Global Laser Atherectomy Devices Market Size, Growth & Revenue 2024-2034

Global Laser Atherectomy Devices Market is segmented by Product Type (Excimer Laser Atherectomy, Excimer Laser with Angioplasty, Excimer Laser with Stent, Other Laser Atherectomy Types), Application (Peripheral Artery Disease, Coronary Artery Disease, Carotid Artery Disease, Renal Artery Disease, Other Applications), End-Use Industry (Hospitals, Cardiovascular Clinics, Outpatient Surgical Centers, Specialized Vascular Centers), Distribution Channel (Direct Sales, Distributors, Online Medical Equipment Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Laser Atherectomy Devices market is defined by its focus on advanced medical equipment designed to treat arterial blockages through laser-based plaque removal. This market's scope encompasses various excimer laser technologies integrated with angioplasty and stenting procedures, offering minimally invasive solutions for cardiovascular diseases affecting peripheral, coronary, carotid, and renal arteries. The devices provide precision, reduced procedural times, and improved patient outcomes compared to traditional atherectomy methods. The market serves a broad range of healthcare providers including hospitals, outpatient surgical centers, and specialized cardiovascular clinics worldwide. Increasing prevalence of cardiovascular disorders, technological innovation, and growing awareness of less invasive treatment options are central to the market's expansion. The industry also encompasses regulatory standards, device manufacturing innovations, and evolving clinical guidelines that collectively shape market dynamics. Primary use cases involve treatment of peripheral artery disease, coronary artery disease, and related vascular conditions with enhanced safety and efficacy profiles.

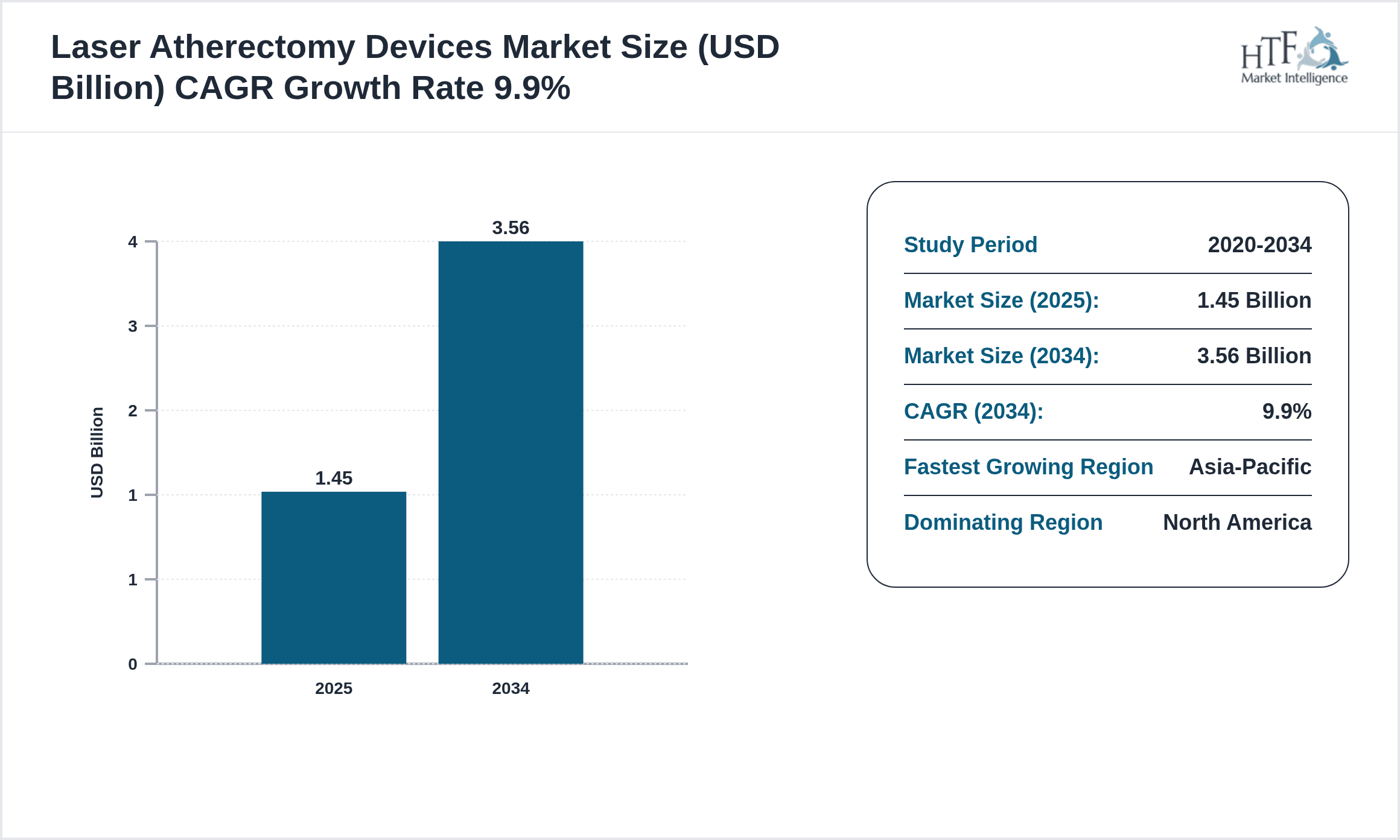

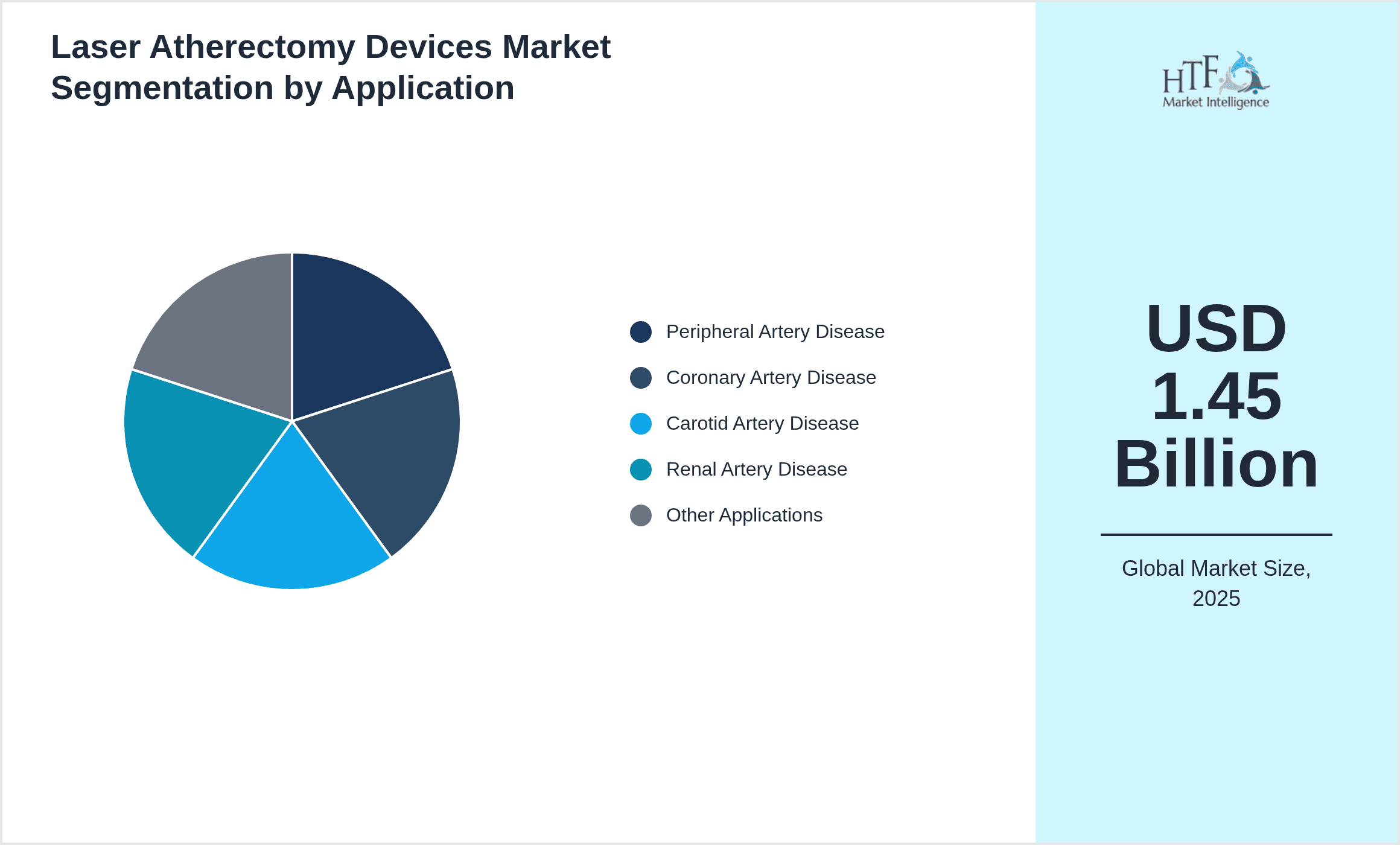

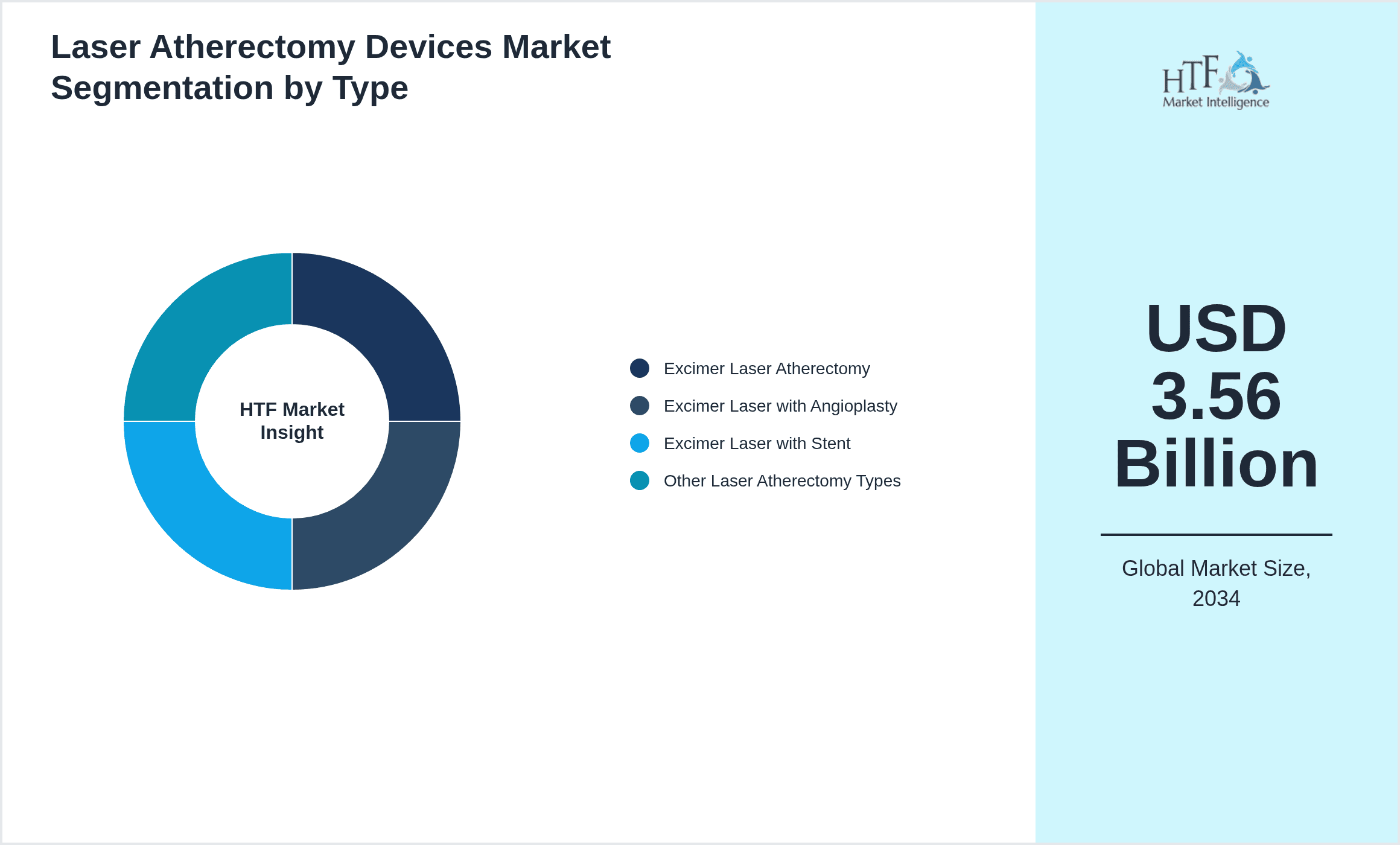

- •Key market highlights include a base market valuation of USD 1.45 Billion in 2024, with projections estimating growth to USD 3.56 Billion by 2034 at a robust CAGR of 9.9%. North America currently dominates the market owing to advanced healthcare infrastructure and early adoption of cutting-edge medical technologies, while Asia-Pacific is identified as the fastest growing region driven by expanding healthcare access and rising cardiovascular disease incidence. Excimer Laser Atherectomy leads as the dominant product type due to its clinical effectiveness, followed by Excimer Laser with Angioplasty showing fastest growth supported by combined procedural advantages. Peripheral artery disease remains the largest application segment globally, benefitting from increasing patient populations and innovative device development improving treatment outcomes.

- •The value proposition of the Laser Atherectomy Devices market lies in providing minimally invasive, precise, and effective vascular intervention options that reduce complications and recovery times. The strategic importance of this market is underscored by its role in addressing the global cardiovascular disease burden, enhancing procedural safety, and enabling clinicians to treat complex arterial lesions with improved success rates. It holds significant potential across healthcare systems seeking to optimize cardiovascular care pathways, reduce hospital stays, and improve quality of life for patients. Stakeholders including device manufacturers, healthcare providers, and regulatory bodies benefit from continuous technological innovation and favorable market trends fostering growth and competitive differentiation.

Competitive Landscape

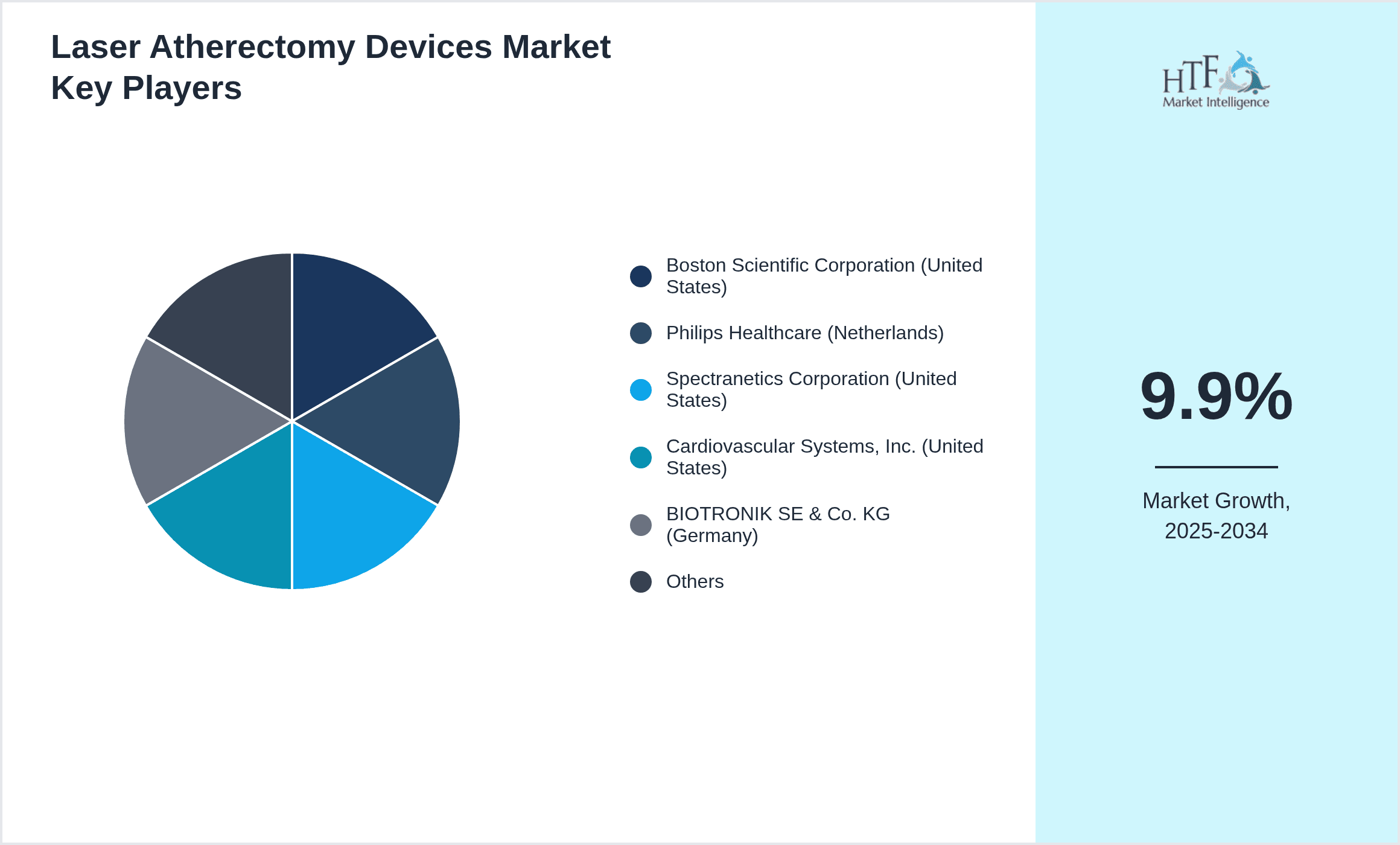

The competitive environment within the Global Laser Atherectomy Devices market is characterized by intense rivalry among key players focused on innovation, strategic partnerships, and expanding geographical reach. Market leaders emphasize continuous product development integrating advanced laser technologies with complementary procedures such as angioplasty and stenting to enhance clinical outcomes. Differentiation is achieved through proprietary laser systems, catheter designs, and minimally invasive delivery mechanisms. Pricing strategies vary by region but generally reflect premium positioning due to device sophistication and clinical benefits. Mergers and acquisitions have played a significant role in consolidating technological expertise and market presence, while collaborations with healthcare providers accelerate adoption. Competitive barriers include high R&D costs, stringent regulatory requirements, and the need for extensive clinical validation. Regional competition dynamics are influenced by healthcare infrastructure, reimbursement policies, and disease prevalence, with North America and Europe maintaining leadership, while Asia-Pacific offers significant growth potential due to increasing healthcare investments and rising cardiovascular disease incidence.

Companies Shaping the Laser Atherectomy Devices Market

- •Boston Scientific Corporation (United States)

- •Philips Healthcare (Netherlands)

- •Spectranetics Corporation (United States)

- •Cardiovascular Systems, Inc. (United States)

- •BIOTRONIK SE & Co. KG (Germany)

- •Terumo Corporation (Japan)

- •Siemens Healthineers AG (Germany)

- •Abbott Laboratories (United States)

- •Medtronic plc (Ireland)

- •Asahi Intecc Co., Ltd. (Japan)

- •Cook Medical (United States)

- •C.R. Bard, Inc. (United States)

- •Boston Scientific Corporation (United States)

- •B. Braun Melsungen AG (Germany)

- •Lumenis Ltd. (Israel)

- •Edwards Lifesciences Corporation (United States)

- •Canon Medical Systems Corporation (Japan)

- •Vascular Solutions, Inc. (United States)

- •Medico S.p.A. (Italy)

- •Hoya Corporation (Japan)

- •Terumo Medical Corporation (United States)

- •AngioDynamics, Inc. (United States)

- •Nipro Corporation (Japan)

- •iVascular, S.L. (Spain)

- •Biosensors International Group, Ltd. (Singapore)

Market Breakdown

- •By Product Type

- ◦Excimer Laser Atherectomy

- ◦Excimer Laser with Angioplasty

- ◦Excimer Laser with Stent

- ◦Other Laser Atherectomy Types

- •By Application

- ◦Peripheral Artery Disease

- ◦Coronary Artery Disease

- ◦Carotid Artery Disease

- ◦Renal Artery Disease

- ◦Other Applications

- •By End-Use Industry

- ◦Hospitals

- ◦Cardiovascular Clinics

- ◦Outpatient Surgical Centers

- ◦Specialized Vascular Centers

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Medical Equipment Platforms

Growth Dynamics

- •The rising global prevalence of cardiovascular diseases, especially peripheral and coronary artery disease, significantly drives demand for laser atherectomy devices as minimally invasive alternatives to surgery. Increasing aging populations and lifestyle-related risk factors contribute to this growth trajectory.

- •Technological advancements in excimer laser systems, including enhanced catheter designs and integrated imaging, improve procedural efficacy and safety, encouraging adoption by clinicians worldwide.

- •Growing healthcare infrastructure investments in emerging economies, particularly within Asia-Pacific, facilitate access to advanced cardiovascular intervention technologies, representing a major growth opportunity.

- •Favorable reimbursement policies and increased awareness of minimally invasive treatments among patients and healthcare providers further stimulate market expansion.

- •Strategic collaborations between device manufacturers and healthcare institutions enable clinical trials and real-world evidence generation, promoting confidence and uptake of laser atherectomy solutions.

Market Trends

- •Integration of laser atherectomy devices with real-time imaging technologies such as intravascular ultrasound enhances precision in plaque removal, representing a significant trend in device innovation.

- •Shift towards combination therapies, including excimer laser atherectomy coupled with angioplasty or stenting, is gaining traction due to improved clinical outcomes and reduced restenosis rates.

- •Increased adoption of outpatient and ambulatory surgical centers for vascular interventions reflects evolving treatment paradigms favoring cost efficiency and patient convenience.

- •Sustainability initiatives are influencing device manufacturing, with companies focusing on reducing environmental impact through eco-friendly materials and processes.

- •Collaborative ecosystems involving device developers, healthcare providers, and regulatory bodies are fostering accelerated innovation and streamlined product approvals.

Market Opportunities

- •Emerging markets in Asia-Pacific and Latin America offer significant growth potential due to increasing cardiovascular disease burden and improving healthcare infrastructure.

- •Development of next-generation laser atherectomy devices with enhanced safety profiles and expanded indications presents attractive opportunities for market entrants and incumbents.

- •Integration of artificial intelligence and machine learning to optimize procedural planning and device performance is a promising avenue for innovation and differentiation.

- •Expanding applications beyond traditional cardiovascular diseases, including treatment of complex lesions and chronic total occlusions, can drive market diversification.

- •Strategic partnerships and acquisitions targeting complementary technologies and regional expansion can accelerate market penetration and revenue growth.

Market Challenges

- •High costs associated with laser atherectomy devices and procedural expenses limit accessibility, especially in low- and middle-income countries, restraining market growth.

- •Complex regulatory pathways and stringent approval requirements across different regions increase time-to-market and development costs for new devices.

- •Limited awareness and adoption among some healthcare providers due to preference for traditional intervention techniques pose barriers to broader market acceptance.

- •Potential complications and safety concerns related to laser energy application necessitate extensive clinical validation to build practitioner confidence.

- •Supply chain disruptions and raw material shortages may impact manufacturing and availability of laser atherectomy devices globally.

Regulatory Framework

- •Between 2019 and 2024, key regulatory bodies including the US FDA and European CE marking authorities updated guidelines mandating rigorous clinical evidence and post-market surveillance for laser atherectomy devices, enhancing safety standards and market trust.

- •New compliance requirements emphasize biocompatibility testing, electromagnetic compatibility, and sterilization protocols, impacting design and manufacturing processes.

- •Regulations now require detailed risk management documentation and traceability throughout the supply chain to ensure device integrity and patient safety.

- •Several countries have introduced expedited review pathways for innovative cardiovascular devices demonstrating significant clinical benefits, facilitating faster market entry.

- •Government initiatives promoting minimally invasive cardiovascular treatments have resulted in reimbursement policy adjustments, supporting wider adoption of laser atherectomy technologies.

Market Intelligence

- •15th January 2025, Boston Scientific Corporation announced the launch of its next-generation Excimer Laser Atherectomy system featuring enhanced catheter flexibility and real-time imaging integration, targeting improved treatment of complex peripheral artery disease lesions. This product aims to reduce procedural times and improve patient outcomes in minimally invasive cardiovascular interventions. The launch is expected to strengthen Boston Scientific's market leadership by addressing unmet clinical needs with innovative technology. Source: Official Boston Scientific Press Release

- •10th March 2025, Philips Healthcare unveiled a new hybrid laser atherectomy device combining excimer laser technology with angioplasty capabilities in a single platform, designed to optimize coronary artery disease treatment. This innovation supports clinicians with streamlined workflows and improved lesion clearance efficiency, potentially reducing restenosis rates. The device also incorporates digital health features for enhanced procedural monitoring. Source: Philips Healthcare Official Announcement

- •22nd June 2024, Cardiovascular Systems, Inc. completed the acquisition of a European laser catheter manufacturer to expand its product portfolio and enhance presence in the Asia-Pacific and European regions. This strategic move aims to accelerate innovation, broaden clinical indications, and strengthen distribution networks across key markets. The acquisition is aligned with the company’s growth strategy targeting emerging markets with rising cardiovascular disease prevalence. Source: Industry Publication on Medical Device M&A

- •5th September 2024, Medtronic plc announced a global partnership with a leading imaging technology firm to develop AI-powered laser atherectomy devices incorporating advanced diagnostic capabilities. This collaboration focuses on enhancing procedural precision and patient safety through integrated imaging and data analytics, anticipating regulatory approvals within the next two years. The partnership exemplifies the growing trend of combining AI with cardiovascular intervention technologies. Source: Medtronic Corporate Communications

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.45 Billion |

| Forecast Year Market Size | USD 3.56 Billion |

| CAGR | 9.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.5% |

| Scope of Report | Market is segmented by Product Type (Excimer Laser Atherectomy, Excimer Laser with Angioplasty, Excimer Laser with Stent, Other Laser Atherectomy Types), Application (Peripheral Artery Disease, Coronary Artery Disease, Carotid Artery Disease, Renal Artery Disease, Other Applications), End-Use Industry (Hospitals, Cardiovascular Clinics, Outpatient Surgical Centers, Specialized Vascular Centers), Distribution Channel (Direct Sales, Distributors, Online Medical Equipment Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Boston Scientific Corporation (United States), Philips Healthcare (Netherlands), Spectranetics Corporation (United States), Cardiovascular Systems, Inc. (United States), BIOTRONIK SE & Co. KG (Germany), Terumo Corporation (Japan), Siemens Healthineers AG (Germany), Abbott Laboratories (United States), Medtronic plc (Ireland), Asahi Intecc Co., Ltd. (Japan), Cook Medical (United States), C.R. Bard, Inc. (United States), Boston Scientific Corporation (United States), B. Braun Melsungen AG (Germany), Lumenis Ltd. (Israel), Edwards Lifesciences Corporation (United States), Canon Medical Systems Corporation (Japan), Vascular Solutions, Inc. (United States), Medico S.p.A. (Italy), Hoya Corporation (Japan), Terumo Medical Corporation (United States), AngioDynamics, Inc. (United States), Nipro Corporation (Japan), iVascular, S.L. (Spain), Biosensors International Group, Ltd. (Singapore) |

Global Laser Atherectomy Devices Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.