Global Commercial Purpose Drone Market Size, Growth & Revenue 2024-2034

Global Commercial Purpose Drone Market is segmented by Product Type (Fixed Wing Drones, Multi-Rotor Drones, Single Rotor Drones, Hybrid Drones, Nano Drones), Application (Agriculture, Infrastructure Inspection, Delivery Services, Surveillance & Security, Media & Entertainment), End-Use Industry (Agriculture & Farming, Construction & Infrastructure, Logistics & Transportation, Government & Defense), Distribution Channel (Direct Sales, Third-Party Retailers, Online Sales Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Commercial Purpose Drone market is defined by the deployment of unmanned aerial vehicles for various commercial applications, including agriculture, infrastructure inspection, delivery services, surveillance, and media production. This market covers a wide range of drone types such as fixed wing, multi-rotor, single rotor, hybrid, and nano drones, each catering to distinct operational requirements. The industry scope extends from drone manufacturing and software development to service provision and data analytics integration. Technological advancements such as enhanced autonomy, improved battery life, and advanced sensors have significantly broadened the use cases and operational efficiency of commercial drones. The market is also influenced by evolving regulatory frameworks that aim to balance innovation with safety and privacy considerations. The expanding demand for drones in precision agriculture, logistics, and security sectors drives robust market growth globally. Increasing investments in drone technology and infrastructure further underscore the strategic importance of this market across multiple industries worldwide.

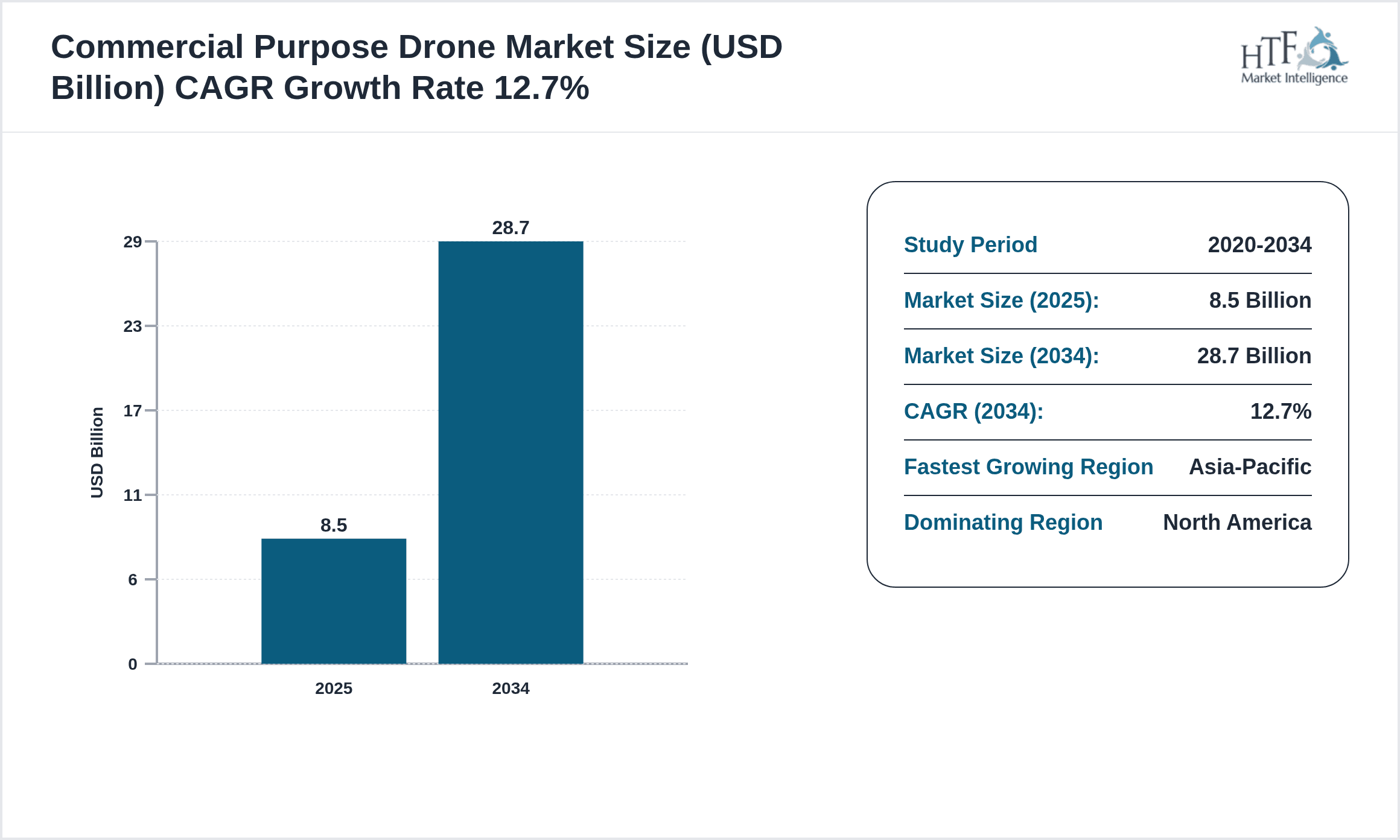

- •Key market highlights include a current valuation of USD 8.5 Billion in 2024, with projections reaching USD 28.7 Billion by 2034, reflecting a compound annual growth rate (CAGR) of 12.7%. Multi-rotor drones dominate the product segment due to their versatility and ease of use, while hybrid drones emerge as the fastest-growing type, driven by their enhanced flight capabilities. In application segments, agriculture leads adoption, followed closely by infrastructure inspection as industries seek cost-effective monitoring solutions. Regionally, North America holds the largest market share owing to mature drone regulations and strong industrial adoption, whereas Asia-Pacific is the fastest-growing region, fueled by expanding commercial drone utilization across developing economies. Year-over-year growth is robust at approximately 12.0%, indicating sustained market momentum and increasing acceptance of commercial drone technologies worldwide.

- •The commercial drone market offers significant value propositions by enabling enhanced operational efficiency, cost reduction, and improved data accuracy across diverse industries. For agriculture, drones facilitate precision farming techniques that optimize resource use and crop management. In logistics, drones provide last-mile delivery solutions that reduce delivery times and operational costs. Surveillance and security applications benefit from real-time aerial monitoring capabilities, enhancing situational awareness. The media and entertainment sector leverages drones for innovative filming and photography techniques. Stakeholders including manufacturers, service providers, technology developers, and regulatory bodies find strategic opportunities in this evolving market to foster innovation, expand service offerings, and capture growing demand. The market’s dynamic nature and cross-sector applicability position it as a critical growth area in the global technology landscape.

Competitive Landscape

The Global Commercial Purpose Drone market is characterized by intense competition driven by technological innovation, strategic partnerships, and evolving regulatory compliance. Market players focus heavily on product differentiation through the integration of advanced sensors, AI-powered analytics, and improved flight endurance to cater to diverse commercial needs. Competitive strategies include expanding service portfolios, enhancing drone capabilities with payload versatility, and establishing robust distribution networks worldwide. Mergers and acquisitions are common to consolidate market presence and accelerate technology adoption. Regional competition varies, with North America and Europe dominated by established manufacturers, while Asia-Pacific sees rapid growth from both global and local players. The market entry barriers include stringent regulatory approvals and high R&D investments. Future trends indicate increased collaboration between drone manufacturers and software companies to deliver integrated solutions, positioning innovation and agility as key competitive advantages in this fast-evolving sector.

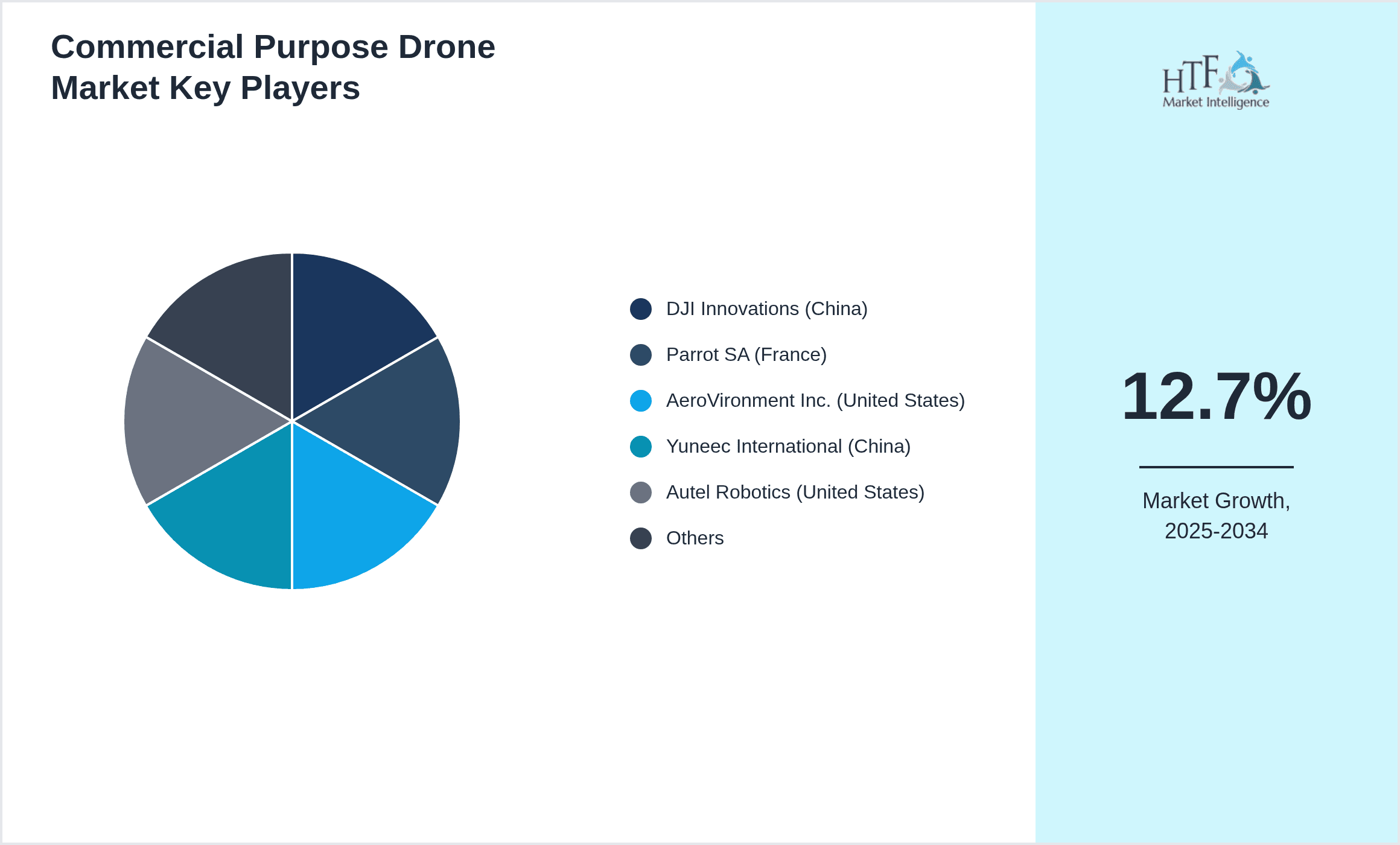

Key Players in Commercial Purpose Drone Market

- •DJI Innovations (China)

- •Parrot SA (France)

- •AeroVironment Inc. (United States)

- •Yuneec International (China)

- •Autel Robotics (United States)

- •Teledyne FLIR LLC (United States)

- •Delair (France)

- •senseFly (Switzerland)

- •Intel Corporation (United States)

- •Lockheed Martin Corporation (United States)

- •Northrop Grumman Corporation (United States)

- •Aeryon Labs Inc. (Canada)

- •Skydio Inc. (United States)

- •Insitu Inc. (United States)

- •FLIR Systems (United States)

- •Hubsan Technology Co. Ltd. (China)

- •EHang Holdings Limited (China)

- •CyPhy Works (United States)

- •Kespry Inc. (United States)

- •Walkera Technology Co. Ltd. (China)

- •DroneDeploy Inc. (United States)

- •AgEagle Aerial Systems Inc. (United States)

- •Terra Drone Corporation (Japan)

- •Volansi Inc. (United States)

- •Zipline International Inc. (United States)

Market Breakdown

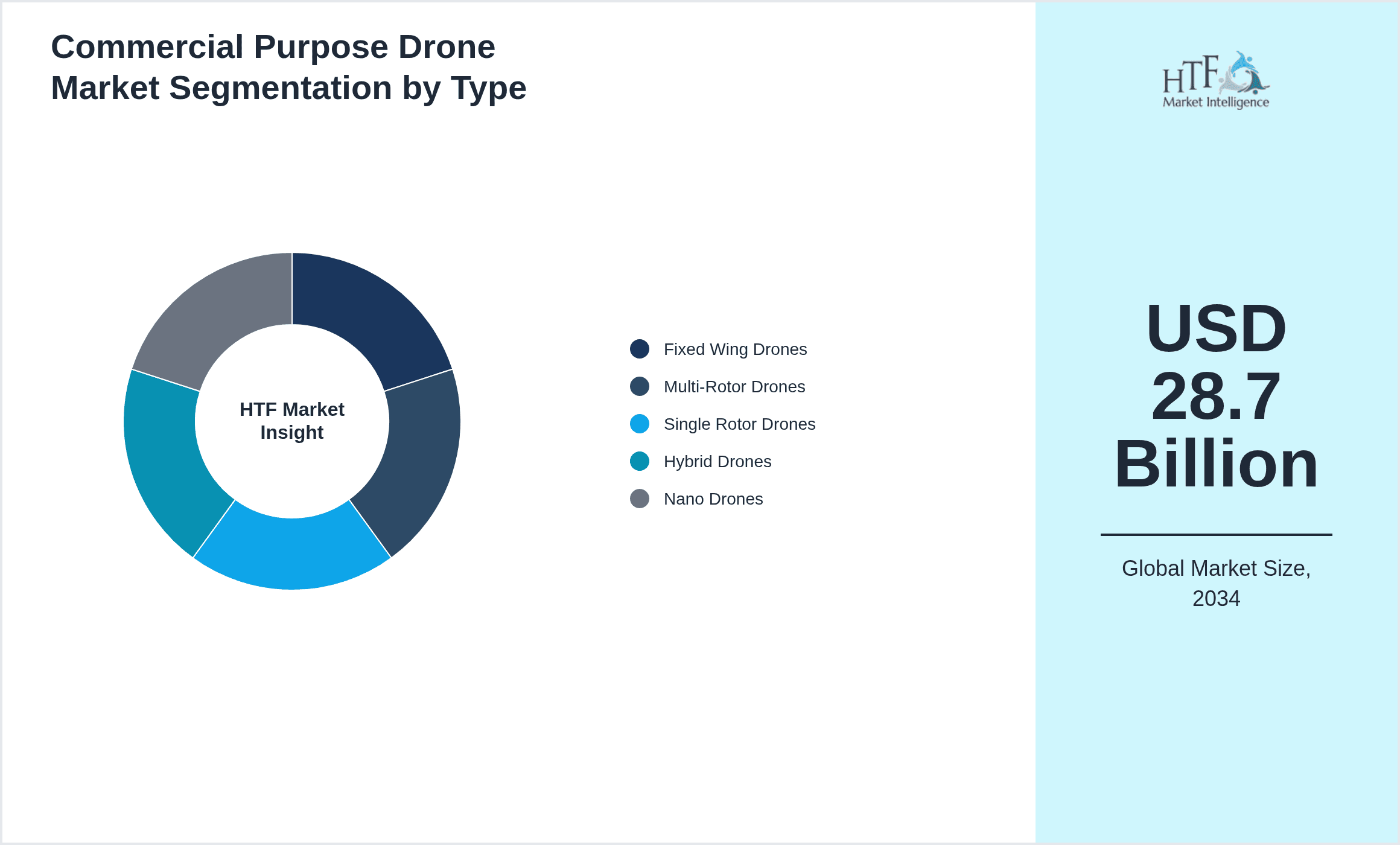

- •By Product Type

- ◦Fixed Wing Drones

- ◦Multi-Rotor Drones

- ◦Single Rotor Drones

- ◦Hybrid Drones

- ◦Nano Drones

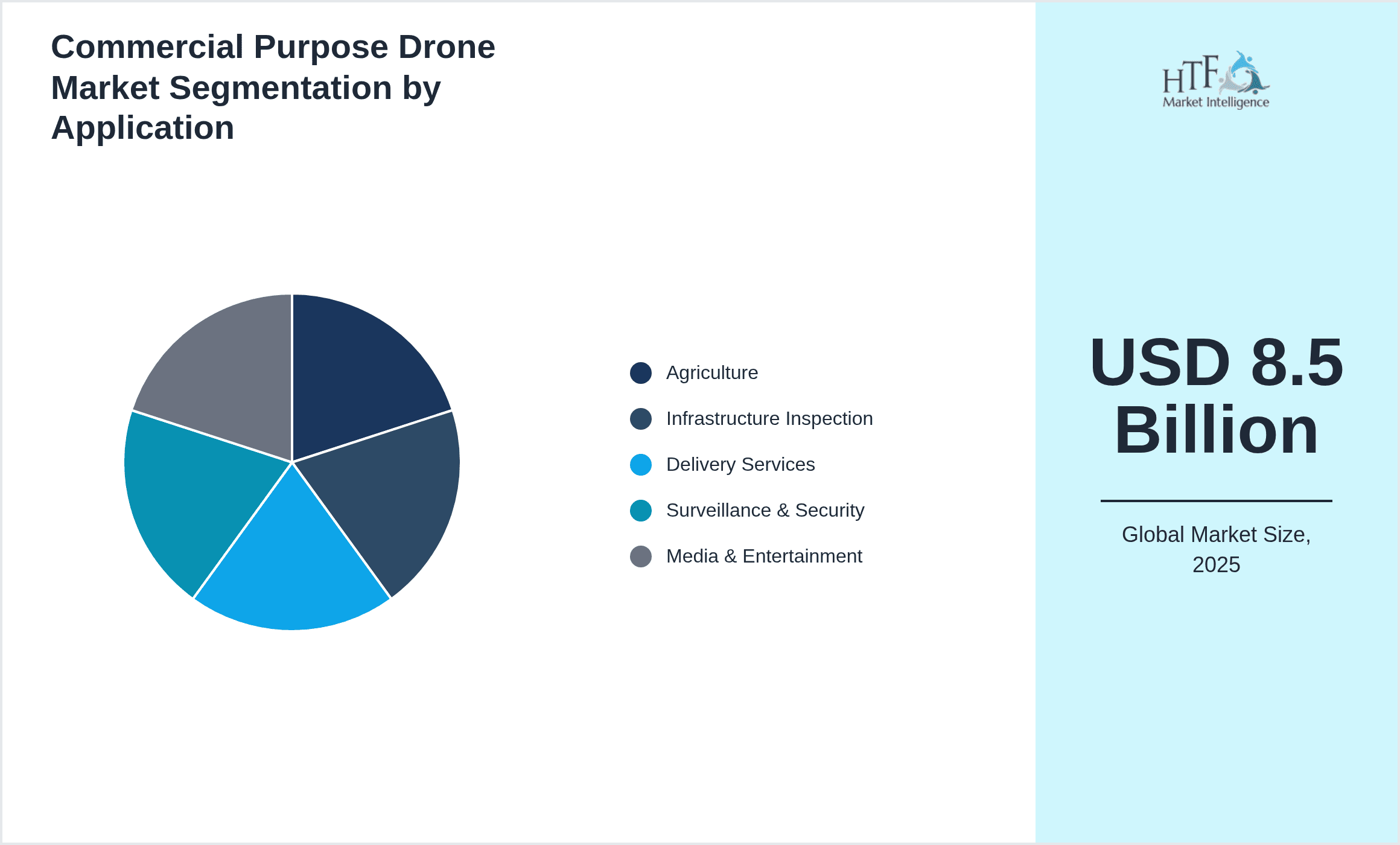

- •By Application

- ◦Agriculture

- ◦Infrastructure Inspection

- ◦Delivery Services

- ◦Surveillance & Security

- ◦Media & Entertainment

- •By End-Use Industry

- ◦Agriculture & Farming

- ◦Construction & Infrastructure

- ◦Logistics & Transportation

- ◦Government & Defense

- •By Distribution Channel

- ◦Direct Sales

- ◦Third-Party Retailers

- ◦Online Sales Platforms

Growth Dynamics

- •Rising adoption of drones in precision agriculture is a major growth driver, enabling farmers to optimize crop yields through detailed aerial imaging and resource management. Companies like DJI and senseFly provide tailored drone solutions that enhance data accuracy and operational efficiency in farming practices.

- •Technological advancements in drone autonomy and AI-powered analytics are expanding commercial applications, allowing for more complex and cost-effective operations in infrastructure inspection and delivery services. These innovations reduce human intervention and improve operational safety.

- •Increasing investments in drone infrastructure and government initiatives to integrate drones into national airspace systems facilitate market expansion. Regulatory frameworks are evolving to support commercial drone deployments, encouraging industry growth globally.

- •The growing demand for rapid delivery services, particularly in e-commerce and healthcare logistics, is driving the adoption of delivery drones, which reduce delivery times and operational costs in urban and remote areas alike.

- •Environmental monitoring and disaster management applications are increasingly utilizing drones for real-time data collection, enhancing response capabilities and promoting sustainable practices across sectors.

- •Strategic collaborations between drone manufacturers and software companies enhance solution integration, offering end-to-end services that attract diverse commercial customers across regions.

- •Expanding use of drones in media and entertainment for aerial photography and live event coverage offers creative opportunities and drives market diversification.

Market Trends

- •Integration of AI and machine learning in drone systems is transforming data processing capabilities, enabling real-time decision-making and autonomous operations that enhance efficiency in commercial applications.

- •The rise of hybrid drones combining fixed wing and multi-rotor features is gaining traction due to their extended flight time and versatile maneuverability, meeting complex operational demands.

- •Increasing use of drones for last-mile delivery by companies like Zipline and Volansi reflects a strategic shift towards drone-enabled logistics, particularly in healthcare and e-commerce sectors.

- •Sustainability initiatives are influencing drone usage, with electric-powered drones reducing carbon footprints and aligning with global environmental goals.

- •Collaborative ecosystems between technology providers, regulatory bodies, and end-users are fostering innovation and accelerating market penetration of commercial drones.

- •Customized drone solutions tailored to specific industry needs are emerging, supported by modular designs and adaptable payload options.

- •Expansion of drone service platforms offering data analytics and fleet management is enhancing user experience and operational scalability in commercial drone deployments.

Market Opportunities

- •Emerging markets in Asia-Pacific present significant growth potential due to increasing industrialization, infrastructure development, and favorable government policies supporting drone adoption across sectors.

- •Untapped applications in environmental conservation and renewable energy monitoring offer avenues for drone technology integration and service expansion.

- •Investment opportunities exist in developing advanced hybrid drone platforms that combine long endurance with operational flexibility, addressing diverse commercial demands.

- •Geographical expansion into Latin America and Middle East & Africa regions is promising, driven by growing infrastructure needs and logistical challenges that drones can address effectively.

- •Product innovations focusing on payload versatility and enhanced sensor integration can improve value propositions and attract new commercial segments.

- •Strategic partnerships and acquisitions can facilitate technology sharing and market entry, accelerating growth trajectories for key players.

- •Anticipated regulatory relaxations and harmonization will open new operational corridors, enabling expanded drone service offerings and market diversification.

Market Challenges

- •Stringent and varied regulatory frameworks across different regions create compliance complexities, slowing down market entry and operational scalability for commercial drone operators.

- •Technical limitations such as limited battery life, payload capacity, and vulnerability to adverse weather conditions restrict operational efficiency and application scope.

- •Privacy and security concerns related to data collection and aerial surveillance pose challenges for widespread drone acceptance and regulatory approvals.

- •High initial investment and maintenance costs can deter small and medium enterprises from adopting commercial drone technologies, affecting market penetration.

- •Competitive pressure from low-cost drone manufacturers challenges established players to continuously innovate and optimize cost structures.

- •Supply chain disruptions and shortages of critical components such as semiconductors impact production timelines and product availability.

- •Talent shortage in skilled drone operators and data analysts limits the potential for rapid market expansion and service quality improvements.

Regulatory Framework

- •The FAA Modernization and Reform Act updates from 2019 to 2024 have introduced specific requirements for commercial drone registration, remote pilot certification, and operational limits, enhancing safety and airspace integration.

- •The European Union's UAS Regulation 2019/947 establishes a standardized framework for drone operations across member states, including categories for open, specific, and certified operations, impacting manufacturers and service providers.

- •China's Civil Aviation Administration regulations implemented between 2020 and 2023 require real-name registration and flight authorization for commercial drones, promoting responsible usage and reducing unauthorized flights.

- •India's Drone Rules 2021 introduced a digital sky platform for drone approvals and airspace management, streamlining regulatory processes and encouraging commercial drone adoption.

- •Various countries in the Middle East and Latin America have updated their drone policies from 2022 to 2024 to balance innovation facilitation with privacy and security concerns, impacting market entry strategies.

Market Intelligence

- •15th January 2025, DJI Innovations launched the Matrice 350 RTK, a hybrid drone equipped with advanced payload options and extended flight time, targeting infrastructure inspection and agricultural mapping markets globally. The product aims to enhance operational efficiency with integrated AI analytics and robust connectivity features, positioning DJI as a continued market leader.

- •20th March 2025, Parrot SA introduced the Anafi USA drone featuring enhanced thermal imaging and secure data transmission capabilities. This innovation targets government and defense segments, emphasizing reliability and compliance with strict security standards to expand Parrot's footprint in critical commercial applications.

- •10th May 2025, AeroVironment Inc. announced a strategic partnership with logistics provider Zipline to co-develop delivery drone systems aimed at improving medical supply chains in remote regions. This collaboration is expected to accelerate drone-based delivery adoption and expand market reach in underserved areas.

- •5th August 2025, senseFly completed the acquisition of a European AI software startup specializing in data analytics for precision agriculture drones. This move strengthens senseFly's position in the agriculture sector by integrating advanced machine learning capabilities to optimize crop monitoring services.

- •Source: Official press releases and company websites

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.5 Billion |

| Forecast Year Market Size | USD 28.7 Billion |

| CAGR | 12.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12% |

| Scope of Report | Market is segmented by Product Type (Fixed Wing Drones, Multi-Rotor Drones, Single Rotor Drones, Hybrid Drones, Nano Drones), Application (Agriculture, Infrastructure Inspection, Delivery Services, Surveillance & Security, Media & Entertainment), End-Use Industry (Agriculture & Farming, Construction & Infrastructure, Logistics & Transportation, Government & Defense), Distribution Channel (Direct Sales, Third-Party Retailers, Online Sales Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | DJI Innovations (China), Parrot SA (France), AeroVironment Inc. (United States), Yuneec International (China), Autel Robotics (United States) |

Global Commercial Purpose Drone Market Size, Growth & Revenue 2024-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.