Global Cancer Imaging System Market Size, Growth & Revenue 2024-2034

Global Cancer Imaging System Market is segmented by Product Type (Magnetic Resonance Imaging (MRI) Systems, Computed Tomography (CT) Scanners, Positron Emission Tomography (PET) Scanners, Ultrasound Imaging Systems, X-ray Imaging Systems), Application (Breast Cancer Imaging, Lung Cancer Imaging, Prostate Cancer Imaging, Colorectal Cancer Imaging, Other Cancer Imaging Applications), End-Use Industry (Hospitals, Diagnostic Centers, Ambulatory Surgical Centers, Research & Academic Institutes), Distribution Channel (Direct Sales, Distributors, Online Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global cancer imaging system market represents a critical sector within medical diagnostics, focusing on technologies that enable precise detection, diagnosis, and management of cancerous conditions. This market includes imaging modalities such as MRI, CT, PET, ultrasound, and X-ray systems, each offering unique capabilities to visualize tumors and assess disease progression across a variety of cancer types including breast, lung, prostate, and colorectal cancers. The market scope covers hardware manufacturers, software developers, and service providers aiming to enhance imaging resolution, speed, and patient comfort. Key industry drivers include rising cancer prevalence, advancements in imaging technology, and growing awareness of early diagnosis benefits. The market is highly influenced by technological innovations such as artificial intelligence, hybrid imaging techniques, and improved contrast agents, which collectively contribute to more accurate and timely cancer detection. Additionally, stringent regulatory frameworks ensure device safety and clinical efficacy. Geographically, North America leads the market, benefiting from advanced healthcare infrastructure, while Asia-Pacific is emerging as the fastest-growing region due to increasing healthcare investments and expanding patient populations. Overall, the cancer imaging system market is positioned for robust growth, driven by continuous innovation and expanding clinical applications.

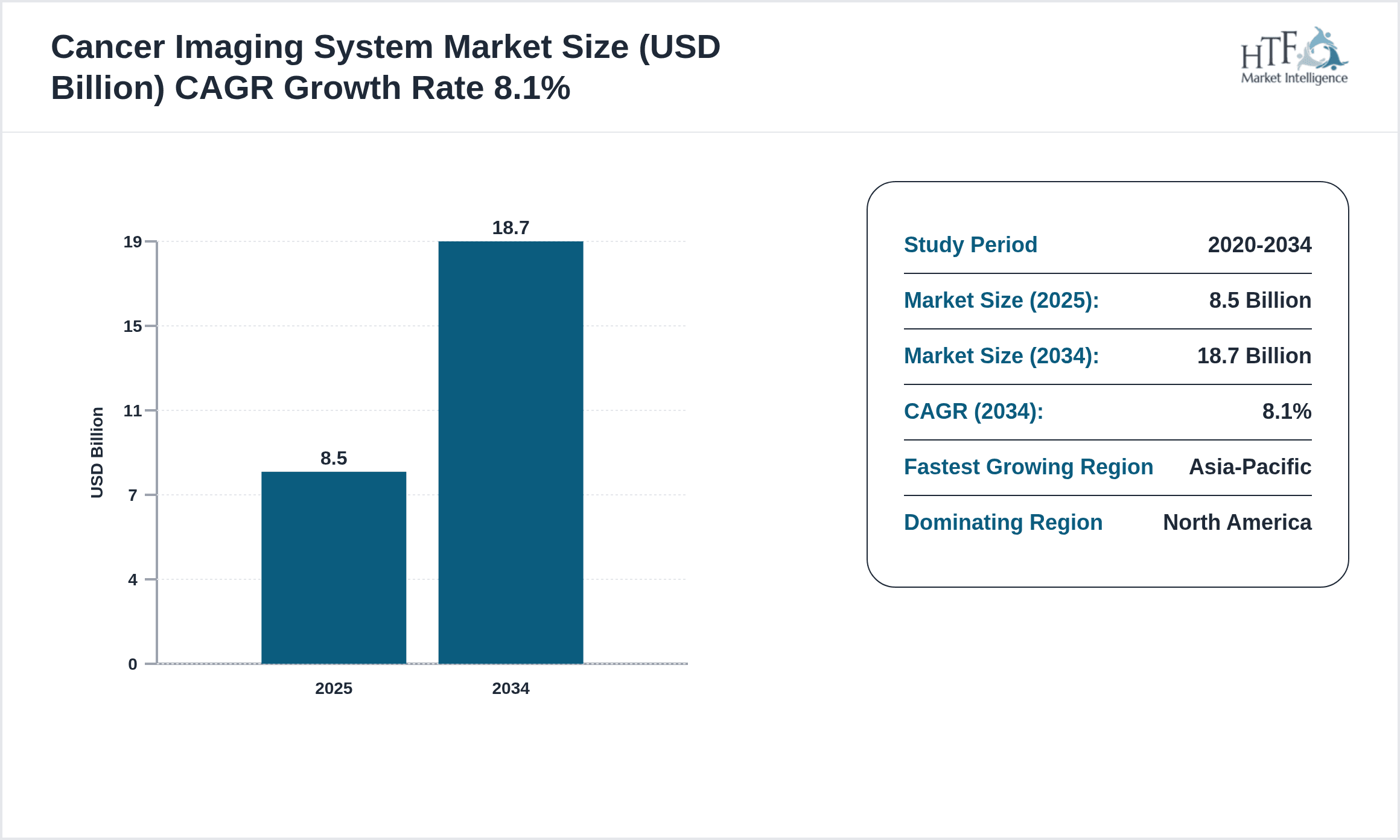

- •Key market highlights include a base market valuation of USD 8.5 billion in 2024, projected to reach USD 18.7 billion by 2034, reflecting a compound annual growth rate (CAGR) of 8.1%. MRI systems dominate the product segment due to their superior soft-tissue contrast and non-invasive nature, while PET scanners are witnessing the fastest growth owing to their functional imaging capabilities. Breast cancer imaging remains the leading application segment, followed closely by lung cancer imaging, driven by high incidence rates and screening programs globally. North America holds the largest market share, supported by advanced healthcare systems and high adoption rates, whereas Asia-Pacific offers significant growth potential due to rising cancer cases and improving healthcare infrastructure. Market growth is further bolstered by technological advancements, increasing healthcare expenditure, and expanding awareness about cancer diagnostics.

- •The cancer imaging system market offers substantial value propositions to healthcare providers, patients, and technology developers by enabling earlier and more accurate cancer detection, which translates to improved treatment outcomes and survival rates. For clinicians, these systems provide critical diagnostic information that guides personalized therapy decisions and monitoring. For manufacturers and investors, the market presents opportunities driven by innovation in imaging technologies, integration of artificial intelligence, and expansion into emerging regions. Additionally, the market supports broader oncology care initiatives by facilitating screening programs and research efforts. The strategic importance of this market spans hospitals, diagnostic centers, and research institutions, underscoring its role as a cornerstone of modern cancer management and precision medicine.

Competitive Landscape

The global cancer imaging system market is characterized by intense competition among multinational corporations, regional players, and innovative startups striving for technological leadership and market share. Companies compete on the basis of product innovation, imaging precision, software capabilities, and integrated solutions that enhance diagnostic workflows. Strategic partnerships, mergers, and acquisitions are common as firms aim to expand their product portfolios and geographic reach. Innovation approaches often focus on integrating artificial intelligence for improved image analysis, developing hybrid imaging modalities, and enhancing patient comfort. Market positioning is influenced by the ability to offer comprehensive cancer imaging solutions tailored to diverse clinical needs. Pricing strategies balance the high cost of advanced equipment with the value derived from improved diagnostic accuracy. Distribution channels encompass direct sales, distributors, and strategic collaborations with healthcare providers. Entrants face significant barriers due to regulatory requirements and the need for clinical validation. Future competition will increasingly revolve around digital transformation and personalized oncology imaging.

Key Players in Cancer Imaging System Market

- •Siemens Healthineers (Germany)

- •GE Healthcare (United States)

- •Philips Healthcare (Netherlands)

- •Canon Medical Systems Corporation (Japan)

- •Fujifilm Healthcare (Japan)

- •Hologic, Inc. (United States)

- •Samsung Medison Co., Ltd. (South Korea)

- •Hitachi Medical Corporation (Japan)

- •Shimadzu Corporation (Japan)

- •Carestream Health (United States)

- •Esaote S.p.A. (Italy)

- •Analogic Corporation (United States)

- •United Imaging Healthcare Co., Ltd. (China)

- •Planmed Oy (Finland)

- •Koninklijke Philips N.V. (Netherlands)

- •Neusoft Corporation (China)

- •PerkinElmer, Inc. (United States)

- •Elekta AB (Sweden)

- •Bracco Imaging S.p.A. (Italy)

- •Mediso Medical Imaging Systems (Hungary)

- •Carestream Health, Inc. (United States)

- •Hitachi, Ltd. (Japan)

- •Analogic Corporation (United States)

- •Shimadzu Corporation (Japan)

- •Samsung Electronics Co., Ltd. (South Korea)

Market Breakdown

- •By Product Type

- ◦Magnetic Resonance Imaging (MRI) Systems

- ◦Computed Tomography (CT) Scanners

- ◦Positron Emission Tomography (PET) Scanners

- ◦Ultrasound Imaging Systems

- ◦X-ray Imaging Systems

- •By Application

- ◦Breast Cancer Imaging

- ◦Lung Cancer Imaging

- ◦Prostate Cancer Imaging

- ◦Colorectal Cancer Imaging

- ◦Other Cancer Imaging Applications

- •By End-Use Industry

- ◦Hospitals

- ◦Diagnostic Centers

- ◦Ambulatory Surgical Centers

- ◦Research & Academic Institutes

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Sales

Growth Dynamics

The global cancer imaging system market growth is primarily driven by the increasing prevalence of cancer worldwide, which necessitates advanced diagnostic tools for early detection and treatment monitoring. Technological advancements such as AI-powered imaging analysis, hybrid imaging modalities combining anatomical and functional data, and improvements in imaging resolution are propelling market expansion. Additionally, rising healthcare expenditure and growing awareness about cancer screening programs contribute significantly. The adoption of minimally invasive diagnostic procedures supported by enhanced imaging techniques is improving patient outcomes and driving demand. Furthermore, strategic collaborations between technology providers and healthcare institutions facilitate the development of customized imaging solutions, stimulating market growth. Emerging economies are witnessing increased investments in healthcare infrastructure, thereby expanding the market footprint. Regulatory support for innovative imaging devices and reimbursement policies further underpin market dynamics, making cancer imaging systems an indispensable component of modern oncology care.

Market Trends

Recent years have seen a pronounced trend towards integration of artificial intelligence and machine learning in cancer imaging systems, enhancing diagnostic accuracy through automated lesion detection and characterization. Hybrid imaging systems combining PET and CT or MRI are gaining traction due to their ability to provide complementary anatomical and metabolic information, facilitating comprehensive cancer assessment. Additionally, there is a shift towards portable and compact imaging devices that improve accessibility in remote and resource-limited settings. Market players are focusing on software enhancements to enable real-time image processing and cloud-based data sharing to support telemedicine initiatives. Moreover, sustainability trends are influencing product design, with manufacturers aiming to reduce radiation exposure and improve energy efficiency. Patient-centric innovations such as reduced scan times and improved comfort features are also becoming standard, aligning with evolving healthcare delivery models. The convergence of imaging and therapeutic technologies is expected to shape future developments, fostering personalized oncology treatment.

Market Opportunities

Significant opportunities exist in emerging markets, especially Asia-Pacific and Latin America, where rising cancer incidence and expanding healthcare infrastructure are creating unmet demand for advanced imaging systems. The increasing adoption of AI and machine learning technologies offers potential for developing intelligent diagnostic platforms that can streamline workflows and improve detection rates. Additionally, advancements in molecular imaging and targeted contrast agents present avenues for more precise tumor visualization and treatment monitoring. Collaborations between technology companies and pharmaceutical firms for companion diagnostics represent another growth area. Furthermore, expanding applications of cancer imaging beyond traditional tumor sites, including rare cancers and pediatric oncology, provide avenues for market penetration. Government initiatives and favorable reimbursement policies supporting cancer screening and early diagnosis further enhance market attractiveness. Investment in portable imaging devices designed for low-resource settings can tap into underserved populations, broadening market reach and improving global cancer care.

Market Challenges

The cancer imaging system market faces several challenges including high equipment costs, which limit adoption in developing regions and smaller healthcare facilities. Complex regulatory approval processes and stringent compliance requirements can delay product launches and increase development expenses. Additionally, the need for specialized operator training and maintenance support can pose barriers to widespread implementation. Technical limitations such as image artifacts, radiation exposure concerns, and variability in diagnostic accuracy across modalities require ongoing innovation and validation. Market competition is intense, driving pricing pressures that can impact profitability for manufacturers. Data privacy and cybersecurity concerns related to AI-driven image analysis and cloud-based solutions also present risks. Furthermore, reimbursement uncertainties and inconsistent healthcare policies across regions may restrict market growth. Addressing these challenges requires strategic investments in R&D, robust training programs, and collaborations with regulatory bodies to facilitate smoother market entry and adoption.

Regulatory Framework

Between 2020 and 2024, regulatory authorities worldwide have introduced updated guidelines to enhance the safety and efficacy of cancer imaging systems. The U.S. FDA implemented more rigorous premarket approval requirements focusing on clinical validation and software reliability, particularly for AI-enabled imaging devices. The European Union’s Medical Device Regulation (MDR) enforced stricter conformity assessments and post-market surveillance mandates, impacting manufacturers' compliance strategies. In Asia-Pacific, regulatory bodies have accelerated approval processes for innovative diagnostic technologies to address growing cancer burdens. Additionally, international standards such as ISO 13485 and IEC 62304 have been increasingly adopted to standardize quality management and software lifecycle processes. These regulatory developments aim to ensure patient safety, improve diagnostic accuracy, and support innovation by providing clear pathways for device approvals. They also encourage manufacturers to invest in robust clinical trials and cybersecurity measures, thereby fostering trust among healthcare providers and patients.

Market Intelligence

- •15th February 2024, Siemens Healthineers announced the launch of its next-generation MRI system tailored for oncology diagnostics, featuring enhanced AI-driven image reconstruction and reduced scan times. This system aims to improve early cancer detection accuracy while increasing patient throughput in clinical settings. The product integrates seamlessly with hospital information systems, enabling streamlined workflows and real-time data analytics. Siemens aims to leverage this launch to strengthen its position in the global cancer imaging market, particularly within North America and Europe. Source: Siemens Healthineers Official Press Release

- •10th November 2023, GE Healthcare introduced an advanced PET/CT scanner equipped with cutting-edge digital detectors and AI-based image enhancement algorithms. This innovation provides superior lesion detectability and quantitative accuracy, facilitating better treatment planning and response assessment in oncology. The scanner also includes patient comfort features such as noise reduction and faster scan protocols, catering to diverse clinical needs. GE Healthcare plans to expand its distribution network across Asia-Pacific to capitalize on the region's growing demand for cancer imaging technologies. Source: GE Healthcare Newsroom

- •20th August 2024, Philips Healthcare announced a strategic partnership with a leading AI software developer to co-create integrated cancer imaging solutions combining hardware and intelligent diagnostics. The collaboration focuses on developing cloud-based platforms for remote image analysis and decision support, aiming to improve accessibility and efficiency in cancer care globally. This initiative aligns with Philips’ vision to drive digital transformation in medical imaging and expand its footprint in emerging markets. Source: Philips Corporate Announcement

- •5th May 2023, Canon Medical Systems Corporation completed the acquisition of a specialized medical imaging software company to enhance its portfolio of cancer imaging solutions. The acquisition is expected to accelerate innovation in AI-powered diagnostics and provide comprehensive imaging analytics capabilities. Canon aims to integrate these technologies into its CT and MRI systems to offer personalized cancer detection and monitoring services. This move strengthens Canon’s competitive edge and supports its global expansion strategy, especially in Asia-Pacific and Europe. Source: Canon Medical Systems Press Release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.5 Billion |

| Forecast Year Market Size | USD 18.7 Billion |

| CAGR | 8.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.8% |

| Scope of Report | Market is segmented by Product Type (Magnetic Resonance Imaging (MRI) Systems, Computed Tomography (CT) Scanners, Positron Emission Tomography (PET) Scanners, Ultrasound Imaging Systems, X-ray Imaging Systems), Application (Breast Cancer Imaging, Lung Cancer Imaging, Prostate Cancer Imaging, Colorectal Cancer Imaging, Other Cancer Imaging Applications), End-Use Industry (Hospitals, Diagnostic Centers, Ambulatory Surgical Centers, Research & Academic Institutes), Distribution Channel (Direct Sales, Distributors, Online Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Siemens Healthineers (Germany), GE Healthcare (United States), Philips Healthcare (Netherlands), Canon Medical Systems Corporation (Japan), Fujifilm Healthcare (Japan), Hologic, Inc. (United States), Samsung Medison Co., Ltd. (South Korea), Hitachi Medical Corporation (Japan), Shimadzu Corporation (Japan), Carestream Health (United States), Esaote S.p.A. (Italy), Analogic Corporation (United States), United Imaging Healthcare Co., Ltd. (China), Planmed Oy (Finland), Koninklijke Philips N.V. (Netherlands), Neusoft Corporation (China), PerkinElmer, Inc. (United States), Elekta AB (Sweden), Bracco Imaging S.p.A. (Italy), Mediso Medical Imaging Systems (Hungary), Carestream Health, Inc. (United States), Hitachi, Ltd. (Japan), Analogic Corporation (United States), Shimadzu Corporation (Japan), Samsung Electronics Co., Ltd. (South Korea) |

Global Cancer Imaging System Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.