Global Microfluidic Device Pumps Market Size, Growth & Revenue 2024-2034

Global Microfluidic Device Pumps Market is segmented by Product Type (Peristaltic Pumps, Syringe Pumps, Electroosmotic Pumps, Centrifugal Pumps, Piezoelectric Pumps), Application (Biomedical Research, Diagnostics, Drug Delivery, Environmental Monitoring, Food Safety), End-Use Industry (Pharmaceuticals, Healthcare, Environmental Agencies, Food & Beverage), Distribution Channel (Direct Sales, OEM Partnerships, Online Retail), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Microfluidic Device Pumps Market is characterized by the production and application of highly precise pumps designed for controlling fluid movement in micro-scale systems. These devices are pivotal in biomedical research, diagnostics, drug delivery systems, environmental testing, and food safety analysis, allowing for accurate manipulation of fluids at micro and nano levels. The market includes various pump technologies such as peristaltic, syringe, electroosmotic, centrifugal, and piezoelectric pumps, each suited to different operational needs and fluid types. Growth in this market is fueled by the increasing adoption of lab-on-a-chip and point-of-care diagnostic devices, advancing microfabrication techniques, and rising investments in biomedical research globally. The development of portable and automated microfluidic systems is further expanding market applications, creating significant opportunities for innovation and integration across healthcare, environmental monitoring, and food safety sectors. The market’s scope extends across diverse geographic regions, with North America leading in adoption and Asia-Pacific demonstrating the highest growth potential.

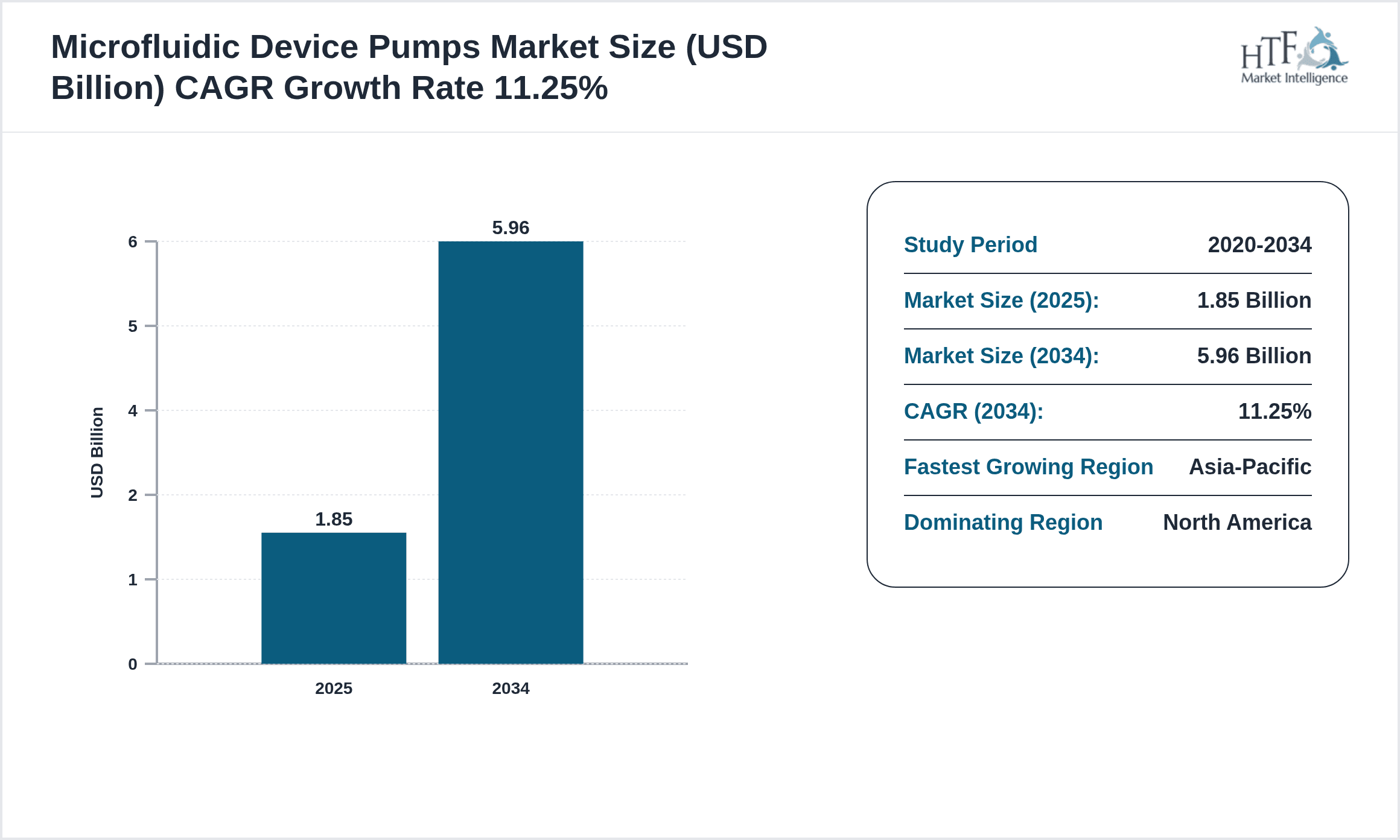

- •Market highlights include a base market size of USD 1.85 billion in 2024, projected to reach USD 5.96 billion by 2034, at a robust CAGR of 11.25%. Peristaltic pumps currently dominate the product segment due to their reliability and gentle pumping mechanism, whereas piezoelectric pumps are the fastest-growing type owing to their compact size and energy efficiency. Biomedical research remains the leading application, closely followed by diagnostics, driven by increasing demand for rapid and precise analytical tools. Regionally, North America holds the largest market share, supported by strong healthcare infrastructure and significant R&D expenditure. Asia-Pacific is the fastest-growing region, benefiting from expanding healthcare facilities and government initiatives to support technological advancements in microfluidics.

- •The market offers substantial value to stakeholders including pump manufacturers, research institutions, healthcare providers, and environmental agencies by enabling miniaturized, efficient, and high-precision fluid control solutions. Strategic investments in R&D and partnerships are critical for technological advancement and market penetration. The integration of microfluidic pumps with diagnostics and drug delivery devices is redefining standard practices in personalized medicine and point-of-care testing. Additionally, the market’s growth aligns with sustainability goals by reducing reagent volumes and waste generation. Overall, the microfluidic device pumps market is poised for transformative growth, driven by innovation, expanding applications, and increasing adoption in emerging economies worldwide.

Competitive Landscape

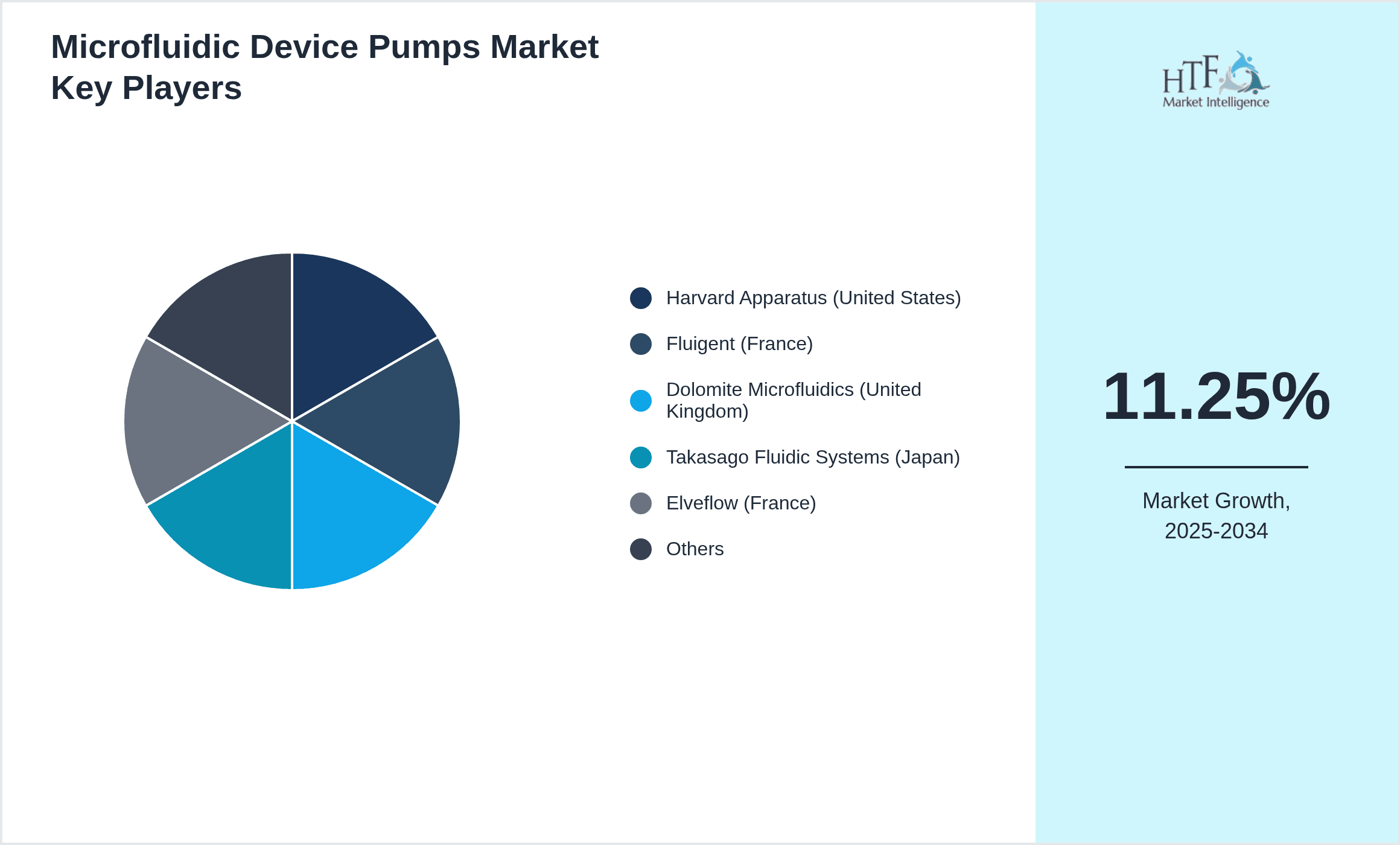

The global microfluidic device pumps market is highly competitive with numerous players focusing on innovation, strategic collaborations, and geographic expansion to strengthen their market position. Companies compete by enhancing pump precision, miniaturization, and energy efficiency while reducing cost and footprint. Market rivalry intensifies as firms adopt differentiated technologies such as piezoelectric and electroosmotic pumps to address specific application requirements. Innovation pipelines emphasize integration with lab-on-a-chip platforms and automated systems, driving technology leadership. Strategic partnerships and acquisitions are common to expand product portfolios and enter new regional markets. Pricing strategies vary, balancing premium products for high-end research and cost-effective solutions for emerging markets. Distribution channels are optimized for global reach, including direct sales and OEM partnerships. Continuous technological advancements and regulatory compliance remain critical competitive factors, with companies investing heavily in R&D to maintain leadership and address evolving customer needs globally.

Major Microfluidic Device Pumps Industry Players

- •Harvard Apparatus (United States)

- •Fluigent (France)

- •Dolomite Microfluidics (United Kingdom)

- •Takasago Fluidic Systems (Japan)

- •Elveflow (France)

- •Bartels Mikrotechnik (Germany)

- •Chemyx Inc. (United States)

- •Sensirion AG (Switzerland)

- •MicruX Technologies (Spain)

- •IDEX Health & Science (United States)

- •Instech Laboratories (United States)

- •Micronit Microtechnologies (Netherlands)

- •Precision Nanosystems (Canada)

- •NResearch (United States)

- •SyringePump.com (United States)

- •CETONI GmbH (Germany)

- •Microsaic Systems (United Kingdom)

- •Bio-Chem Fluidics (United States)

- •Microfluidic ChipShop (Germany)

- •Fluigent Inc. (United States)

- •Harvard Bioscience (United States)

- •Dolomite Microfluidics Ltd. (United Kingdom)

- •Takasago Fluidic Systems, Inc. (Japan)

- •Elveflow SAS (France)

- •Bartels Mikrotechnik GmbH (Germany)

Market Breakdown

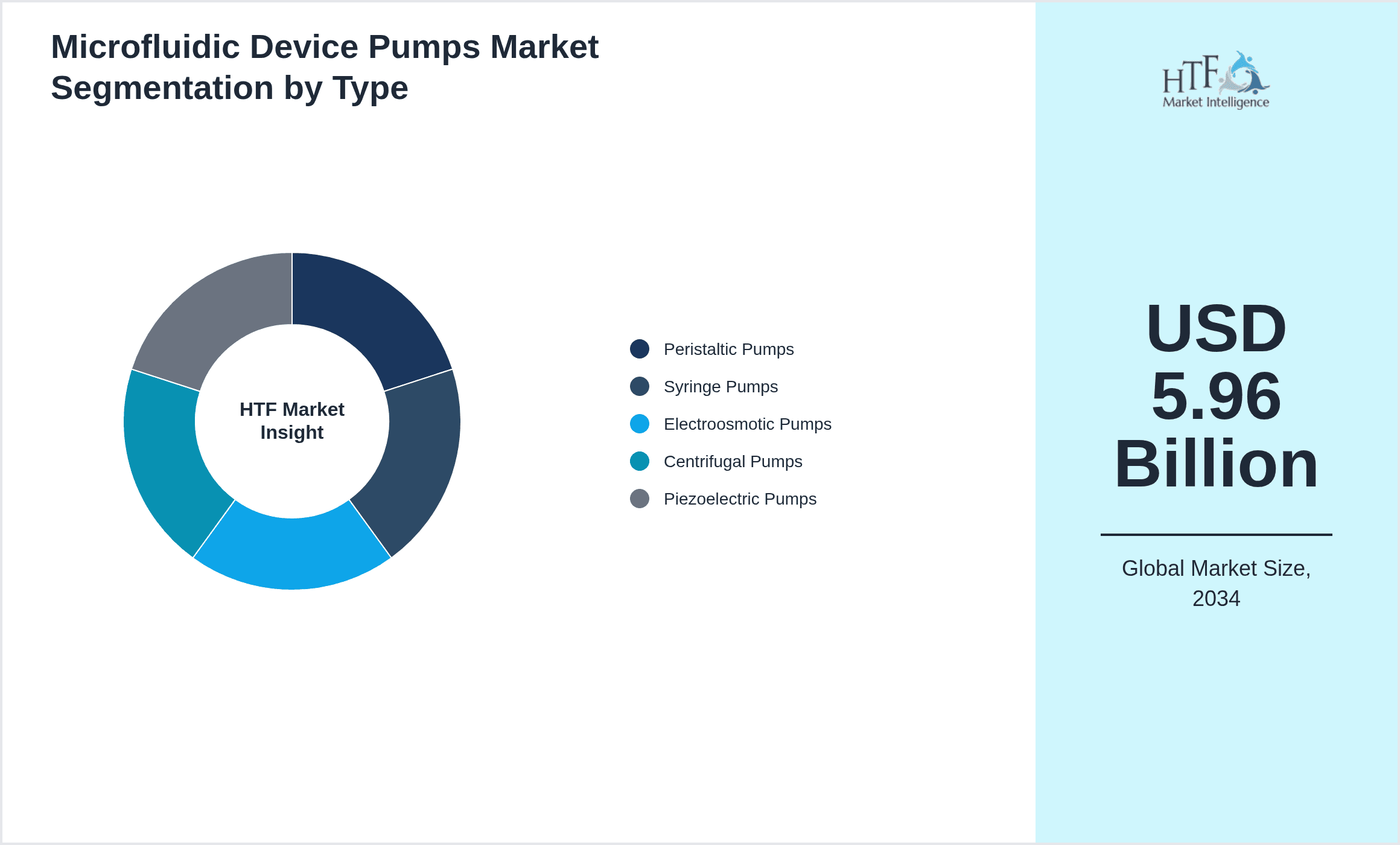

- •By Product Type

- ◦Peristaltic Pumps

- ◦Syringe Pumps

- ◦Electroosmotic Pumps

- ◦Centrifugal Pumps

- ◦Piezoelectric Pumps

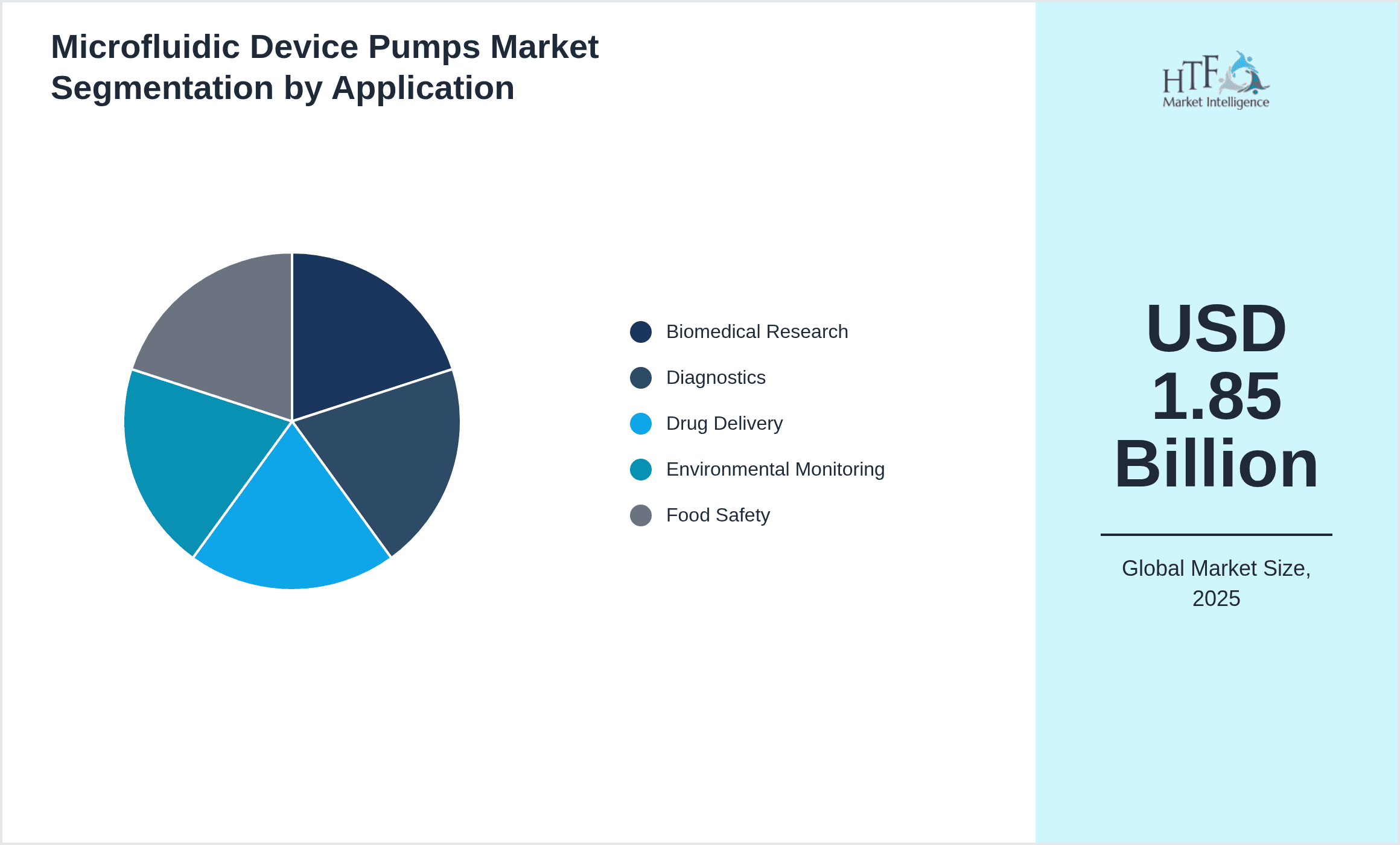

- •By Application

- ◦Biomedical Research

- ◦Diagnostics

- ◦Drug Delivery

- ◦Environmental Monitoring

- ◦Food Safety

- •By End-Use Industry

- ◦Pharmaceuticals

- ◦Healthcare

- ◦Environmental Agencies

- ◦Food & Beverage

- •By Distribution Channel

- ◦Direct Sales

- ◦OEM Partnerships

- ◦Online Retail

Growth Dynamics

- •The expanding adoption of lab-on-a-chip technologies is a primary driver, enabling miniaturized, automated fluid handling that significantly enhances throughput and accuracy in biomedical and diagnostic applications.

- •Rising investments in personalized medicine and point-of-care diagnostics are fueling demand for precise, reliable microfluidic pumps capable of handling minute fluid volumes with high reproducibility.

- •Technological advancements such as integration of piezoelectric materials and electroosmotic pumping mechanisms are improving pump efficiency and device miniaturization, opening new application avenues.

- •Increasing regulatory approvals for microfluidic devices in healthcare and environmental monitoring are fostering market confidence and accelerating commercialization of advanced pumps.

- •Growth in emerging economies due to expanding healthcare infrastructure and rising awareness about rapid diagnostic technologies is providing new market opportunities globally.

Market Trends

- •Integration of microfluidic pumps with wireless and IoT-enabled systems is trending, allowing remote monitoring and control for real-time diagnostics and environmental sensing applications.

- •Adoption of eco-friendly and energy-efficient pumping solutions such as piezoelectric pumps is increasing in response to sustainability initiatives within the microfluidics industry.

- •Collaborations between pump manufacturers and chip developers are on the rise to create fully integrated microfluidic platforms, enhancing device functionality and user experience.

- •Customization and modularity of pump systems are gaining prominence, enabling end-users to tailor setups for specific research and industrial applications.

- •The emergence of 3D printing technologies is facilitating rapid prototyping and cost-effective manufacturing of microfluidic pump components, accelerating innovation cycles.

Market Opportunities

- •Expanding applications in wearable drug delivery devices offer significant growth potential by enabling controlled release of therapeutics via microfluidic pumps in personalized medicine.

- •Increasing demand for rapid environmental testing solutions presents opportunities to develop portable, sensitive microfluidic pump systems tailored for on-site analysis.

- •Emerging markets in Asia-Pacific and Latin America provide untapped customer bases for affordable, high-performance microfluidic pump technologies, supported by growing healthcare investments.

- •Strategic partnerships between microfluidic pump manufacturers and pharmaceutical companies can accelerate adoption in drug discovery and development workflows.

- •Integration of AI and machine learning with microfluidic systems promises enhanced automation and predictive maintenance, creating value-added offerings for end-users.

Market Challenges

- •High manufacturing costs and complexity of microfluidic pumps limit accessibility for small and medium research labs, constraining widespread adoption in certain regions.

- •Technical challenges related to pump durability and leakage at micro scales require continuous innovation to improve reliability and user confidence.

- •Regulatory compliance across different regions remains complex, with varying standards affecting product approval and market entry timelines.

- •Competition from alternative fluid control technologies such as passive microvalves poses a challenge to the growth of active microfluidic pumps.

- •Supply chain disruptions and scarcity of specialized materials for pump components can impact production schedules and cost structures.

Regulatory Framework

- •Between 2019 and 2024, regulatory bodies globally have tightened standards for microfluidic device safety and performance, mandating rigorous validation protocols to ensure reliability in clinical and environmental settings.

- •The introduction of harmonized international standards for microfluidic medical devices has streamlined compliance requirements, facilitating smoother cross-border market access.

- •Environmental regulations focusing on sustainable manufacturing processes have prompted manufacturers to adopt greener materials and reduce waste in pump production.

- •Region-specific mandates in North America and Europe require detailed documentation of biocompatibility and device sterilization methods, impacting design and development cycles.

- •Government incentives and funding programs supporting innovation in microfluidics have encouraged R&D activities, accelerating regulatory submissions and product launches.

Market Intelligence

- •15th January 2025, Harvard Apparatus announced the launch of a new line of compact peristaltic microfluidic pumps designed for portable diagnostic devices. The pumps feature enhanced flow precision with integrated digital control, aimed at improving point-of-care testing capabilities. This innovation supports rapid fluid manipulation with minimal power consumption, targeting biomedical and environmental applications. The product launch is part of Harvard Apparatus’s strategy to expand its footprint in the microfluidics market by offering versatile and user-friendly solutions for researchers and clinicians worldwide. Source: Harvard Apparatus Official Release

- •22nd March 2025, Fluigent introduced an advanced piezoelectric pump platform that offers ultra-low flow rates suitable for drug delivery systems and single-cell analysis. Incorporating AI-driven flow regulation technology, the platform ensures optimal fluid control with minimal pulsation. This development positions Fluigent as a leader in next-generation microfluidic pumping solutions, emphasizing precision and compact design. The launch is expected to accelerate adoption in pharmaceutical research and personalized medicine sectors. Source: Fluigent Press Announcement

- •10th May 2025, Dolomite Microfluidics announced a strategic partnership with a leading pharmaceutical company to co-develop integrated microfluidic pump systems for high-throughput drug screening. The collaboration aims to combine Dolomite’s microfluidic expertise with the partner’s drug discovery capabilities to accelerate screening processes and reduce costs. This alliance underscores the growing trend of cross-industry cooperation to enhance innovation and market reach in microfluidic technologies. Source: Dolomite Microfluidics Newsroom

- •5th July 2025, Takasago Fluidic Systems completed an acquisition of a boutique microfluidic pump startup specializing in electroosmotic pumping technologies. This acquisition enhances Takasago’s product portfolio by integrating novel fluid manipulation mechanisms that complement existing offerings. The strategic move aims to strengthen Takasago’s competitive position in the global market, offering customers broader solutions for diverse microfluidic applications. Source: Takasago Corporate Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 5.96 Billion |

| CAGR | 11.25% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.25% |

| Scope of Report | Market is segmented by Product Type (Peristaltic Pumps, Syringe Pumps, Electroosmotic Pumps, Centrifugal Pumps, Piezoelectric Pumps), Application (Biomedical Research, Diagnostics, Drug Delivery, Environmental Monitoring, Food Safety), End-Use Industry (Pharmaceuticals, Healthcare, Environmental Agencies, Food & Beverage), Distribution Channel (Direct Sales, OEM Partnerships, Online Retail) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Harvard Apparatus (United States), Fluigent (France), Dolomite Microfluidics (United Kingdom), Takasago Fluidic Systems (Japan), Elveflow (France), Bartels Mikrotechnik (Germany), Chemyx Inc. (United States), Sensirion AG (Switzerland), MicruX Technologies (Spain), IDEX Health & Science (United States), Instech Laboratories (United States), Micronit Microtechnologies (Netherlands), Precision Nanosystems (Canada), NResearch (United States), SyringePump.com (United States), CETONI GmbH (Germany), Microsaic Systems (United Kingdom), Bio-Chem Fluidics (United States), Microfluidic ChipShop (Germany), Fluigent Inc. (United States), Harvard Bioscience (United States), Dolomite Microfluidics Ltd. (United Kingdom), Takasago Fluidic Systems, Inc. (Japan), Elveflow SAS (France), Bartels Mikrotechnik GmbH (Germany) |

Global Microfluidic Device Pumps Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.