Global Commercial Cladding System Market Size, Growth & Revenue 2024-2034

Global Commercial Cladding System Market is segmented by Product Type (Metal Cladding, Composite Panels, Stone Cladding, Glass Cladding, Ceramic Cladding), Application (Office Buildings, Retail Complexes, Healthcare Facilities, Educational Institutions, Hospitality), End-Use Industry (Commercial Construction, Renovation & Refurbishment, Public Infrastructure, Industrial Facilities), Distribution Channel (Direct Sales, Distributors & Dealers, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

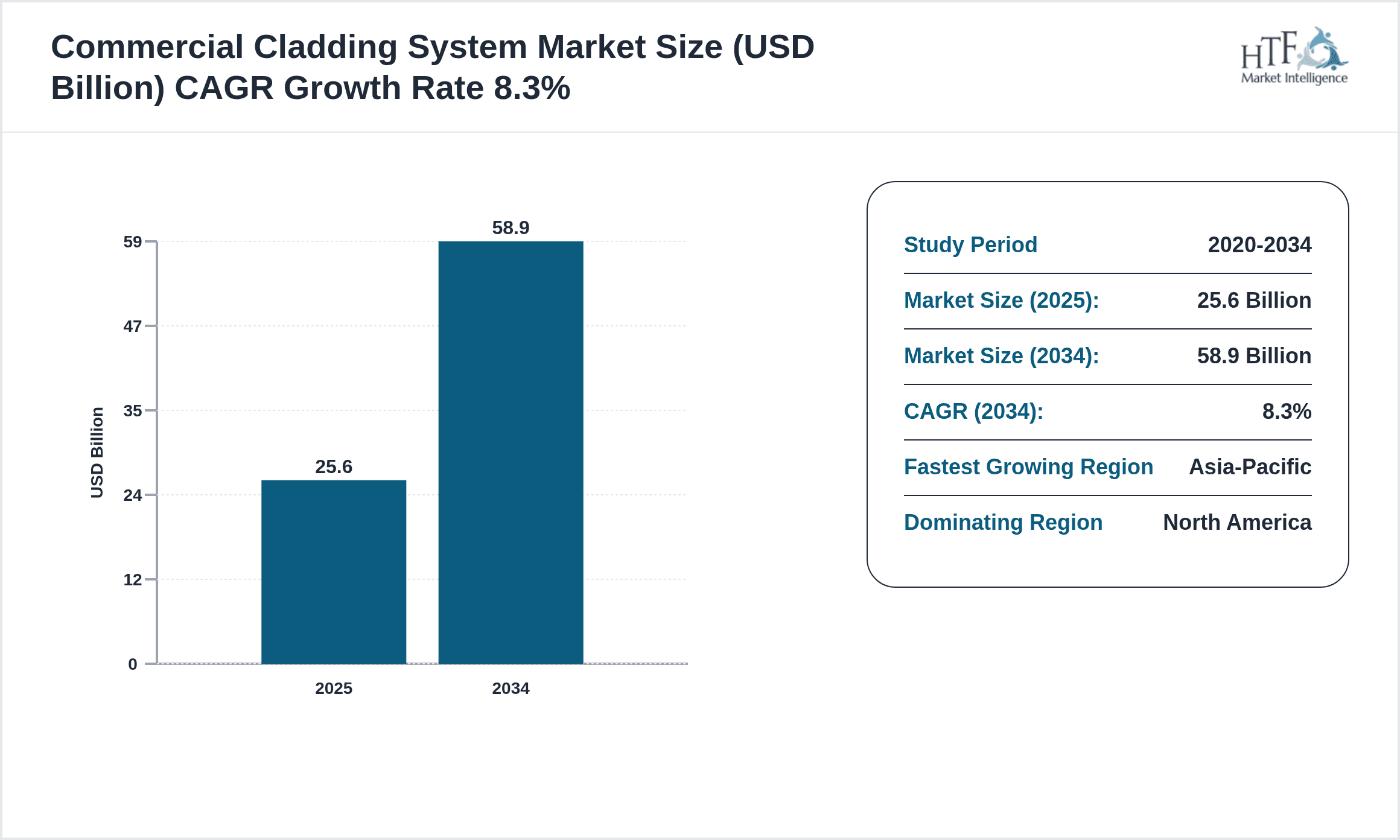

- •The Global Commercial Cladding System Market represents a critical segment within the construction industry focused on providing external facade solutions that combine functionality and design excellence for commercial infrastructures. This market includes a variety of cladding materials such as metal, composite panels, stone, glass, and ceramic that cater to diverse architectural demands and climatic conditions. Commercial cladding systems serve dual roles: enhancing building aesthetics and offering protection against environmental factors like moisture, UV radiation, and thermal variations. Driven by growing urbanization, rising demand for energy-efficient buildings, and increasing construction activities worldwide, the market spans multiple applications including office buildings, retail complexes, healthcare facilities, educational institutions, and hospitality sectors. Technological innovations have led to advanced cladding options that offer improved fire resistance, sustainability, and ease of installation, thereby broadening market scope and adoption. Regulatory policies emphasizing building safety and environmental compliance further shape market dynamics globally. Overall, the market is poised for steady growth driven by evolving architectural trends and infrastructural developments.

- •Significant market highlights include a 2024 base market size of USD 25.6 Billion projected to reach USD 58.9 Billion by 2034, registering a robust CAGR of 8.3%. The metal cladding segment currently dominates due to its durability and versatility, while composite panels are witnessing the fastest growth attributed to lightweight and sustainable properties. North America leads the market in size owing to stringent building codes and high construction expenditure, whereas Asia-Pacific emerges as the fastest growing region fueled by rapid urbanization and infrastructural investments. Growth is supported by technological advancements, increasing demand for energy-efficient facades, and rising renovation activities in mature markets. However, challenges such as high installation costs and regulatory complexities remain. Opportunities lie in expanding applications, material innovations, and emerging markets. These factors collectively contribute to a dynamic and evolving commercial cladding system industry worldwide.

- •The commercial cladding system market offers significant value propositions including enhanced building performance, superior aesthetic appeal, and compliance with global environmental standards. It enables architects and builders to meet sustainability goals by integrating energy-efficient materials and designs. For stakeholders such as manufacturers, contractors, and investors, the market presents strategic growth avenues through product innovation, geographic expansion, and partnerships. The increasing focus on green buildings and fire safety regulations amplifies the importance of advanced cladding solutions. Overall, the market is a critical enabler of modern commercial infrastructure development, balancing functionality with design and regulatory compliance to meet future urbanization demands.

Competitive Landscape

The competitive landscape of the global commercial cladding system market is characterized by intense rivalry among established multinational corporations and emerging regional players. Leading companies focus heavily on innovation, investing in R&D to develop fire-resistant, lightweight, and sustainable cladding materials that comply with evolving global regulations. Market participants employ diverse strategies including product differentiation, strategic partnerships, mergers and acquisitions, and geographic expansion to strengthen their market positions. Pricing strategies are competitive, balancing cost and quality to capture diverse customer segments across different regions. Distribution channel optimization and customer-centric service offerings further enhance competitiveness. Moreover, the market faces moderate entry barriers due to capital intensity and regulatory compliance requirements, although technological progress has lowered some access thresholds. Regional competition varies with North America and Europe emphasizing advanced product features, while Asia-Pacific focuses on affordability and volume growth. Future trends suggest increased collaboration within the value chain, digitalization in manufacturing, and sustainability-driven innovation will shape the competitive dynamics.

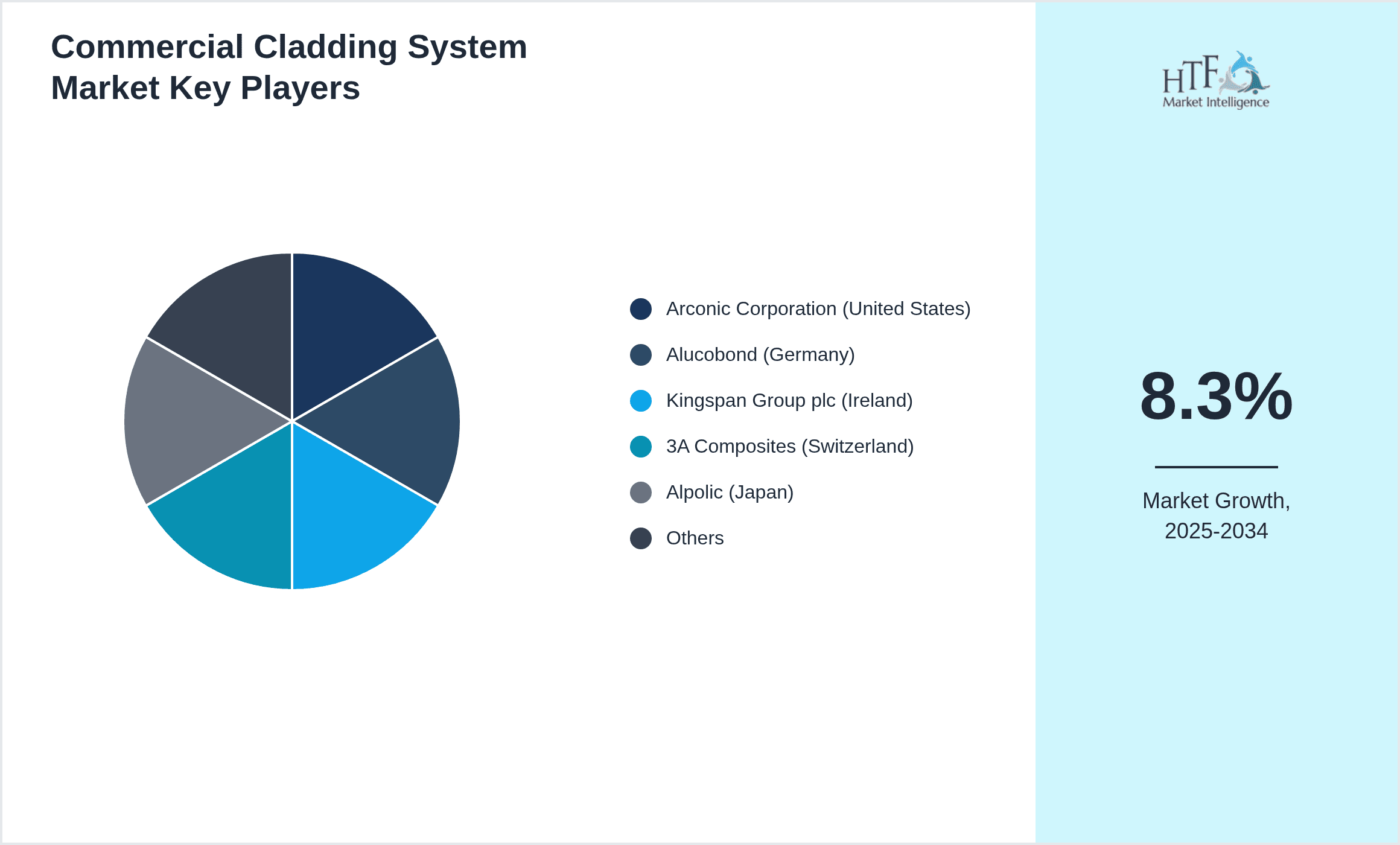

Leading Companies in Commercial Cladding System Market

- •Arconic Corporation (United States)

- •Alucobond (Germany)

- •Kingspan Group plc (Ireland)

- •3A Composites (Switzerland)

- •Alpolic (Japan)

- •Teckentrup GmbH & Co. KG (Germany)

- •Rockwool International A/S (Denmark)

- •James Hardie Industries plc (Ireland)

- •Tamlyn Group (United Kingdom)

- •Zamil Industrial Investment Co. (Saudi Arabia)

- •Formica Group (United States)

- •Alpolic Materials (Japan)

- •Mitsubishi Chemical Corporation (Japan)

- •Cembrit Holding A/S (Denmark)

- •Dri-Design Inc. (United States)

- •Boral Limited (Australia)

- •Etex Group (Belgium)

- •Kingspan Insulation Ltd (Ireland)

- •Alcoa Corporation (United States)

- •Saint-Gobain S.A. (France)

- •Hunter Douglas N.V. (Netherlands)

- •Schüco International KG (Germany)

- •Wienerberger AG (Austria)

- •Facade Technologies (United States)

- •Kingspan Facades (Ireland)

Market Breakdown

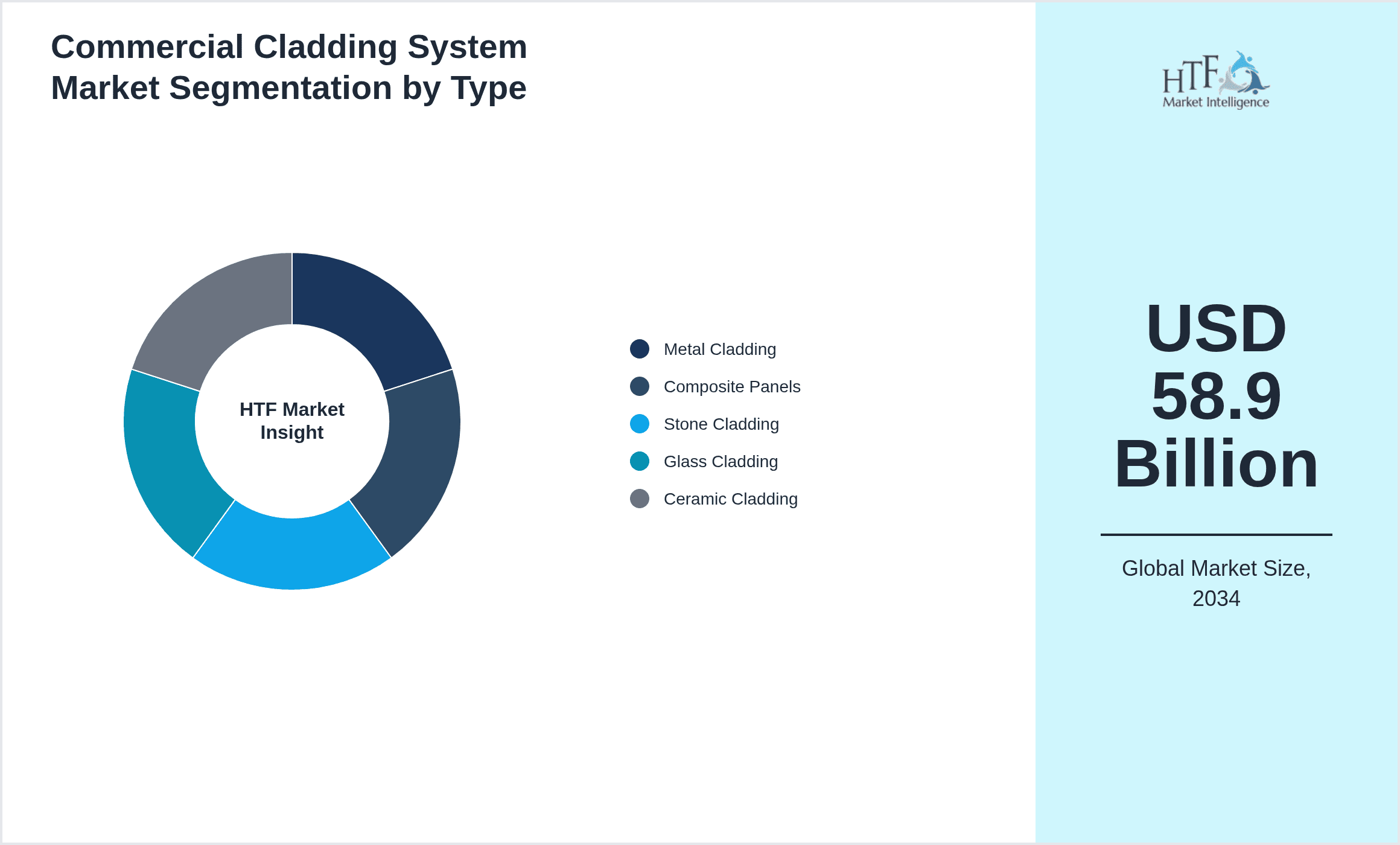

- •By Product Type

- ◦Metal Cladding

- ◦Composite Panels

- ◦Stone Cladding

- ◦Glass Cladding

- ◦Ceramic Cladding

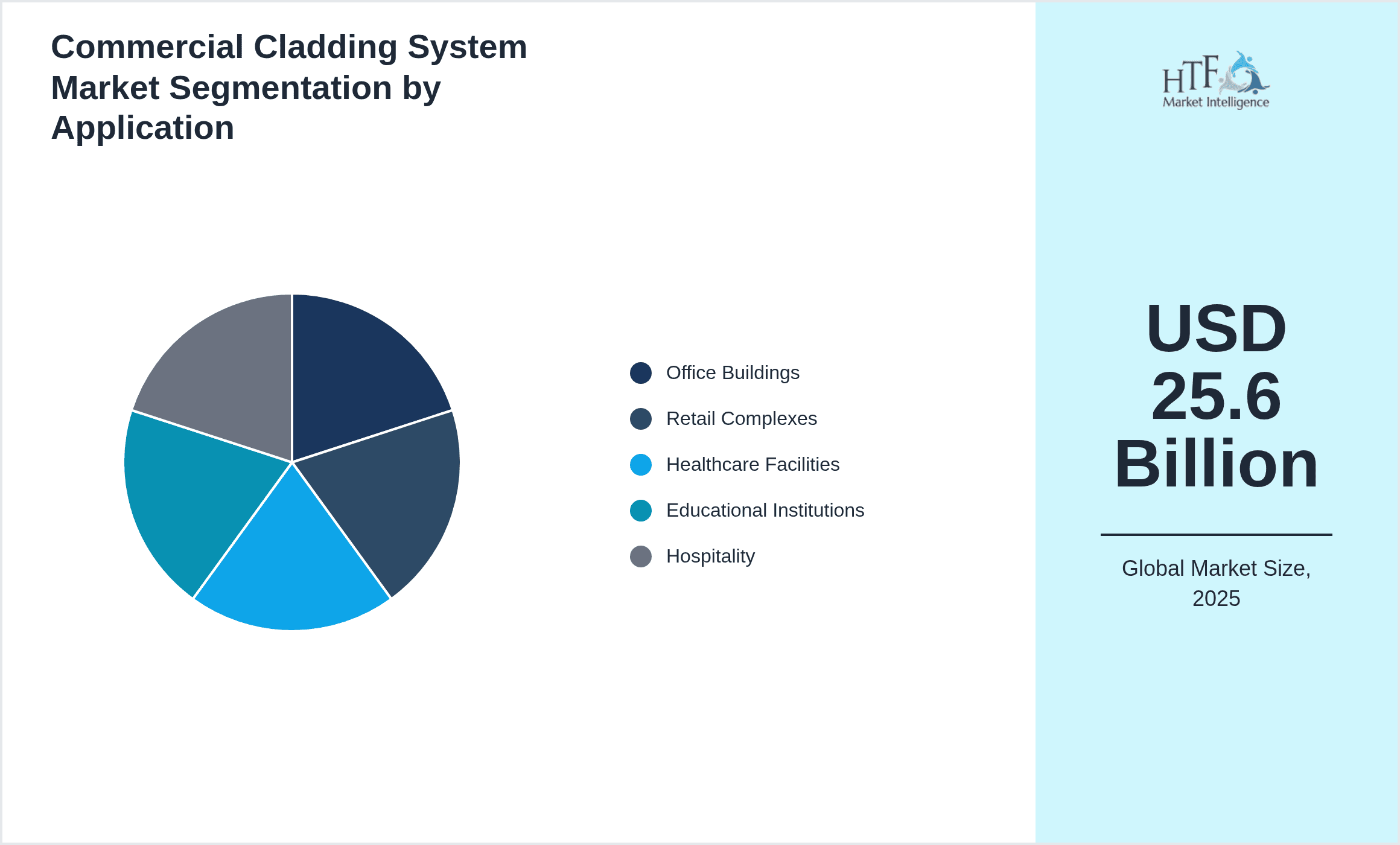

- •By Application

- ◦Office Buildings

- ◦Retail Complexes

- ◦Healthcare Facilities

- ◦Educational Institutions

- ◦Hospitality

- •By End-Use Industry

- ◦Commercial Construction

- ◦Renovation & Refurbishment

- ◦Public Infrastructure

- ◦Industrial Facilities

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Dealers

- ◦Online Platforms

Growth Dynamics

- •Rising urbanization and increasing commercial construction activities worldwide are primary growth drivers, with major investments in smart city projects fueling demand for advanced cladding systems that offer energy efficiency and aesthetic appeal.

- •Technological advancements such as development of lightweight composite panels and fire-resistant coatings enhance product performance, making cladding systems more attractive for compliance with stringent building codes and sustainability standards.

- •Government regulations promoting green buildings and energy-efficient architecture incentivize the adoption of eco-friendly cladding materials, thereby driving innovation and market expansion.

- •Increasing renovation and refurbishment projects in developed economies create opportunities for retrofitting existing structures with modern cladding solutions that improve thermal insulation and reduce operational costs.

- •Growing awareness among architects and builders about the benefits of modern cladding systems, including fire safety and weather resistance, is accelerating market penetration across emerging and mature markets.

- •The integration of digital manufacturing and modular construction techniques streamlines production and installation processes, reducing costs and time, which positively impacts market growth.

- •Expanding applications beyond commercial buildings into public infrastructure and industrial facilities broaden the market scope and revenue streams for cladding system manufacturers.

Market Trends

- •Sustainability remains a key trend with increasing demand for recyclable and low-carbon footprint cladding materials, driven by global environmental agendas and consumer preferences for green buildings.

- •The adoption of smart cladding technologies embedded with sensors for real-time monitoring of building envelope performance is emerging, enhancing maintenance and energy management capabilities.

- •Integration of aesthetically versatile cladding designs using digital printing and customizable panels enables architects to realize innovative facades, differentiating brand identity and customer appeal.

- •Collaborative partnerships between material manufacturers and construction firms are increasing to ensure seamless supply chain operations and faster project delivery.

- •Increasing preference for lightweight composite panels is evident in fast-growing markets due to ease of installation and superior thermal performance compared to traditional materials.

- •Regulatory focus on fire safety in cladding materials is intensifying after high-profile incidents, influencing product development and certification processes globally.

- •Digital transformation in sales and distribution channels, including e-commerce platforms for cladding products, is reshaping market accessibility and customer engagement.

Market Opportunities

- •Emerging economies present significant growth potential due to rapid urbanization and infrastructural development, offering opportunities to introduce advanced cladding technologies tailored to local climatic conditions.

- •Innovations in sustainable materials, such as bio-based composites and recycled content panels, open new market segments focused on eco-friendly construction solutions.

- •Expanding retrofit and refurbishment markets in developed regions create avenues for aftermarket cladding products that enhance energy efficiency and building aesthetics.

- •Technological integration of smart sensors within cladding systems offers opportunities for value-added services including predictive maintenance and enhanced building management.

- •Strategic collaborations between manufacturers and technology providers can accelerate product innovation and market penetration globally.

- •Geographic expansion into underpenetrated regions such as Latin America and Middle East & Africa holds promise due to increasing commercial construction investments.

- •Development of modular and prefabricated cladding systems can reduce installation time and costs, appealing to fast-paced construction projects.

Market Challenges

- •High initial costs associated with premium cladding materials and installation limit adoption especially in price-sensitive emerging markets, posing a significant barrier to market growth.

- •Stringent and varying regulatory requirements across different regions create compliance complexities and increase time-to-market for new cladding products.

- •Supply chain disruptions impacting raw material availability and price volatility challenge manufacturers' ability to maintain consistent product delivery and margins.

- •Lack of skilled labor for specialized installation techniques can affect project timelines and quality, particularly in rapidly developing markets.

- •Environmental concerns related to non-recyclable or hazardous cladding materials necessitate continuous innovation and may lead to regulatory restrictions.

- •Competition from alternative facade solutions such as curtain walls and EIFS (Exterior Insulation and Finish Systems) can limit market penetration.

- •Market fragmentation with numerous small regional players creates pricing pressures and challenges in establishing global standards.

Regulatory Framework

- •Between 2019 and 2024, major markets implemented enhanced fire safety regulations for commercial cladding systems, mandating use of non-combustible materials and rigorous certification processes, significantly impacting product design and approval timelines.

- •Environmental regulations promoting use of sustainable and recyclable materials have been introduced globally, with incentives for manufacturers adopting green practices and penalties for non-compliance, fostering innovation in eco-friendly cladding solutions.

- •Building codes in North America, Europe, and Asia-Pacific have increasingly incorporated energy efficiency standards requiring cladding systems to contribute to thermal insulation and reduce carbon emissions, influencing material selection and system design.

- •Regional mandates such as the EU Construction Products Regulation (CPR) and the North American NFPA 285 testing standard have standardized performance criteria for cladding materials, enhancing safety and market transparency.

- •Government initiatives offering subsidies and tax benefits for green buildings and renovations have incentivized adoption of advanced commercial cladding systems, accelerating market uptake in several countries.

Market Intelligence

- •15th January 2025, Kingspan Group plc launched a new line of ultra-lightweight composite panels designed to improve fire resistance and thermal performance for commercial facades, targeting rapid urbanization markets in Asia-Pacific and Europe. This innovation supports compliance with stricter fire safety regulations and offers ease of installation, aiming to capture significant market share in retrofit projects. Source: Official Kingspan Press Release

- •10th March 2025, Arconic Corporation introduced an advanced metal cladding solution featuring integrated solar panels, combining aesthetic value with renewable energy generation. This product is positioned to meet rising demand for sustainable building materials and smart facade technology, enhancing energy efficiency in commercial buildings worldwide. Source: Arconic Corporate Website

- •22nd June 2024, Alucobond (Germany) completed a strategic partnership with a leading construction firm in North America to expand its distribution network and accelerate deployment of fire-resistant aluminum composite panels in high-rise commercial projects, responding to heightened regulatory demands. Source: Industry Publication

- •5th September 2024, Mitsubishi Chemical Corporation announced the commercialization of recyclable glass cladding panels with enhanced durability and reduced carbon footprint, aiming to address sustainability trends in the commercial construction sector globally. This initiative aligns with regulatory incentives and growing environmental awareness. Source: Official Company Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 25.6 Billion |

| Forecast Year Market Size | USD 58.9 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.98% |

| Scope of Report | Market is segmented by Product Type (Metal Cladding, Composite Panels, Stone Cladding, Glass Cladding, Ceramic Cladding), Application (Office Buildings, Retail Complexes, Healthcare Facilities, Educational Institutions, Hospitality), End-Use Industry (Commercial Construction, Renovation & Refurbishment, Public Infrastructure, Industrial Facilities), Distribution Channel (Direct Sales, Distributors & Dealers, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Arconic Corporation (United States), Alucobond (Germany), Kingspan Group plc (Ireland), 3A Composites (Switzerland), Alpolic (Japan), Teckentrup GmbH & Co. KG (Germany), Rockwool International A/S (Denmark), James Hardie Industries plc (Ireland), Tamlyn Group (United Kingdom), Zamil Industrial Investment Co. (Saudi Arabia), Formica Group (United States), Alpolic Materials (Japan), Mitsubishi Chemical Corporation (Japan), Cembrit Holding A/S (Denmark), Dri-Design Inc. (United States), Boral Limited (Australia), Etex Group (Belgium), Kingspan Insulation Ltd (Ireland), Alcoa Corporation (United States), Saint-Gobain S.A. (France), Hunter Douglas N.V. (Netherlands), Schüco International KG (Germany), Wienerberger AG (Austria), Facade Technologies (United States), Kingspan Facades (Ireland) |

Global Commercial Cladding System Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Market market is projected to grow at a steady CAGR from 2025 to 2030, driven by increasing demand and expansion in various applications.

North America currently leads the market, followed by Europe and Asia-Pacific.

Key growth drivers include increasing activities, rising demand for innovative solutions, technological advancements, and growing preference for efficient products.