Global Lignosulfonate Market Size, Growth & Revenue 2024-2034

Global Lignosulfonate Market is segmented by Product Type (Calcium Lignosulfonate, Sodium Lignosulfonate, Magnesium Lignosulfonate, Ammonium Lignosulfonate, Others), Application (Concrete Admixtures, Animal Feed, Dust Control, Oil Drilling, Others), End-Use Industry (Construction, Agriculture, Oil & Gas, Animal Nutrition), Distribution Channel (Direct Sales, Distributors, Online Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Lignosulfonate market includes the manufacturing and application of lignosulfonates, derived primarily from the sulfite pulping process of lignin. These water-soluble polymers are extensively used as binding agents, dispersants, and complexing agents across industries such as construction, agriculture, oil drilling, and dust control. The market covers product types such as calcium, sodium, magnesium, and ammonium lignosulfonates, each catering to specific industrial needs. Growing environmental concerns and the push for sustainable industrial additives have expanded the market scope, with lignosulfonates serving as eco-friendly alternatives to synthetic chemicals. The market's boundaries extend globally, with significant activity in North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Key applications include concrete admixtures, animal feed, dust control, and oil drilling, reflecting diverse end-use industries. The market is characterized by innovation in product formulations and increasing penetration in emerging economies, highlighting its strategic importance in enhancing product performance and sustainability worldwide.

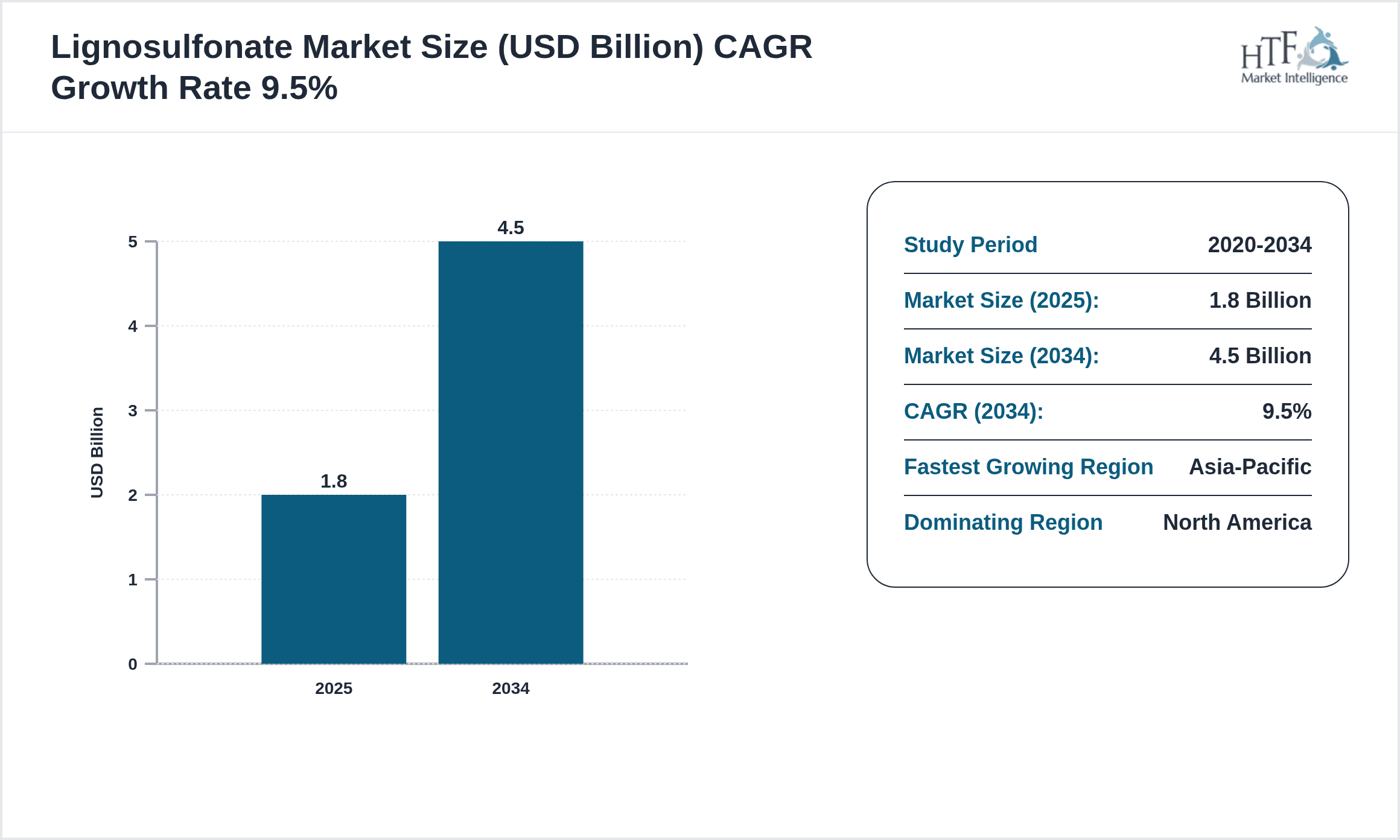

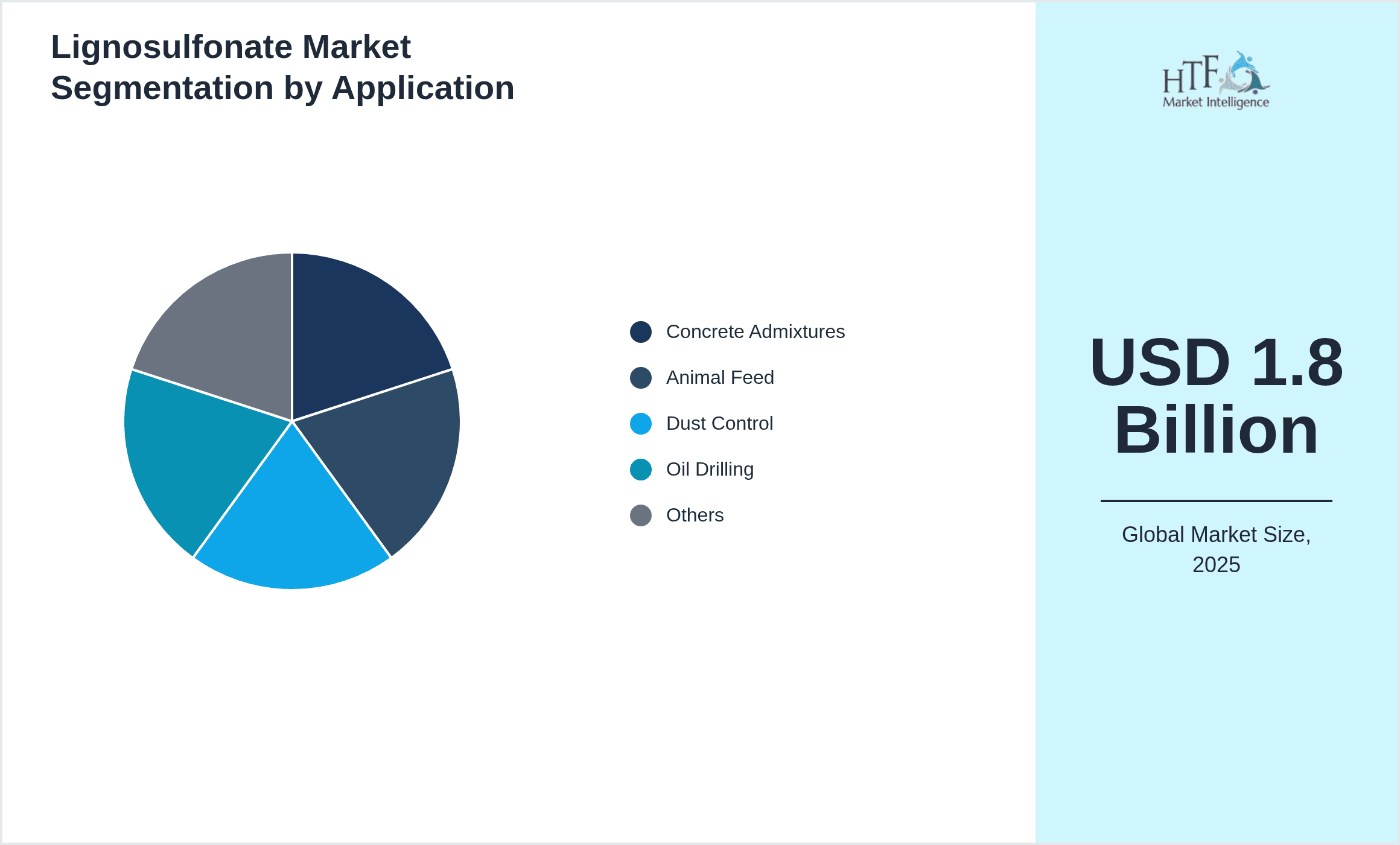

- •Key market highlights include a base market size of USD 1.8 billion in 2024, projected to reach USD 4.5 billion by 2034, representing a CAGR of 9.5%. The Asia-Pacific region is the fastest-growing market segment driven by infrastructure development and expanding agricultural activities. Calcium lignosulfonate dominates the product type segment due to its extensive use in concrete admixtures and animal feed, while sodium lignosulfonate exhibits the highest growth rate. Concrete admixtures remain the leading application, followed by animal feed, reflecting the importance of lignosulfonates in construction and agriculture. North America holds the dominant regional market share, supported by advanced industrial capabilities and stringent environmental regulations favoring bio-based additives.

- •The value proposition of the lignosulfonate market lies in its multifunctional applications that improve product efficiency and environmental profiles. For industries such as construction and agriculture, lignosulfonates offer cost-effective, sustainable solutions that enhance product quality and reduce ecological footprints. Stakeholders including manufacturers, end-users, and regulatory bodies benefit from innovations that align with global sustainability goals. The strategic importance of this market is underscored by its potential to replace synthetic additives, promote circular economy principles, and support growing demands in emerging markets, thereby driving long-term growth and competitive advantage.

Competitive Landscape

The competitive landscape of the global lignosulfonate market is marked by intense rivalry among multinational chemical manufacturers and regional producers seeking market share through innovation, product differentiation, and strategic partnerships. Leading companies focus on developing advanced lignosulfonate formulations with enhanced performance characteristics tailored to specific applications such as concrete admixtures and animal nutrition. Market players adopt competitive strategies including capacity expansions, acquisitions, and collaborations to strengthen their global footprint and meet regional demand variations. Innovation in eco-friendly and bio-based lignosulfonates is a key differentiator, addressing rising environmental regulations and consumer preferences. Pricing strategies are influenced by raw material availability and production costs, with companies striving to balance affordability with quality. Distribution channels are diversified, encompassing direct sales, distributors, and e-commerce platforms to optimize market penetration. The market entry barriers include high capital requirements and regulatory compliance, which protect incumbents while encouraging technological advancements. Regional competition varies, with Asia-Pacific witnessing rapid market entry by new players, while North America and Europe emphasize product innovation and regulatory adherence.

Leading Companies in Lignosulfonate Market

- •Borregaard ASA (Norway)

- •Domsjö Fabriker AB (Sweden)

- •Tembec Inc. (Canada)

- •West Fraser Timber Co. Ltd. (Canada)

- •Sappi Limited (South Africa)

- •UPM-Kymmene Corporation (Finland)

- •Kraft Lignin Ltd. (Canada)

- •LignoTech USA LLC (United States)

- •Hansol PNS Co., Ltd. (South Korea)

- •Norbord Inc. (Canada)

- •Jiangsu Xinda Lignin Co., Ltd. (China)

- •Metsä Group (Finland)

- •GreenValue S.A. (Poland)

- •GranBio (Brazil)

- •Shandong Longlive Bio-Technology Co., Ltd. (China)

- •Westinghouse Electric Company LLC (United States)

- •Aditya Birla Group (India)

- •Tianjin Bohui Paper Co., Ltd. (China)

- •UPM Biochemicals (Finland)

- •Resolute Forest Products (Canada)

- •International Paper Company (United States)

- •Suzano Papel e Celulose S.A. (Brazil)

- •Domtar Corporation (United States)

- •Södra Cell (Sweden)

- •Fibria Celulose S.A. (Brazil)

Market Breakdown

- •By Product Type

- ◦Calcium Lignosulfonate

- ◦Sodium Lignosulfonate

- ◦Magnesium Lignosulfonate

- ◦Ammonium Lignosulfonate

- ◦Others

- •By Application

- ◦Concrete Admixtures

- ◦Animal Feed

- ◦Dust Control

- ◦Oil Drilling

- ◦Others

- •By End-Use Industry

- ◦Construction

- ◦Agriculture

- ◦Oil & Gas

- ◦Animal Nutrition

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Sales

Growth Dynamics

- •Increasing demand for eco-friendly and sustainable additives in construction and agriculture sectors is driving the global lignosulfonate market. Lignosulfonates serve as biodegradable dispersants and binders, facilitating greener industrial processes and aligning with global environmental regulations.

- •Rising infrastructure development globally, especially in emerging economies, boosts the need for concrete admixtures, a primary application for calcium lignosulfonate. This trend is supported by urbanization and government investments in smart city projects.

- •The animal nutrition segment benefits from lignosulfonates as pellet binders and feed additives that improve digestibility and nutrient absorption, thereby enhancing livestock productivity and reducing feed wastage.

- •Technological advancements in lignosulfonate extraction and purification have improved product quality and application versatility, enabling manufacturers to tailor products for specific industry needs and increase adoption rates.

- •Expanding oil and gas drilling activities globally increase the use of lignosulfonates as dispersants and drilling mud additives, driven by growing energy demands and exploration in offshore and unconventional reserves.

Market Trends

- •Adoption of green chemistry principles is prompting manufacturers to innovate bio-based lignosulfonates with enhanced biodegradability and reduced environmental impact, gaining traction in Europe and North America.

- •Integration of lignosulfonates with nanomaterials and polymers is emerging, enhancing performance characteristics such as water retention, binding strength, and dispersibility in construction and agriculture applications.

- •Collaborative R&D efforts between chemical companies and academic institutions are accelerating product innovation and diversification, enabling lignosulfonates to enter new application domains like water treatment and pharmaceuticals.

- •Increasing digitalization in supply chain management and sales channels is optimizing distribution efficiency, expanding market reach, and enabling real-time customer engagement in the lignosulfonate sector.

- •Sustainability certifications and eco-labeling are becoming significant market differentiators, influencing purchasing decisions and regulatory approvals for lignosulfonate-based products globally.

Market Opportunities

- •Emerging markets in Asia-Pacific and Latin America present substantial growth opportunities due to increasing construction activities and rising demand for sustainable agricultural inputs.

- •Development of customized lignosulfonate formulations for specialized applications such as water treatment and pharmaceuticals offers avenues for market expansion and higher profit margins.

- •Strategic partnerships and joint ventures among chemical manufacturers and technology firms can accelerate product innovation and penetration into untapped markets.

- •Increasing regulatory emphasis on reducing synthetic chemical usage opens opportunities for lignosulfonates to replace conventional additives in various industrial processes.

- •Investment in sustainable supply chains and circular economy initiatives can enhance raw material availability and reduce production costs, boosting competitive advantage.

Market Challenges

- •Fluctuations in raw material availability and prices, primarily sourced from the pulp and paper industry, pose supply chain risks impacting production costs and market stability.

- •Stringent regulatory compliance related to environmental safety and chemical usage increases operational complexities and costs for lignosulfonate manufacturers.

- •Competition from alternative synthetic dispersants and binders with established market presence limits the penetration of lignosulfonates in some applications.

- •Technical challenges in consistent quality and performance of lignosulfonate products across varied industrial applications require continuous R&D investment.

- •Limited consumer awareness about the benefits of lignosulfonates in certain regions restricts market growth potential and adoption rates.

Regulatory Framework

- •Between 2019 and 2024, multiple environmental regulations were enacted globally mandating reduction in synthetic chemical additives in industrial processes, promoting the use of bio-based alternatives like lignosulfonates. Compliance with REACH in Europe and TSCA in the United States requires manufacturers to ensure product safety and environmental impact assessments.

- •Enforcement of stricter wastewater discharge standards in North America and Europe has increased demand for lignosulfonates in water treatment applications due to their biodegradability and lower toxicity.

- •Safety standards related to animal feed additives have been updated in Asia-Pacific countries, requiring rigorous testing and certification for lignosulfonate-based products to ensure livestock health and food safety.

- •Country-specific mandates in Latin America and Middle East & Africa focus on sustainable sourcing and reduction of carbon emissions in chemical production, influencing lignosulfonate manufacturing practices and supply chain management.

- •Government incentive programs and subsidies for green chemicals in regions such as Europe and North America support R&D and commercialization of sustainable lignosulfonate products, fostering innovation and market expansion.

Market Intelligence

- •15th February 2025, Borregaard ASA launched an innovative sodium lignosulfonate product line designed for enhanced dispersing efficiency in concrete admixtures. The new formulation offers improved water retention and reduced environmental impact, targeting construction companies in Asia-Pacific and Europe. This launch reinforces Borregaard's commitment to sustainability and product innovation, aiming to capture growing demand in emerging markets with stringent green building standards. The product's compatibility with various cement types and its cost-effectiveness position it as a competitive solution for global infrastructure projects. Source: Official Borregaard Press Release

- •10th May 2025, Domsjö Fabriker AB introduced a bio-based calcium lignosulfonate variant optimized for animal feed applications. The product demonstrates superior pellet binding properties and enhanced digestibility, addressing increasing livestock nutrition requirements in North America and Europe. The launch is part of the company’s strategic focus on expanding its agricultural portfolio while aligning with environmental sustainability goals. The innovation is expected to reduce feed wastage and improve animal health outcomes, strengthening Domsjö Fabriker’s position in the global feed additives market. Source: Domsjö Fabriker Official Website

- •22nd March 2025, West Fraser Timber Co. Ltd. announced a strategic partnership with a leading chemical manufacturer to co-develop advanced lignosulfonate products for oil drilling applications. The collaboration aims to enhance drilling fluid performance and environmental compliance in shale and offshore drilling projects globally. This initiative leverages West Fraser's raw material expertise and the partner’s chemical formulation capabilities to address evolving industry challenges. The partnership is expected to accelerate product development cycles and expand market reach in North America and Asia-Pacific regions. Source: Industry Publication

- •5th January 2025, Sappi Limited completed the expansion of its lignosulfonate production facility in South Africa, increasing capacity by 30%. The expansion supports growing demand from construction and agriculture sectors in Africa and Europe. Enhanced production capabilities enable Sappi to offer a wider product range with improved quality and delivery timelines. The investment aligns with the company’s sustainability strategy focused on bio-based chemical solutions. This expansion also facilitates closer proximity to key markets, reducing logistics costs and carbon footprint. Source: Sappi Limited Corporate Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 4.5 Billion |

| CAGR | 9.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.1% |

| Scope of Report | Market is segmented by Product Type (Calcium Lignosulfonate, Sodium Lignosulfonate, Magnesium Lignosulfonate, Ammonium Lignosulfonate, Others), Application (Concrete Admixtures, Animal Feed, Dust Control, Oil Drilling, Others), End-Use Industry (Construction, Agriculture, Oil & Gas, Animal Nutrition), Distribution Channel (Direct Sales, Distributors, Online Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Borregaard ASA (Norway), Domsjö Fabriker AB (Sweden), Tembec Inc. (Canada), West Fraser Timber Co. Ltd. (Canada), Sappi Limited (South Africa), UPM-Kymmene Corporation (Finland), Kraft Lignin Ltd. (Canada), LignoTech USA LLC (United States), Hansol PNS Co., Ltd. (South Korea), Norbord Inc. (Canada), Jiangsu Xinda Lignin Co., Ltd. (China), Metsä Group (Finland), GreenValue S.A. (Poland), GranBio (Brazil), Shandong Longlive Bio-Technology Co., Ltd. (China), Westinghouse Electric Company LLC (United States), Aditya Birla Group (India), Tianjin Bohui Paper Co., Ltd. (China), UPM Biochemicals (Finland), Resolute Forest Products (Canada), International Paper Company (United States), Suzano Papel e Celulose S.A. (Brazil), Domtar Corporation (United States), Södra Cell (Sweden), Fibria Celulose S.A. (Brazil) |

Global Lignosulfonate Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.