GPS & GNSS Receivers Market - Global Size & Outlook 2020-2033

Global GPS & GNSS Receivers Market is segmented by Application (Mapping & Surveying, Fleet Management, Timing & Synchronization, Consumer Devices, Defense), Type (Handheld, Embedded, Survey-Grade, Timing, Automotive), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

INDUSTRY OVERVIEW

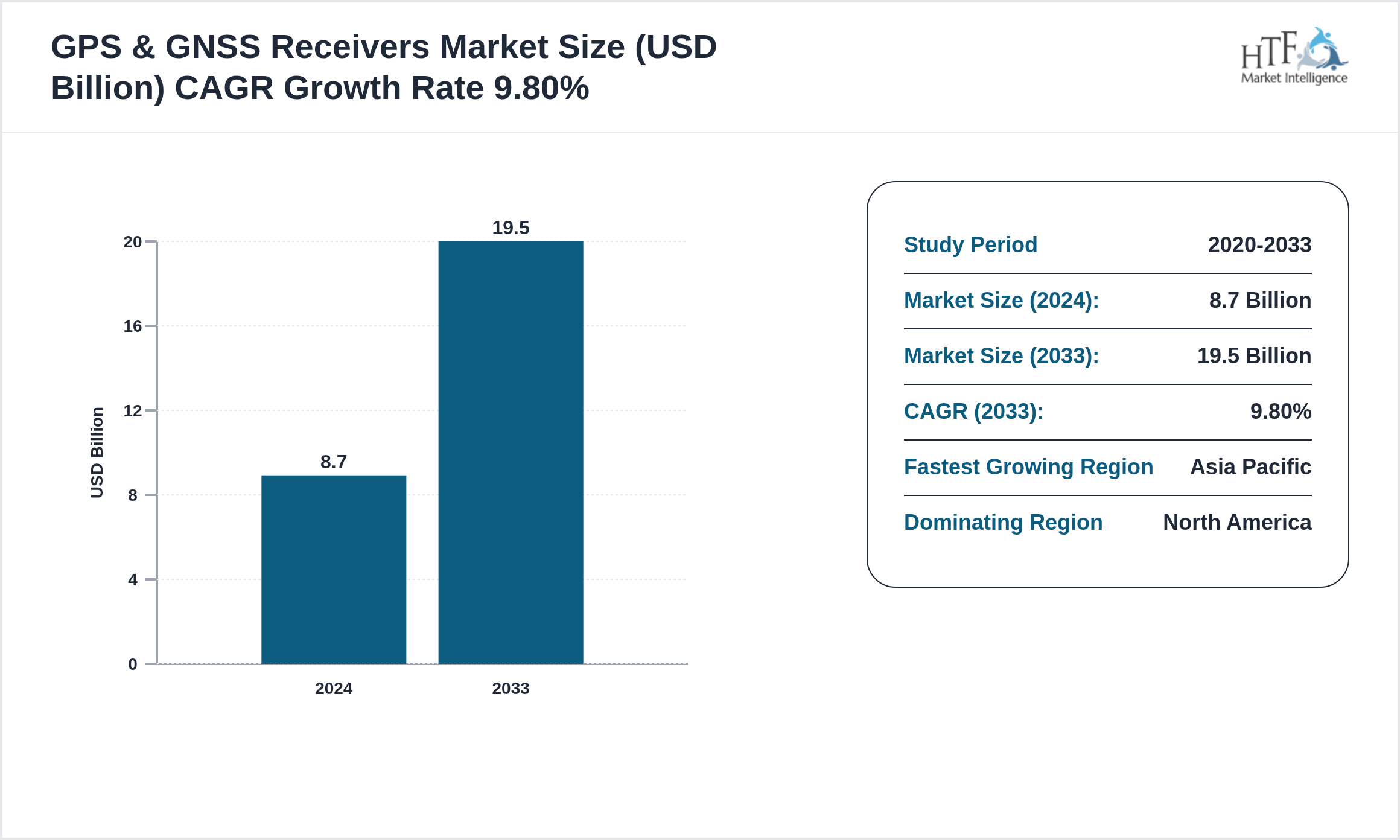

The GPS & GNSS Receivers market is experiencing robust growth, projected to achieve a compound annual growth rate CAGR of 9.80% during the forecast period. Valued at 8.70 billion, the market is expected to reach 19.50 billion by 2033, with a year-on-year growth rate of 5.90%. This upward trajectory is driven by factors such as evolving consumer preferences, technological advancements, and increased investment in innovation, positioning the market for significant expansion in the coming years. Companies should strategically focus on enhancing their offerings and exploring new market opportunities to capitalize on this growth potential.

Source: HTF Market Intelligence (HTF MI)

GPS & GNSS receivers decode signals from multi-constellation satellites—GPS, GLONASS, Galileo, BeiDou—to calculate precise geospatial coordinates for navigation, surveying, and timing. Front-end RF ASICs capture L1/L5 dual-frequency bands, pass them through SAW filters, and digitise them into baseband correlation engines that acquire pseudorandom codes. Multi-band reception mitigates ionospheric error, while real-time kinematic (RTK) or PPP corrections attain centimetre-level accuracy. MEMS inertial sensors fuse dead reckoning for urban-canyon continuity, and anti-jamming algorithms reject spoofing using angle-of-arrival and encrypted P(Y) codes. Low-power modes serve IoT trackers, whereas 10 Hz update rates empower autonomous-vehicle path planning. Timing receivers discipline network clocks to <10 ns, essential for 5G and financial exchanges. Open-source APIs and NMEA messages integrate GNSS data into countless consumer, industrial, and defence applications worldwide.

Geographic Analysis of GPS & GNSS Receivers

The GPS & GNSS Receivers market exhibits significant regional variation, shaped by different economic conditions and consumer behaviors.

Currently, North America dominates the market due to high consumption, population growth, and sustained economic progress. Meanwhile, Asia Pacific is experiencing the fastest growth, driven by large-scale infrastructure investments, industrial development, and rising consumer demand.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

Regulatory Landscape

- • Regulated under ITU FCC and CE certification for spectrum compliance. ISO 17123 standards govern positioning accuracy.

Key Highlights

• The GPS & GNSS Receivers is growing at a CAGR of 9.80% during the forecasted period of 2020 to 2033

• Year-on-year growth for the market is 5.90%.

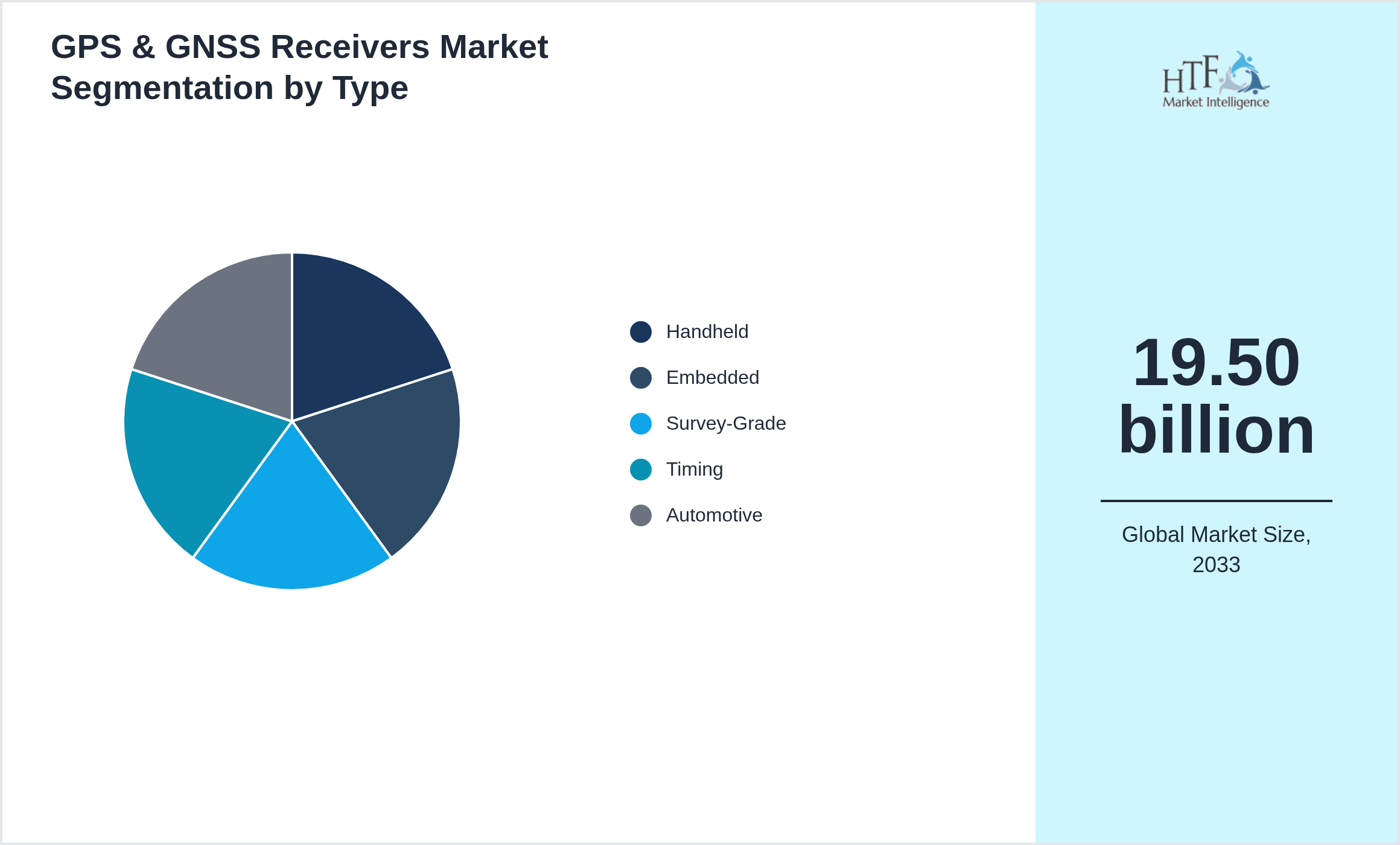

• Based on type, the market is bifurcated into Handheld, Embedded, Survey-Grade, Timing, Automotive

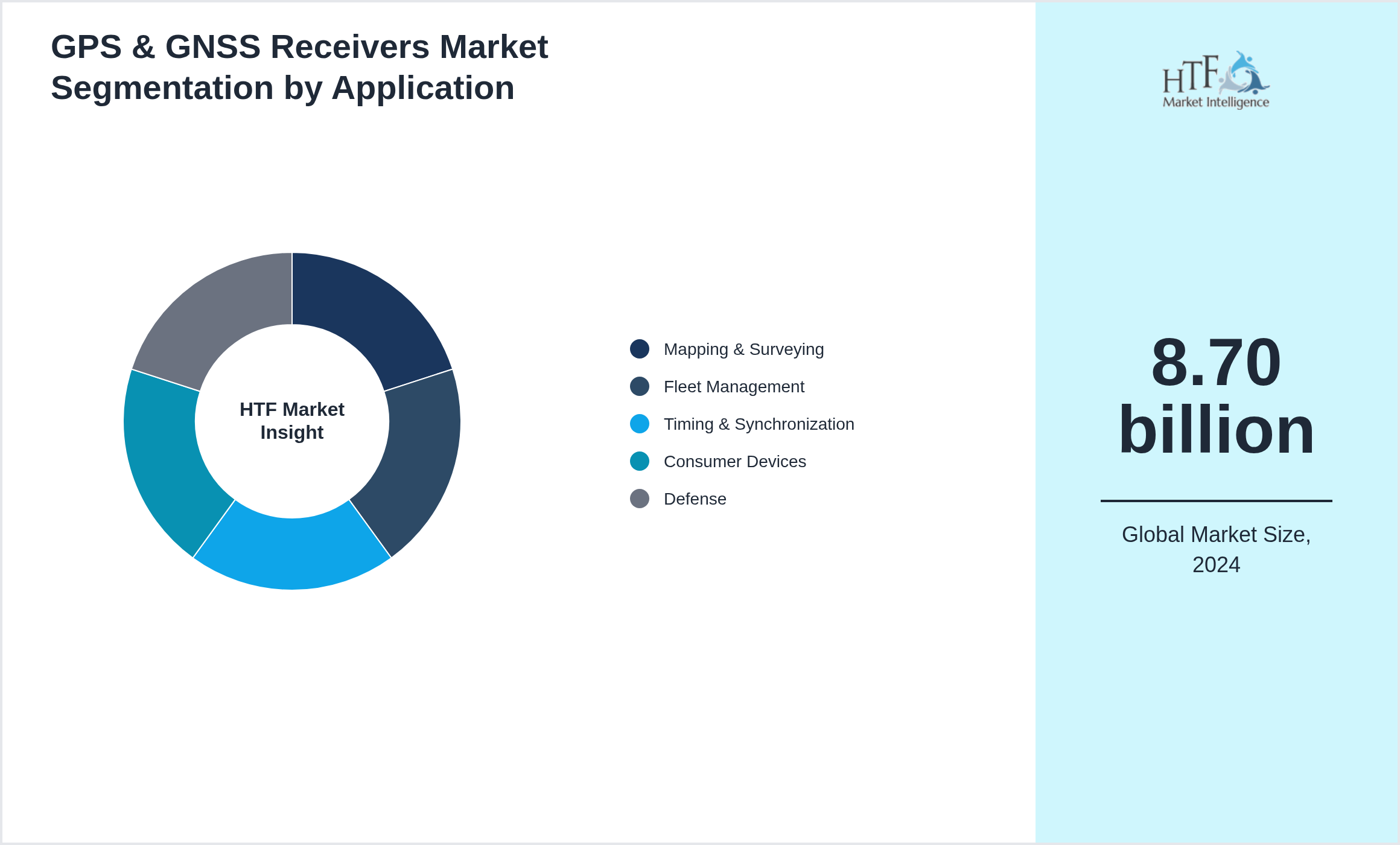

• Based on application, the market is segmented into Mapping & Surveying, Fleet Management, Timing & Synchronization, Consumer Devices, Defense

• Global import/export in terms of K tons, K units, and metric tons will be provided if applicable, based on industry best practices.

Market Segmentation Analysis

Segmentation by Type

- • Handheld

- • Embedded

- • Survey-Grade

- • Timing

- • Automotive

Segmentation by Application

- • Mapping & Surveying

- • Fleet Management

- • Timing & Synchronization

- • Consumer Devices

- • Defense

Key Players

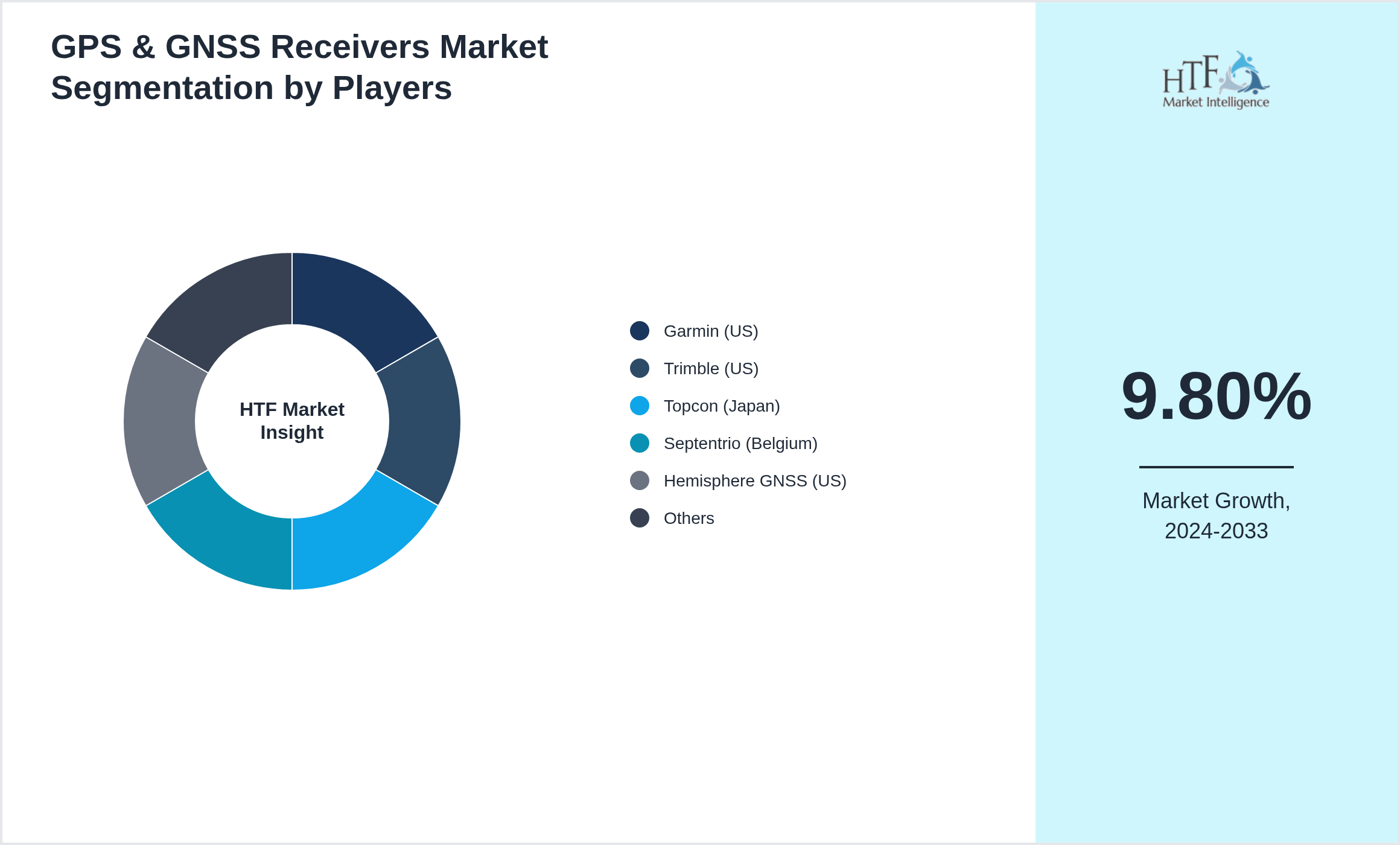

Several key players in the GPS & GNSS Receivers market are strategically focusing on expanding their operations in developing regions to capture a larger market share, particularly as the year-on-year growth rate for the market stands at 5.90%. The companies featured in this profile were selected based on insights from primary experts, evaluating their market penetration, product offerings, and geographical reach. By targeting emerging markets, these companies aim to leverage new opportunities, enhance their competitive advantage, and drive revenue growth. This approach not only aligns with their overall business objectives but also positions them to respond effectively to the evolving demands of consumers in these regions.

- • Garmin (US)

- • Trimble (US)

- • Topcon (Japan)

- • Septentrio (Belgium)

- • Hemisphere GNSS (US)

- • u-blox (Switzerland)

- • Leica Geosystems (Switzerland)

- • NovAtel (Canada)

- • Furuno (Japan)

- • Navcom (US)

- • STMicroelectronics (Switzerland)

- • Broadcom (US)

- • Qualcomm (US)

- • Broadpeak (France)

- • Telit (UK)

- • Telstra (Australia)

- • Sierra Wireless (Canada)

- • Quectel (China)

- • ZTE (China)

- • Huawei (China)

- • Ericsson (Sweden)

- • Nokia (Finland)

- • Cisco (US)

- • Dell (US)

- • Intel (US)

Research Methodology

The comprehensive market research is provided that combines both secondary and primary methodologies. The secondary research involves rigorous analysis of existing data sources, such as industry reports, market databases, and competitive landscapes, to provide a robust foundation of market knowledge. This is complemented by our primary research services to gather firsthand data through surveys, interviews, and focus groups tailored specifically to your business needs. By integrating these approaches, we offer a thorough understanding of market trends, consumer behavior, and competitive dynamics, enabling us to make well-informed strategic decisions.

Market Dynamics

Market dynamics refer to the forces that influence the supply and demand of products and services within a market. These forces include factors such as consumer preferences, technological advancements, regulatory changes, economic conditions, and competitive actions. Understanding market dynamics is crucial for businesses as it helps them anticipate changes, identify opportunities, and mitigate risks.

By analyzing market dynamics, companies can better understand market trends, predict potential shifts, and develop strategic responses. This analysis enables businesses to align their product offerings, pricing strategies, and marketing efforts with evolving market conditions, ultimately leading to more informed decision-making and a stronger competitive position in the marketplace.

Market Driver

- • Embedded system proliferation

- • IoT device expansion

- • Cost-effective computing demand

- • Consumer electronics growth

- • Automation across industries

- • System-on-chip integration

- • Low-power architectures

- • Edge computing adoption

- • AI-enabled microcontrollers

- • Advanced fabrication nodes

- • Smart appliances growth

- • Industrial IoT expansion

- • Automotive electronics demand

- • Education and maker ecosystems

- • Medical device integration

Challenge

- • Semiconductor supply risks

- • Design complexity

- • Firmware security threats

- • Rapid obsolescence

- • Price pressure

Regional Analysis

- • North America and Europe dominate technology development. AsiaPacific led by China’s BeiDou and India’s NavIC expands localization.

Market Entropy

- • Dec 2025: Navigation OEMs rolled out multiband GPS/GNSS receivers with centimeterlevel accuracy for autonomous mobile robots.

Merger & Acquisition

- • Apr 2025 – GeoSignal Systems acquired NavStar Receivers merging L1/L5 chipsets AI multipath rejection and loworbit correction services; new rugged modules cut centimeterlevel RTK costs 35 % targeting robotics precision ag and autonomous shipping lanes.

Regulatory Landscape

- • Regulated under ITU FCC and CE certification for spectrum compliance. ISO 17123 standards govern positioning accuracy.

Patent Analysis

- • Patents center on multiconstellation processing antijamming systems and AIbased signal prediction.

Investment and Funding Scenario

- • Heavy investments from defense automotive and logistics industries.

Regional Outlook

The North America region holds the largest market share in 2024 and is expected to grow at a good CAGR. The Asia Pacific Region is the fastest-growing region due to increasing development and disposable income.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

|

Report Features |

Details |

|

Base Year |

2024 |

|

Based Year Market Size (2024) |

8.70 billion |

|

Historical Period Market Size (2020) |

USD Million ZZ |

|

CAGR (2024 to 2033) |

9.80% |

|

Forecast Period |

2026 to 2033 |

|

Forecasted Period Market Size (2033) |

19.50 billion |

|

Scope of the Report |

By Type, By Application, By Region |

|

Quantitative Units |

Revenue in USD million/billion, volume in kilotons, and CAGR from 2024 to 2033 |

|

Year-on-Year Growth |

5.90% |

|

Companies Covered |

Garmin (US), Trimble (US), Topcon (Japan), Septentrio (Belgium), Hemisphere GNSS (US), u-blox (Switzerland), Leica Geosystems (Switzerland), NovAtel (Canada), Furuno (Japan), Navcom (US), STMicroelectronics (Switzerland), Broadcom (US), Qualcomm (US), Broadpeak (France), Telit (UK), Telstra (Australia), Sierra Wireless (Canada), Quectel (China), ZTE (China), Huawei (China), Ericsson (Sweden), Nokia (Finland), Cisco (US), Dell (US), Intel (US) |

|

Customization Scope |

15% Free Customization (For EG) |

|

Delivery Format |

PDF and Excel through Email

|

Regulatory Framework

The Information and Communications Technology (ICT) industry is primarily regulated by the Federal Communications Commission (FCC) in the United States, along with other national and international regulatory bodies. The FCC oversees the allocation of spectrum, ensures compliance with telecommunications laws, and fosters fair competition within the sector. It also establishes guidelines for data privacy, cybersecurity, and service accessibility, which are crucial for maintaining industry standards and protecting consumer interests.

Globally, various regulatory agencies, such as the European Telecommunications Standards Institute (ETSI) and the International Telecommunication Union (ITU), play significant roles in standardizing practices and facilitating international cooperation. These bodies work together to create a cohesive regulatory framework that addresses emerging technologies, cross-border data flow, and infrastructure development. Their regulations aim to ensure the ICT industry's growth is both innovative and compliant with global standards, promoting a secure and competitive market environment.