Global Optical Level Sensor Market Size, Growth & Revenue 2024-2034

Global Optical Level Sensor Market is segmented by Product Type (Reflective Optical Level Sensors, Transmissive Optical Level Sensors, Fiber Optic Sensors, Capacitive Optical Level Sensors, Ultrasonic Optical Level Sensors), Application (Industrial Automation, Automotive, Consumer Electronics, Healthcare, Aerospace), End-Use Industry (Manufacturing, Oil & Gas, Pharmaceuticals, Food & Beverage), Distribution Channel (Direct Sales, Distributors, Online Retail), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Optical Level Sensor market is a dynamic sector centered on the development and deployment of optical sensing technologies to measure liquid and solid levels accurately in diverse environments. This market covers sensor types such as reflective, transmissive, fiber optic, capacitive, and ultrasonic sensors, which are used extensively across industrial automation, automotive, consumer electronics, healthcare, and aerospace industries. The sensors enable non-contact, high-precision level measurements, crucial for process control, safety, and quality assurance. Advancements in sensor miniaturization, integration with IoT and Industry 4.0 technologies, and growing demand for automation are key market drivers. The market operates globally, with significant adoption in North America and Asia-Pacific, driven by industrial modernization and increasing technological investments. Additionally, regulatory compliance and environmental monitoring act as catalysts for demand. The competitive landscape is marked by innovation, strategic partnerships, and mergers aimed at expanding product portfolios and geographical reach. Overall, the market is poised for robust growth through 2034, propelled by continuous technological evolution and expanding applications across verticals.

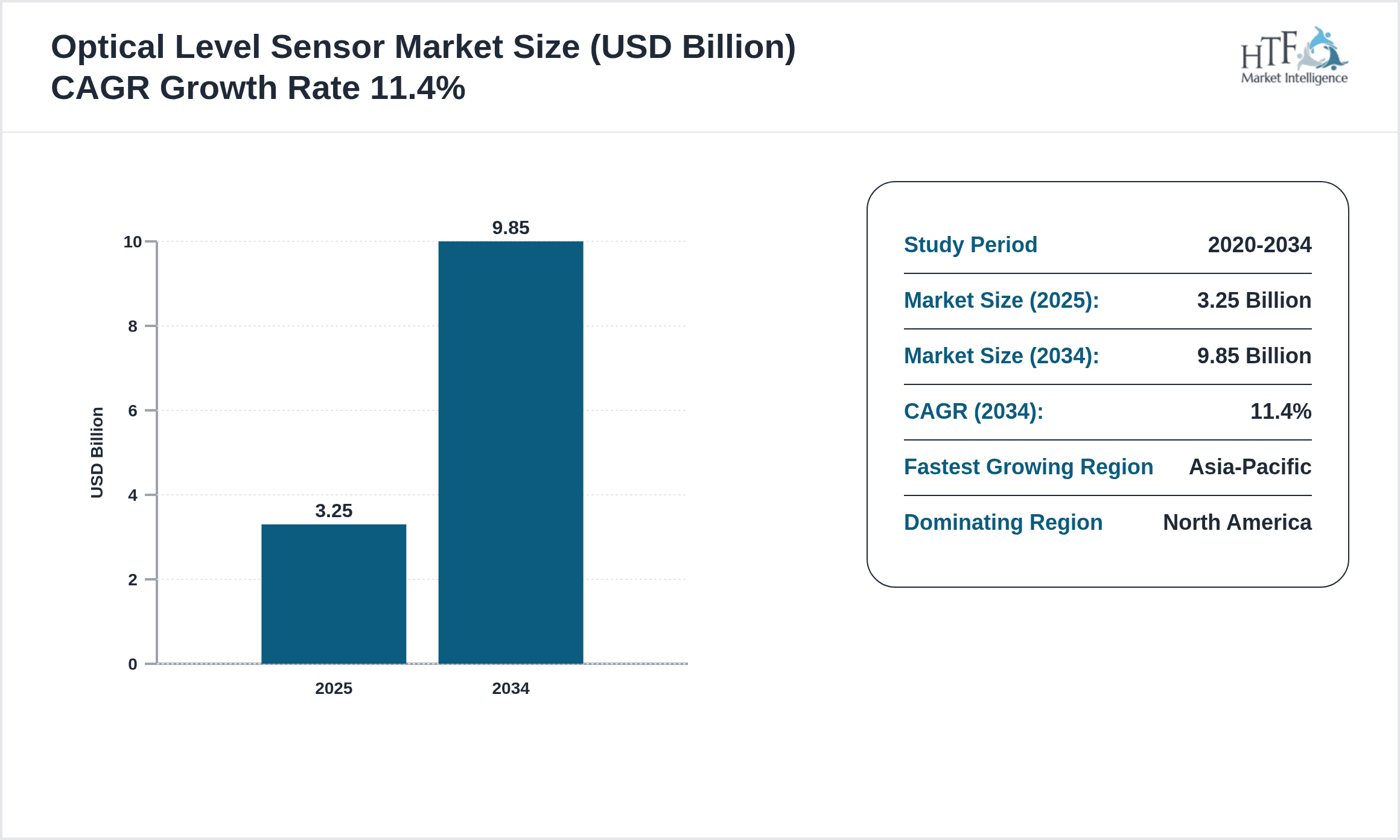

- •Market highlights include a base market size of USD 3.25 Billion in 2024, forecasting to reach USD 9.85 Billion by 2034, reflecting a CAGR of approximately 11.4%. Reflective optical level sensors currently dominate the product segment, whereas fiber optic sensors exhibit the fastest growth rate due to their precision and suitability for harsh environments. Industrial automation leads applications, followed closely by automotive. North America holds the largest regional share owing to early adoption and strong industrial infrastructure, while Asia-Pacific shows the highest growth potential driven by rapid industrialization and investments in smart manufacturing. The market benefits from rising demand for automated level measurement solutions, increasing focus on energy efficiency, and expanding end-user industries adopting advanced sensor technologies.

- •The value proposition of optical level sensors lies in their accuracy, reliability, and adaptability to various challenging environments, offering non-contact measurement that reduces maintenance and operational downtime. This strategic importance spans multiple industries including manufacturing, automotive, healthcare, and aerospace, which rely on precise level detection for safety, quality, and efficiency. The integration of optical sensors into IoT and smart systems enhances real-time monitoring and predictive maintenance capabilities, further strengthening their market demand. Stakeholders benefit from expanding applications, regulatory support, and technological advancements, positioning optical level sensors as critical components in the evolving landscape of automation and digital transformation worldwide.

Competitive Landscape

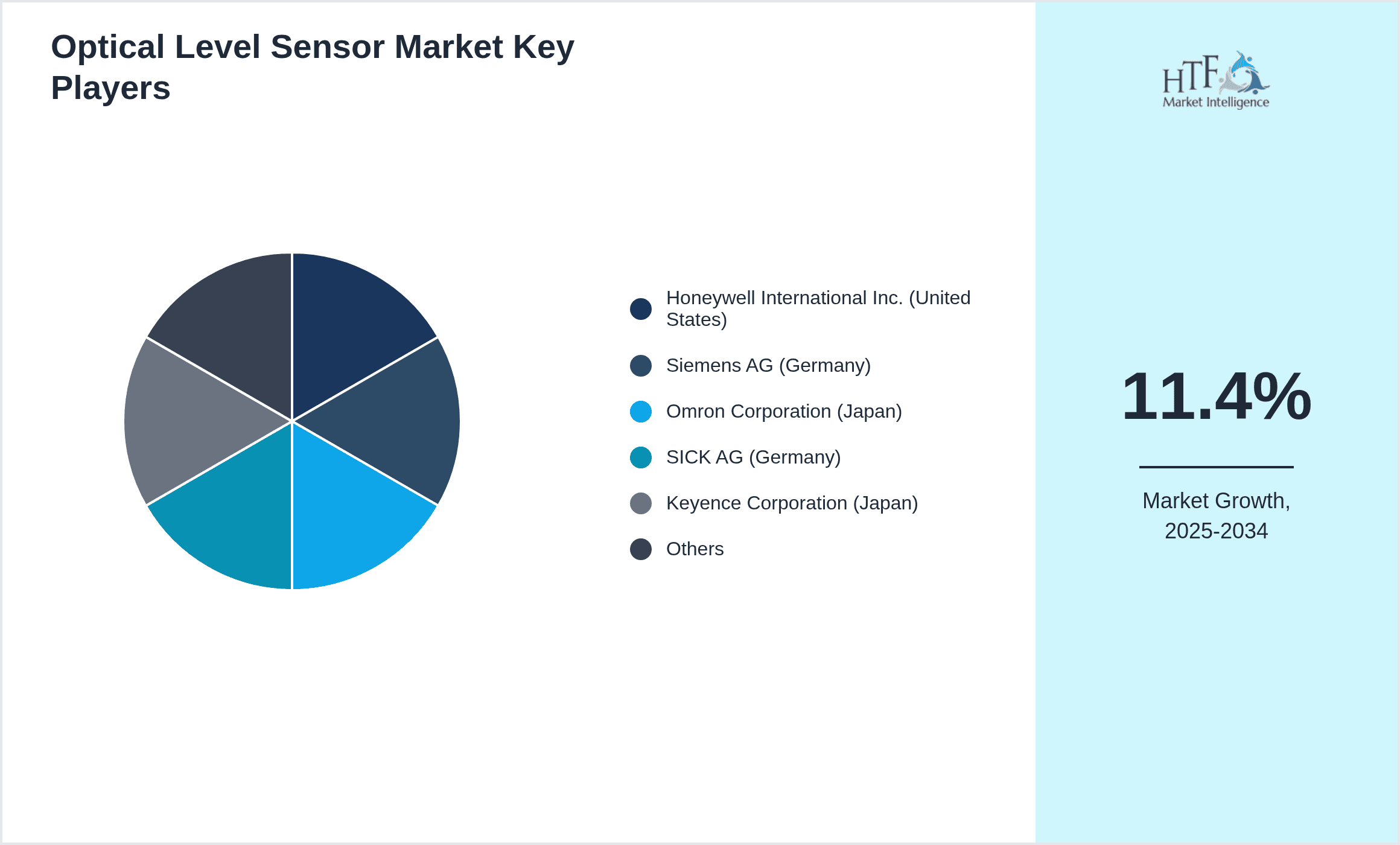

The global Optical Level Sensor market is characterized by intense competition among established multinational corporations and emerging technology innovators. Market participants focus heavily on research and development to introduce advanced sensor technologies that offer higher accuracy, durability, and integration capabilities with digital ecosystems. Competitive strategies include product differentiation through technological enhancements such as miniaturization, wireless connectivity, and enhanced environmental resistance. Companies actively pursue strategic partnerships, acquisitions, and collaborations to expand their product portfolios and geographic footprints. Pricing strategies are balanced against innovation and quality to maintain market share, especially in price-sensitive regions. The competitive landscape also reflects regional dynamics, where players adapt offerings to meet local regulatory requirements and customer preferences. Future competitive trends will likely emphasize sustainable technologies, AI integration for predictive analytics, and enhanced sensor performance, driving continuous industry evolution and rivalry.

Companies Shaping the Optical Level Sensor Market

- •Honeywell International Inc. (United States)

- •Siemens AG (Germany)

- •Omron Corporation (Japan)

- •SICK AG (Germany)

- •Keyence Corporation (Japan)

- •Balluff GmbH (Germany)

- •IFM Electronic GmbH (Germany)

- •ABB Ltd. (Switzerland)

- •Panasonic Corporation (Japan)

- •Banner Engineering Corp. (United States)

- •Pepperl+Fuchs GmbH (Germany)

- •TE Connectivity Ltd. (Switzerland)

- •Rockwell Automation, Inc. (United States)

- •Autonics Corporation (South Korea)

- •Murata Manufacturing Co., Ltd. (Japan)

- •Baumer Group (Switzerland)

- •Panasonic Industrial Devices SUNX Co., Ltd. (Japan)

- •E+E Elektronik GmbH (Austria)

- •Vega Grieshaber KG (Germany)

- •Honeywell Sensing and Productivity Solutions (United States)

- •Schneider Electric SE (France)

- •Omni Instruments Ltd. (United Kingdom)

- •Sensata Technologies Holding plc (United States)

- •Dynisco Instruments LLC (United States)

- •First Sensor AG (Germany)

Market Breakdown

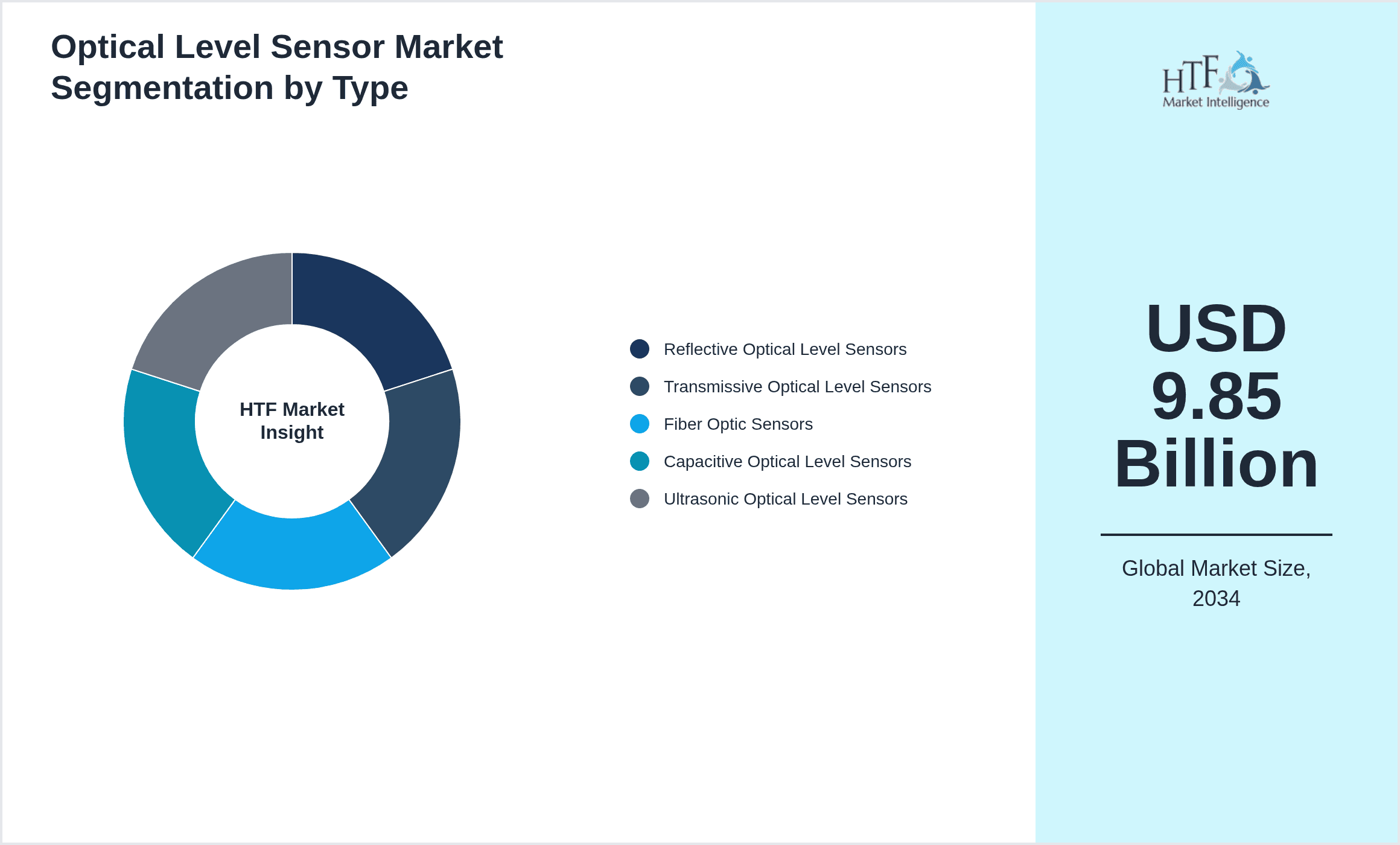

- •By Product Type

- ◦Reflective Optical Level Sensors

- ◦Transmissive Optical Level Sensors

- ◦Fiber Optic Sensors

- ◦Capacitive Optical Level Sensors

- ◦Ultrasonic Optical Level Sensors

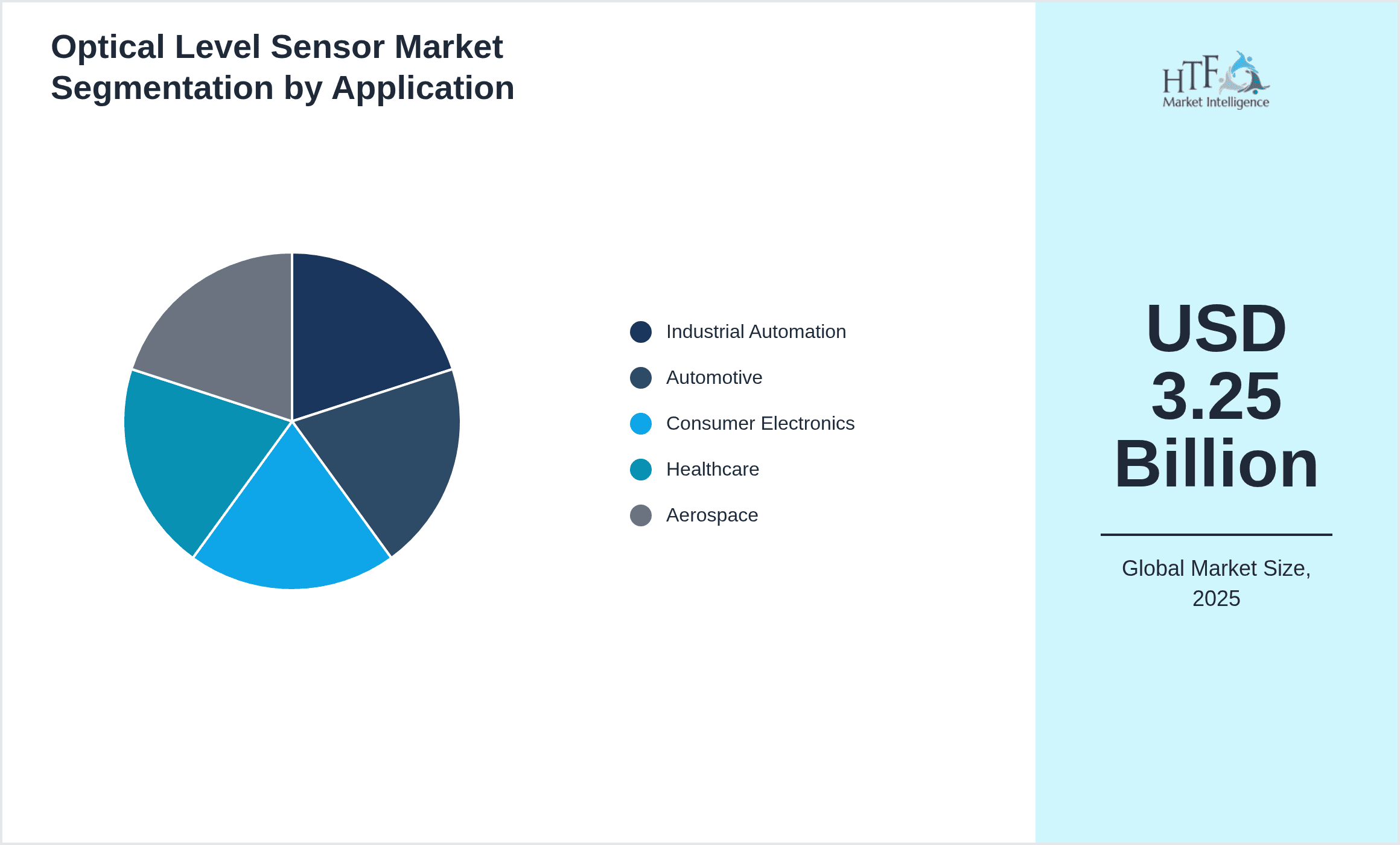

- •By Application

- ◦Industrial Automation

- ◦Automotive

- ◦Consumer Electronics

- ◦Healthcare

- ◦Aerospace

- •By End-Use Industry

- ◦Manufacturing

- ◦Oil & Gas

- ◦Pharmaceuticals

- ◦Food & Beverage

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Retail

Growth Dynamics

- •Rising industrial automation globally is a primary growth driver, with optical level sensors enabling precise, real-time monitoring that enhances manufacturing efficiency and process safety. For example, automotive factories increasingly integrate these sensors for fluid level management, reducing downtime and improving product quality.

- •Advancements in fiber optic sensor technology, offering high sensitivity and immunity to electromagnetic interference, are driving adoption in harsh industrial and aerospace environments, fueling market expansion especially in Asia-Pacific and North America.

- •Growing demand for non-contact and maintenance-free sensing solutions in healthcare devices and consumer electronics is accelerating the development of miniaturized, energy-efficient optical level sensors tailored for compact applications.

- •Government initiatives promoting Industry 4.0 and smart manufacturing across major economies stimulate investments in optical sensing technologies, enhancing market growth by fostering digital integration and data-driven process control.

- •Expansion of renewable energy and environmental monitoring applications requires reliable liquid level measurement, presenting new growth avenues for optical level sensor manufacturers focusing on sustainable and energy-efficient products.

- •Increasing replacement of traditional mechanical sensors with optical variants due to their higher reliability and longer lifespan supports sustained market demand and innovation.

- •Strategic mergers and technology collaborations among key players facilitate rapid innovation cycles and global distribution, strengthening competitive positioning and market reach.

Market Trends

- •Integration of optical level sensors with IoT and Industry 4.0 platforms is a significant trend, enabling real-time data analytics and predictive maintenance that improve operational efficiency across industries such as manufacturing and healthcare.

- •Miniaturization and wireless connectivity in sensor design are increasingly adopted to meet the demands of compact consumer electronics and automotive applications, enhancing market penetration and user convenience.

- •Sustainability-driven innovation is leading manufacturers to develop energy-efficient sensors with reduced material use and enhanced recyclability, aligning with global environmental regulations and corporate responsibility goals.

- •Adoption of advanced materials such as silicon photonics and novel optical coatings is improving sensor sensitivity and durability, especially in harsh industrial and aerospace environments.

- •Collaborative ecosystems among sensor manufacturers, software developers, and system integrators are emerging to deliver holistic sensing solutions tailored to specific industrial processes and customer needs.

- •Market fragmentation is decreasing as larger players acquire niche technology providers, consolidating product portfolios and expanding geographical reach to better serve global customers.

- •The shift towards smart factories and autonomous systems is driving demand for optical level sensors integrated with AI and machine learning algorithms for enhanced decision-making and automation.

Market Opportunities

- •Emerging economies in Asia-Pacific and Latin America present substantial opportunities due to increasing industrialization and adoption of automation technologies, creating new demand for optical level sensors in manufacturing and automotive sectors.

- •Expanding applications in healthcare, particularly in medical devices requiring precise fluid level measurement, open avenues for specialized sensor development and market penetration.

- •Integration of optical level sensors with IoT and cloud computing platforms offers opportunities for developing value-added services such as remote monitoring and predictive analytics, enhancing customer engagement and revenue streams.

- •Development of multi-parameter sensors combining level detection with temperature or pressure sensing can meet complex industrial requirements, providing a competitive edge and expanded market share.

- •Strategic partnerships with system integrators and technology providers enable access to new end-use industries and customized solutions, driving growth and diversification.

- •Increasing focus on sustainability and regulatory compliance encourages innovation in eco-friendly sensor designs, creating differentiation and new product lines.

- •Digital transformation initiatives in traditional industries offer opportunities for retrofitting existing systems with optical sensors, boosting aftermarket sales and long-term customer relationships.

Market Challenges

- •High initial costs of advanced optical level sensors compared to traditional mechanical sensors pose adoption barriers, especially in cost-sensitive emerging markets.

- •Complexity of integrating optical sensors into existing legacy systems can delay deployment and increase implementation costs, deterring potential customers.

- •Stringent regulatory requirements and certification processes in key industries such as healthcare and aerospace impose compliance challenges and extend time-to-market for new products.

- •Competition from alternative sensing technologies such as ultrasonic and capacitive sensors requires continuous innovation and differentiation to maintain market share.

- •Supply chain disruptions and component shortages, particularly for high-precision optical components, impact production schedules and market availability.

- •Lack of skilled workforce and technical expertise in emerging regions slows adoption and limits the scalability of optical level sensor solutions.

- •Cybersecurity concerns related to IoT-enabled sensor networks necessitate robust data protection measures, increasing development complexity and costs.

Regulatory Framework

- •Between 2019 and 2024, key regulations such as the EU’s Machinery Directive and RoHS compliance have mandated stringent safety and environmental standards for optical sensors, impacting design and manufacturing processes globally.

- •The introduction of ISO 13849 and IEC 61508 functional safety standards has required manufacturers to enhance sensor reliability and incorporate fail-safe mechanisms, driving innovation and quality assurance.

- •Environmental regulations focusing on hazardous substances and electronic waste management, such as WEEE directives, have influenced material selection and end-of-life management strategies in sensor production.

- •Regional mandates in North America and Asia-Pacific regarding electromagnetic compatibility and wireless communication protocols have necessitated compliance testing and certification for connected optical sensor devices.

- •Government initiatives promoting Industry 4.0 adoption include incentives for deploying smart sensors and automation technologies, encouraging market growth and technological advancement in optical level sensing.

Market Intelligence

- •15th January 2025, Honeywell International Inc. launched its latest reflective optical level sensor series designed for harsh industrial environments, featuring enhanced temperature tolerance and wireless connectivity. This new product aims to improve reliability in automotive and manufacturing applications while reducing maintenance costs through IoT integration, aligning with Industry 4.0 trends and strengthening Honeywell's position in the global market. Source: Official Honeywell press release

- •30th March 2025, Keyence Corporation introduced an innovative fiber optic sensor with unprecedented sensitivity and miniaturization for medical device applications. The sensor's design facilitates precise fluid level monitoring in compact healthcare devices, addressing the rising demand for non-invasive measurements and enabling new market segments for Keyence. This launch underscores the company's commitment to R&D and expanding its healthcare market footprint. Source: Keyence official announcement

- •12th July 2024, Siemens AG announced a strategic partnership with a leading IoT platform provider to develop integrated optical level sensor solutions for smart manufacturing. This collaboration focuses on enhancing data analytics capabilities and predictive maintenance using sensor data, aiming to deliver seamless automation benefits to clients globally. The partnership is expected to accelerate digital transformation initiatives and expand Siemens' sensor technology ecosystem. Source: Siemens corporate news

- •22nd November 2024, Omron Corporation completed the acquisition of a niche optical sensor startup specializing in capacitive and ultrasonic technologies. This move strengthens Omron’s product portfolio, enabling comprehensive level sensing solutions across multiple industries and expanding its technological capabilities in sensor innovation. The acquisition supports Omron’s growth strategy focused on smart automation and precision sensing. Source: Omron official press release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.25 Billion |

| Forecast Year Market Size | USD 9.85 Billion |

| CAGR | 11.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.4% |

| Scope of Report | Market is segmented by Product Type (Reflective Optical Level Sensors, Transmissive Optical Level Sensors, Fiber Optic Sensors, Capacitive Optical Level Sensors, Ultrasonic Optical Level Sensors), Application (Industrial Automation, Automotive, Consumer Electronics, Healthcare, Aerospace), End-Use Industry (Manufacturing, Oil & Gas, Pharmaceuticals, Food & Beverage), Distribution Channel (Direct Sales, Distributors, Online Retail) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Honeywell International Inc. (United States), Siemens AG (Germany), Omron Corporation (Japan), SICK AG (Germany), Keyence Corporation (Japan), Balluff GmbH (Germany), IFM Electronic GmbH (Germany), ABB Ltd. (Switzerland), Panasonic Corporation (Japan), Banner Engineering Corp. (United States), Pepperl+Fuchs GmbH (Germany), TE Connectivity Ltd. (Switzerland), Rockwell Automation, Inc. (United States), Autonics Corporation (South Korea), Murata Manufacturing Co., Ltd. (Japan), Baumer Group (Switzerland), Panasonic Industrial Devices SUNX Co., Ltd. (Japan), E+E Elektronik GmbH (Austria), Vega Grieshaber KG (Germany), Honeywell Sensing and Productivity Solutions (United States), Schneider Electric SE (France), Omni Instruments Ltd. (United Kingdom), Sensata Technologies Holding plc (United States), Dynisco Instruments LLC (United States), First Sensor AG (Germany) |

Global Optical Level Sensor Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.