Global Metallic Cable Market Size, Growth & Revenue 2024-2034

Global Metallic Cable Market is segmented by Product Type (Coaxial Cable, Twisted Pair Cable, Shielded Cable, Ribbon Cable, Other Metallic Cables), Application (Power Transmission, Telecommunications, Industrial Machinery, Construction, Automotive), End-Use Industry (Energy & Utilities, Telecom & IT, Automotive & Transportation, Building & Construction), Distribution Channel (Direct Sales, Distributors & Dealers, Online Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Metallic Cable Market is a pivotal sector within the electrical and telecommunications industries, comprising an array of metal-based cables used for efficient power transmission and data communication. This market includes various cable types such as coaxial, twisted pair, shielded, and ribbon cables, each engineered to meet distinct technical specifications and application demands. The market's scope extends across diverse end-use industries including power utilities, automotive, construction, and industrial machinery, emphasizing its essential role in infrastructure development and technological growth worldwide. Driven by rapid urbanization, expanding telecommunication networks, and increased adoption of automation in industrial sectors, the metallic cable market is poised for significant expansion. Key characteristics include high electrical conductivity, durability, and compatibility with modern communication technologies, supporting the global demand for reliable and high-performance cabling solutions. The market also encompasses the manufacturing processes, distribution networks, and regulatory frameworks governing cable standards internationally.

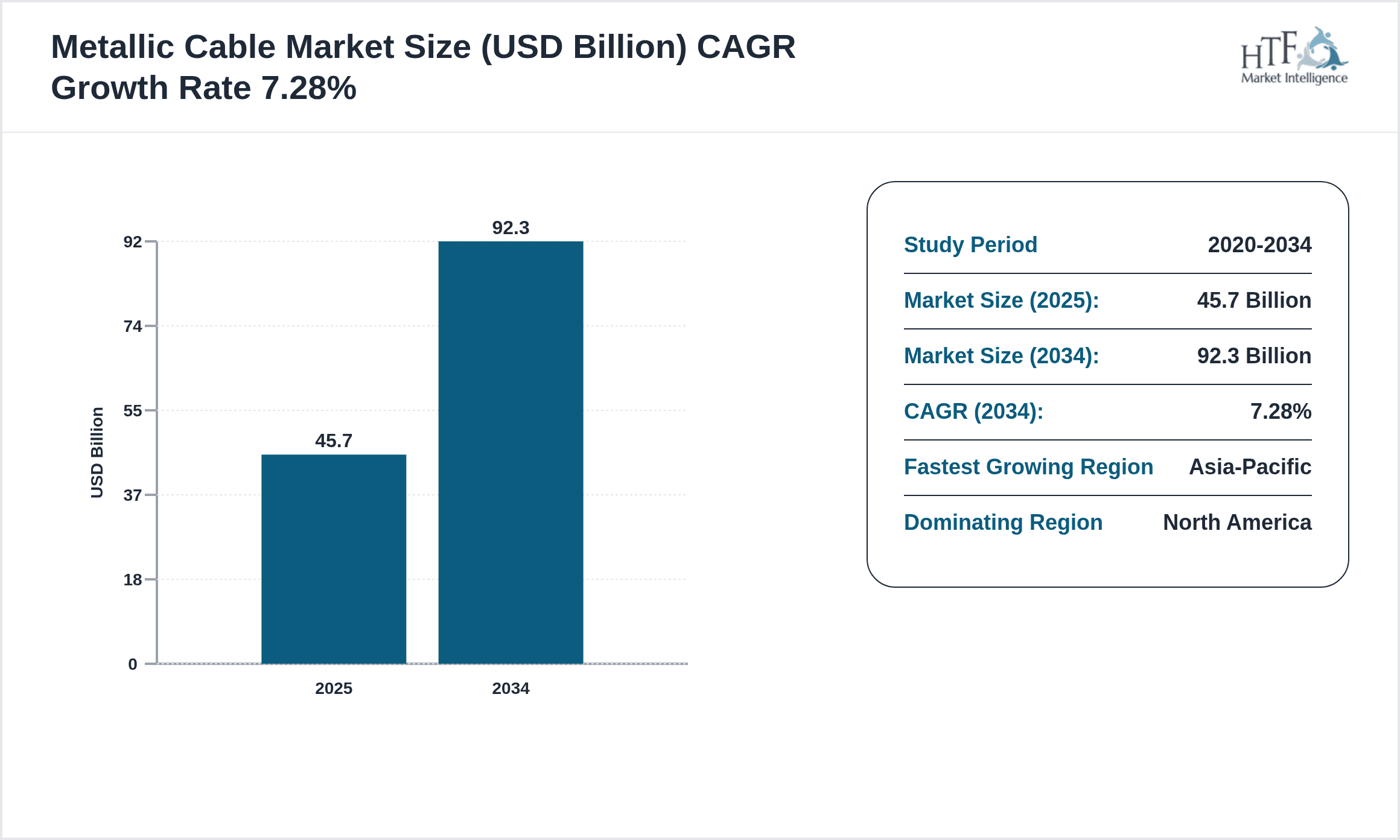

- •Market highlights include a robust CAGR of 7.28% projected from 2024 to 2034, with the market size expected to double from USD 45.7 billion in 2024 to USD 92.3 billion by 2034. North America currently dominates market revenue due to advanced infrastructure and technological adoption, while Asia-Pacific is the fastest-growing region driven by industrialization and expanding telecommunications infrastructure. Coaxial cables hold the largest market share among product types, supported by their extensive use in broadband and broadcasting applications, whereas shielded cables are witnessing the fastest growth due to increasing demand for interference-free data transmission in industrial settings. Power transmission remains the leading application segment, reflecting the global emphasis on expanding energy infrastructure and grid modernization.

- •The metallic cable market offers significant value propositions to stakeholders, including manufacturers, distributors, and end-users, by enabling efficient energy and data transmission critical for modern communication and power systems. Its strategic importance is underscored by ongoing investments in smart grid technologies, 5G deployments, and industrial automation, which rely heavily on high-quality metallic cables. Additionally, the market supports environmental sustainability through advancements in cable materials and insulation technologies that reduce energy loss and enhance durability. By addressing the growing demand for connectivity and power distribution, the metallic cable market contributes to economic growth, infrastructure resilience, and technological innovation on a global scale.

Competitive Landscape

The competitive environment in the global metallic cable market is characterized by intense rivalry among established multinational corporations and emerging regional players. Market leaders differentiate themselves through continuous innovation in cable design, materials, and manufacturing technologies to enhance performance and compliance with evolving standards. Strategic partnerships and collaborations are prevalent as companies seek to expand their geographic presence and product portfolios. Mergers and acquisitions are key strategies employed to consolidate market share, access new technologies, and leverage economies of scale. Pricing strategies remain competitive due to raw material cost fluctuations and customer demand for cost-effective yet high-quality solutions. Furthermore, companies are investing in digital transformation and sustainability initiatives to align with regulatory requirements and customer expectations, shaping future competitive dynamics. Market entry barriers such as high capital investment and stringent quality certifications also influence competitive positioning and long-term viability.

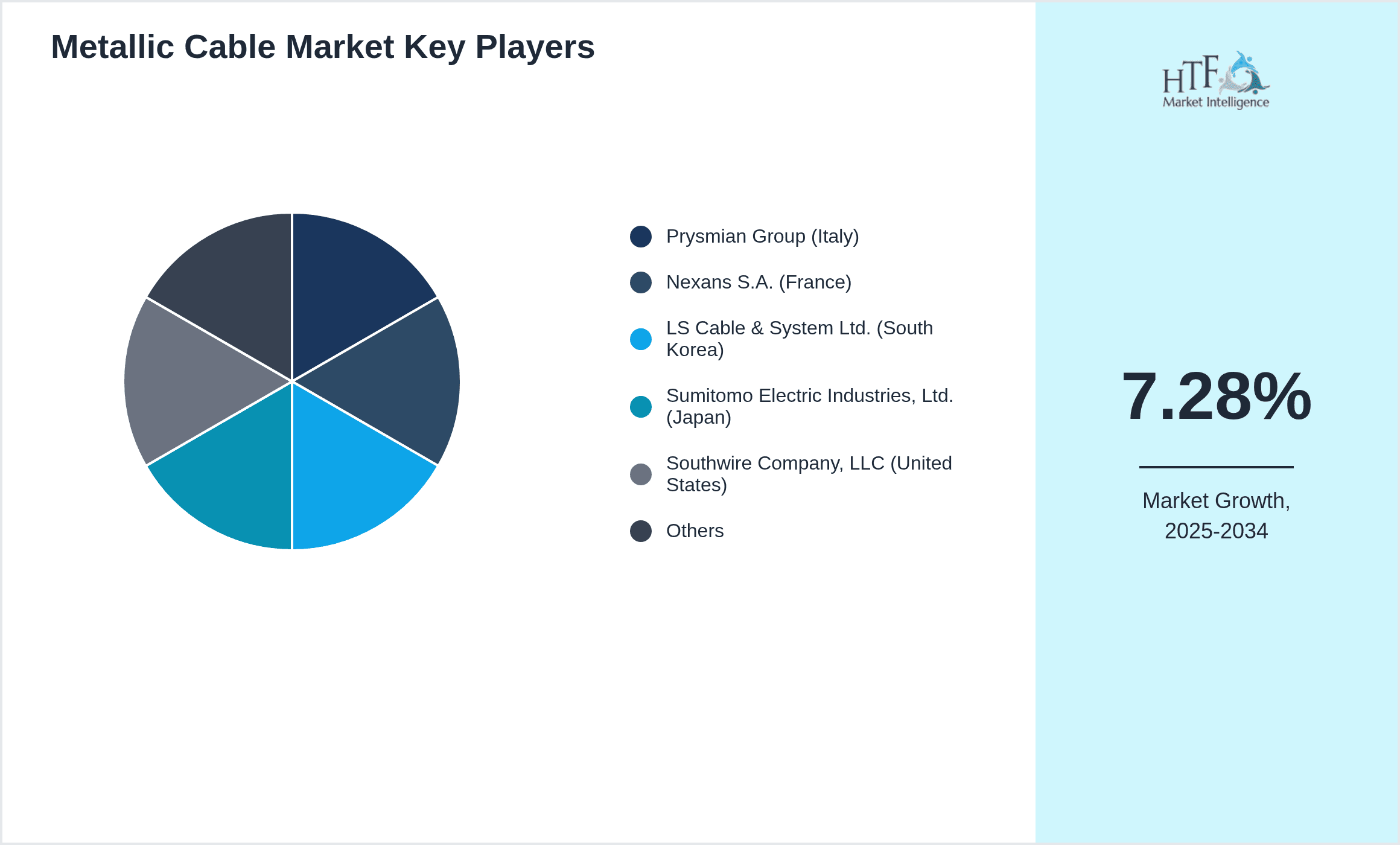

Companies Shaping the Metallic Cable Market

- •Prysmian Group (Italy)

- •Nexans S.A. (France)

- •LS Cable & System Ltd. (South Korea)

- •Sumitomo Electric Industries, Ltd. (Japan)

- •Southwire Company, LLC (United States)

- •General Cable Corporation (United States)

- •Hengtong Group Co., Ltd. (China)

- •Furukawa Electric Co., Ltd. (Japan)

- •Belden Inc. (United States)

- •Chongqing Cable Company Limited (China)

- •Encore Wire Corporation (United States)

- •Leoni AG (Germany)

- •NKT A/S (Denmark)

- •Hubbell Incorporated (United States)

- •Taihan Electric Wire Co., Ltd. (South Korea)

- •South East Cable Group (United Kingdom)

- •KEI Industries Limited (India)

- •Encore Wire Corporation (United States)

- •General Cable Corporation (United States)

- •Prysmians Cables & Systems Ltd. (United Kingdom)

- •Zhejiang Hengdian Group Co., Ltd. (China)

- •Sumitomo Wiring Systems, Ltd. (Japan)

- •LS Industrial Systems Co., Ltd. (South Korea)

- •Taiyo Cabletec Corporation (Japan)

- •Polycab Wires Private Limited (India)

Market Breakdown

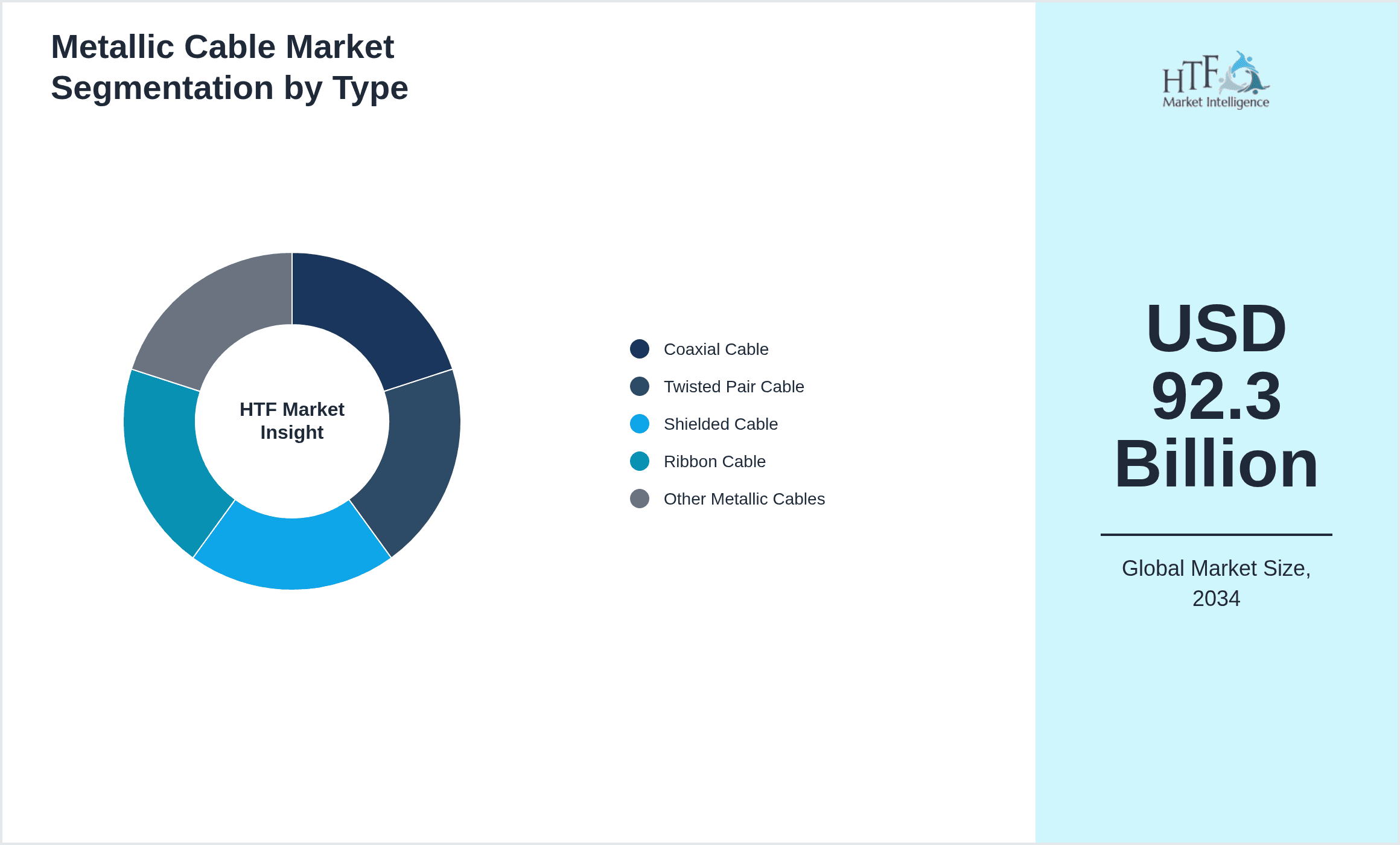

- •By Product Type

- ◦Coaxial Cable

- ◦Twisted Pair Cable

- ◦Shielded Cable

- ◦Ribbon Cable

- ◦Other Metallic Cables

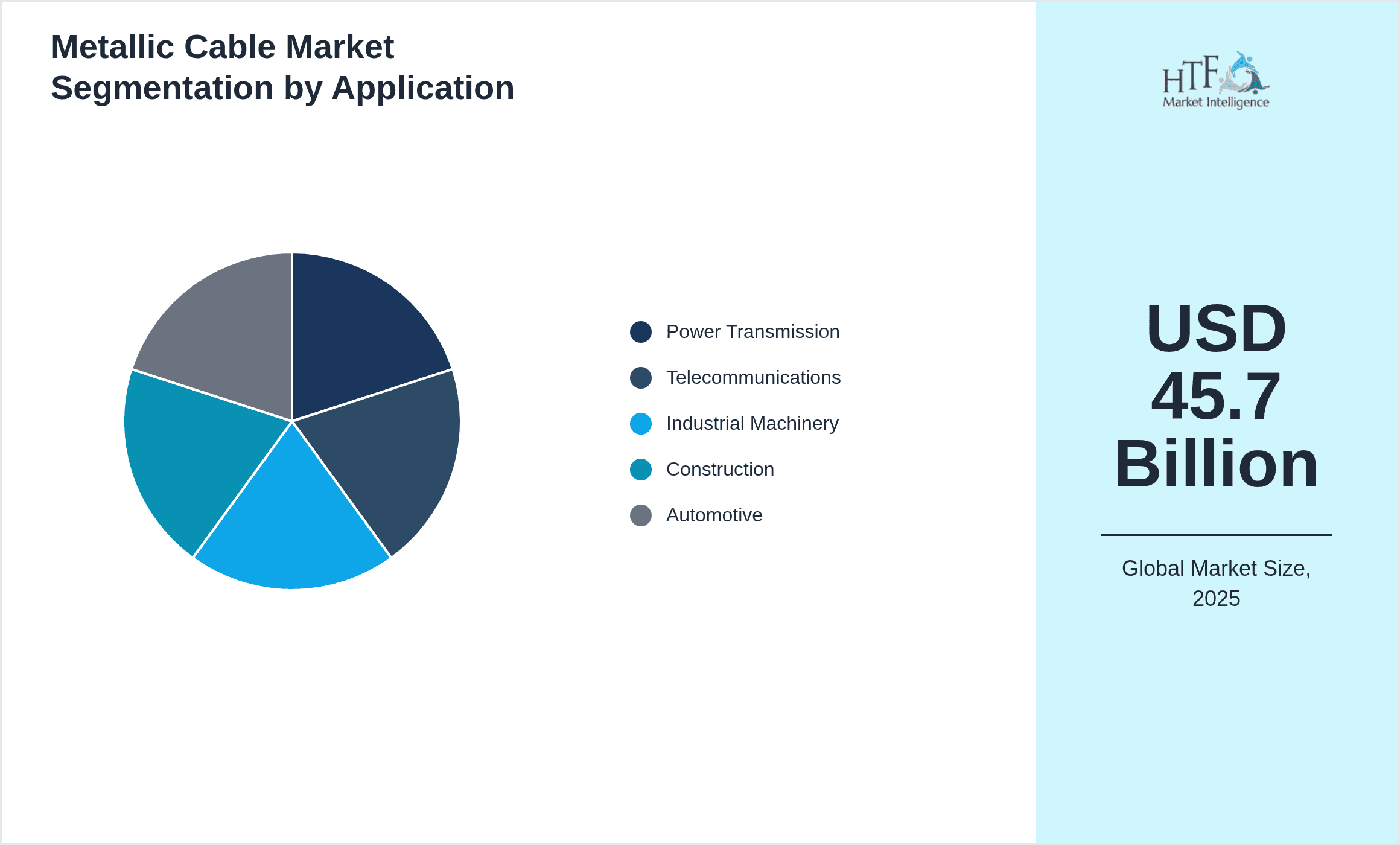

- •By Application

- ◦Power Transmission

- ◦Telecommunications

- ◦Industrial Machinery

- ◦Construction

- ◦Automotive

- •By End-Use Industry

- ◦Energy & Utilities

- ◦Telecom & IT

- ◦Automotive & Transportation

- ◦Building & Construction

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Dealers

- ◦Online Sales

Growth Dynamics

- •Increasing global demand for reliable power transmission infrastructure is a primary growth driver, with governments investing heavily in smart grid technologies and renewable energy integration, boosting metallic cable requirements.

- •The rapid expansion of telecommunications networks, including 5G rollout, fuels demand for high-performance metallic cables capable of supporting faster data transmission with minimal interference.

- •Technological advancements in cable materials and manufacturing processes enhance durability and performance, encouraging adoption in harsh industrial and automotive environments.

- •Urbanization and expanding construction activities worldwide increase the need for robust cabling solutions in commercial and residential buildings, driving market growth.

- •Rising preference for shielded cables in industrial automation to reduce electromagnetic interference is accelerating segment growth, supported by increasing industrial digitization.

- •Growing investments in electric vehicles and smart transportation systems create new applications for metallic cables with specialized design requirements.

- •Government incentives promoting infrastructure modernization in developing regions stimulate demand, particularly in Asia-Pacific and Latin America.

Market Trends

- •The shift towards eco-friendly and recyclable cable materials is gaining traction, aligning with global sustainability goals and regulatory pressures.

- •Integration of IoT and smart sensors in metallic cables enhances real-time monitoring capabilities, improving maintenance and operational efficiency.

- •Manufacturers are increasingly adopting automation and Industry 4.0 technologies in production to improve quality and reduce costs.

- •Collaborations between cable manufacturers and technology firms are fostering innovation in cable design and application-specific solutions.

- •Rising adoption of armored and shielded cables in hazardous environments reflects growing industry focus on safety and reliability.

- •Digital sales channels and e-commerce platforms are becoming significant distribution avenues, enhancing market accessibility and customer reach.

- •Emerging markets in Asia-Pacific and Latin America are witnessing accelerated demand due to infrastructure development and industrialization.

Market Opportunities

- •Expanding renewable energy projects globally present opportunities for metallic cables designed for high voltage and harsh environmental conditions.

- •Development of specialized cables for electric vehicle charging infrastructure offers significant growth potential in the automotive sector.

- •Emerging applications in smart cities and IoT-enabled infrastructure create demand for advanced metallic cable solutions with integrated sensing capabilities.

- •Geographical expansion into underpenetrated markets in Africa and the Middle East can drive incremental revenue streams for manufacturers.

- •Investment in R&D to develop lightweight and flexible cables can cater to next-generation industrial and telecommunication needs.

- •Strategic partnerships with technology providers can enhance product innovation and market penetration globally.

- •Increasing demand for retrofit and replacement cabling in aging infrastructure offers substantial aftermarket opportunities.

Market Challenges

- •Fluctuating raw material prices, particularly copper and aluminum, pose significant cost challenges impacting profitability and pricing strategies.

- •Stringent regulatory standards and certification requirements increase compliance costs and time-to-market for new products.

- •High competition from substitute technologies such as fiber optics in telecommunications restricts metallic cable market share expansion in certain segments.

- •Supply chain disruptions and logistics complexities, especially during global crises, hamper timely delivery and increase operational costs.

- •Environmental concerns related to cable disposal and recycling require manufacturers to invest in sustainable practices and materials.

- •Technical limitations regarding cable flexibility and installation in constrained spaces limit adoption in some advanced applications.

- •Talent shortages in skilled manufacturing and engineering roles affect innovation pace and production capabilities.

Regulatory Framework

- •Between 2019 and 2024, international standards such as IEC 60502 and ISO 9001 have been updated to enhance safety and quality parameters for metallic cables, mandating stricter testing and certification processes globally.

- •The European Union's RoHS Directive, reinforced in 2021, limits hazardous substances in cable manufacturing, compelling manufacturers to adopt eco-friendly materials and processes.

- •In North America, the National Electrical Code (NEC) revisions from 2020 introduced enhanced guidelines for cable installation in residential and commercial infrastructure to improve fire safety and electrical performance.

- •China’s Ministry of Industry and Information Technology implemented updated regulations in 2023 focusing on electromagnetic compatibility and environmental impact for metallic cables used in telecommunications and power sectors.

- •Government incentive programs in Asia-Pacific have been established to support infrastructure modernization and adoption of sustainable cabling solutions, promoting compliance with environmental and safety standards through 2024.

Market Intelligence

- •15th January 2025, Prysmian Group launched a new range of low-smoke zero-halogen (LSZH) metallic cables designed for safer use in confined spaces, targeting the construction and transportation sectors. These cables offer enhanced fire resistance and reduced toxic emissions, aligning with global safety standards and increasing demand for sustainable building materials. The launch aims to strengthen Prysmian’s market position in Europe and Asia-Pacific by catering to evolving regulatory requirements and customer preferences for environmentally responsible products. Source: Prysmian Group Official Website

- •9th March 2025, Nexans S.A. introduced an innovative shielded cable series optimized for 5G telecommunications infrastructure, featuring superior electromagnetic interference resistance and flexible installation capabilities. This product targets telecom operators and infrastructure developers looking to upgrade existing networks to support higher data speeds and reliability. The strategic release supports Nexans’ growth in the Asia-Pacific and North America markets, where 5G deployments are accelerating rapidly. Source: Nexans Press Release

- •22nd May 2024, Southwire Company, LLC announced a strategic partnership with a leading electric vehicle charging infrastructure provider to develop specialized metallic cables that meet stringent durability and performance standards required for EV applications. This collaboration focuses on co-developing next-generation cable solutions that support fast charging and enhanced safety. The initiative positions Southwire to capitalize on the growing EV market in North America and Europe. Source: Southwire Corporate News

- •11th November 2024, LS Cable & System Ltd. completed the acquisition of a regional cable manufacturer in Southeast Asia to expand its footprint and production capacity in emerging markets. The acquisition includes advanced manufacturing facilities and a diversified product portfolio, enabling LS Cable to better serve the Asia-Pacific region's growing infrastructure demands. This move strengthens LS Cable’s competitive edge amid rising regional demand for metallic cables across multiple industries. Source: LS Cable & System News

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45.7 Billion |

| Forecast Year Market Size | USD 92.3 Billion |

| CAGR | 7.28% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.03% |

| Scope of Report | Market is segmented by Product Type (Coaxial Cable, Twisted Pair Cable, Shielded Cable, Ribbon Cable, Other Metallic Cables), Application (Power Transmission, Telecommunications, Industrial Machinery, Construction, Automotive), End-Use Industry (Energy & Utilities, Telecom & IT, Automotive & Transportation, Building & Construction), Distribution Channel (Direct Sales, Distributors & Dealers, Online Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Prysmian Group (Italy), Nexans S.A. (France), LS Cable & System Ltd. (South Korea), Sumitomo Electric Industries, Ltd. (Japan), Southwire Company, LLC (United States), General Cable Corporation (United States), Hengtong Group Co., Ltd. (China), Furukawa Electric Co., Ltd. (Japan), Belden Inc. (United States), Chongqing Cable Company Limited (China), Encore Wire Corporation (United States), Leoni AG (Germany), NKT A/S (Denmark), Hubbell Incorporated (United States), Taihan Electric Wire Co., Ltd. (South Korea), South East Cable Group (United Kingdom), KEI Industries Limited (India), Encore Wire Corporation (United States), General Cable Corporation (United States), Prysmians Cables & Systems Ltd. (United Kingdom), Zhejiang Hengdian Group Co., Ltd. (China), Sumitomo Wiring Systems, Ltd. (Japan), LS Industrial Systems Co., Ltd. (South Korea), Taiyo Cabletec Corporation (Japan), Polycab Wires Private Limited (India) |

Global Metallic Cable Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.