Global Agricultural Miticide Market Size, Growth & Revenue 2025-2034

Global Agricultural Miticide Market is segmented by Product Type (Biological Miticides, Chemical Miticides, Botanical Miticides, Synthetic Miticides, Others), Application (Ornamental Crops, Field Crops, Fruits & Vegetables, Turf & Landscape Management, Others), End-Use Industry (Agriculture, Horticulture, Turf Management, Research & Development), Distribution Channel (Direct Sales, Distributors/Wholesalers, Online Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global agricultural miticide market is defined by its role in mitigating the adverse impacts of mite infestations across diverse crop types including ornamental crops, field crops, fruits, vegetables, and turf. This market involves the production and distribution of chemical, biological, botanical, and synthetic miticides, which are integral to pest management strategies designed to safeguard crop health and optimize yields. The value chain spans from raw material procurement to the end-user application, encompassing formulation, manufacturing, and distribution channels used by agricultural producers globally. The market’s growth is fueled by increasing agricultural intensification, rising awareness of plant health, and the demand for sustainable crop protection products. Regulatory scrutiny ensures safety and efficacy, influencing product innovation and market dynamics. Key applications involve protecting economically significant crops from mite damage, reducing crop loss, and enhancing food security. The market also reflects growing environmental concerns, with a shift towards biological and botanical miticides as eco-friendly alternatives to conventional chemical products. Regional variations in agricultural practices, climate, and regulatory environments create a complex landscape for market participants. Overall, the market demonstrates robust growth potential driven by technological advancements, integrated pest management adoption, and expanding end-use sectors.

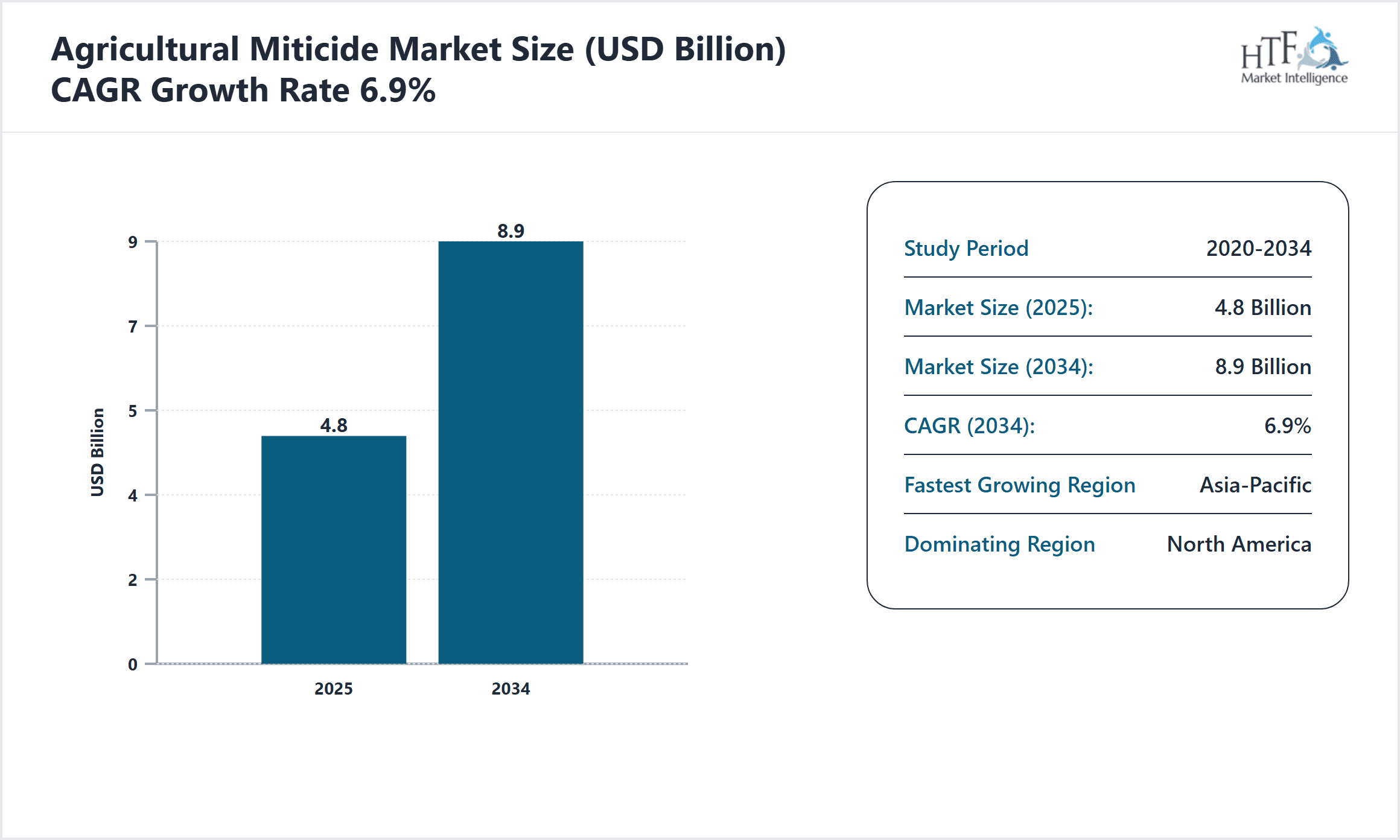

- •Market highlights include a base year valuation of USD 4.8 billion in 2025, with a forecast to reach USD 8.9 billion by 2034, reflecting a compound annual growth rate (CAGR) of 6.9%. North America currently dominates the market, attributed to advanced agricultural practices and stringent regulatory frameworks, while the Asia-Pacific region is the fastest-growing due to expanding agricultural activities and increasing adoption of sustainable pest control solutions. Chemical miticides maintain the largest market share, though biological miticides are growing rapidly due to their eco-friendly nature and regulatory support. Trends such as integrated pest management and development of novel formulations further enhance market growth prospects.

- •The strategic importance of the agricultural miticide market lies in its contribution to global food security by protecting crops from destructive mite infestations. It offers value to stakeholders from manufacturers to end-users by providing effective pest control solutions that improve yield and quality. Investment in research and development drives innovation in safer and more efficient products, aligning with environmental regulations and consumer preferences. The market supports sustainable agricultural practices, thereby positioning itself as a critical segment within the broader crop protection industry.

Competitive Landscape

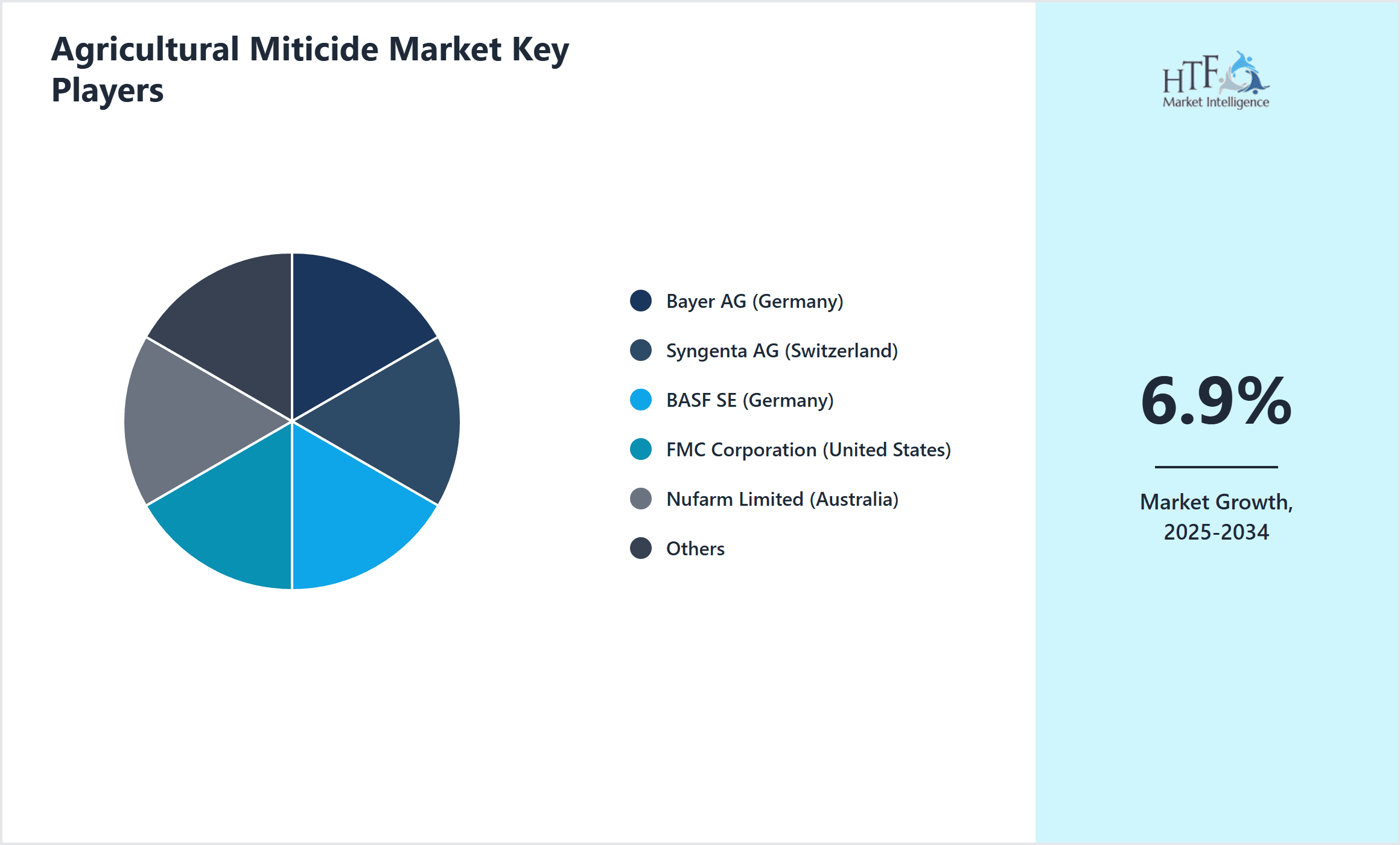

The global agricultural miticide market is characterized by intense competition among key players, driven by innovation, strategic partnerships, and mergers and acquisitions. Market leaders focus on developing advanced formulations that offer enhanced efficacy with reduced environmental impact, leveraging biotechnology and integrated pest management practices. Competitive strategies include expanding product portfolios, geographic reach, and investing in sustainable solutions to meet increasing regulatory and consumer demands. Pricing strategies balance affordability with high performance, while distribution networks are optimized for broad market coverage. Emerging players focus on niche segments such as biological miticides, benefiting from growing demand for eco-friendly alternatives. Technological adoption, including precision agriculture and digital pest monitoring, further influences competitive dynamics. Market entry barriers remain significant due to stringent regulatory approvals and high R&D costs. Regional competition is shaped by local agricultural practices, regulatory environments, and crop profiles, with North America and Europe exhibiting mature competitive landscapes and Asia-Pacific presenting rapid expansion opportunities. Future trends point to consolidation and innovation as key drivers shaping the competitive environment.

Leading Companies in Agricultural Miticide Market

- •Bayer AG (Germany)

- •Syngenta AG (Switzerland)

- •BASF SE (Germany)

- •FMC Corporation (United States)

- •Nufarm Limited (Australia)

- •UPL Limited (India)

- •Sumitomo Chemical Co., Ltd. (Japan)

- •ADAMA Agricultural Solutions Ltd. (Israel)

- •Makhteshim Agan Industries Ltd. (Israel)

- •Certis USA LLC (United States)

- •Sipcam Oxon S.p.A. (Italy)

- •Koppert Biological Systems (Netherlands)

- •Valent U.S.A. LLC (United States)

- •Nissan Chemical Corporation (Japan)

- •Sumitomo Chemical Company (Japan)

- •Gowan Company (United States)

- •Isagro S.p.A. (Italy)

- •Arysta LifeScience Corporation (Japan)

- •Bionema Ltd. (United Kingdom)

- •Ginkgo Bioworks (United States)

- •Marrone Bio Innovations, Inc. (United States)

- •Certis Europe B.V. (Netherlands)

- •InnovaFeed (France)

- •Symborg S.L. (Spain)

- •AgBiome, Inc. (United States)

Market Breakdown

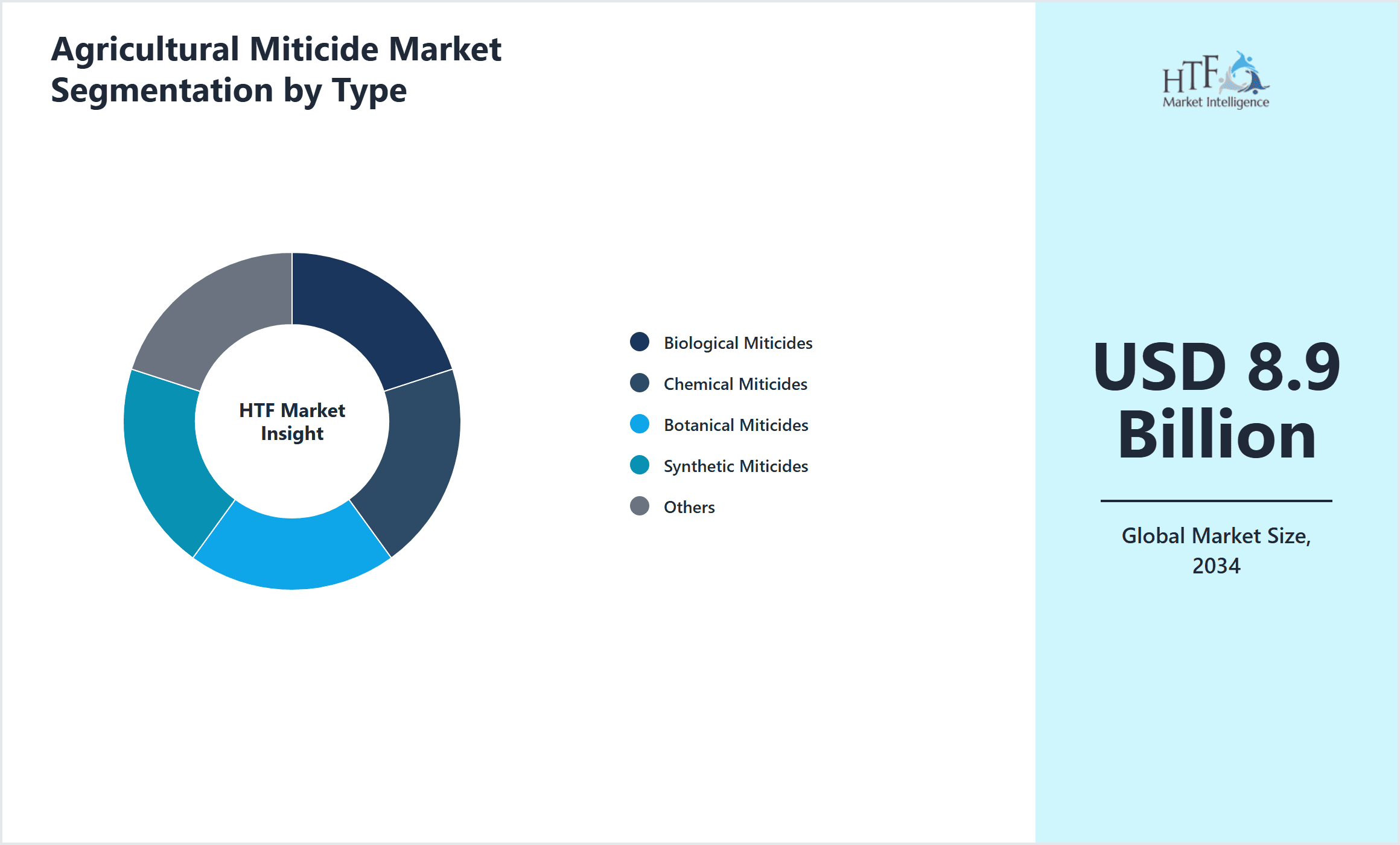

- •By Product Type

- ◦Biological Miticides

- ◦Chemical Miticides

- ◦Botanical Miticides

- ◦Synthetic Miticides

- ◦Others

- •By Application

- ◦Ornamental Crops

- ◦Field Crops

- ◦Fruits & Vegetables

- ◦Turf & Landscape Management

- ◦Others

- •By End-Use Industry

- ◦Agriculture

- ◦Horticulture

- ◦Turf Management

- ◦Research & Development

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors/Wholesalers

- ◦Online Sales

Growth Dynamics

- •Rising global demand for sustainable crop protection solutions fuels growth in the agricultural miticide market, with increased adoption of biological and botanical miticides as eco-friendly alternatives to chemical products. This shift is driven by regulatory pressures and consumer preference for organic produce.

- •Technological advancements in formulation and delivery mechanisms enhance miticide efficacy and reduce environmental impact, encouraging wider adoption across diverse crop types and geographies. Innovations such as microencapsulation and controlled-release formulations improve application efficiency.

- •Expansion of high-value crop cultivation in emerging markets, particularly in Asia-Pacific and Latin America, creates significant demand for effective mite control products to protect yields and quality. Increasing agricultural intensification in these regions supports market growth.

- •Integration of miticides into comprehensive integrated pest management (IPM) programs promotes sustainable agriculture and drives market growth by optimizing pest control while minimizing chemical use and resistance development.

- •Government initiatives and subsidies promoting sustainable agriculture and integrated pest management encourage farmers to adopt advanced miticide products, supporting market expansion and innovation.

- •Growing awareness among farmers about the economic losses caused by mite infestations and the benefits of timely miticide application increases product demand and market penetration globally.

- •Rising investments in research and development by market players to develop safer and more effective miticides drive competitive advantage and product differentiation, stimulating market growth.

Market Trends

- •A notable trend is the increasing preference for biological miticides derived from naturally occurring microorganisms and plant extracts, driven by environmental regulations and consumer demand for sustainable agriculture products.

- •Digital agriculture technologies, including precision spraying and pest monitoring systems, are being integrated with miticide application to improve efficacy and reduce chemical usage, representing a significant technological shift.

- •Strategic collaborations between chemical manufacturers and biotech companies are fostering innovation in miticide development, combining chemical efficacy with biological safety to meet evolving regulatory standards.

- •The market is witnessing a trend towards multi-functional crop protection products, where miticides are combined with fungicides or insecticides to provide broad-spectrum pest control, increasing operational efficiency for farmers.

- •Sustainability and carbon footprint reduction efforts are prompting companies to reformulate miticides with lower environmental impact and to adopt green manufacturing processes.

- •E-commerce platforms are increasingly becoming important distribution channels, improving accessibility and availability of miticide products to small and medium-scale farmers.

- •Consumer awareness campaigns and educational programs on integrated pest management are influencing adoption patterns and driving demand for safer miticide options globally.

Market Opportunities

- •The growing adoption of organic farming and demand for chemical-free produce presents significant opportunities for the development and commercialization of biological and botanical miticides that align with organic certification standards.

- •Emerging economies in Asia-Pacific and Latin America offer untapped markets with expanding agricultural sectors and increasing awareness about pest management, creating avenues for market expansion.

- •Advancements in biotechnology and microbial formulations enable the creation of next-generation miticides with enhanced specificity and environmental compatibility, opening new product development opportunities.

- •Partnerships between technology providers and agricultural companies to integrate digital pest management tools with miticide application present growth potential through precision agriculture adoption.

- •Investment in education and training programs for farmers on effective pest management strategies can increase market penetration and product usage frequency, boosting sales.

- •Regulatory support for sustainable agriculture and incentives for adopting eco-friendly pest control solutions create a favorable environment for innovative miticide products.

- •Product line extensions combining miticides with other crop protection agents enable companies to offer comprehensive solutions, increasing customer loyalty and market share.

Market Challenges

- •Stringent regulatory requirements and lengthy approval processes for new miticide products delay market entry and increase development costs, posing significant challenges for manufacturers.

- •Resistance development among mite populations due to repeated use of chemical miticides reduces product efficacy and necessitates frequent innovation, increasing operational complexity.

- •High cost of biological and botanical miticides compared to traditional chemical formulations limits adoption, especially among smallholder farmers in developing regions.

- •Limited awareness and technical knowledge about integrated pest management and advanced miticide products restrict market growth in certain geographies.

- •Supply chain disruptions and raw material price volatility impact production costs and market stability, affecting availability and pricing of miticide products.

- •Environmental concerns and public scrutiny over chemical residues in food and soil necessitate rigorous compliance and transparency, increasing regulatory burden on producers.

- •Competition from alternative pest control methods such as biological control agents and cultural practices exerts pressure on the miticide market to innovate and differentiate.

Regulatory Framework

- •The EU Regulation on Plant Protection Products (enforced between 2020 and 2025) mandates rigorous safety assessments and authorizations for miticides, significantly impacting market access and product formulations within Europe.

- •The U.S. Environmental Protection Agency (EPA) updated its pesticide registration review process during this period, enforcing stricter residue limits and environmental safety measures that influence product approvals and usage guidelines.

- •China’s Ministry of Agriculture implemented new pesticide registration and evaluation standards focusing on reducing hazardous chemicals and promoting green alternatives, affecting both domestic and international manufacturers seeking market entry.

- •The adoption of global harmonization standards such as those from the Codex Alimentarius Commission ensures consistent pesticide residue limits and promotes international trade compliance, impacting export-oriented companies.

- •Government initiatives including subsidies and incentives for integrated pest management and sustainable agriculture foster compliance and encourage the adoption of eco-friendly miticides across multiple regions.

Market Intelligence

- •12th January 2024, Bayer AG launched a next-generation biological miticide formulated with advanced microbial strains targeting a broad spectrum of mite species to reduce crop damage in fruits and vegetables. This product offers enhanced environmental safety and compatibility with integrated pest management systems, aiming to capture increasing demand in North America and Europe. Bayer's strategic objective is to expand its portfolio of sustainable crop protection products amid tightening regulatory standards. Source: Bayer Official Press Release

- •5th April 2024, Syngenta AG introduced a novel synthetic miticide with a unique mode of action designed to overcome resistance issues prevalent in key mite populations affecting field crops. The innovation promises improved efficacy and longer residual activity, positioning Syngenta as a market leader in chemical miticides. This launch supports Syngenta’s commitment to innovation and sustainability in its product offerings. Source: Syngenta Newsroom

- •18th August 2024, FMC Corporation announced a strategic partnership with a leading biotech firm to co-develop botanical miticide formulations leveraging natural plant extracts. This collaboration aims to accelerate product development cycles and address the growing market for organic and eco-friendly pest control solutions, especially in Asia-Pacific. FMC expects this initiative to strengthen its competitive position and meet evolving consumer preferences. Source: FMC Corporate Announcement

- •27th November 2024, UPL Limited completed the acquisition of a regional biological pest control company to enhance its sustainable agriculture portfolio and expand its footprint in Latin America. The acquisition provides UPL with access to innovative microbial technologies and strengthens its position in the growing market for biological miticides. This move aligns with UPL’s strategic growth plans focusing on diversification and sustainability. Source: UPL Press Release

- •Source: Official press releases / Company websites / Industry publications

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.8 Billion |

| Forecast Year Market Size | USD 8.9 Billion |

| CAGR | 6.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.9% |

| Scope of Report | Market is segmented by Product Type (Biological Miticides, Chemical Miticides, Botanical Miticides, Synthetic Miticides, Others), Application (Ornamental Crops, Field Crops, Fruits & Vegetables, Turf & Landscape Management, Others), End-Use Industry (Agriculture, Horticulture, Turf Management, Research & Development), Distribution Channel (Direct Sales, Distributors/Wholesalers, Online Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Bayer AG (Germany), Syngenta AG (Switzerland), BASF SE (Germany), FMC Corporation (United States), Nufarm Limited (Australia), UPL Limited (India), Sumitomo Chemical Co., Ltd. (Japan), ADAMA Agricultural Solutions Ltd. (Israel), Makhteshim Agan Industries Ltd. (Israel), Certis USA LLC (United States), Sipcam Oxon S.p.A. (Italy), Koppert Biological Systems (Netherlands), Valent U.S.A. LLC (United States), Nissan Chemical Corporation (Japan), Sumitomo Chemical Company (Japan), Gowan Company (United States), Isagro S.p.A. (Italy), Arysta LifeScience Corporation (Japan), Bionema Ltd. (United Kingdom), Ginkgo Bioworks (United States), Marrone Bio Innovations, Inc. (United States), Certis Europe B.V. (Netherlands), InnovaFeed (France), Symborg S.L. (Spain), AgBiome, Inc. (United States) |

Global Agricultural Miticide Market Size, Growth & Revenue 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.