Global Coagulation Factor Concentrate Market Size, Growth & Revenue 2025-2034

Global Coagulation Factor Concentrate Market is segmented by Product Type (Plasma-Derived Concentrates, Recombinant Concentrates, Extended Half-Life Concentrates, Prothrombin Complex Concentrates, Activated Factor Concentrates), Application (Hemophilia A, Hemophilia B, Von Willebrand Disease, Acquired Coagulation Disorders, Other Bleeding Disorders), End-Use Industry (Hospitals, Specialty Clinics, Homecare Settings, Research Institutes), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global coagulation factor concentrate market is a vital segment within hematology, addressing the needs of patients suffering from bleeding disorders such as hemophilia A, hemophilia B, von Willebrand disease, and other acquired coagulation deficiencies. This market comprises plasma-derived concentrates, recombinant concentrates, extended half-life products, prothrombin complex concentrates, and activated factor concentrates, each offering distinct therapeutic benefits. Rising incidence and diagnosis rates of bleeding disorders, coupled with technological advancements in recombinant DNA technology and improved safety profiles, have significantly bolstered market expansion. The treatment landscape is further shaped by increasing patient awareness, enhanced healthcare infrastructure, and supportive reimbursement policies globally. The market is geographically diverse, with North America leading in revenue generation due to established healthcare systems and high patient awareness, while Asia-Pacific is the fastest-growing region driven by increasing healthcare investments and rising prevalence. Industry players emphasize innovation, strategic collaborations, and regulatory compliance to maintain competitive advantage. Overall, the coagulation factor concentrate market demonstrates robust growth potential, underpinned by continuous advancements in biotechnology and expanding patient populations worldwide.

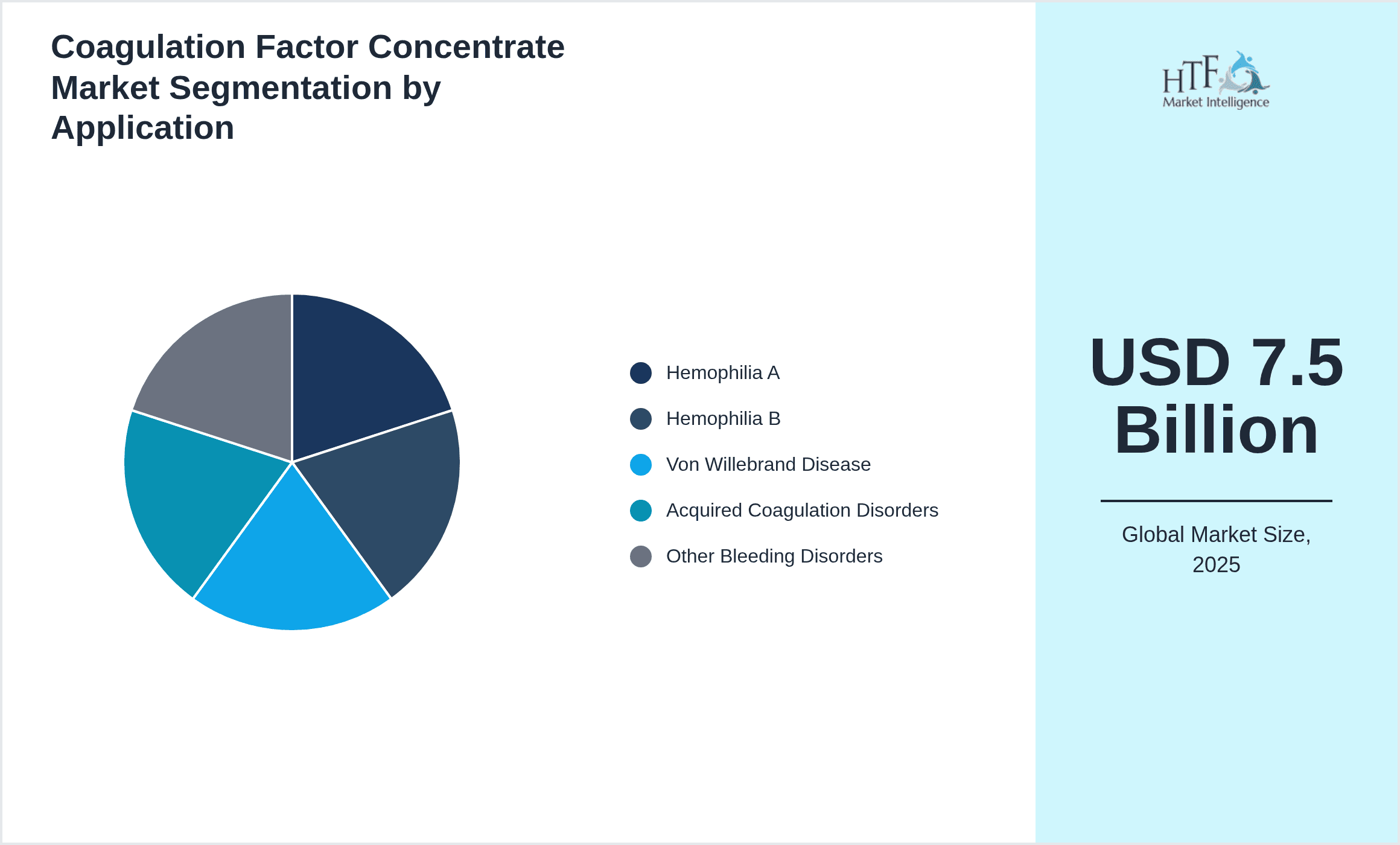

- •Key market highlights include a base market size of USD 7.5 Billion in 2025, forecasted to reach USD 15.8 Billion by 2034, reflecting a strong CAGR of 8.2%. The recombinant concentrates segment holds the leading share due to their enhanced safety and efficacy profiles, while extended half-life concentrates are anticipated to exhibit the fastest growth owing to improved patient compliance and reduced treatment frequency. North America dominates the market, with Asia-Pacific emerging as a dynamic growth hub. Market drivers include technological innovations, increasing prevalence of bleeding disorders, and favorable reimbursement landscapes. Challenges such as high treatment costs and regulatory complexities persist, but opportunities abound with expanding indications and emerging markets. These insights underscore the strategic importance of coagulation factor concentrates for healthcare providers, pharmaceutical manufacturers, and investors aiming to capitalize on this expanding therapeutic arena.

- •This market offers significant value propositions through improved patient outcomes, reduced healthcare burdens, and enhanced quality of life. Coagulation factor concentrates enable personalized treatment regimens, minimizing bleeding episodes and associated complications. Stakeholders benefit from evolving technological platforms enabling cost-effective production and extended product pipelines. The strategic importance of this market spans pharmaceutical innovation, healthcare delivery, and patient-centric care models, making it integral to advancing hematological therapeutics on a global scale.

Competitive Landscape

The global coagulation factor concentrate market features a highly competitive environment characterized by strategic alliances, mergers and acquisitions, and continuous product innovation. Leading pharmaceutical firms are investing heavily in research and development to introduce recombinant and extended half-life products, enhancing therapeutic efficacy and patient adherence. Competition is intensified by pricing pressures, regulatory requirements, and the emergence of biosimilars. Market players deploy diversified strategies including geographic expansion, portfolio diversification, and partnerships with healthcare providers to strengthen market presence. Technological advancements in biotechnology and manufacturing processes serve as key differentiators, enabling companies to improve safety, reduce immunogenicity, and optimize dosing schedules. Additionally, distribution channel optimization and patient support programs are critical components in gaining competitive advantage. The evolving landscape necessitates agility and innovation, with companies focusing on personalized medicine approaches and digital health integration to sustain growth and respond to emerging market demands.

Prominent Players in Coagulation Factor Concentrate Market

- •Pfizer Inc. (United States)

- •Takeda Pharmaceutical Company Limited (Japan)

- •Baxalta Incorporated (United States)

- •Bayer AG (Germany)

- •Octapharma AG (Switzerland)

- •CSL Behring (Australia)

- •Grifols, S.A. (Spain)

- •Novo Nordisk A/S (Denmark)

- •LFB Group (France)

- •Sobi (Sweden)

- •Haemonetics Corporation (United States)

- •Shire plc (Ireland)

- •Bioverativ Inc. (United States)

- •Mitsubishi Tanabe Pharma Corporation (Japan)

- •Chugai Pharmaceutical Co., Ltd. (Japan)

- •Zhejiang Hisun Pharmaceutical Co., Ltd. (China)

- •LFB Biomedicaments (France)

- •China Biologic Products Holdings, Inc. (China)

- •Sangamo Therapeutics, Inc. (United States)

- •Grifols Therapeutics LLC (United States)

- •Mylan N.V. (United States)

- •Cangene Corporation (Canada)

- •F. Hoffmann-La Roche AG (Switzerland)

- •BioMarin Pharmaceutical Inc. (United States)

- •UniQure N.V. (Netherlands)

Market Breakdown

- •By Product Type

- ◦Plasma-Derived Concentrates

- ◦Recombinant Concentrates

- ◦Extended Half-Life Concentrates

- ◦Prothrombin Complex Concentrates

- ◦Activated Factor Concentrates

- •By Application

- ◦Hemophilia A

- ◦Hemophilia B

- ◦Von Willebrand Disease

- ◦Acquired Coagulation Disorders

- ◦Other Bleeding Disorders

- •By End-Use Industry

- ◦Hospitals

- ◦Specialty Clinics

- ◦Homecare Settings

- ◦Research Institutes

- •By Distribution Channel

- ◦Hospital Pharmacies

- ◦Retail Pharmacies

- ◦Online Pharmacies

Growth Dynamics

The global coagulation factor concentrate market is driven by increasing prevalence and diagnosis of bleeding disorders worldwide, which has led to heightened demand for effective therapies. Advances in recombinant DNA technology and bioprocessing have yielded safer, more efficacious concentrates, including extended half-life products that reduce infusion frequency and enhance patient quality of life. Favorable reimbursement policies and growing awareness among healthcare providers and patients further stimulate market growth. Additionally, emerging markets, particularly in Asia-Pacific and Latin America, offer significant expansion opportunities due to improving healthcare infrastructure and increasing government initiatives. Continuous research and development investments by industry players to innovate novel therapeutics and biosimilars contribute to sustained market momentum. These factors collectively underpin a robust growth trajectory for coagulation factor concentrates globally.

Market Trends

The coagulation factor concentrate market is witnessing a trend towards personalized medicine, with tailored treatment regimens based on genetic profiling and patient-specific factors. Additionally, there is an increased adoption of extended half-life concentrates, which improve adherence by reducing dosing frequency. Technological integration such as digital health platforms and remote monitoring is enhancing patient engagement and treatment outcomes. The growing focus on gene therapy as a potential curative approach is also influencing market dynamics, prompting pharmaceutical companies to diversify their portfolios. Furthermore, collaborations between biotech firms and healthcare providers are fostering innovation and accelerating product development pipelines, shaping the future landscape of coagulation therapeutics.

Market Opportunities

Significant opportunities exist in emerging regions like Asia-Pacific and Latin America, where rising healthcare expenditure and improved diagnostic capabilities are expanding the patient base. Development of biosimilar coagulation factor concentrates presents a cost-effective alternative, enabling broader market penetration and accessibility. Additionally, expanding indications for coagulation factors beyond traditional hemophilia treatment, such as acquired bleeding disorders and surgical prophylaxis, open new avenues for growth. Investments in gene therapy and novel delivery systems also provide avenues for differentiation and long-term value creation. Strategic partnerships and acquisitions can facilitate market entry and portfolio expansion, capitalizing on unmet clinical needs and evolving healthcare landscapes.

Market Challenges

Despite favorable growth prospects, the coagulation factor concentrate market faces challenges including high treatment costs that limit accessibility, particularly in low- and middle-income countries. Regulatory complexities and stringent approval processes can delay product launches and increase development costs. Immunogenicity concerns and the risk of inhibitor development in patients pose clinical challenges requiring continuous innovation. Supply chain constraints, including plasma sourcing and manufacturing scalability, impact product availability. Additionally, competition from emerging gene therapies and alternative treatment modalities introduces uncertainty in long-term market dynamics. Addressing these challenges requires coordinated efforts among manufacturers, regulators, and healthcare providers to optimize patient outcomes and market sustainability.

Regulatory Framework

Between 2020 and 2025, regulatory authorities worldwide have enforced stringent guidelines governing the safety, efficacy, and quality of coagulation factor concentrates. Agencies such as the FDA, EMA, and PMDA require comprehensive clinical data demonstrating product safety, including immunogenicity and viral inactivation validation for plasma-derived products. Post-market surveillance and risk management plans have been mandated to monitor adverse events and ensure ongoing patient safety. Regulatory frameworks also address biosimilar approvals with tailored requirements to facilitate faster market access while maintaining rigorous standards. Regional mandates emphasize traceability, labeling, and pharmacovigilance to enhance transparency and patient confidence. Additionally, expedited review pathways and orphan drug designations have been implemented to incentivize innovation and address unmet medical needs in rare bleeding disorders. These evolving regulations impact market entry strategies, manufacturing practices, and compliance costs, shaping industry operations globally.

Market Intelligence

- •15th February 2025, Pfizer Inc. announced the launch of a next-generation recombinant coagulation factor concentrate with an extended half-life, targeting hemophilia A patients. This product utilizes innovative PEGylation technology to reduce infusion frequency, thereby improving patient adherence and quality of life. The launch is aligned with Pfizer’s strategic focus on rare disease therapeutics and expands its hematology portfolio. Clinical trials demonstrated superior efficacy and safety profiles compared to existing treatments, positioning the product competitively in the global market. This development is expected to accelerate market growth, particularly in North America and Europe, where demand for advanced therapies is high. Source: Pfizer official press release.

- •8th April 2025, Takeda Pharmaceutical Company Limited introduced a biosimilar recombinant factor VIII concentrate in the Asia-Pacific region, addressing affordability and accessibility challenges. This strategic move aims to capture the growing patient population in emerging markets by offering cost-effective alternatives without compromising quality. The product received regulatory approval following robust clinical evaluations, supporting its safety and efficacy. Takeda’s initiative reflects broader industry trends towards biosimilar adoption and market expansion in developing economies. Market analysts anticipate positive reception driven by increasing hemophilia diagnosis rates and improving healthcare infrastructure in the region. Source: Takeda corporate announcement.

- •20th June 2025, Bayer AG announced a strategic collaboration with a biotechnology firm to develop gene therapy candidates for hemophilia B. This partnership leverages advanced vector technology to potentially offer curative treatment options, reducing lifelong dependence on factor concentrates. Bayer plans to integrate this pipeline with its existing coagulation portfolio to provide comprehensive patient care solutions. The collaboration highlights the market’s evolution towards next-generation therapies and reflects industry commitment to innovation. This initiative is expected to influence competitive dynamics and stimulate further investment in gene therapy research. Source: Bayer official press release.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 7.5 Billion |

| Forecast Year Market Size | USD 15.8 Billion |

| CAGR | 8.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.9% |

| Scope of Report | Market is segmented by Product Type (Plasma-Derived Concentrates, Recombinant Concentrates, Extended Half-Life Concentrates, Prothrombin Complex Concentrates, Activated Factor Concentrates), Application (Hemophilia A, Hemophilia B, Von Willebrand Disease, Acquired Coagulation Disorders, Other Bleeding Disorders), End-Use Industry (Hospitals, Specialty Clinics, Homecare Settings, Research Institutes), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Pfizer Inc. (United States), Takeda Pharmaceutical Company Limited (Japan), Baxalta Incorporated (United States), Bayer AG (Germany), Octapharma AG (Switzerland), CSL Behring (Australia), Grifols, S.A. (Spain), Novo Nordisk A/S (Denmark), LFB Group (France), Sobi (Sweden), Haemonetics Corporation (United States), Shire plc (Ireland), Bioverativ Inc. (United States), Mitsubishi Tanabe Pharma Corporation (Japan), Chugai Pharmaceutical Co., Ltd. (Japan), Zhejiang Hisun Pharmaceutical Co., Ltd. (China), LFB Biomedicaments (France), China Biologic Products Holdings, Inc. (China), Sangamo Therapeutics, Inc. (United States), Grifols Therapeutics LLC (United States), Mylan N.V. (United States), Cangene Corporation (Canada), F. Hoffmann-La Roche AG (Switzerland), BioMarin Pharmaceutical Inc. (United States), UniQure N.V. (Netherlands) |

Global Coagulation Factor Concentrate Market Size, Growth & Revenue 2025-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.