Global Single-use Hysteroscopy Instruments Market Size, Growth & Revenue 2025-2034

Global Single-use Hysteroscopy Instruments Market is segmented by Product Type (Flexible Hysteroscopes, Rigid Hysteroscopes, Video Hysteroscopes, Fiber Optic Hysteroscopes, Compatible Accessories), Application (Diagnostic Hysteroscopy, Operative Hysteroscopy, Fertility Assessment, Polypectomy, Myomectomy), End-Use Industry (Hospitals, Ambulatory Surgical Centers, Fertility Clinics, Specialty Clinics), Distribution Channel (Direct Sales, Medical Distributors, E-commerce Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Single-use Hysteroscopy Instruments market includes disposable devices designed for minimally invasive diagnostic and operative intrauterine procedures. This market covers a broad range of products including flexible, rigid, video, and fiber optic hysteroscopes used in applications such as diagnostic hysteroscopy, operative hysteroscopy, fertility assessment, polypectomy, and myomectomy. The value chain extends from raw material procurement to manufacturing, distribution, and end-user application in hospitals, ambulatory centers, and fertility clinics. Single-use instruments address significant hygiene challenges by eliminating cross-contamination risks inherent in reusable devices, thereby improving patient safety and reducing sterilization-related operational costs. Technological advancements have enhanced visualization quality and operational ease, driving adoption among gynecologists and fertility specialists worldwide. Market growth is supported by increasing prevalence of uterine disorders, rising demand for minimally invasive procedures, and expanding awareness of reproductive health. Strategic investments and product innovations further propel market expansion, establishing single-use hysteroscopes as essential tools in modern gynecological care.

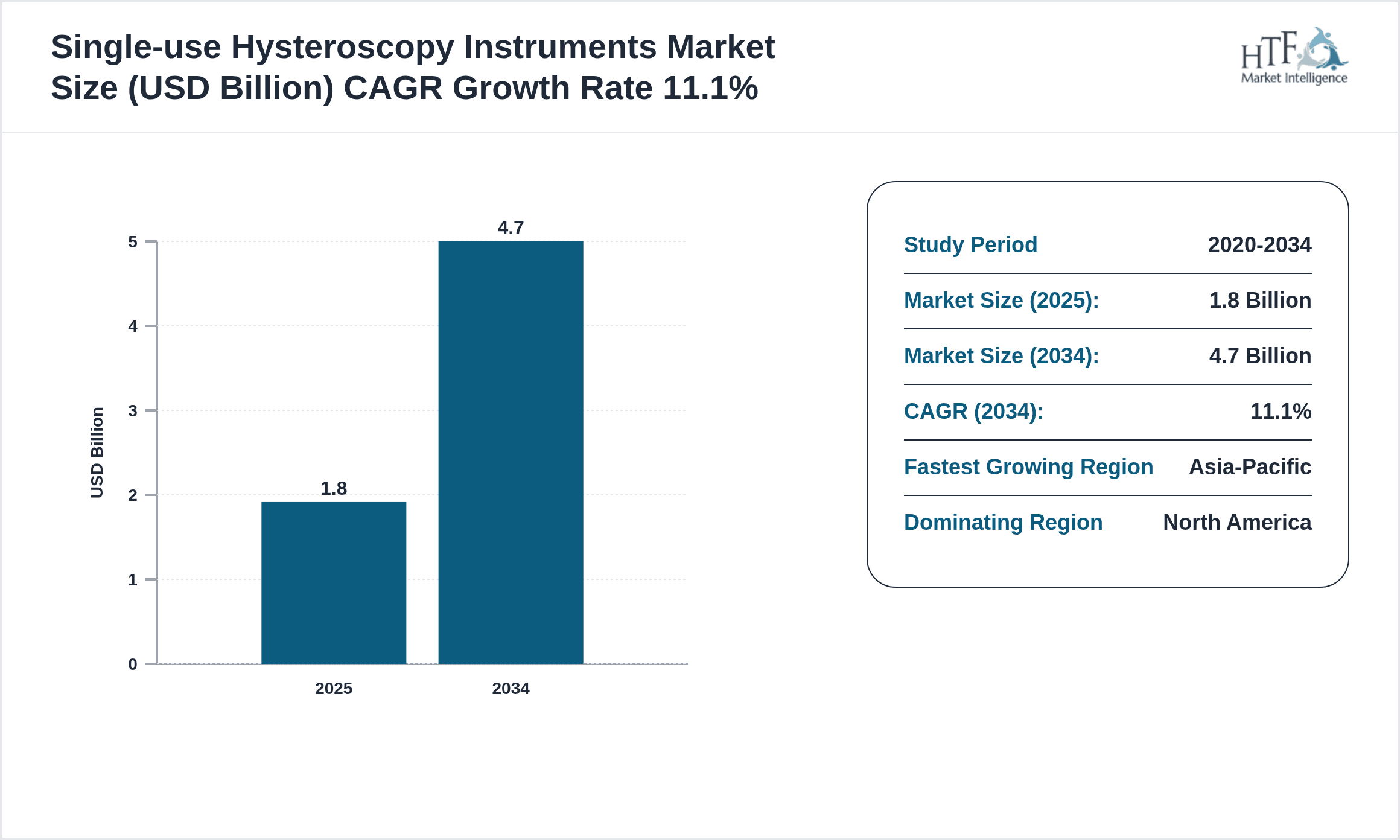

- •Key market highlights include a base market size of USD 1.8 Billion in 2025 with projections to reach USD 4.7 Billion by 2034, representing a robust CAGR of 11.1%. The North American region dominates the market owing to advanced healthcare infrastructure and heightened adoption of single-use technologies. Asia-Pacific is identified as the fastest growing region due to increasing healthcare expenditure and rising awareness of women’s health issues. Rigid hysteroscopes currently lead the product segment; however, flexible hysteroscopes are anticipated to register the fastest growth driven by their enhanced maneuverability and comfort. Market trends indicate rising integration of video capabilities and fiber optic technologies to improve procedural efficacy.

- •The value proposition of single-use hysteroscopy instruments lies in their ability to reduce infection risks, streamline procedural workflows, and lower total cost of ownership by eliminating sterilization requirements. These attributes make them strategically important to hospitals, ambulatory surgical centers, and fertility clinics aiming to improve patient outcomes and operational efficiencies. Furthermore, the market’s growth aligns with global shifts toward minimally invasive surgical techniques and regulatory support for disposable medical devices. Stakeholders including manufacturers, healthcare providers, and investors stand to benefit from innovations and expanding applications within this dynamic market landscape.

Competitive Landscape

The global Single-use Hysteroscopy Instruments market exhibits a competitive environment characterized by a mix of established multinational medical device manufacturers and emerging specialized companies. Market dynamics are influenced by continuous technological innovations, product diversification, and strategic partnerships that enhance portfolio offerings. Leading players focus on developing advanced optics, ergonomic designs, and integrated imaging solutions to differentiate their products. Pricing strategies balance affordability with high-quality standards, addressing diverse healthcare settings from developed to emerging markets. Distribution channels vary from direct hospital supply agreements to collaborations with medical distributors, optimizing market reach. Entry barriers include stringent regulatory approvals and the need for robust clinical validations. Mergers and acquisitions serve as key growth strategies, enabling companies to expand geographic presence and technological capabilities. Regional competition is intense, with North American and European firms leading innovation, while Asia-Pacific companies capitalize on cost advantages and growing local demand. Future trends suggest increased adoption of digital and AI-enhanced hysteroscopy systems, potentially reshaping competitive dynamics.

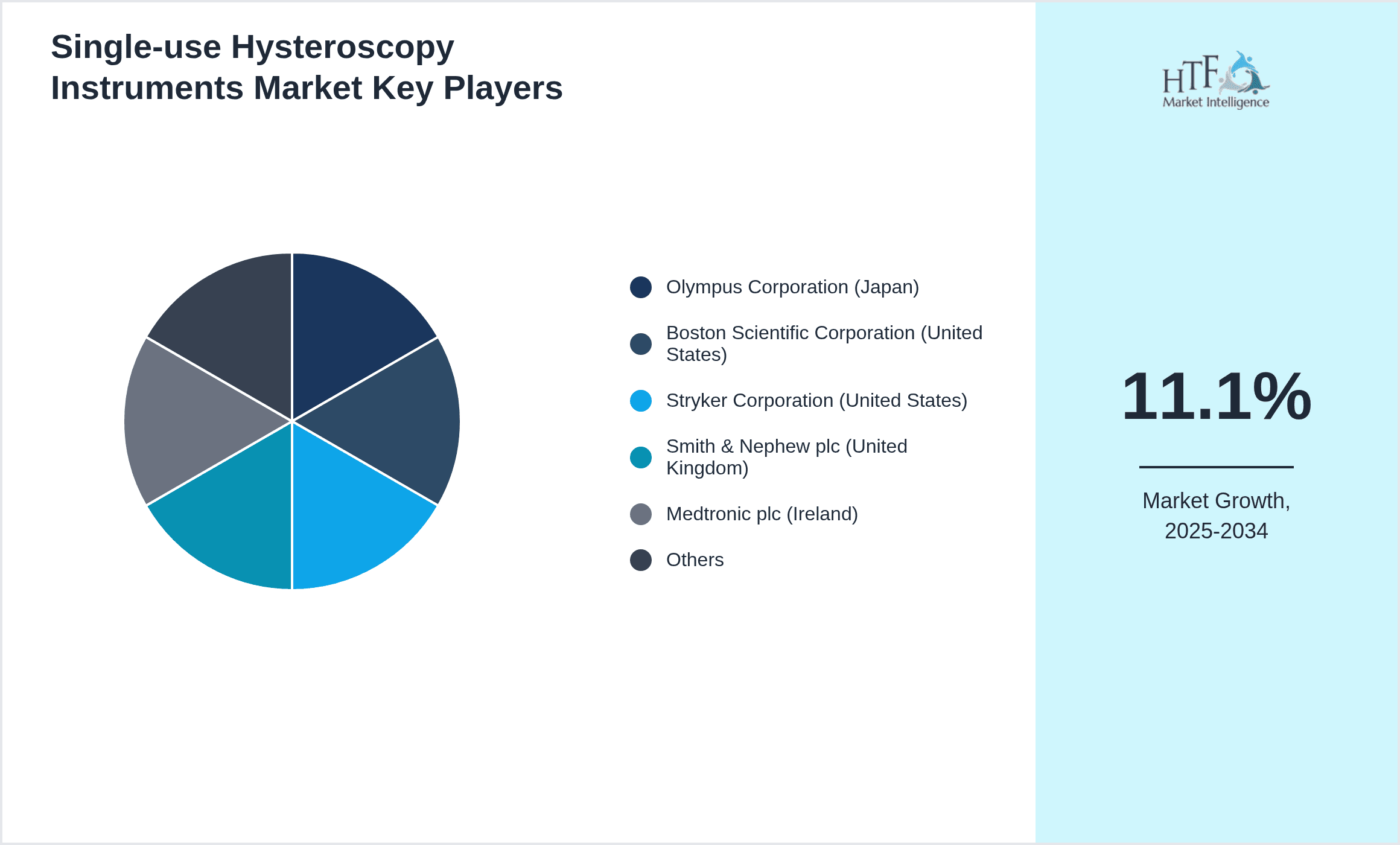

Leading Companies in Single-use Hysteroscopy Instruments Market

- •Olympus Corporation (Japan)

- •Boston Scientific Corporation (United States)

- •Stryker Corporation (United States)

- •Smith & Nephew plc (United Kingdom)

- •Medtronic plc (Ireland)

- •Richard Wolf GmbH (Germany)

- •Karl Storz SE & Co. KG (Germany)

- •Hologic, Inc. (United States)

- •ConMed Corporation (United States)

- •Ambu A/S (Denmark)

- •Cook Medical, LLC (United States)

- •Pentax Medical (Japan)

- •B. Braun Melsungen AG (Germany)

- •Medline Industries, Inc. (United States)

- •Sejong Medical (South Korea)

- •Allium Medical Solutions (Israel)

- •EndoMed Systems (United States)

- •Micro-Tech Endoscopy USA, Inc. (United States)

- •Irvine Scientific (United States)

- •Biosense Webster, Inc. (United States)

- •Nobel Biocare Services AG (Switzerland)

- •Vygon SA (France)

- •SurgiTel, Inc. (United States)

- •Cook Medical (Ireland)

- •LeMaitre Vascular, Inc. (United States)

Market Breakdown

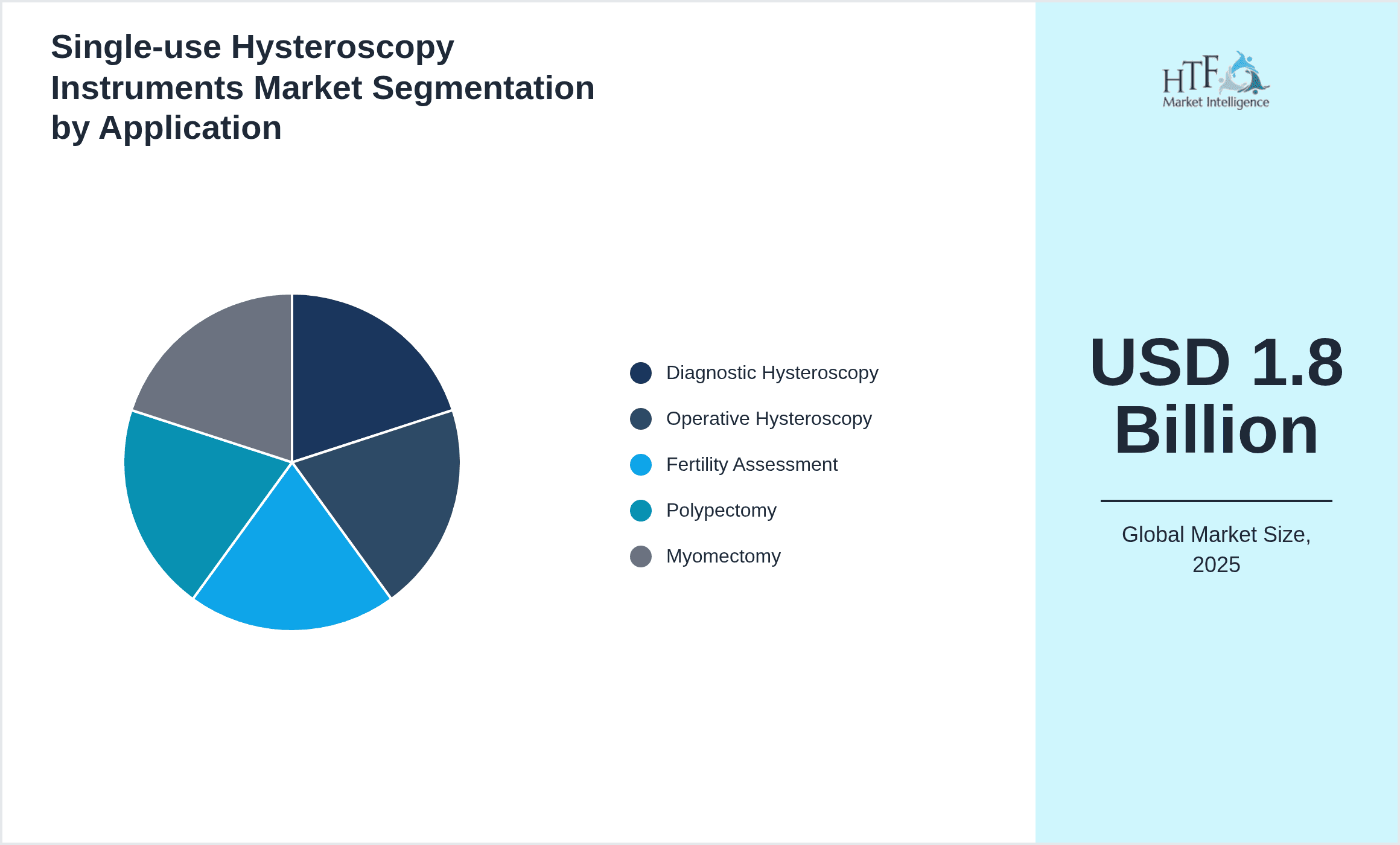

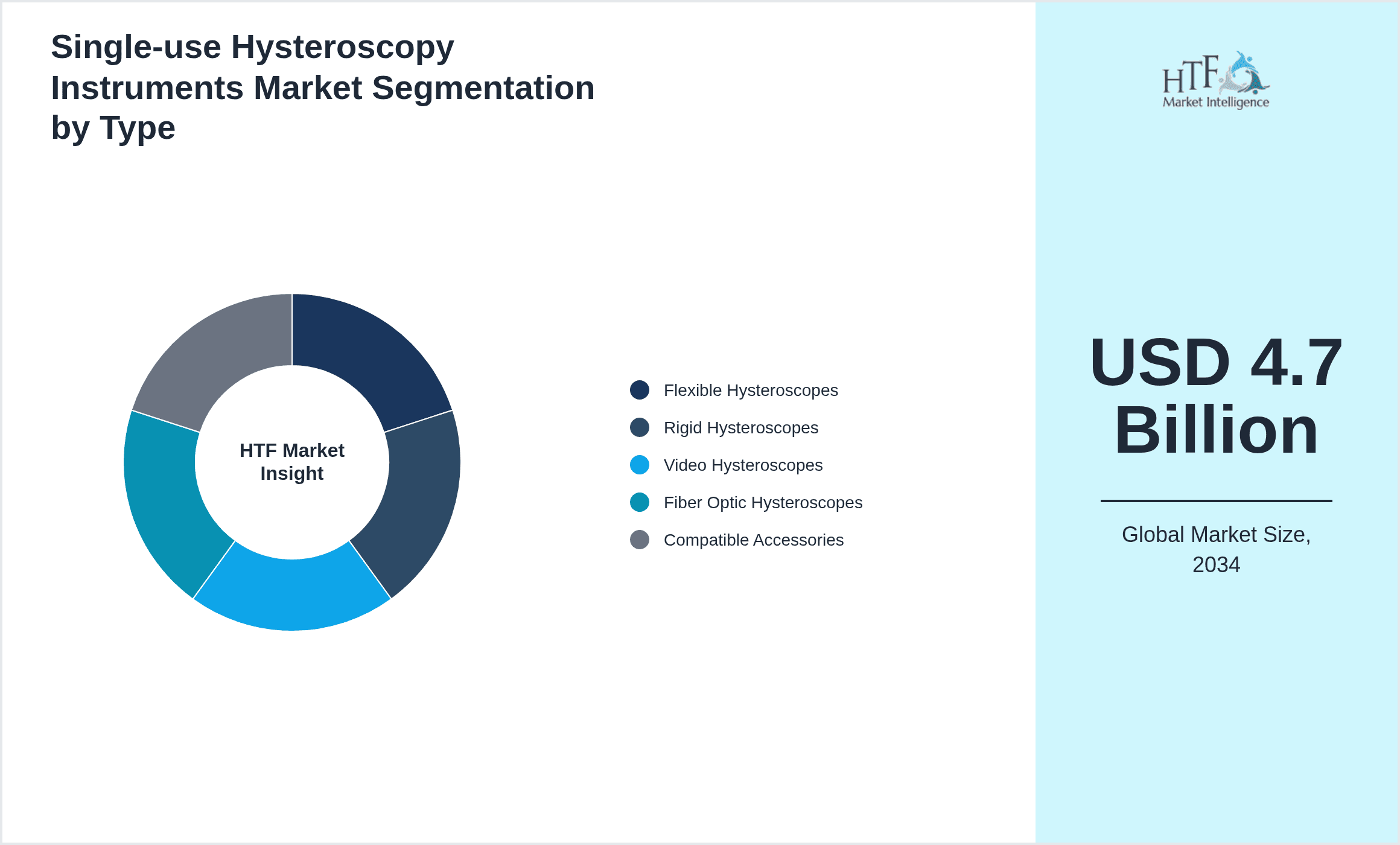

- •By Product Type

- ◦Flexible Hysteroscopes

- ◦Rigid Hysteroscopes

- ◦Video Hysteroscopes

- ◦Fiber Optic Hysteroscopes

- ◦Compatible Accessories

- •By Application

- ◦Diagnostic Hysteroscopy

- ◦Operative Hysteroscopy

- ◦Fertility Assessment

- ◦Polypectomy

- ◦Myomectomy

- •By End-Use Industry

- ◦Hospitals

- ◦Ambulatory Surgical Centers

- ◦Fertility Clinics

- ◦Specialty Clinics

- •By Distribution Channel

- ◦Direct Sales

- ◦Medical Distributors

- ◦E-commerce Platforms

Growth Dynamics

- •The increasing prevalence of uterine disorders globally has substantially driven demand for single-use hysteroscopy instruments, ensuring safer, minimally invasive diagnostic and therapeutic procedures. This is supported by rising awareness among women’s health advocates and improved access to gynecological care in emerging markets.

- •Technological advancements such as integration of high-definition imaging and flexible scopes enhance procedural accuracy and patient comfort, thereby expanding the applications of these devices in complex gynecological interventions.

- •Healthcare providers increasingly prefer disposable hysteroscopes to mitigate infection risks and reduce sterilization costs, aligning with stringent regulatory mandates for infection control in clinical settings.

- •Rising investments and government initiatives promoting women’s health infrastructure in Asia-Pacific and Latin America are accelerating adoption rates, contributing to rapid market expansion in these regions.

- •The growing trend toward outpatient surgeries and ambulatory care centers fosters demand for portable, user-friendly single-use hysteroscopy instruments that facilitate quick turnaround times and lower operational expenses.

- •Collaborations between medical device manufacturers and healthcare institutions are fostering innovation and tailored product development to meet evolving clinical needs and regulatory requirements globally.

- •Increasing consumer preference for minimally invasive diagnostic tools and enhanced procedural safety is encouraging ongoing research and development, which is expected to sustain long-term market growth.

Market Trends

- •Integration of video and fiber optic technologies in single-use hysteroscopes is a key trend, improving visualization and diagnostic accuracy during procedures, as evidenced by product launches from leading manufacturers in 2023 and 2024.

- •Sustainability concerns are prompting development of eco-friendly disposable instruments with biodegradable components, reflecting a shift towards greener healthcare solutions.

- •The rise of telemedicine and remote diagnostics is fostering demand for portable and easy-to-use hysteroscopy devices that enable remote consultations and procedures in underserved regions.

- •Collaborative partnerships between device makers and healthcare providers focus on customization of single-use instruments for specialized gynecological procedures, enhancing clinical outcomes and user satisfaction.

- •Emerging markets are witnessing rapid adoption of single-use hysteroscopy due to increasing healthcare expenditure, improving insurance coverage, and growing patient awareness of minimally invasive options.

- •Digitalization of healthcare workflows encourages incorporation of smart features and data analytics in hysteroscopy devices to support precision medicine and personalized treatment planning.

- •Manufacturers are increasingly focusing on ergonomic designs and disposable instrument kits that streamline surgical procedures, reduce operation times, and enhance clinician comfort.

Market Opportunities

- •Expanding applications in fertility assessment and assisted reproductive technologies represent significant growth avenues, with single-use hysteroscopes offering less invasive and safer diagnostic alternatives.

- •Emerging markets in Asia-Pacific and Latin America present untapped potential due to rising healthcare infrastructure investments and growing awareness of women’s health issues.

- •Development of multifunctional hysteroscopy instruments integrating imaging, therapeutic, and monitoring capabilities can capture broader market segments and increase clinical utility.

- •Strategic collaborations and licensing agreements between technology innovators and established manufacturers can accelerate product pipeline expansion and geographic penetration.

- •Growing demand for home-based and outpatient gynecological procedures opens avenues for portable single-use devices tailored for these settings.

- •Investment in digital health integration, including AI-enabled image analysis, presents opportunities to enhance diagnostic precision and workflow efficiency.

- •Regulatory support for infection control and patient safety globally encourages adoption of disposable medical instruments, providing a favorable market environment.

Market Challenges

- •High cost of advanced single-use hysteroscopy instruments compared to reusable counterparts may limit adoption in cost-sensitive healthcare settings, particularly in developing regions.

- •Stringent regulatory approvals and quality compliance requirements can delay product launches and increase development costs for manufacturers.

- •Environmental concerns regarding medical waste generated by disposable devices pose challenges, necessitating development of eco-friendly alternatives.

- •Lack of awareness and training among healthcare professionals in emerging markets restricts rapid uptake of new single-use technologies.

- •Competition from reusable hysteroscopy instruments with established market presence and lower per-use costs creates pricing and preference barriers.

- •Supply chain disruptions and raw material cost volatility can impact manufacturing efficiency and product availability.

- •Limited reimbursement policies for single-use devices in some regions reduce market attractiveness for providers and patients.

Regulatory Framework

- •From 2020 to 2025, the FDA implemented enhanced guidelines for single-use medical devices focusing on sterilization validation, biocompatibility, and labeling accuracy, ensuring patient safety and reducing cross-contamination risks in the US market.

- •The European Union’s Medical Device Regulation (MDR) enforced in 2021 introduced stringent conformity assessment procedures and post-market surveillance requirements, impacting market entry and compliance costs for disposable hysteroscopy instruments.

- •China’s National Medical Products Administration (NMPA) updated regulatory standards in 2023 to accelerate approvals for innovative single-use devices, fostering faster commercialization while maintaining rigorous safety assessments.

- •Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) revised device classification criteria between 2020-2025, facilitating streamlined registration processes for low-risk disposable hysteroscopy products, enhancing market accessibility.

- •Government initiatives globally promote adoption of single-use devices to combat hospital-acquired infections, supported by policy frameworks incentivizing manufacturers through subsidies and expedited review pathways.

Market Intelligence

- •15th February 2025, Ambu A/S announced the launch of its next-generation single-use flexible hysteroscope featuring enhanced HD imaging and improved ergonomic design. The device targets outpatient clinics and fertility centers aiming to enhance patient comfort and procedural efficiency. The innovation integrates disposable video chips to deliver superior visualization without sterilization needs, reducing turnaround times and infection risks. This launch is expected to strengthen Ambu’s market position in the Asia-Pacific and North American regions significantly. Ambu’s strategic focus on user-friendly, high-performance single-use devices aligns with rising demand for minimally invasive gynecological tools worldwide. Source: Official Ambu press release

- •30th March 2024, Olympus Corporation introduced a new line of single-use rigid hysteroscopes with advanced fiber optic technology and antimicrobial coatings. This product line was developed to meet stringent infection control standards and improve surgical precision in operative hysteroscopy procedures. The devices are targeted at hospitals and ambulatory surgical centers globally, with initial rollout in Europe and North America. Olympus emphasized environmental sustainability by introducing recyclable components to reduce medical waste footprint. The initiative reflects Olympus’s commitment to innovation and environmental responsibility in the disposable medical device market. Source: Olympus corporate announcement

- •10th January 2025, Boston Scientific Corporation announced a strategic partnership with a leading AI software provider to develop smart hysteroscopy instruments capable of real-time image analysis and anomaly detection. This collaboration aims to enhance diagnostic accuracy and clinical decision-making during intrauterine procedures. The AI-enabled devices are expected to launch by late 2025, targeting advanced healthcare facilities in North America and Europe initially, followed by broader global deployment. This initiative represents a significant step towards digital transformation and precision medicine in gynecological care. Boston Scientific plans to leverage this technology to differentiate its product portfolio and capture emerging market segments. Source: Boston Scientific press release

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 4.7 Billion |

| CAGR | 11.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11% |

| Scope of Report | Market is segmented by Product Type (Flexible Hysteroscopes, Rigid Hysteroscopes, Video Hysteroscopes, Fiber Optic Hysteroscopes, Compatible Accessories), Application (Diagnostic Hysteroscopy, Operative Hysteroscopy, Fertility Assessment, Polypectomy, Myomectomy), End-Use Industry (Hospitals, Ambulatory Surgical Centers, Fertility Clinics, Specialty Clinics), Distribution Channel (Direct Sales, Medical Distributors, E-commerce Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Olympus Corporation (Japan), Boston Scientific Corporation (United States), Stryker Corporation (United States), Smith & Nephew plc (United Kingdom), Medtronic plc (Ireland), Richard Wolf GmbH (Germany), Karl Storz SE & Co. KG (Germany), Hologic, Inc. (United States), ConMed Corporation (United States), Ambu A/S (Denmark), Cook Medical, LLC (United States), Pentax Medical (Japan), B. Braun Melsungen AG (Germany), Medline Industries, Inc. (United States), Sejong Medical (South Korea), Allium Medical Solutions (Israel), EndoMed Systems (United States), Micro-Tech Endoscopy USA, Inc. (United States), Irvine Scientific (United States), Biosense Webster, Inc. (United States), Nobel Biocare Services AG (Switzerland), Vygon SA (France), SurgiTel, Inc. (United States), Cook Medical (Ireland), LeMaitre Vascular, Inc. (United States) |

Global Single-use Hysteroscopy Instruments Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.