Global Mobile Computer (PDA) Market Size, Growth & Revenue 2025-2034

Global Mobile Computer (PDA) Market is segmented by Product Type (Rugged PDA - Durable handheld devices designed for harsh industrial environments, Consumer PDA - General purpose mobile computing devices for everyday use, Enterprise PDA - Business-centric handhelds with enhanced security and connectivity, Barcode Scanners - Devices specialized in scanning and processing barcode data, Wearable PDAs - Hands-free devices designed for mobility and operational efficiency), Application (Inventory Management - Tracking and managing stock in warehouses and retail, Field Service - Mobile devices for technicians and service personnel in the field, Retail - Point-of-sale and customer service handheld PDAs, Healthcare - Patient monitoring, data entry, and asset tracking applications, Logistics - Shipment tracking, delivery management, and route optimization), End-Use Industry (Manufacturing - Production monitoring and quality control, Transportation & Logistics - Fleet management and cargo tracking, Healthcare - Clinical data management and patient care, Retail - Sales operations and inventory control), Distribution Channel (Direct Sales - Manufacturer to end-user transactions, Channel Partners - Resellers, distributors, and system integrators, Online Retail - E-commerce platforms for device sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Mobile Computer (PDA) Market refers to the industry segment involving handheld devices engineered to enhance data collection, communication, and operational efficiency across multiple sectors such as inventory management, healthcare, retail, field service, and logistics. These devices are characterized by their portability, durability, and integration of advanced technologies like barcode scanning, wireless connectivity, and ruggedized hardware. The market scope covers various PDA types including rugged PDAs designed for tough environments, consumer-grade PDAs for general use, enterprise PDAs tailored for business applications, barcode scanners for inventory accuracy, and wearable PDAs that enable hands-free mobility. End users span manufacturing, warehousing, retail, healthcare, and transportation sectors, relying on these devices for real-time data capture and workflow optimization. The value chain comprises component suppliers, device manufacturers, software providers, and service partners delivering comprehensive solutions. Market growth is propelled by rising demand for mobile workforce enablement, automation, and real-time information access, alongside advancements in wireless technologies and device capabilities. Emerging markets in Asia-Pacific and Latin America present significant adoption opportunities, while established regions like North America and Europe maintain leadership through innovation and infrastructure investments.

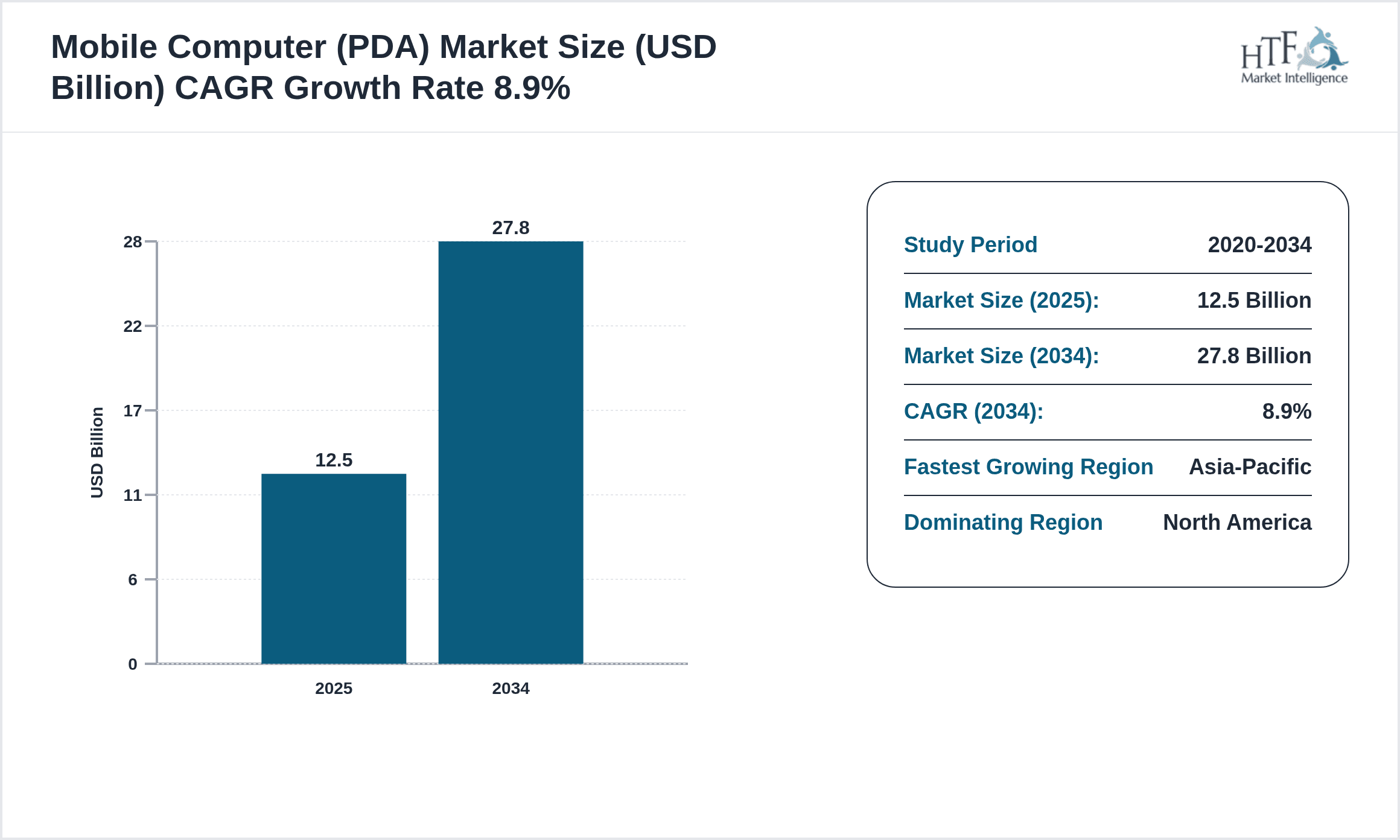

- •Key market highlights include a base market size of USD 12.5 Billion in 2025, forecasted to reach USD 27.8 Billion by 2034, reflecting a compound annual growth rate (CAGR) of 8.9%. The market exhibits a robust year-over-year growth of approximately 8.5%, driven by expanding applications in inventory management and healthcare sectors. Rugged PDAs currently dominate the product type segment, while wearable PDAs are registering the fastest growth due to increasing demand for hands-free computing in logistics and field operations. North America remains the dominant region by market share, supported by advanced infrastructure and high adoption rates, whereas Asia-Pacific is the fastest growing region, fueled by rapid industrialization and digital transformation initiatives.

- •The market offers significant value propositions including enhanced operational efficiency, real-time data capture, and improved accuracy in data-intensive tasks across industries. Strategic importance lies in enabling mobility and automation, which are critical for digital transformation agendas in manufacturing, retail, healthcare, and logistics sectors. Stakeholders such as device manufacturers, software developers, system integrators, and end users benefit from the evolving ecosystem that promotes innovation, scalability, and integration with emerging technologies like IoT and AI. The market's growth trajectory aligns with increasing investments in mobile computing infrastructure, regulatory support for digitalization, and growing awareness of the benefits of rugged and wearable PDA solutions.

Competitive Landscape

The competitive landscape of the Global Mobile Computer (PDA) Market is characterized by intense rivalry among established multinational corporations and emerging regional players. Companies compete through innovation, product differentiation, and strategic partnerships, focusing on delivering ruggedness, advanced connectivity, and integration capabilities to meet diverse industry requirements. Pricing strategies vary, with premium segments emphasizing durability and advanced features, while cost-effective solutions target emerging markets. Market entry barriers include technological complexity, certification requirements, and significant R&D investments. Leading players adopt mergers and acquisitions, joint ventures, and collaborations to expand geographic reach and enhance product portfolios. The proliferation of IoT and AI integration is shaping competitive dynamics by enabling smarter and more connected PDA solutions. Distribution channels span direct sales, channel partners, and e-commerce platforms, facilitating widespread market penetration. Future trends suggest increasing focus on wearable PDAs and cloud-based software solutions to address evolving customer needs and operational challenges globally.

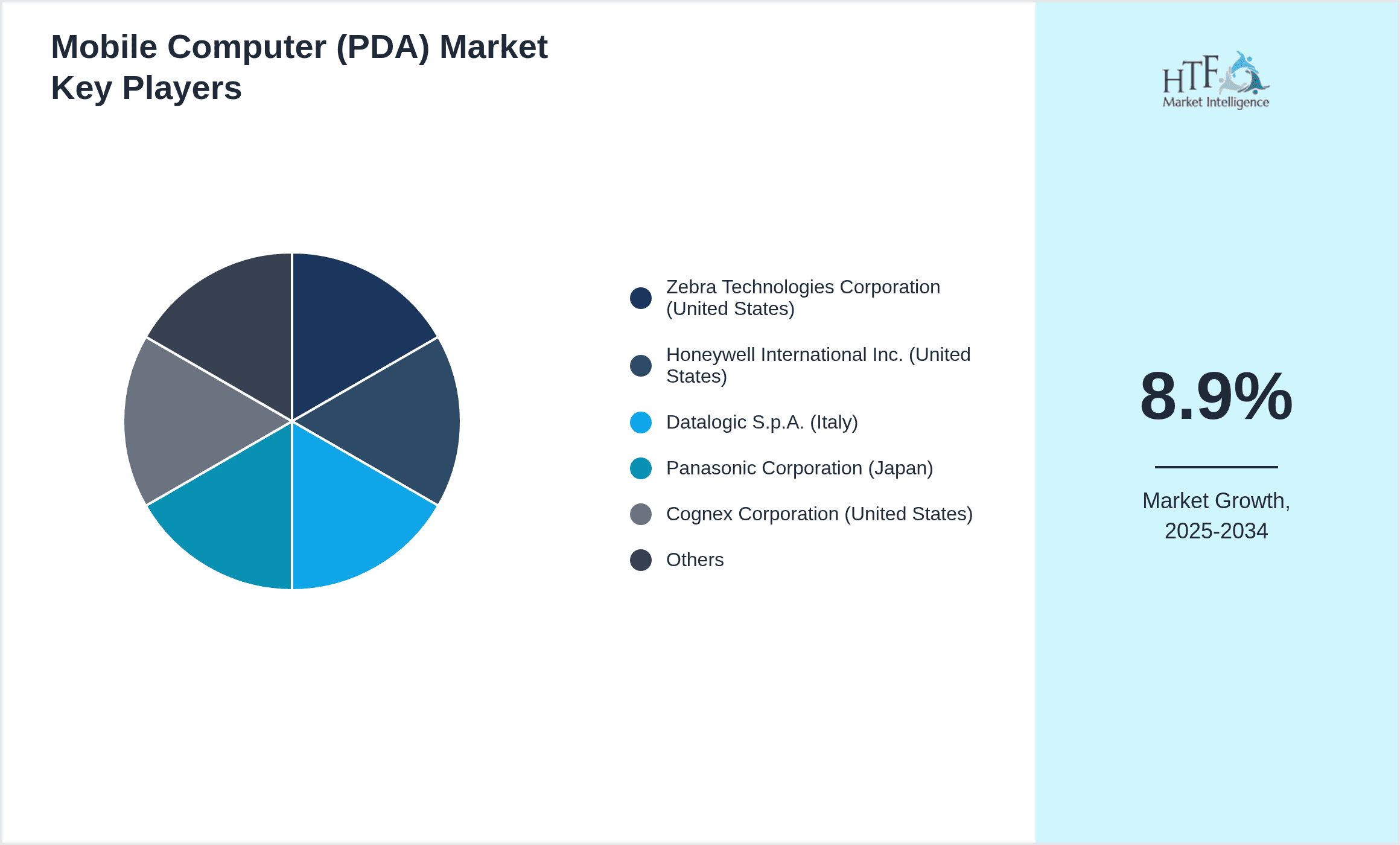

Leading Companies in Mobile Computer (PDA) Market

- •Zebra Technologies Corporation (United States)

- •Honeywell International Inc. (United States)

- •Datalogic S.p.A. (Italy)

- •Panasonic Corporation (Japan)

- •Cognex Corporation (United States)

- •CipherLab Co., Ltd. (Taiwan)

- •Intermec Inc. (United States)

- •Unitech Electronics Co., Ltd. (Taiwan)

- •Psion Teklogix Inc. (United Kingdom)

- •Bluebird Inc. (South Korea)

- •Opticon Sensors Europe B.V. (Netherlands)

- •Motorola Solutions Inc. (United States)

- •Samsung Electronics Co., Ltd. (South Korea)

- •Honeywell Scanning & Mobility (United States)

- •Casio Computer Co., Ltd. (Japan)

- •Getac Technology Corporation (Taiwan)

- •Denso Wave Incorporated (Japan)

- •Toshiba Tec Corporation (Japan)

- •Newland Auto-ID Tech Co., Ltd. (China)

- •Advantech Co., Ltd. (Taiwan)

- •Honeywell Safety and Productivity Solutions (United States)

- •Janam Technologies LLC (United States)

- •Bluebird Inc. (South Korea)

- •CipherLab Co., Ltd. (Taiwan)

- •Panasonic Corporation (Japan)

Market Breakdown

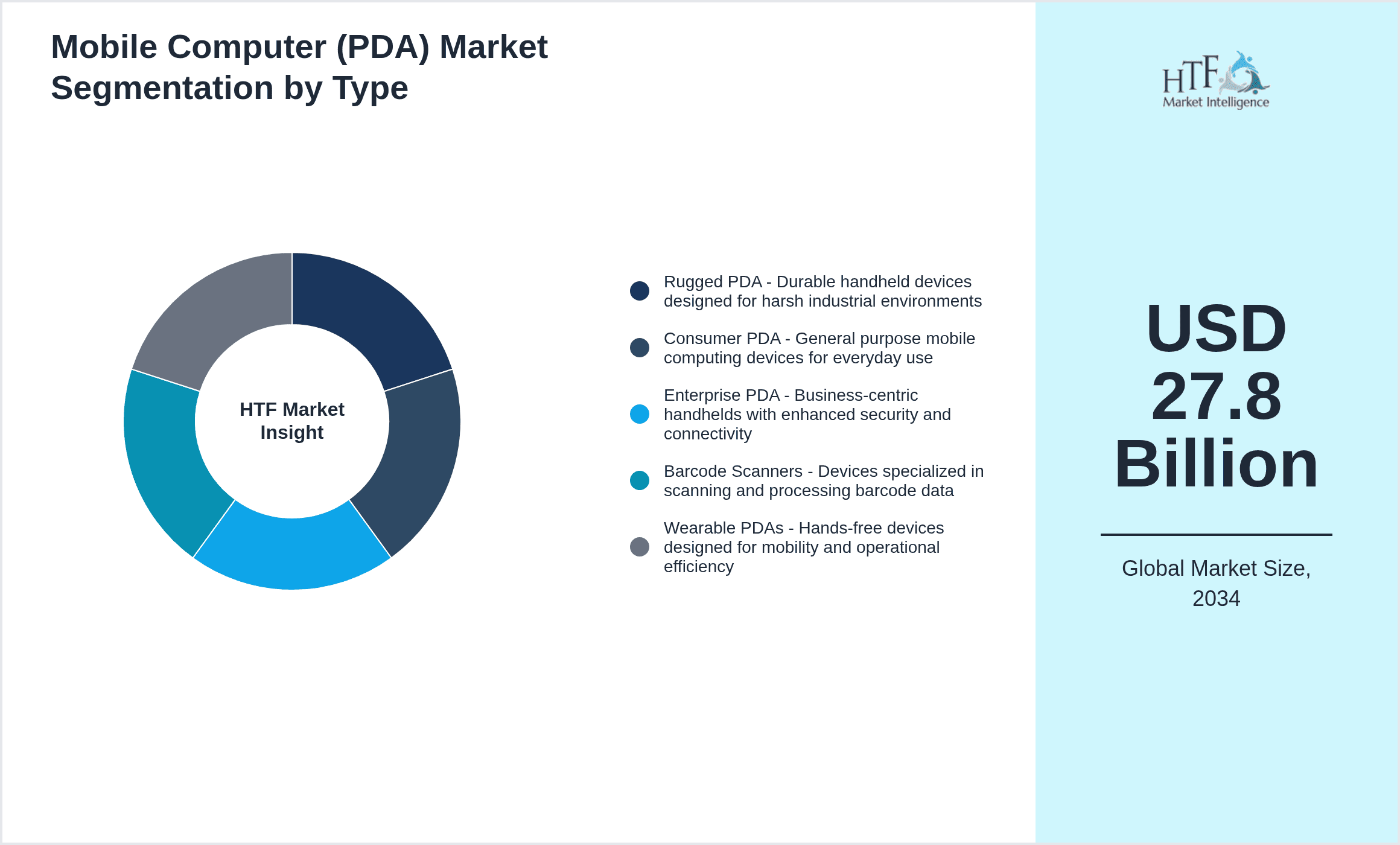

- •By Product Type

- ◦Rugged PDA - Durable handheld devices designed for harsh industrial environments

- ◦Consumer PDA - General purpose mobile computing devices for everyday use

- ◦Enterprise PDA - Business-centric handhelds with enhanced security and connectivity

- ◦Barcode Scanners - Devices specialized in scanning and processing barcode data

- ◦Wearable PDAs - Hands-free devices designed for mobility and operational efficiency

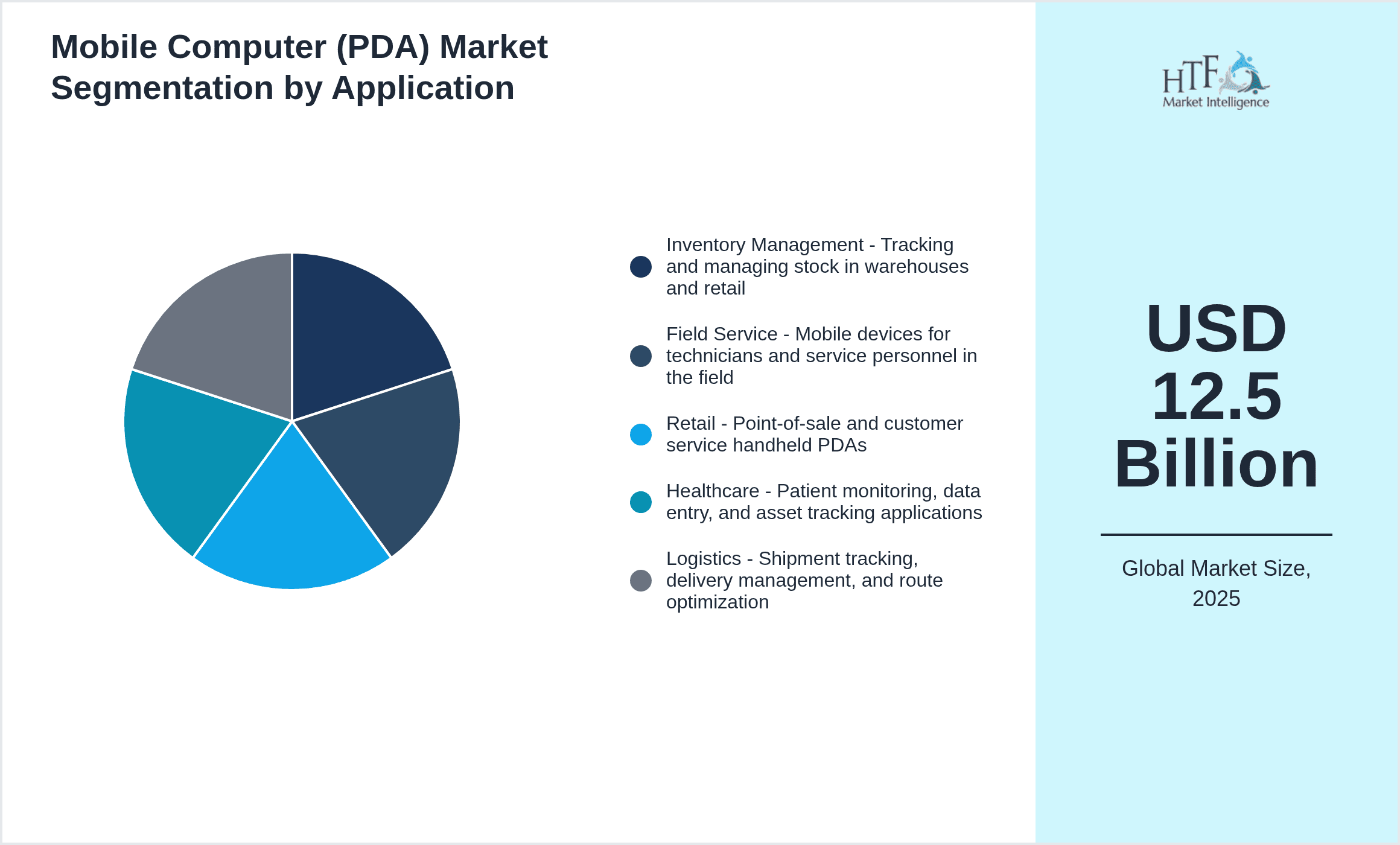

- •By Application

- ◦Inventory Management - Tracking and managing stock in warehouses and retail

- ◦Field Service - Mobile devices for technicians and service personnel in the field

- ◦Retail - Point-of-sale and customer service handheld PDAs

- ◦Healthcare - Patient monitoring, data entry, and asset tracking applications

- ◦Logistics - Shipment tracking, delivery management, and route optimization

- •By End-Use Industry

- ◦Manufacturing - Production monitoring and quality control

- ◦Transportation & Logistics - Fleet management and cargo tracking

- ◦Healthcare - Clinical data management and patient care

- ◦Retail - Sales operations and inventory control

- •By Distribution Channel

- ◦Direct Sales - Manufacturer to end-user transactions

- ◦Channel Partners - Resellers, distributors, and system integrators

- ◦Online Retail - E-commerce platforms for device sales

Growth Dynamics

- •Increasing demand for real-time data capture and mobile workforce enablement is driving the adoption of mobile computers globally. Industries such as retail and logistics leverage PDAs to improve operational efficiency and accuracy, reducing manual errors significantly.

- •Technological advancements in wireless communication, including 5G and Wi-Fi 6, are enhancing PDA connectivity, enabling faster data transmission and improved device performance in remote and challenging environments.

- •Growing adoption of rugged and wearable PDAs in harsh industrial and field service environments is fueling market growth. These devices offer durability, hands-free operation, and extended battery life critical for demanding applications.

- •The expansion of e-commerce and omni-channel retailing is increasing the need for efficient inventory management and real-time stock monitoring, thereby boosting demand for mobile computers in retail supply chains.

- •Government initiatives promoting digitalization and Industry 4.0 adoption in emerging economies are creating new growth avenues for mobile computer devices across sectors such as manufacturing and healthcare.

- •Integration of AI and IoT technologies with PDAs is enabling smarter analytics and predictive maintenance, enhancing device utility and opening new market opportunities.

- •Strategic partnerships between hardware manufacturers and software developers are fostering innovative solutions tailored to specific industry needs, driving product adoption and customer satisfaction.

Market Trends

- •There is a rising trend towards the deployment of wearable PDAs that facilitate hands-free operations, particularly in logistics and field services, improving worker productivity and safety.

- •Sustainability-focused product designs are gaining traction, with manufacturers emphasizing energy-efficient devices and recyclable materials to meet regulatory and customer demands.

- •Cloud-based software integration with mobile computers is becoming prevalent, enabling seamless data synchronization, remote management, and enhanced security features.

- •The shift towards ruggedized devices continues as enterprises prioritize durability and reliability in extreme environmental conditions, reducing downtime and maintenance costs.

- •Collaborative ecosystems involving device manufacturers, software providers, and channel partners are emerging to deliver end-to-end mobile computing solutions tailored to industry-specific requirements.

- •Consumer-grade PDAs are being enhanced with enterprise features to cater to small and medium-sized businesses seeking affordable yet capable mobile computing solutions.

- •Advancements in biometric authentication and embedded sensors in PDAs are improving device security and operational efficiency, aligning with increasing cybersecurity concerns.

Market Opportunities

- •Expanding applications of PDAs in emerging sectors such as healthcare for patient monitoring and asset management present significant growth potential driven by increasing digitization efforts.

- •Untapped markets in Latin America and Middle East & Africa offer opportunities for market expansion due to rising industrialization and infrastructure development.

- •Investment in research and development focusing on wearable and AI-enabled PDAs can unlock innovation-led growth and competitive advantage.

- •Geographical expansion through partnerships and localized product offerings can help companies penetrate diverse markets with tailored solutions addressing regional needs.

- •Developing integrated software platforms with mobile hardware enhances value propositions for end users seeking comprehensive mobility solutions.

- •Strategic acquisitions and alliances can accelerate technology adoption and broaden product portfolios, enabling faster market access and customer reach.

- •Regulatory support for digital transformation, especially in public sector and healthcare, is expected to create new demand channels for mobile computers.

Market Challenges

- •High initial investment and total cost of ownership for rugged and enterprise PDAs can deter adoption among small and medium-sized enterprises, limiting market penetration.

- •Rapid technological obsolescence requires continuous innovation and product updates, imposing significant R&D and supply chain burdens on manufacturers.

- •Interoperability issues between mobile computers and legacy enterprise systems can complicate integration efforts and increase deployment costs.

- •Stringent regulatory compliance and certification processes vary by region, posing challenges to global product standardization and market entry.

- •Competition from smartphones and tablets equipped with similar functionalities may reduce demand for dedicated PDA devices in certain segments.

- •Supply chain disruptions and component shortages, as witnessed during global crises, impact production schedules and market availability.

- •Security concerns related to data breaches and device tampering necessitate robust cybersecurity measures, increasing complexity and cost.

Regulatory Framework

- •The General Data Protection Regulation (GDPR) enacted in 2018 in Europe has necessitated stringent data security and privacy features in mobile computing devices, influencing product design and compliance frameworks globally.

- •The Federal Communications Commission (FCC) regulations between 2018 and 2025 mandate wireless device certifications and electromagnetic compatibility standards, ensuring safe and reliable PDA operations in the United States.

- •RoHS Directive (Restriction of Hazardous Substances) updated in 2021 enforces limits on hazardous materials in electronic devices, impacting component sourcing and manufacturing processes worldwide.

- •The ISO 9001 quality management standards applied to manufacturing processes from 2019 onwards require continuous quality control and risk management practices across the PDA production lifecycle.

- •Regional mandates on electronic waste management, including the WEEE Directive in Europe, have imposed responsibilities on manufacturers for device recycling and environmental sustainability since 2020.

Market Intelligence

- •15th January 2025, Zebra Technologies Corporation launched its next-generation rugged PDA featuring enhanced 5G connectivity, extended battery life, and advanced thermal imaging capabilities aimed at logistics and field service sectors. This device supports seamless integration with cloud platforms and AI-driven analytics, enabling enterprises to optimize operations and reduce downtime. The launch aligns with increasing demand for durable, high-performance mobile computing devices in harsh environments worldwide. Zebra's strategic focus on innovation and customer-centric design is expected to strengthen its market leadership and expand its global footprint. Source: Official Zebra Technologies Press Release

- •20th March 2025, Honeywell International Inc. introduced its wearable PDA series integrating augmented reality (AR) with voice recognition technology tailored for healthcare and manufacturing industries. These devices provide hands-free operation and real-time data visualization, enhancing worker productivity and safety. The innovation reflects growing market trends towards wearable computing and smart device convergence. Honeywell's initiative demonstrates its commitment to advancing mobile computing capabilities to meet evolving customer demands and regulatory requirements. Source: Honeywell Corporate Website

- •5th June 2025, Datalogic S.p.A. announced a strategic partnership with a leading cloud services provider to develop integrated mobile computing solutions combining rugged PDAs with IoT analytics platforms. This collaboration aims to deliver comprehensive end-to-end solutions for supply chain optimization and asset management. The partnership is expected to accelerate adoption of smart mobile devices in logistics and retail sectors, driving revenue growth and competitive differentiation. Datalogic's approach underscores the importance of ecosystem collaboration in the rapidly evolving mobile computer market. Source: Industry Publication - Logistics Tech News

- •10th September 2025, Panasonic Corporation completed the acquisition of a niche wearable PDA manufacturer specializing in healthcare applications, expanding its product portfolio and market presence in Asia-Pacific. This strategic move enables Panasonic to offer specialized solutions addressing clinical workflow challenges and asset tracking in hospitals. The acquisition supports Panasonic's growth strategy focusing on innovation and regional market expansion, leveraging synergies in technology and customer base. It is anticipated to enhance Panasonic's competitiveness in the global mobile computer market. Source: Panasonic Official Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 27.8 Billion |

| CAGR | 8.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.5% |

| Scope of Report | Market is segmented by Product Type (Rugged PDA - Durable handheld devices designed for harsh industrial environments, Consumer PDA - General purpose mobile computing devices for everyday use, Enterprise PDA - Business-centric handhelds with enhanced security and connectivity, Barcode Scanners - Devices specialized in scanning and processing barcode data, Wearable PDAs - Hands-free devices designed for mobility and operational efficiency), Application (Inventory Management - Tracking and managing stock in warehouses and retail, Field Service - Mobile devices for technicians and service personnel in the field, Retail - Point-of-sale and customer service handheld PDAs, Healthcare - Patient monitoring, data entry, and asset tracking applications, Logistics - Shipment tracking, delivery management, and route optimization), End-Use Industry (Manufacturing - Production monitoring and quality control, Transportation & Logistics - Fleet management and cargo tracking, Healthcare - Clinical data management and patient care, Retail - Sales operations and inventory control), Distribution Channel (Direct Sales - Manufacturer to end-user transactions, Channel Partners - Resellers, distributors, and system integrators, Online Retail - E-commerce platforms for device sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Zebra Technologies Corporation (United States), Honeywell International Inc. (United States), Datalogic S.p.A. (Italy), Panasonic Corporation (Japan), Cognex Corporation (United States) |

Global Mobile Computer (PDA) Market Size, Growth & Revenue 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Market market is projected to grow at a steady CAGR from 2025 to 2030, driven by increasing demand and expansion in various applications.

North America currently leads the market, followed by Europe and Asia-Pacific.

Key growth drivers include increasing activities, rising demand for innovative solutions, technological advancements, and growing preference for efficient products.