Global Health Care Information System Market Size, Growth & Revenue 2025-2034

Global Health Care Information System Market is segmented by Product Type (Electronic Health Records, Practice Management Software, Revenue Cycle Management, Telemedicine Solutions, Patient Engagement Solutions), Application (Hospital Information System, Clinical Information System, Ambulatory Care Information System, Imaging Information System, Pharmacy Information System), End-Use Industry (Hospitals, Clinics, Ambulatory Care Centers, Telehealth Providers), Distribution Channel (Direct Sales, Channel Partners, Digital Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Health Care Information System market is a dynamic and rapidly evolving sector that integrates advanced software solutions to optimize healthcare delivery worldwide. This market encompasses various products such as Electronic Health Records (EHR), Practice Management Software, Revenue Cycle Management, Telemedicine Solutions, and Patient Engagement platforms, which collectively enhance clinical efficiency, patient data management, and administrative processes across hospitals, clinics, and ambulatory care centers. The applications span Hospital Information Systems, Clinical Information Systems, Ambulatory Care Information Systems, Imaging Information Systems, and Pharmacy Information Systems, enabling seamless healthcare operations and improved patient outcomes. Driven by the increasing need for digital transformation, regulatory compliance, and cost containment in healthcare, these systems are pivotal for supporting evidence-based medicine, remote patient monitoring, and interoperability between diverse healthcare stakeholders. The market has witnessed significant growth fueled by technological advancements, rising adoption of telehealth services, and demand for real-time data analytics, positioning it as a critical component in modern healthcare infrastructure. As global healthcare ecosystems become more complex, Health Care Information Systems continue to evolve, integrating artificial intelligence and cloud computing to deliver scalable, secure, and patient-centric solutions that address challenges such as data security, workflow optimization, and care coordination.

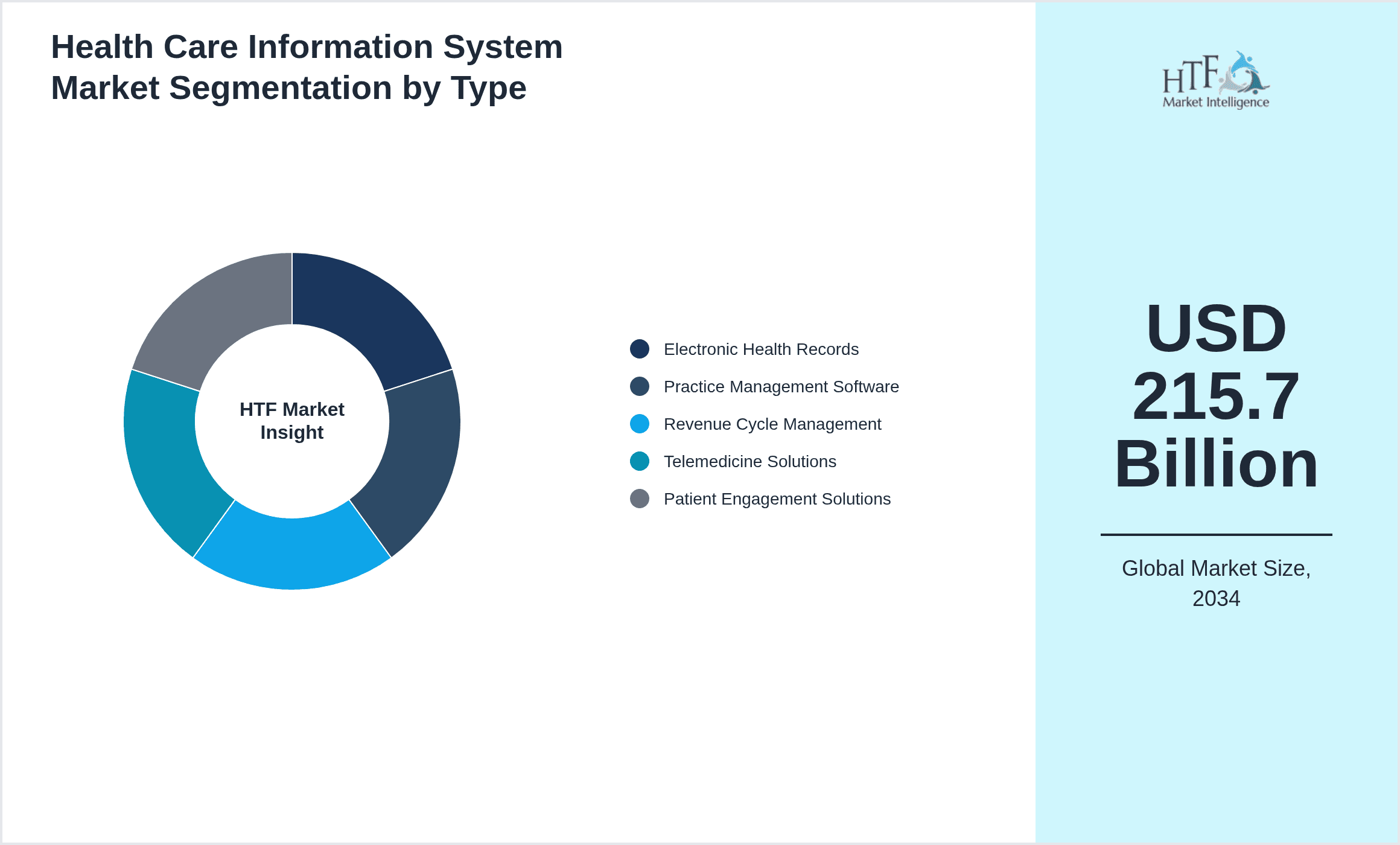

- •Key market highlights include a robust CAGR of 11.3% from 2025 to 2034, with the market size expanding from USD 85.5 Billion in 2025 to an anticipated USD 215.7 Billion by 2034. North America currently dominates the market, attributed to extensive healthcare IT infrastructure and early adoption of digital health technologies, while the Asia-Pacific region is identified as the fastest growing due to increasing healthcare expenditure, government initiatives, and rising telemedicine penetration. Electronic Health Records remain the leading product type, offering comprehensive patient data management, whereas Telemedicine Solutions are the fastest growing segment, propelled by the global shift towards remote care and virtual consultations. The market is characterized by continuous innovation, strategic partnerships, and rising investments aimed at enhancing system interoperability, patient engagement, and regulatory compliance, driving sustained growth and expanding application across diverse healthcare settings.

- •The Health Care Information System market presents significant value to healthcare providers, payers, technology vendors, and policymakers by facilitating improved clinical outcomes, operational efficiency, and patient satisfaction. These systems support strategic decision-making through data analytics and enable compliance with evolving healthcare regulations. Furthermore, the market's growth is underpinned by the increasing prevalence of chronic diseases, aging populations, and the need for cost-effective care delivery models. Stakeholders leverage these solutions to enhance care coordination, reduce medical errors, and expand access to healthcare services, particularly through telehealth. As digital transformation accelerates globally, the Health Care Information System market remains a cornerstone for healthcare modernization, offering scalable, interoperable, and secure platforms vital for future-ready healthcare ecosystems.

Competitive Landscape

The competitive environment in the Global Health Care Information System market is marked by intense rivalry among established technology providers and emerging innovators striving to capture market share through product differentiation, technological innovation, and strategic collaborations. Market leaders focus on expanding their portfolios by integrating artificial intelligence, machine learning, and cloud-based services to enhance system capabilities such as predictive analytics, patient engagement, and interoperability. Key competitive strategies include mergers and acquisitions to consolidate technological expertise and geographic reach, partnerships with healthcare providers for customized solution development, and investments in research and development to stay ahead in regulatory compliance and data security standards. Pricing strategies are tailored to accommodate diverse customer segments ranging from large hospital networks to small clinics, with subscription-based and scalable deployment models gaining traction. Distribution channels encompass direct sales, channel partners, and digital platforms, facilitating broad market penetration. Regional competition is influenced by varying levels of healthcare IT adoption, with North America and Europe exhibiting mature markets while Asia-Pacific and Latin America present high-growth opportunities. Future trends in competition will be shaped by advancements in interoperability frameworks, patient-centric designs, and the integration of telehealth and mobile health applications, necessitating agility and innovation from market participants to maintain competitive advantages.

Prominent Players in Health Care Information System Market

- •Cerner Corporation (United States)

- •Epic Systems Corporation (United States)

- •Allscripts Healthcare Solutions, Inc. (United States)

- •McKesson Corporation (United States)

- •Philips Healthcare (Netherlands)

- •Siemens Healthineers (Germany)

- •GE Healthcare (United States)

- •athenahealth, Inc. (United States)

- •MEDITECH (United States)

- •Optum, Inc. (United States)

- •NextGen Healthcare, Inc. (United States)

- •IBM Watson Health (United States)

- •eClinicalWorks (United States)

- •Netsmart Technologies (United States)

- •CPSI (Computer Programs and Systems, Inc.) (United States)

- •HCL Technologies (India)

- •Fujitsu Limited (Japan)

- •Hitachi, Ltd. (Japan)

- •Dell Technologies (United States)

- •Oracle Corporation (United States)

- •IBM Corporation (United States)

- •Infor, Inc. (United States)

- •Cerner Middle East (United Arab Emirates)

- •Philips Asia (Singapore)

- •Samsung SDS (South Korea)

Market Breakdown

- •By Product Type

- ◦Electronic Health Records

- ◦Practice Management Software

- ◦Revenue Cycle Management

- ◦Telemedicine Solutions

- ◦Patient Engagement Solutions

- •By Application

- ◦Hospital Information System

- ◦Clinical Information System

- ◦Ambulatory Care Information System

- ◦Imaging Information System

- ◦Pharmacy Information System

- •By End-Use Industry

- ◦Hospitals

- ◦Clinics

- ◦Ambulatory Care Centers

- ◦Telehealth Providers

- •By Distribution Channel

- ◦Direct Sales

- ◦Channel Partners

- ◦Digital Platforms

Growth Dynamics

The Global Health Care Information System market is propelled by the increasing digitization of healthcare services, driven by the need for streamlined patient data management and operational efficiency. Rising chronic disease prevalence and aging populations worldwide necessitate advanced solutions for care coordination, driving demand for integrated healthcare IT systems. Technological advancements such as artificial intelligence, cloud computing, and big data analytics are enhancing system capabilities, enabling predictive diagnostics and personalized medicine. Government initiatives and regulatory mandates to adopt electronic health records and improve healthcare data interoperability further accelerate market growth. Additionally, the COVID-19 pandemic has underscored the critical importance of telemedicine and remote monitoring solutions, boosting adoption rates across regions. Strategic investments and partnerships among healthcare providers and technology firms facilitate continuous innovation, expanding the market’s reach into emerging economies. Furthermore, increasing patient awareness and demand for improved healthcare experiences propel the integration of patient engagement tools within health care information systems, contributing to sustained market expansion.

Market Trends

A prominent trend in the Health Care Information System market is the rapid adoption of cloud-based solutions, which offer scalability, cost-efficiency, and enhanced data security. Healthcare providers are increasingly leveraging cloud platforms to facilitate interoperability and real-time data access across multiple care settings. The integration of artificial intelligence and machine learning is transforming clinical decision support systems, enabling predictive analytics and early diagnosis. Telemedicine platforms have gained significant traction, driven by regulatory relaxation and increased patient acceptance, fostering virtual care delivery. Additionally, there is a growing emphasis on patient-centric technologies, including mobile health applications and wearable integrations, to empower patients in managing their health proactively. The market is also witnessing strategic collaborations between healthcare IT vendors and pharmaceutical companies to leverage health data for drug development and clinical trials. Sustainability and data privacy concerns are shaping development priorities, with vendors adopting HIPAA-compliant and GDPR-aligned frameworks to ensure regulatory adherence.

Market Opportunities

Emerging economies present significant opportunities for Health Care Information System vendors due to increasing healthcare spending, expanding infrastructure, and growing awareness of digital health benefits. The rising adoption of telemedicine in remote and underserved regions offers potential for market penetration, supported by government incentives and improved internet connectivity. Integration of AI-driven analytics into health care systems opens avenues for innovative diagnostic and treatment solutions, enhancing clinical outcomes and operational efficiencies. The growing emphasis on personalized medicine and patient engagement creates demand for customized software solutions that cater to individual health needs. Furthermore, expansion into specialty care segments such as oncology, cardiology, and mental health presents niche opportunities for tailored information systems. Strategic partnerships with healthcare providers and technology firms can facilitate co-development of advanced platforms, accelerating market growth. The evolving regulatory landscape, with mandates for electronic health records and data interoperability, also drives demand for compliant and secure systems, creating a favorable environment for new entrants and existing players alike.

Market Challenges

The Health Care Information System market faces several challenges, including high implementation costs and complexity, which can deter small and medium-sized healthcare providers from adoption. Data security and privacy concerns remain paramount, with frequent cyber threats targeting sensitive patient information, necessitating robust compliance with regulations such as HIPAA and GDPR. Interoperability issues due to heterogeneous systems and lack of standardized protocols hinder seamless data exchange across different healthcare entities. Resistance to change and limited IT expertise among healthcare staff can slow down technology integration and utilization. Additionally, regulatory uncertainties and evolving compliance requirements create barriers for vendors and users alike. The need for continuous system upgrades and maintenance adds to operational expenses, impacting overall profitability. Furthermore, disparities in healthcare infrastructure across regions pose challenges for uniform adoption, particularly in developing countries where digital health literacy and connectivity may be limited.

Regulatory Framework

Between 2020 and 2025, several key regulations shaped the Health Care Information System market globally. HIPAA (Health Insurance Portability and Accountability Act) in the United States mandated strict standards for patient data privacy and security, compelling vendors to implement advanced encryption and access controls. The European Union’s GDPR (General Data Protection Regulation), effective since 2018 but continuously enforced through 2025, established rigorous data protection requirements, influencing system design and cross-border data transfer protocols. The United States also saw the HITECH Act promoting meaningful use of electronic health records, incentivizing healthcare providers to adopt certified EHR technology. Additionally, the FDA updated its guidance on software as a medical device (SaMD), setting new compliance and safety standards for health IT products. Various countries implemented national digital health strategies, including India's National Digital Health Mission, fostering interoperability and standardization. These frameworks collectively accelerated market adoption while emphasizing patient privacy, data security, and system interoperability, shaping vendor offerings and deployment models worldwide.

Market Intelligence

- •12th January 2025, Cerner Corporation announced the launch of its next-generation Electronic Health Record platform integrating artificial intelligence and advanced analytics designed to enhance clinical decision-making and patient outcomes. The new platform offers cloud-native deployment, enabling scalable and secure data management across multiple healthcare facilities. Cerner’s solution aims to streamline workflow automation and support telehealth services, targeting hospitals and ambulatory care providers globally. This strategic initiative reinforces Cerner’s commitment to digital transformation in healthcare and positions the company competitively amid rising demand for interoperable and patient-centric systems. The platform also complies with evolving regulatory standards, including HIPAA and GDPR, ensuring robust data privacy and security. Cerner expects this innovation to accelerate adoption rates and expand its market share in key regions such as North America and Asia-Pacific. Source: Cerner official press release.

- •15th March 2025, Philips Healthcare introduced a comprehensive telemedicine solution suite designed to facilitate remote patient monitoring and virtual care delivery. Leveraging cloud computing and IoT devices, the platform supports real-time health data collection and analytics, enabling proactive clinical interventions. The system targets chronic disease management and post-acute care, aiming to reduce hospital readmissions and improve patient engagement. Philips’ innovation addresses growing telehealth demand accelerated by the COVID-19 pandemic and expanding digital health infrastructure worldwide. The solution is compliant with international data security regulations and supports multi-language interfaces to cater to diverse populations. This launch strengthens Philips’ position in the Health Care Information System market and opens new revenue streams in emerging economies. Source: Philips Healthcare press announcement.

- •22nd July 2025, Epic Systems Corporation announced a strategic partnership with IBM Watson Health to integrate advanced AI-powered analytics into its Electronic Health Records platform. This collaboration aims to enhance predictive diagnostics, personalized treatment plans, and operational efficiencies for healthcare providers. The integration will leverage IBM’s cognitive computing capabilities to analyze vast datasets, providing actionable insights at the point of care. Epic’s expanded solution targets large hospital networks and specialty clinics, with planned rollouts in North America and Europe. The partnership is expected to accelerate innovation cycles and improve patient outcomes while maintaining compliance with healthcare regulations globally. This initiative exemplifies the growing trend of technology alliances to address complex healthcare challenges. Source: Epic Systems and IBM Watson Health joint statement.

- •30th October 2025, GE Healthcare completed the acquisition of a leading telehealth software provider to expand its portfolio of virtual care solutions. The acquisition enables GE Healthcare to offer integrated platforms combining medical imaging, patient monitoring, and telemedicine capabilities. This strategic move aligns with GE’s vision to deliver end-to-end digital health solutions, enhancing care coordination and operational efficiency. The company anticipates that the expanded offerings will capitalize on increasing telehealth adoption across North America, Europe, and Asia-Pacific regions. The integration process will emphasize interoperability, cybersecurity, and user-friendly design to meet diverse healthcare provider needs. This acquisition strengthens GE Healthcare’s competitive position and accelerates its growth in the evolving Health Care Information System market. Source: GE Healthcare corporate press release.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 85.5 Billion |

| Forecast Year Market Size | USD 215.7 Billion |

| CAGR | 11.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.2% |

| Scope of Report | Market is segmented by Product Type (Electronic Health Records, Practice Management Software, Revenue Cycle Management, Telemedicine Solutions, Patient Engagement Solutions), Application (Hospital Information System, Clinical Information System, Ambulatory Care Information System, Imaging Information System, Pharmacy Information System), End-Use Industry (Hospitals, Clinics, Ambulatory Care Centers, Telehealth Providers), Distribution Channel (Direct Sales, Channel Partners, Digital Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Cerner Corporation (United States), Epic Systems Corporation (United States), Allscripts Healthcare Solutions, Inc. (United States), McKesson Corporation (United States), Philips Healthcare (Netherlands), Siemens Healthineers (Germany), GE Healthcare (United States), athenahealth, Inc. (United States), MEDITECH (United States), Optum, Inc. (United States), NextGen Healthcare, Inc. (United States), IBM Watson Health (United States), eClinicalWorks (United States), Netsmart Technologies (United States), CPSI (Computer Programs and Systems, Inc.) (United States), HCL Technologies (India), Fujitsu Limited (Japan), Hitachi, Ltd. (Japan), Dell Technologies (United States), Oracle Corporation (United States), IBM Corporation (United States), Infor, Inc. (United States), Cerner Middle East (United Arab Emirates), Philips Asia (Singapore), Samsung SDS (South Korea) |

Global Health Care Information System Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.