like baghouse collectors, cartridge collectors, cyclone collectors, electrostatic precipitators, and wet scrubbers. Their primary purpose is to enhance air quality, comply with environmental regulations, and safeguard worker health across applications such as metalworking, pharmaceuticals, food processing, chemical manufacturing, and cement production. The market covers both fixed and portable systems tailored for specific industrial needs. Increasing environmental awareness, strict emission norms, and the need for efficient dust management solutions have expanded the market significantly. This growth is further fueled by rapid industrialization in emerging economies, technological advancements in filtration systems, and an emphasis on sustainable manufacturing processes. Overall, the market reflects a dynamic interplay of innovation, regulation, and industrial demand driving the adoption of advanced dust collection technologies globally.

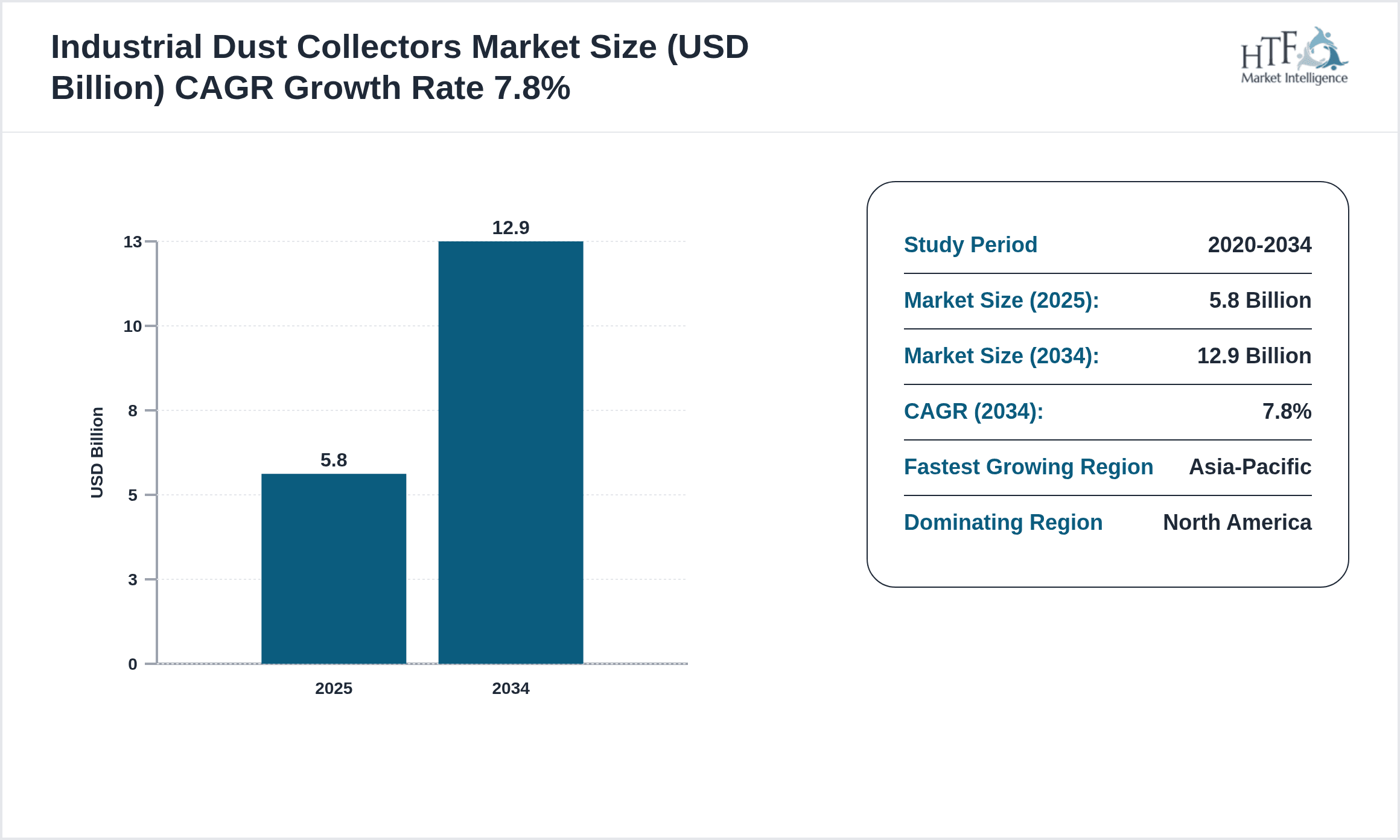

- •Key market highlights include a current valuation of USD 5.8 Billion in 2024, with projections to reach USD 12.9 Billion by 2034, representing a robust CAGR of 7.8%. The baghouse collectors segment dominates product types, while cartridge collectors exhibit the fastest growth due to their compact design and efficiency. Metalworking and pharmaceuticals emerge as leading applications, driven by stringent workplace safety regulations. North America holds the largest market share, supported by regulatory frameworks and industrial base, whereas Asia-Pacific is the fastest-growing region, propelled by rapid industrialization and infrastructure development. These trends underscore the market's expansion and evolving competitive landscape, emphasizing technology-driven innovation and regional growth dynamics.

- •The market offers strategic value to stakeholders including manufacturers, industrial end-users, and regulatory bodies. Industrial dust collectors enhance operational efficiency by reducing equipment wear and mitigating health risks associated with dust exposure. For manufacturers, innovation in filtration media and system design presents opportunities to capture emerging markets. Regulatory compliance is an essential driver, pushing industries towards adopting sustainable dust control solutions. Overall, the market’s growth trajectory reflects its critical role in advancing industrial hygiene standards, promoting environmental stewardship, and enabling industries to meet global emission targets, thus securing its importance across diverse industrial sectors worldwide.

Competitive Landscape

The competitive environment within the Global Industrial Dust Collectors market is characterized by intense rivalry among established multinational corporations and regional players. Market leaders focus heavily on innovation, developing advanced filtration technologies to improve efficiency and reduce operational costs. Strategic partnerships and mergers are prevalent to enhance market penetration and consolidate technological expertise. Companies differentiate through product customization, service quality, and compliance with stringent environmental standards. Pricing strategies are influenced by raw material costs and competitive pressure, while distribution networks are optimized to serve diverse industrial sectors globally. Barriers to entry include high capital investment and regulatory compliance requirements. The future competitive landscape is expected to evolve with digital integration and IoT-enabled dust collection solutions, fostering smarter and more sustainable operations.

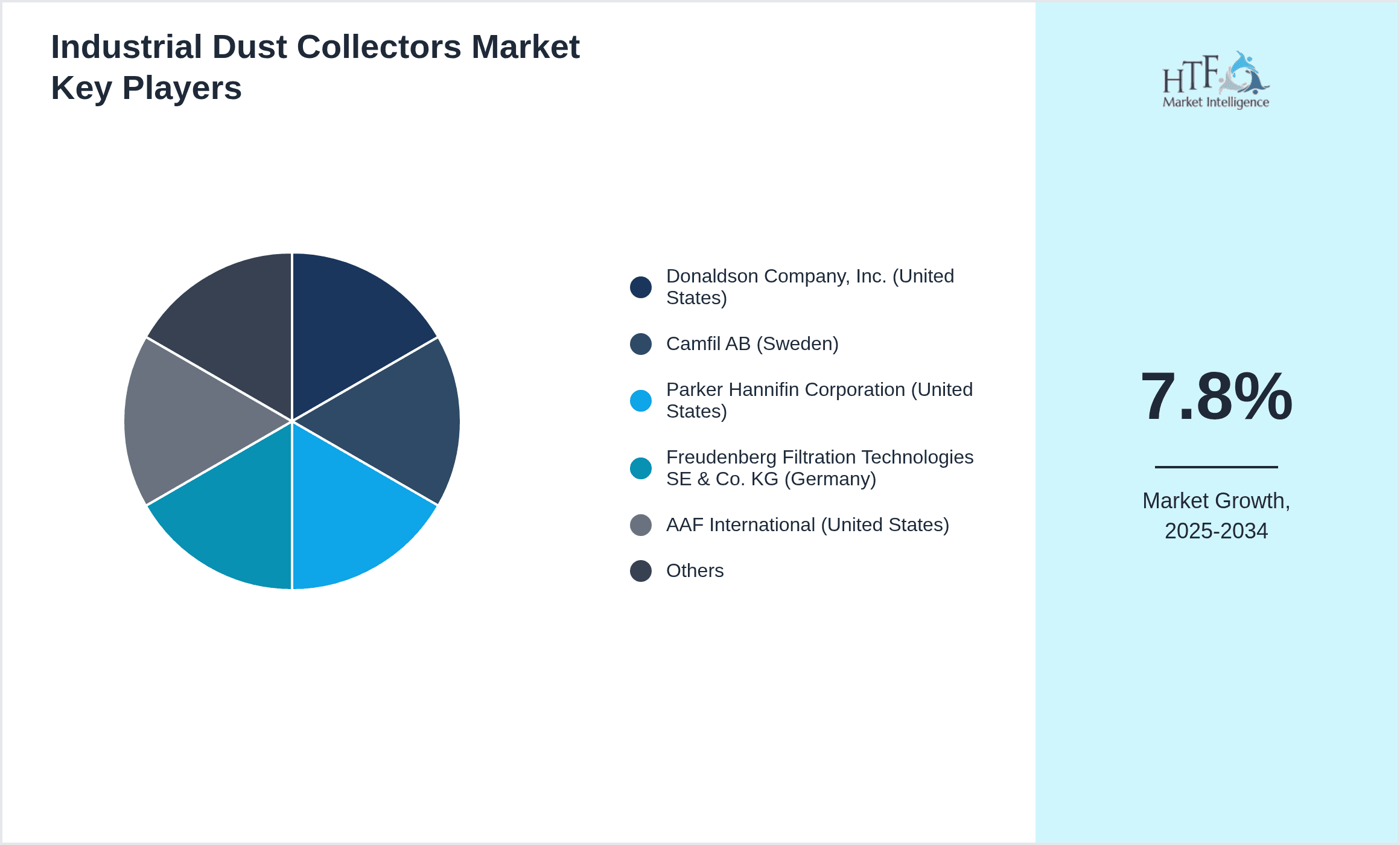

Leading Companies in Industrial Dust Collectors Market

- •Donaldson Company, Inc. (United States)

- •Camfil AB (Sweden)

- •Parker Hannifin Corporation (United States)

- •Freudenberg Filtration Technologies SE & Co. KG (Germany)

- •AAF International (United States)

- •MANN+HUMMEL GmbH (Germany)

- •Nederman Holding AB (Sweden)

- •Pentair plc (United States)

- •SPX FLOW, Inc. (United States)

- •Koch Filter Corporation (United States)

- •Eaton Corporation plc (Ireland)

- •Baker Hughes Company (United States)

- •Enviro Systems, Inc. (United States)

- •Sly Inc. (United States)

- •Hemi Filters (United States)

- •Industrial Air Technology (United States)

- •Air Innovations, Inc. (United States)

- •Filtermist International Ltd (United Kingdom)

- •Aerosol Filtration Solutions (United States)

- •Farr Company (United States)

- •Camfil APC (United States)

- •Donaldson Torit (United States)

- •Nederman Holding AB (Sweden)

- •Clarcor Industrial Air (United States)

- •Pulsa Industrial, Inc. (United States)

Market Breakdown

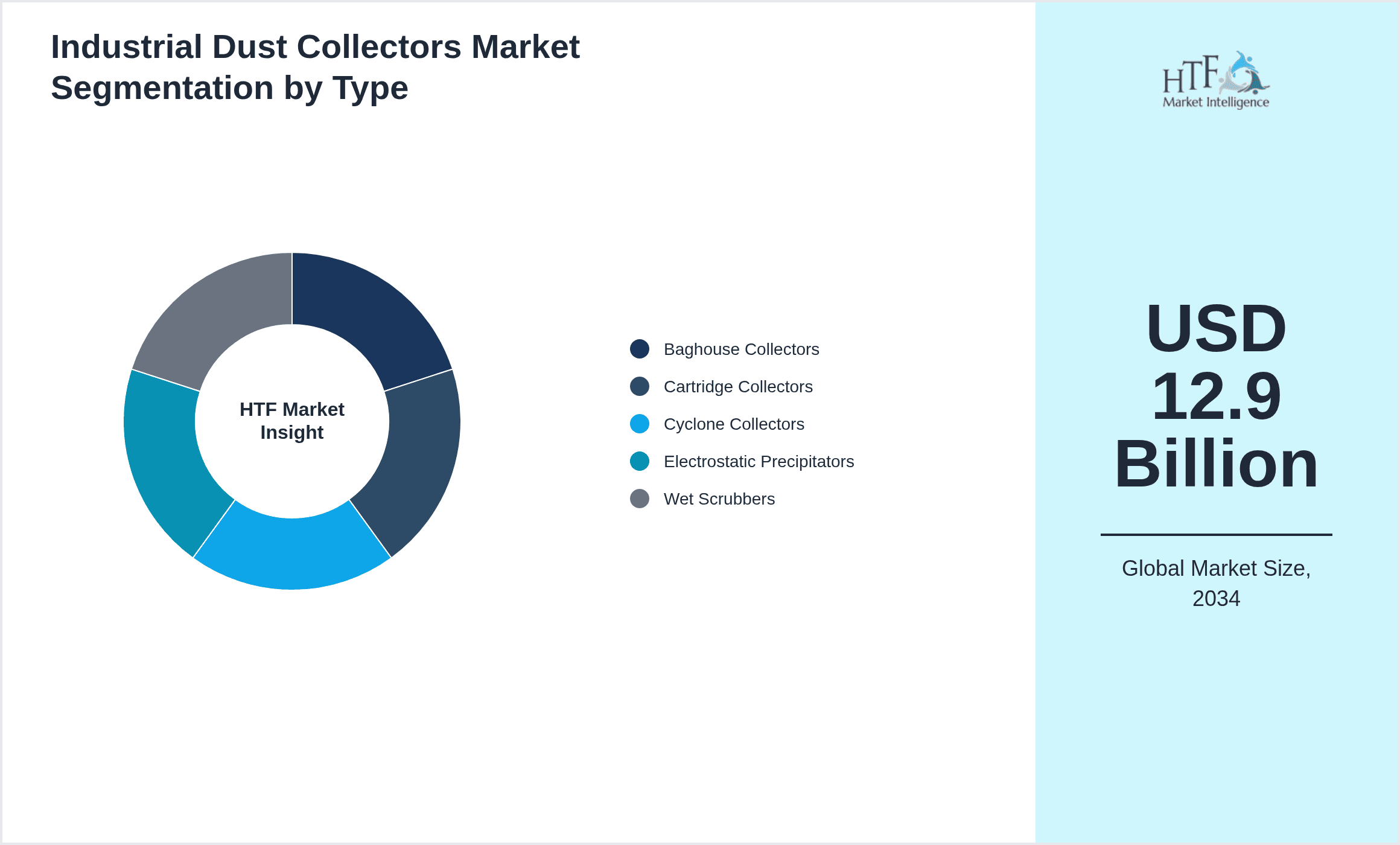

- •By Product Type

- ◦Baghouse Collectors

- ◦Cartridge Collectors

- ◦Cyclone Collectors

- ◦Electrostatic Precipitators

- ◦Wet Scrubbers

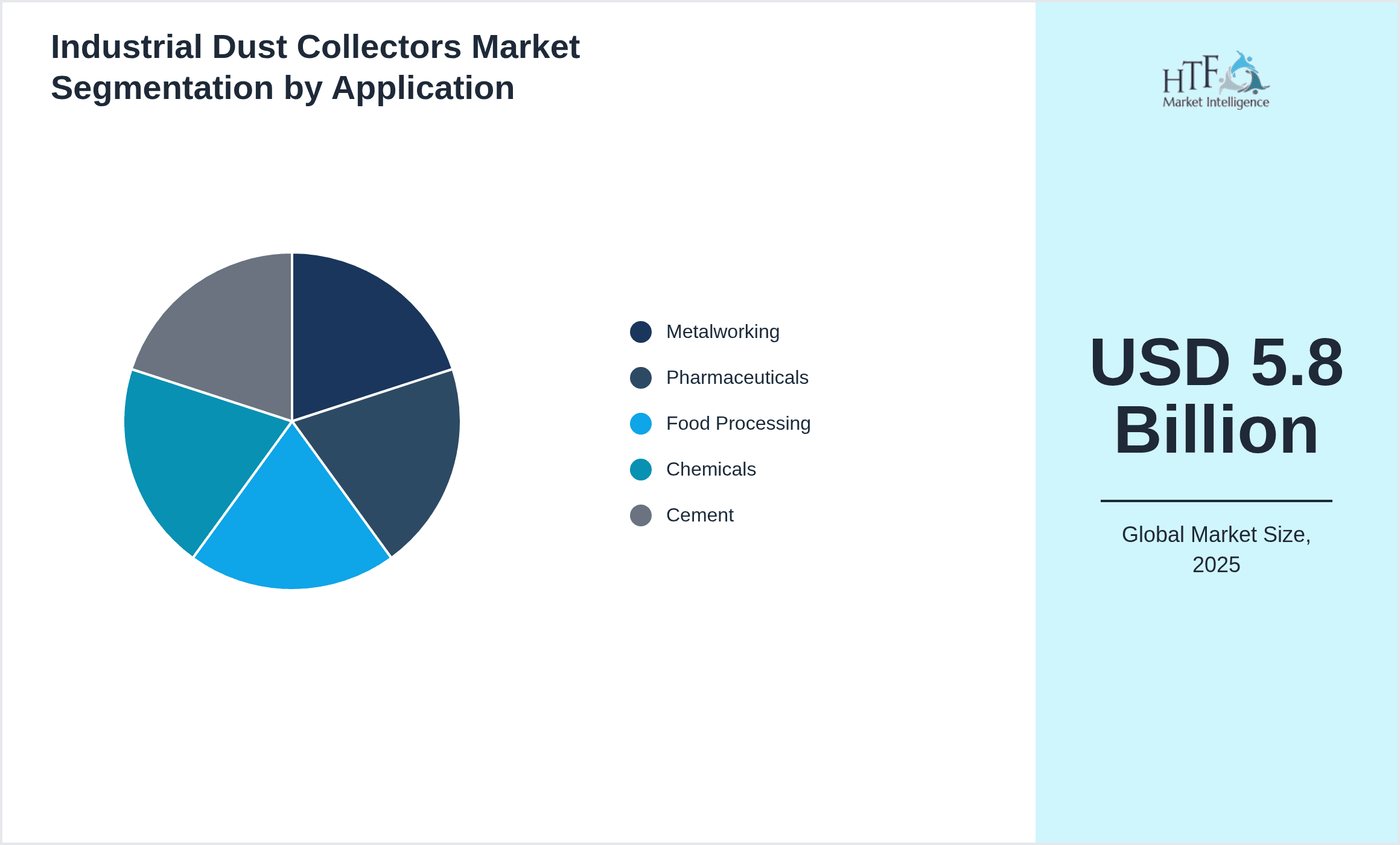

- •By Application

- ◦Metalworking

- ◦Pharmaceuticals

- ◦Food Processing

- ◦Chemicals

- ◦Cement

- •By End-Use Industry

- ◦Automotive

- ◦Manufacturing

- ◦Construction

- ◦Mining

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Sales

Growth Dynamics

- •The Global Industrial Dust Collectors market continues to expand, driven by rising industrial emissions regulations requiring efficient dust management solutions. For example, governments worldwide have tightened air quality standards, compelling industries to adopt advanced dust collection technologies that minimize particulate emissions and environmental impact.

- •Technological advancements such as enhanced filtration media and compact cartridge collectors have improved system efficiency and reduced maintenance needs, encouraging broader adoption across industries like pharmaceuticals and food processing, where contamination control is critical.

- •Rapid industrialization in Asia-Pacific has fueled demand for dust collectors, as countries invest in manufacturing and infrastructure development, increasing the need for compliant and cost-effective dust control systems to support sustainable growth.

- •Growing awareness of occupational health and safety has driven industries to prioritize dust control solutions, reducing workplace hazards and improving employee productivity, which in turn stimulates market growth globally.

- •Investments in smart dust collection technologies integrating IoT and automation enable real-time monitoring and predictive maintenance, enhancing system performance and lowering operational costs, which attracts industrial end-users focused on efficiency.

- •Increasing demand for customized dust collection solutions tailored to specific industrial applications supports market expansion, as companies seek systems optimized for their unique process requirements and environmental conditions.

- •Government incentives promoting sustainable manufacturing and pollution control encourage industries to upgrade existing dust collection infrastructure, further driving market penetration and revenue growth.

Market Trends

- •The market is witnessing a significant shift towards energy-efficient dust collectors that reduce power consumption while maintaining high filtration performance, aligning with sustainability goals of industrial operators.

- •There is growing adoption of modular and portable dust collection systems that offer flexibility and ease of installation, beneficial for small and medium-sized enterprises and temporary industrial setups.

- •Integration of IoT-enabled sensors in dust collectors allows real-time monitoring of particulate levels and system health, enabling predictive maintenance and minimizing downtime, thus enhancing operational reliability.

- •Manufacturers are increasingly utilizing advanced filtration materials such as nanofibers and PTFE membranes that improve dust capture efficiency and extend filter life, reducing replacement frequency and costs.

- •Collaborative initiatives between dust collector manufacturers and industrial end-users are fostering innovation in customized solutions that address specific environmental and process challenges unique to various sectors.

- •Rising demand for compliance with international environmental standards such as ISO and EPA regulations is shaping product development and market strategies, pushing companies to enhance dust collector capabilities.

- •Emerging digital platforms facilitate easier procurement and servicing of dust collection equipment, contributing to improved customer engagement and after-sales support in the global market.

Market Opportunities

- •Expansion into emerging markets, particularly in Asia-Pacific and Latin America, presents significant growth potential due to increasing industrial activities and evolving environmental regulations that mandate dust control solutions.

- •Development of next-generation filtration technologies incorporating sustainable and eco-friendly materials offers opportunities to capture environmentally conscious industrial sectors seeking green solutions.

- •Strategic partnerships and acquisitions can enable companies to broaden product portfolios and geographic reach, leveraging complementary technologies and market presence to accelerate growth.

- •Customization of dust collectors to meet industry-specific requirements, such as pharmaceutical-grade filtration or heavy-duty mining applications, can enhance market penetration and customer loyalty.

- •Integration of smart technologies like AI and machine learning for predictive analytics in dust collection systems can unlock value by improving operational efficiency and reducing maintenance costs.

- •Rising investments in infrastructure and urban development globally create new demand for dust control systems to maintain air quality and comply with strict environmental standards during construction activities.

- •Increasing awareness and regulatory focus on occupational health and safety provide a fertile ground for introducing advanced dust collector solutions that promote safer industrial workplaces.

Market Challenges

- •High initial capital expenditure for advanced dust collection systems can deter small and medium-sized enterprises from investing, limiting market growth potential in certain regions and industries.

- •Complexity in maintenance and filter replacement, especially for large-scale systems, poses operational challenges that may increase downtime and total cost of ownership for industrial users.

- •Stringent and varying regulatory frameworks across different countries create compliance challenges for manufacturers and end-users, affecting market standardization and product design.

- •Competition from low-cost, less efficient dust collection products in emerging markets can undermine adoption of premium, technologically advanced systems, impacting profitability for key players.

- •Supply chain disruptions and raw material price volatility, such as for specialized filtration media, can affect manufacturing costs and market pricing strategies.

- •Limited awareness and technical expertise among industrial operators regarding dust collection technologies can hinder market penetration and optimal system utilization.

- •Challenges in integrating dust collection systems with existing industrial infrastructure without affecting production processes can delay adoption and increase installation complexities.

Regulatory Framework

- •Between 2019 and 2024, the implementation of stricter air quality standards such as the revised National Ambient Air Quality Standards (NAAQS) in North America imposed rigorous particulate emission limits, compelling industries to upgrade dust collection systems to ensure compliance.

- •The European Union introduced the Industrial Emissions Directive updates during this period, emphasizing Best Available Techniques (BAT) for dust control, thereby influencing manufacturers to innovate low-emission, energy-efficient dust collectors.

- •China’s Ministry of Ecology and Environment enforced tighter regulations on industrial particulate emissions, including mandatory adoption of advanced dust filtration technologies in key manufacturing sectors, accelerating market growth in Asia-Pacific.

- •New safety standards for dust explosion prevention were enacted globally, requiring dust collectors to incorporate explosion venting and suppression systems, impacting design and manufacturing practices across the industry.

- •Government incentives and subsidies promoting sustainable industrial practices were introduced in various regions, facilitating investments in state-of-the-art dust collector installations and supporting market expansion.

Market Intelligence

- •15th February 2024, Donaldson Company, Inc. launched its new line of energy-efficient cartridge dust collectors designed for pharmaceutical manufacturing environments. These systems feature enhanced filtration media that reduce energy consumption by up to 25% while meeting stringent contamination control requirements. The launch aligns with growing industry demand for sustainable and compliant dust collection solutions, reinforcing Donaldson’s market leadership and innovation capabilities. Source: Donaldson Official Press Release

- •10th June 2024, Camfil AB introduced an IoT-enabled dust collector monitoring platform that provides real-time data analytics and predictive maintenance alerts. This innovation enhances operational reliability and minimizes downtime for metalworking and chemical processing industries, offering a competitive advantage in the market. The platform’s integration with existing systems facilitates seamless adoption and improved user experience. Source: Camfil Press Announcement

- •22nd September 2024, Parker Hannifin Corporation announced a strategic partnership with a leading filtration media manufacturer to co-develop next-generation nanofiber filter technology. This collaboration aims to improve dust capture efficiency and durability, targeting growth in the food processing and cement sectors. The initiative reflects industry trends towards advanced material innovation to meet evolving regulatory standards. Source: Parker Hannifin Corporate News

- •5th December 2024, Nederman Holding AB completed acquisition of a regional dust collector manufacturer to expand its product portfolio and strengthen presence in emerging markets. The deal is expected to accelerate growth by leveraging complementary technologies and distribution networks, enhancing Nederman’s competitive positioning globally. Source: Nederman Official Release

- •Source: Industry Reports, Company Websites, Market Publications

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 5.8 Billion |

| Forecast Year Market Size | USD 12.9 Billion |

| CAGR | 7.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.5% |

| Scope of Report | Market is segmented by Product Type (Baghouse Collectors, Cartridge Collectors, Cyclone Collectors, Electrostatic Precipitators, Wet Scrubbers), Application (Metalworking, Pharmaceuticals, Food Processing, Chemicals, Cement), End-Use Industry (Automotive, Manufacturing, Construction, Mining), Distribution Channel (Direct Sales, Distributors, Online Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Donaldson Company, Inc. (United States), Camfil AB (Sweden), Parker Hannifin Corporation (United States), Freudenberg Filtration Technologies SE & Co. KG (Germany), AAF International (United States), MANN+HUMMEL GmbH (Germany), Nederman Holding AB (Sweden), Pentair plc (United States), SPX FLOW, Inc. (United States), Koch Filter Corporation (United States), Eaton Corporation plc (Ireland), Baker Hughes Company (United States), Enviro Systems, Inc. (United States), Sly Inc. (United States), Hemi Filters (United States), Industrial Air Technology (United States), Air Innovations, Inc. (United States), Filtermist International Ltd (United Kingdom), Aerosol Filtration Solutions (United States), Farr Company (United States), Camfil APC (United States), Donaldson Torit (United States), Nederman Holding AB (Sweden), Clarcor Industrial Air (United States), Pulsa Industrial, Inc. (United States) |

Global Industrial Dust Collectors Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.