Global Smart Ward Market Size, Growth & Revenue 2025-2034

Global Smart Ward Market is segmented by Product Type (IoT Devices, Software Platforms, Connectivity Solutions, Security Systems, AI & ML Tools), Application (Patient Monitoring, Asset Management, Staff Coordination, Environmental Control, Data Analytics), End-Use Industry (Hospitals, Clinics, Long-Term Care Facilities, Ambulatory Surgery Centers), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Smart Ward market integrates cutting-edge healthcare technologies such as IoT devices, AI & ML platforms, and advanced connectivity solutions to modernize hospital ward management. These innovations focus on critical applications like patient monitoring, asset tracking, staff coordination, and environmental control, delivering real-time data analytics to improve patient outcomes and operational efficiency. Serving a wide range of healthcare providers including hospitals, clinics, and elder care facilities, the market's ecosystem comprises device manufacturers, software providers, and integrators. The value chain emphasizes interoperability, security, compliance, and scalable deployment, reflecting the sector's complexity and innovation dynamics. From 2020 to 2025, the market experienced steady growth driven by healthcare digitization and rising demand for remote patient monitoring. Forecasts to 2034 project robust expansion, fueled by AI integration and increasing adoption in emerging regions. This market is pivotal for enhancing patient safety, reducing healthcare costs, and enabling predictive healthcare management globally.

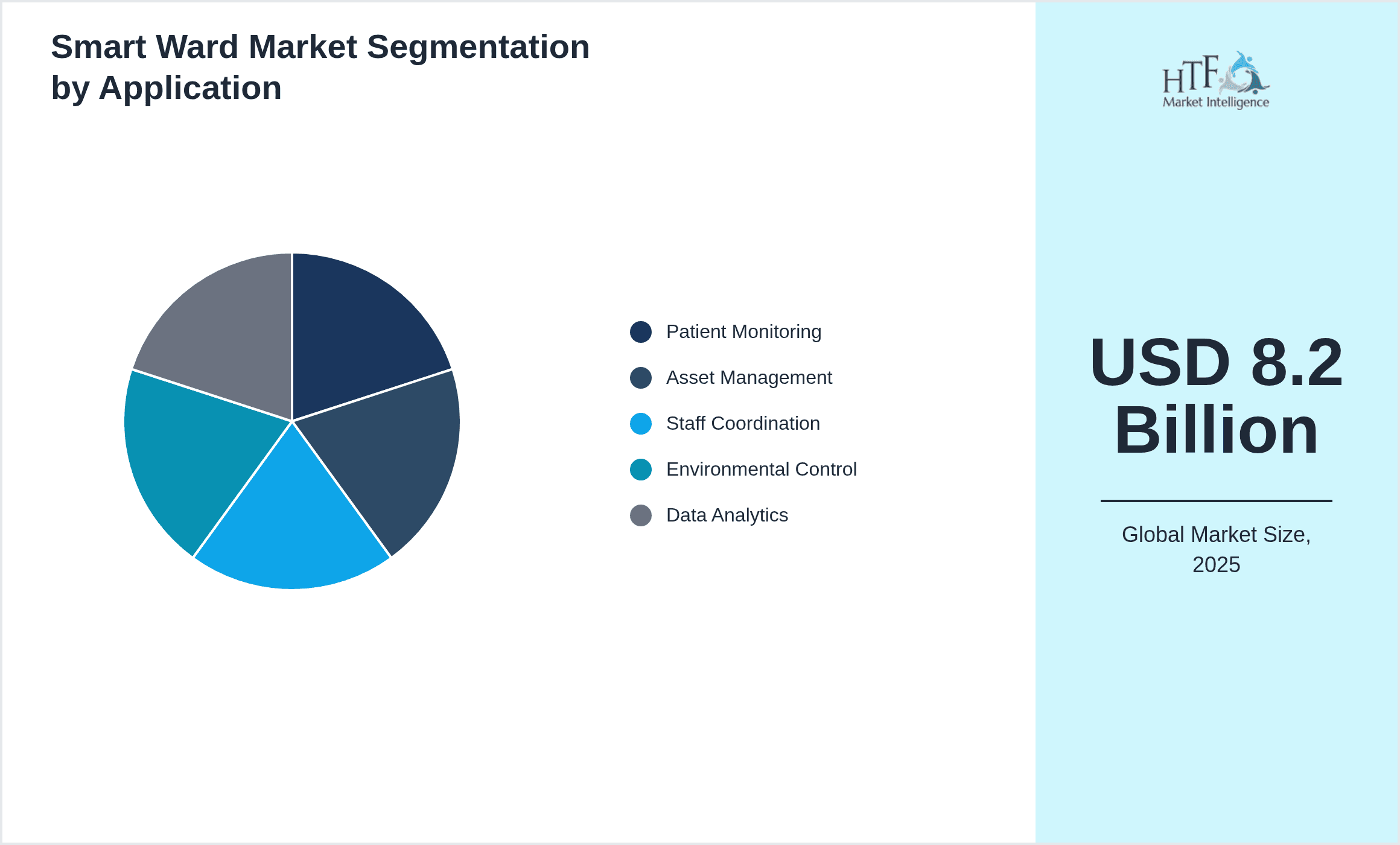

- •Key market highlights include a base market size of USD 8.2 Billion in 2025, forecasted to reach USD 24.7 Billion by 2034, representing a CAGR of 12.5%. North America currently dominates the market, driven by advanced healthcare infrastructure and high technology adoption rates, while Asia-Pacific is identified as the fastest-growing region due to increasing investments and digital transformation initiatives. IoT devices lead the product segment, providing foundational connectivity and monitoring capabilities, whereas AI & ML tools are the fastest-growing product type, enabling advanced analytics and automation. Market drivers include rising chronic diseases, government healthcare initiatives, and the push for operational efficiencies. Challenges such as data security concerns and integration complexities remain, yet opportunities in emerging markets and technology advancements present significant growth avenues.

- •The Smart Ward market offers substantial value propositions to healthcare providers by enhancing patient safety, streamlining workflows, and enabling predictive maintenance of assets. Strategic importance extends to technology vendors and system integrators focusing on delivering integrated solutions that address evolving regulatory requirements and interoperability standards. As healthcare systems worldwide prioritize digital transformation, the Smart Ward market underpins future-ready hospital infrastructures, improves clinical decision-making, and supports better patient engagement and satisfaction. Stakeholders benefit from scalable, flexible solutions aligned with the global push towards value-based care and remote health monitoring.

Competitive Landscape

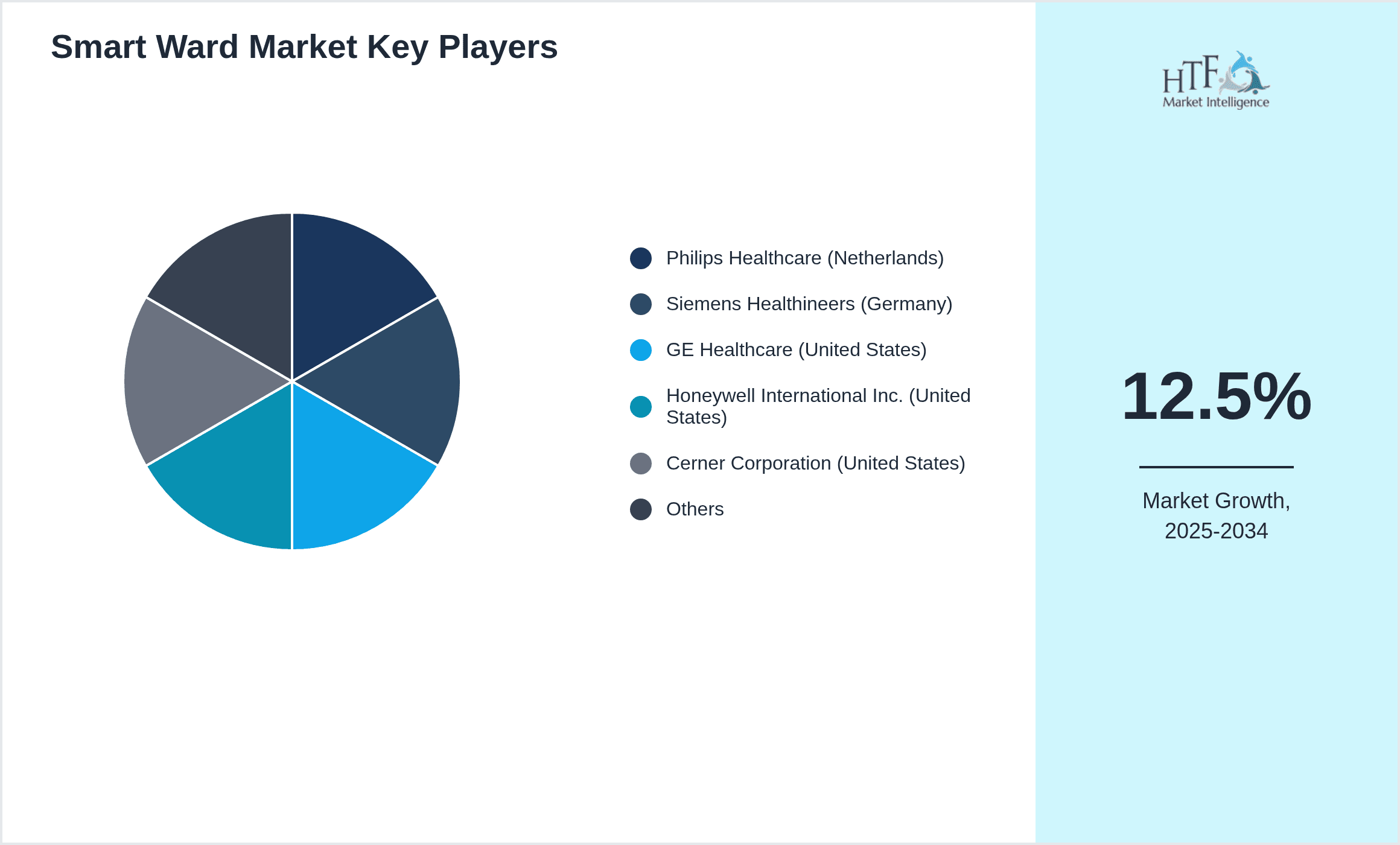

The global Smart Ward market is characterized by intense competition among technology providers, device manufacturers, and integrators focusing on innovation, strategic partnerships, and market expansion. Companies differentiate themselves by investing heavily in R&D to develop AI-enabled analytics, interoperable IoT platforms, and secure connectivity solutions. Market entrants face barriers such as high capital requirements, stringent regulatory compliance, and the need for robust data security frameworks. Leading players adopt multi-channel distribution strategies and establish collaborations with healthcare institutions to expand their footprint. Mergers and acquisitions are common for consolidating technology portfolios and enhancing market reach. Regional competition is influenced by local healthcare infrastructure maturity and government support, fostering diverse growth trajectories. Future trends indicate increased focus on cloud-based solutions, edge computing, and patient-centric services, reinforcing competitiveness in this dynamic landscape.

Leading Companies in Smart Ward Market

- •Philips Healthcare (Netherlands)

- •Siemens Healthineers (Germany)

- •GE Healthcare (United States)

- •Honeywell International Inc. (United States)

- •Cerner Corporation (United States)

- •IBM Corporation (United States)

- •Medtronic plc (Ireland)

- •Cisco Systems, Inc. (United States)

- •Samsung Electronics (South Korea)

- •Honeywell Life Care Solutions (United States)

- •Honeywell Safety and Productivity Solutions (United States)

- •Hill-Rom Holdings, Inc. (United States)

- •Qualcomm Incorporated (United States)

- •Nokia Corporation (Finland)

- •Cisco Systems, Inc. (United States)

- •Zebra Technologies Corporation (United States)

- •Toshiba Medical Systems Corporation (Japan)

- •Honeywell International Inc. (United States)

- •Intel Corporation (United States)

- •Honeywell Life Care Solutions (United States)

- •Johnson & Johnson (United States)

- •Schneider Electric SE (France)

- •Honeywell Safety and Productivity Solutions (United States)

- •Fujifilm Holdings Corporation (Japan)

- •Honeywell International Inc. (United States)

Market Breakdown

- •By Product Type

- ◦IoT Devices

- ◦Software Platforms

- ◦Connectivity Solutions

- ◦Security Systems

- ◦AI & ML Tools

- •By Application

- ◦Patient Monitoring

- ◦Asset Management

- ◦Staff Coordination

- ◦Environmental Control

- ◦Data Analytics

- •By End-Use Industry

- ◦Hospitals

- ◦Clinics

- ◦Long-Term Care Facilities

- ◦Ambulatory Surgery Centers

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

- •Increasing prevalence of chronic diseases globally has elevated the demand for continuous patient monitoring solutions within smart wards, leading to enhanced adoption of IoT devices and remote monitoring tools. This trend is supported by technological advancements enabling real-time data capture and analytics, improving clinical outcomes and reducing hospital readmission rates.

- •Government initiatives and healthcare policies focusing on digital transformation and smart hospital infrastructure investments have accelerated the deployment of smart ward technologies, particularly in developed regions. Subsidies and funding programs further stimulate market growth by lowering adoption barriers for healthcare providers.

- •The integration of AI and machine learning in smart ward solutions is revolutionizing operational workflows by enabling predictive analytics, automated alerts, and intelligent resource allocation. These capabilities increase efficiency, reduce human error, and enhance patient safety, driving demand for advanced AI-powered platforms.

- •Rising patient expectations for improved healthcare experiences and personalized care are encouraging hospitals to adopt smart ward technologies that facilitate seamless communication between staff and patients, as well as environmental controls tailored to patient preferences.

- •Emerging markets in Asia-Pacific and Latin America are witnessing rapid growth due to increasing healthcare expenditure, urbanization, and awareness about smart healthcare solutions, presenting significant opportunities for market players to expand their presence and customize offerings to local needs.

- •Collaborations between technology providers, healthcare institutions, and research organizations foster innovation and accelerate the development of integrated smart ward ecosystems, enhancing market competitiveness and value delivery.

- •The shift towards value-based care models emphasizes outcome-driven healthcare delivery, incentivizing adoption of smart ward technologies that provide measurable improvements in clinical outcomes and cost efficiencies.

Market Trends

- •Adoption of IoT-enabled wearable devices and sensors is expanding within smart wards, enabling continuous and non-invasive patient monitoring that improves data accuracy and patient comfort. This trend is supported by advancements in battery technology and wireless communication protocols.

- •Cloud computing and edge computing integration in smart ward solutions facilitates efficient data processing, storage, and accessibility, allowing healthcare providers to leverage scalable infrastructure and real-time analytics while ensuring data privacy and security compliance.

- •Increased focus on cybersecurity measures within healthcare IT ecosystems is driving the deployment of advanced security systems in smart wards, addressing concerns related to data breaches, ransomware attacks, and unauthorized access to sensitive patient information.

- •Sustainability initiatives are influencing smart ward design, with hospitals adopting energy-efficient devices and environmentally friendly materials to reduce carbon footprints and operational costs while aligning with global environmental standards.

- •Collaborative platforms and integrated communication tools are gaining traction, enabling multidisciplinary teams to coordinate care effectively within smart wards, thereby enhancing clinical workflows and patient engagement.

- •Personalized patient environments leveraging smart lighting, temperature control, and noise management are becoming standard features, contributing to improved patient satisfaction and faster recovery times.

- •The rise of telehealth and remote consultation services complements smart ward technologies, enabling continuous patient care beyond hospital walls and expanding healthcare accessibility.

Market Opportunities

- •Expanding into emerging markets presents significant growth potential due to increasing healthcare investments, rising patient populations, and growing awareness of smart healthcare solutions. Tailored product offerings and localized partnerships can accelerate adoption in these regions.

- •Innovation in AI-powered predictive analytics and decision support systems offers opportunities to enhance clinical outcomes and operational efficiencies within smart wards, attracting healthcare providers seeking advanced technology adoption.

- •Development of interoperable platforms that seamlessly integrate with existing hospital IT infrastructure can reduce deployment complexities and increase customer retention, creating competitive advantages for solution providers.

- •Collaborations with government health agencies and participation in public health initiatives can unlock funding opportunities and foster large-scale smart ward implementations, particularly in regions emphasizing digital health transformation.

- •Integration of wearable and mobile health technologies with smart ward systems can enhance remote patient monitoring capabilities, expanding service offerings and creating new revenue streams.

- •Growing demand for patient-centric care models encourages development of customizable smart ward environments, increasing market differentiation and customer satisfaction.

- •Investing in cybersecurity enhancements tailored for healthcare environments addresses a critical market need and builds trust among stakeholders, facilitating market penetration.

Market Challenges

- •Data privacy and security concerns remain significant barriers to smart ward adoption, with healthcare providers facing stringent regulations and risks of cyberattacks that can compromise sensitive patient information.

- •Integration complexities due to heterogeneous hospital IT systems and legacy infrastructure hinder seamless deployment of smart ward technologies, increasing implementation costs and timelines.

- •High initial investment costs for advanced smart ward solutions can deter smaller healthcare facilities and limit market penetration in cost-sensitive regions.

- •Lack of standardized protocols and interoperability frameworks across devices and platforms creates challenges in achieving cohesive smart ward ecosystems.

- •Resistance to change among healthcare staff due to training requirements and workflow disruptions may slow adoption rates and impact technology utilization efficiency.

- •Regulatory uncertainties and evolving compliance requirements across different regions add complexity to market entry and product certification processes.

- •Supply chain disruptions and component shortages can affect the timely delivery and scalability of smart ward deployments.

Regulatory Framework

- •The Health Insurance Portability and Accountability Act (HIPAA) amendments between 2020 and 2025 mandate strict data privacy and security standards for patient information, significantly influencing smart ward solution designs to ensure compliance and safeguard healthcare data.

- •The European Union’s Medical Device Regulation (MDR) enacted in 2021 introduced rigorous safety and performance requirements for medical devices, impacting manufacturers of IoT devices and software platforms used within smart wards across Europe.

- •FDA’s Digital Health Innovation Action Plan, updated through 2020-2025, provides streamlined pathways for approval of AI-based medical software and connected health devices, facilitating faster market entry while ensuring patient safety.

- •Data protection regulations such as the General Data Protection Regulation (GDPR) enforced in the EU since 2018, with ongoing updates through 2025, impose strict controls on data processing and cross-border transfer, influencing smart ward data management practices.

- •Government initiatives like the US 21st Century Cures Act promote interoperability and prohibit information blocking, encouraging development of integrated smart ward systems that support seamless health information exchange.

Market Intelligence

- •15th January 2025, Philips Healthcare launched its next-generation IoT-enabled patient monitoring system designed for smart wards, featuring enhanced AI-driven analytics, interoperability with hospital EMR systems, and improved wireless connectivity. This solution targets large hospitals aiming to optimize patient care workflows and reduce manual monitoring errors. The launch is expected to strengthen Philips' leadership in the smart ward technology market by addressing critical operational challenges and enabling predictive health management. Source: Philips Healthcare Official Press Release

- •10th March 2025, Siemens Healthineers introduced an advanced AI-powered staff coordination platform that integrates with existing hospital infrastructure to optimize shift scheduling, task allocation, and emergency response within smart wards. The platform leverages machine learning algorithms to predict workload demands and improve staff efficiency, reducing burnout and enhancing patient care quality. This innovation aligns with growing healthcare trends prioritizing workforce management and digital transformation. Source: Siemens Healthineers Corporate Announcement

- •22nd May 2024, GE Healthcare announced a strategic partnership with a leading cloud service provider to develop scalable connectivity solutions for smart wards, focusing on secure data transmission and real-time analytics. This collaboration aims to accelerate adoption of cloud-based smart ward platforms, especially in emerging markets, by offering flexible and cost-effective infrastructure options. The initiative underscores industry efforts to leverage cloud computing for healthcare digitalization. Source: GE Healthcare Press Release

- •5th November 2024, Honeywell International completed the acquisition of a cybersecurity firm specializing in healthcare IT security, enhancing its portfolio of secure connectivity and data protection solutions for smart wards. This acquisition is expected to address increasing concerns over healthcare data breaches and regulatory compliance, positioning Honeywell as a comprehensive provider of secure smart ward technologies. The deal reflects a broader market trend towards integrating cybersecurity within healthcare technology ecosystems. Source: Honeywell Official Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.2 Billion |

| Forecast Year Market Size | USD 24.7 Billion |

| CAGR | 12.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12% |

| Scope of Report | Market is segmented by Product Type (IoT Devices, Software Platforms, Connectivity Solutions, Security Systems, AI & ML Tools), Application (Patient Monitoring, Asset Management, Staff Coordination, Environmental Control, Data Analytics), End-Use Industry (Hospitals, Clinics, Long-Term Care Facilities, Ambulatory Surgery Centers), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Philips Healthcare (Netherlands), Siemens Healthineers (Germany), GE Healthcare (United States), Honeywell International Inc. (United States), Cerner Corporation (United States), IBM Corporation (United States), Medtronic plc (Ireland), Cisco Systems, Inc. (United States), Samsung Electronics (South Korea), Honeywell Life Care Solutions (United States), Honeywell Safety and Productivity Solutions (United States), Hill-Rom Holdings, Inc. (United States), Qualcomm Incorporated (United States), Nokia Corporation (Finland), Cisco Systems, Inc. (United States), Zebra Technologies Corporation (United States), Toshiba Medical Systems Corporation (Japan), Honeywell International Inc. (United States), Intel Corporation (United States), Honeywell Life Care Solutions (United States), Johnson & Johnson (United States), Schneider Electric SE (France), Honeywell Safety and Productivity Solutions (United States), Fujifilm Holdings Corporation (Japan), Honeywell International Inc. (United States) |

Global Smart Ward Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.