Global Beer Glass Market - Outlook 2020-2034

Global Beer Glass Market is segmented by Product Type (Pilsner Glass, Mug Glass, Tulip Glass, Snifter Glass, Stein Glass), Application (Home Consumption, Bars & Pubs, Restaurants, Breweries, Events & Festivals), End-Use Industry (Hospitality, Retail, Brewery Industry, Event Management), Distribution Channel (Offline Retail, Online Retail, Direct Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

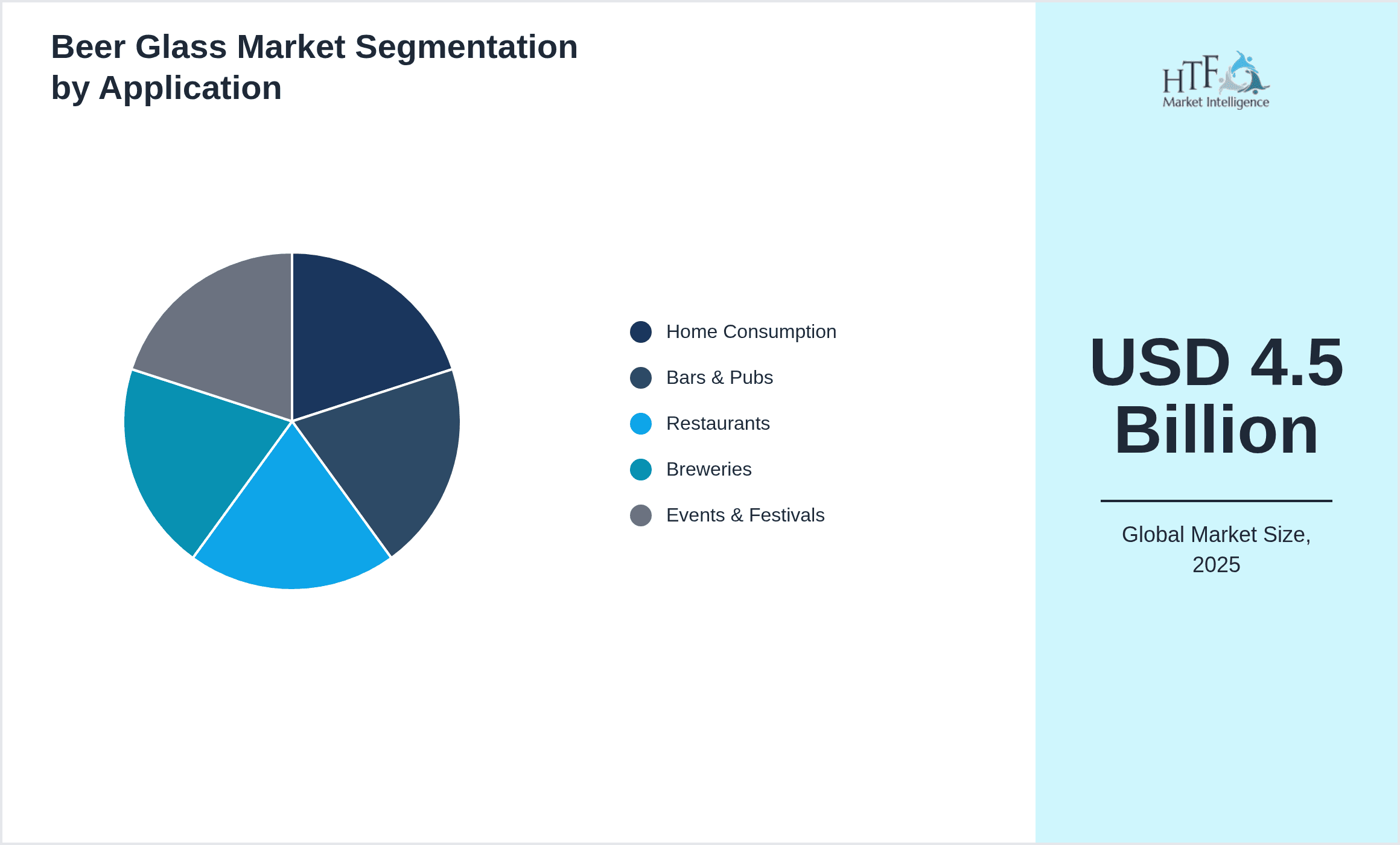

- •The Global Beer Glass Market comprises diverse product types designed to enhance beer consumption experiences worldwide. This market involves a range of glassware styles including pilsner, mug, tulip, snifter, and stein glasses, catering to various consumer preferences and beer types. Applications span from individual home use to commercial settings such as bars, pubs, restaurants, breweries, and large-scale events, reflecting the broad scope and versatility of the market. The value chain integrates raw material sourcing, manufacturing, distribution, and end-user consumption, highlighting the collaborative ecosystem involved. Increasing demand for craft and specialty beers, coupled with rising consumer awareness about the influence of glassware on beer flavor and aroma, propels market growth. Additionally, growth in hospitality and entertainment sectors globally supports expanding sales channels. Technological innovations in glass manufacturing, including durability enhancements and aesthetic customizations, further contribute to market dynamics. Overall, this market represents an essential segment of the global beverage accessories industry, driven by evolving consumer lifestyle trends and expanding beer consumption worldwide.

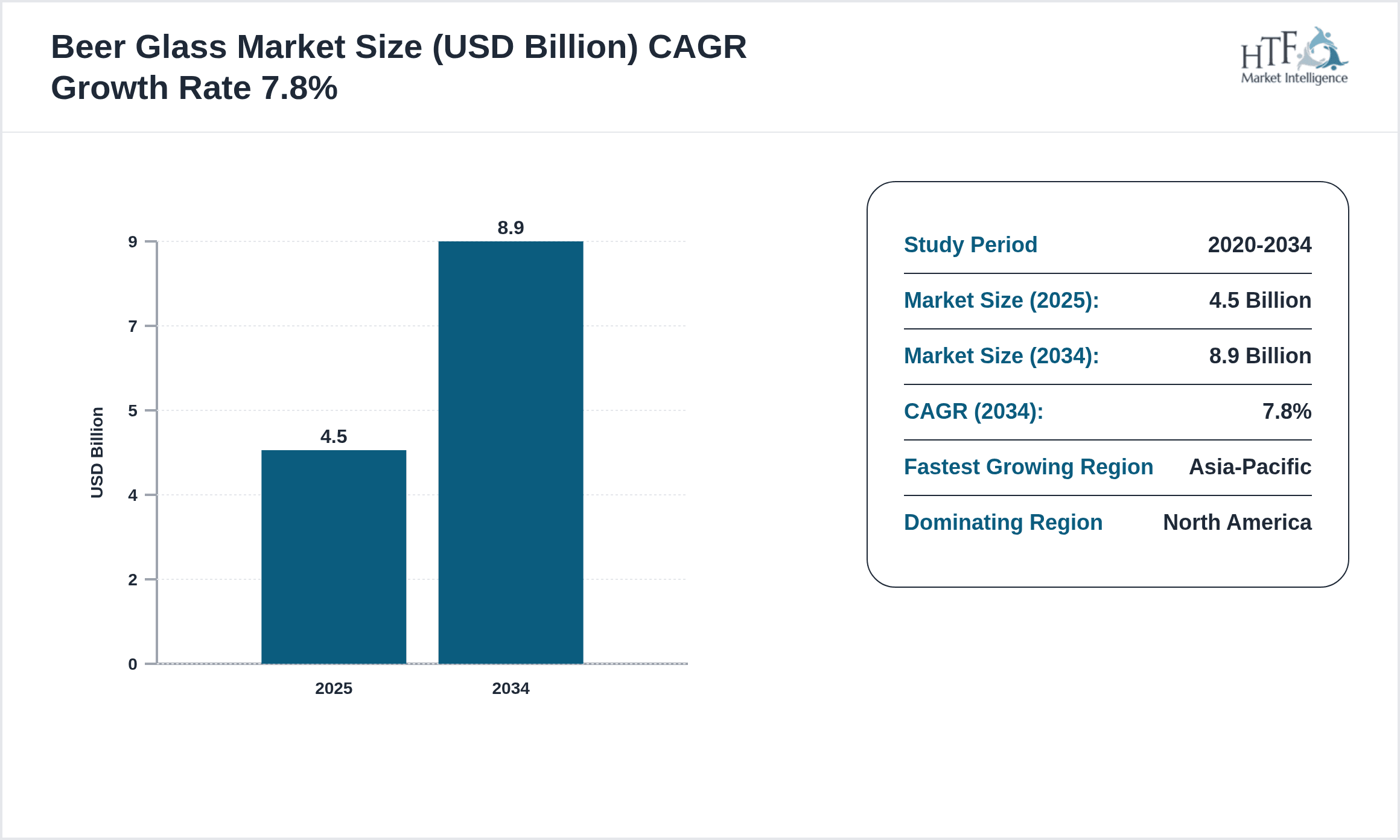

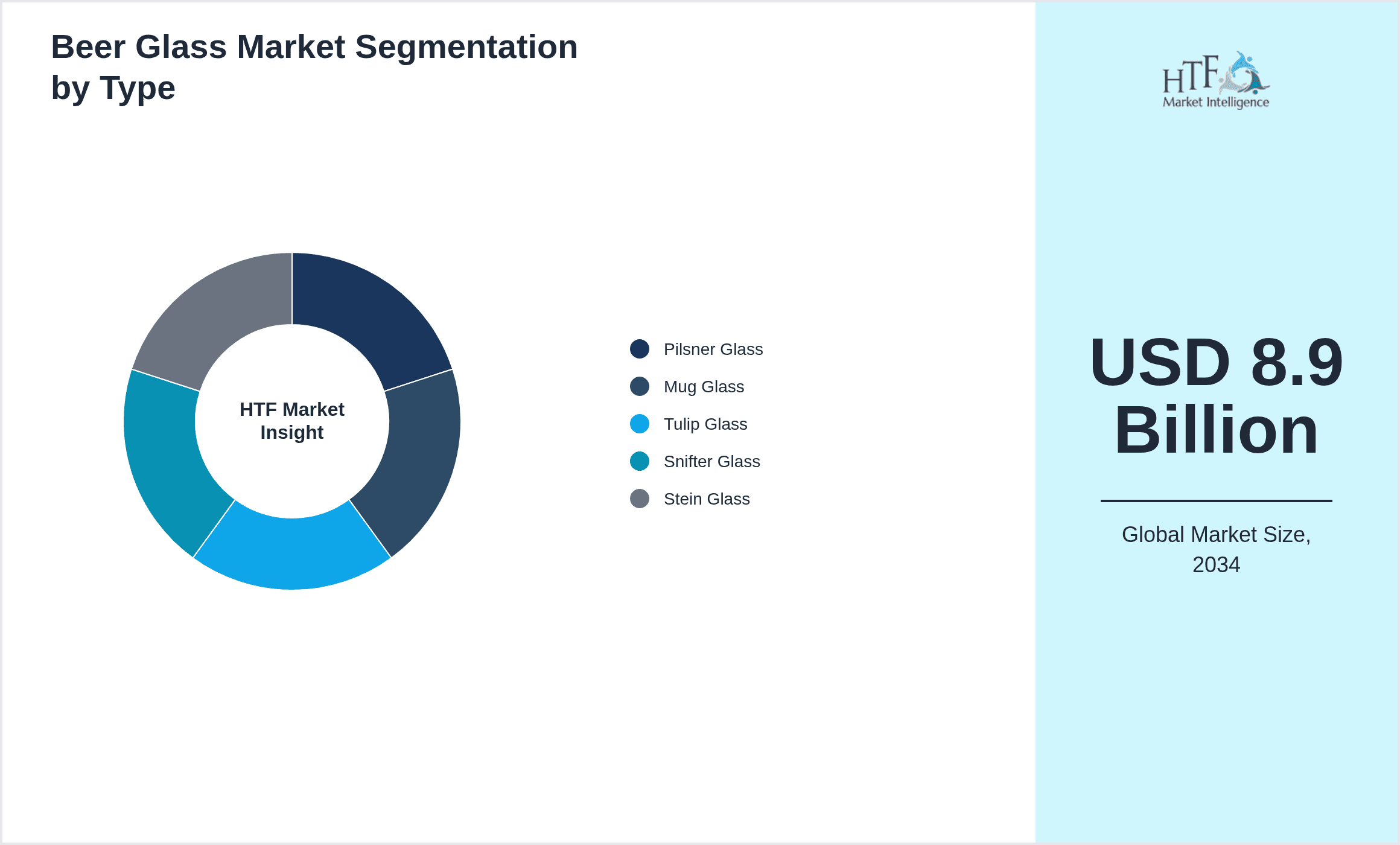

- •Key market highlights include a base market size of USD 4.5 Billion in 2025, forecasted to reach USD 8.9 Billion by 2034, representing a CAGR of 7.8%. The market witnessed steady growth from a historical size of USD 3.1 Billion in 2020, driven by increasing demand in Asia-Pacific and North America. The pilsner glass segment leads in market share, while the tulip glass category is the fastest growing, reflecting changing consumer tastes towards premium and craft beer experiences. North America dominates the market due to mature hospitality infrastructure and high consumer disposable income, whereas Asia-Pacific offers rapid expansion opportunities fueled by growing beer consumption and urbanization. Year-on-year growth averages 7.6%, indicating robust and consistent market momentum across global regions.

- •The beer glass market holds strategic importance for manufacturers, distributors, hospitality businesses, and beverage companies. It enhances the overall beer drinking experience, influencing consumer satisfaction and brand loyalty. For stakeholders, investing in innovative design, sustainable materials, and region-specific product customization presents significant value propositions. The market's alignment with the rising craft beer culture and premiumization trends creates opportunities for differentiation and growth. Additionally, the expanding global beer market and evolving consumer preferences toward specialty glassware underscore the critical role of this segment in the broader alcoholic beverages industry. Stakeholders benefit from understanding regional consumption patterns, technology advancements, and regulatory frameworks to optimize market positioning and capitalize on emerging trends.

Competitive Landscape

The Global Beer Glass Market exhibits a competitive environment characterized by the presence of diversified manufacturers ranging from large multinational corporations to specialized regional producers. Market dynamics are shaped by continuous product innovation, strategic partnerships, and regional customization to meet varying consumer preferences. Companies are investing in advanced glassmaking technologies to improve durability, aesthetic appeal, and functional design such as ergonomic grips and aroma-enhancing contours. Competitive strategies include expanding distribution networks, leveraging e-commerce platforms, and entering emerging markets to capture growing demand, particularly in Asia-Pacific and Latin America. Pricing strategies balance premium product offerings with cost-effective solutions to appeal to both upscale and mass-market consumers. Market consolidation through mergers and acquisitions is limited but remains a potential growth lever to enhance product portfolios and geographic reach. Regulatory compliance related to food safety and sustainability standards also influences competitive positioning. Future trends suggest increased focus on sustainability, smart glassware integration, and customization services to maintain competitive advantages and cater to evolving market needs.

Prominent Players in Beer Glass Market

- •Libbey Inc. (United States)

- •Arc International (France)

- •Rastal GmbH & Co. KG (Germany)

- •Dartington Crystal (United Kingdom)

- •Bormioli Rocco S.p.A. (Italy)

- •Spiegelau (Germany)

- •O-I Glass, Inc. (United States)

- •Zwiesel Kristallglas AG (Germany)

- •Blenko Glass Company (United States)

- •Pasabahce Glass Group (Turkey)

- •Nachtmann (Germany)

- •Luminarc (France)

- •Krosno Glass S.A. (Poland)

- •Schott Zwiesel (Germany)

- •Libbey Glass Inc. (United States)

- •Baccarat (France)

- •Godinger Silver Art Co. Inc. (United States)

- •Arcopal (France)

- •Durobor (Belgium)

- •Anchor Hocking (United States)

- •Reidel (Austria)

- •Waterford Crystal (Ireland)

- •Simon Pearce (United States)

- •Toyo-Sasaki Glass Co., Ltd. (Japan)

- •Marquis by Waterford (United States)

Market Breakdown

- •By Product Type

- ◦Pilsner Glass

- ◦Mug Glass

- ◦Tulip Glass

- ◦Snifter Glass

- ◦Stein Glass

- •By Application

- ◦Home Consumption

- ◦Bars & Pubs

- ◦Restaurants

- ◦Breweries

- ◦Events & Festivals

- •By End-Use Industry

- ◦Hospitality

- ◦Retail

- ◦Brewery Industry

- ◦Event Management

- •By Distribution Channel

- ◦Offline Retail

- ◦Online Retail

- ◦Direct Sales

Growth Dynamics

- •Increasing global consumption of craft and specialty beers has significantly driven demand for diverse beer glass types tailored to specific beer varieties, enhancing consumer sensory experience and satisfaction.

- •Technological advancements in glass manufacturing, including improved durability and innovative designs, have enabled manufacturers to offer premium and customized products, boosting market growth and consumer appeal.

- •Expansion of the hospitality and entertainment sectors worldwide, especially in emerging economies, has increased demand for quality beer glassware in bars, pubs, restaurants, and event venues.

- •Rising consumer preference for home-based leisure activities and at-home beer consumption, accelerated by global lifestyle changes, supports steady growth in retail and online sales channels for beer glass products.

- •Sustainability trends have encouraged manufacturers to adopt eco-friendly materials and production processes, appealing to environmentally conscious consumers and expanding market opportunities.

Market Trends

- •The premiumization trend is influencing consumers to seek high-quality, aesthetically pleasing beer glasses that enhance tasting experiences, leading to innovation in design and material use.

- •Growth in e-commerce and online retail platforms has transformed distribution channels, providing consumers worldwide with convenient access to a wider selection of beer glass products.

- •Customization and personalization services are emerging as key trends, with consumers favoring bespoke glassware featuring logos, unique shapes, or engravings for personal or promotional use.

- •Sustainability and eco-friendly packaging are gaining traction, with manufacturers reducing plastic use and promoting recyclable or biodegradable materials in product packaging.

- •Collaborations between glass manufacturers and breweries are becoming common to co-create specialized glassware that complements specific beer types and branding strategies.

Market Opportunities

- •Emerging markets in Asia-Pacific and Latin America present significant growth potential due to increasing beer consumption and rising disposable incomes, creating demand for premium beer glassware.

- •Integration of smart technology into beer glass designs, such as temperature-sensitive materials and interactive branding, offers innovative avenues for product differentiation and consumer engagement.

- •Expansion of online sales channels enables manufacturers to reach a broader customer base globally, reducing reliance on traditional retail and enhancing market penetration.

- •Collaborative product development with craft breweries can unlock niche segments by producing specialty glassware tailored to unique beer varieties, fostering brand loyalty and exclusivity.

- •Sustainability initiatives focusing on recycled glass and eco-friendly manufacturing processes provide opportunities to appeal to environmentally conscious consumers and comply with regulatory requirements.

Market Challenges

- •High production costs associated with premium and customized beer glassware can limit accessibility in price-sensitive markets and restrict volume sales.

- •Fragmented market landscape with numerous small and regional players creates intense competition, impacting pricing strategies and profit margins for manufacturers.

- •Supply chain disruptions, including raw material shortages and logistics challenges, can adversely affect manufacturing timelines and product availability.

- •Regulatory compliance related to food safety, material standards, and environmental laws requires continuous adaptation, increasing operational complexity and costs.

- •Shifting consumer preferences and the emergence of alternative beverage containers such as cans and bottles may reduce demand for traditional glassware in certain segments.

Regulatory Framework

- •The Food Contact Materials Regulation (EC) No 1935/2004, enforced in Europe between 2020 and 2025, mandates that all beer glassware complies with safety standards ensuring no harmful substances migrate into beverages, impacting manufacturing processes and material selection.

- •The U.S. Food and Drug Administration (FDA) regulations updated in 2023 require stringent testing and certification for glassware materials used in food and beverage applications, influencing product design and quality control.

- •Environmental regulations focusing on recycling and waste reduction, such as the EU Packaging and Packaging Waste Directive amended in 2021, compel manufacturers to adopt sustainable materials and packaging to reduce environmental impact.

- •China’s Mandatory National Standard GB 4806.1-2016 for food contact materials, applied from 2020 to 2025, enforces strict safety criteria on glass products, affecting manufacturers targeting this key market.

- •Various regional regulations concerning energy efficiency and emissions during manufacturing processes, such as North American environmental standards enacted in 2022, require companies to optimize production to reduce their carbon footprint.

Market Intelligence

- •15th January 2025, Libbey Inc. launched an innovative line of eco-friendly beer glasses crafted from 100% recycled glass, targeting environmentally conscious consumers in North America and Europe. The product features enhanced durability and a unique design that improves aroma retention, positioning Libbey as a leader in sustainable glassware solutions. This launch aligns with increasing demand for green packaging and supports Libbey’s strategic objectives to expand its premium product portfolio and reduce environmental impact. Source: Libbey Inc. Official Press Release.

- •3rd March 2025, Arc International announced the introduction of smart beer glasses equipped with temperature-sensitive technology that changes color to indicate optimal drinking temperature. Targeted at the hospitality industry and craft beer enthusiasts, this innovation aims to enhance consumer engagement and differentiation in a competitive market. Arc International plans to roll out these products across Europe and Asia-Pacific by mid-2025, reinforcing its commitment to technological advancement in glassware. Source: Arc International Corporate News.

- •20th June 2025, Rastal GmbH & Co. KG announced a strategic partnership with leading craft breweries across Europe to co-develop bespoke beer glassware tailored to specific beer styles. This collaboration focuses on enhancing brand visibility and consumer experience through customized design and premium materials. The initiative is expected to boost Rastal’s market share in the premium segment and foster deeper industry relationships. Source: Rastal GmbH & Co. KG Press Release.

- •30th August 2024, Bormioli Rocco S.p.A. completed the acquisition of a boutique glassware manufacturer specializing in artisanal beer glasses, expanding its product range to include handcrafted and limited-edition items. This move strengthens Bormioli’s presence in the luxury segment and supports its strategy to diversify offerings globally. The acquisition is projected to enhance cross-market synergies and accelerate growth in emerging regions. Source: Bormioli Rocco S.p.A. Official Announcement.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.5 Billion |

| Forecast Year Market Size | USD 8.9 Billion |

| CAGR | 7.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.6% |

| Scope of Report | Market is segmented by Product Type (Pilsner Glass, Mug Glass, Tulip Glass, Snifter Glass, Stein Glass), Application (Home Consumption, Bars & Pubs, Restaurants, Breweries, Events & Festivals), End-Use Industry (Hospitality, Retail, Brewery Industry, Event Management), Distribution Channel (Offline Retail, Online Retail, Direct Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Libbey Inc. (United States), Arc International (France), Rastal GmbH & Co. KG (Germany), Dartington Crystal (United Kingdom), Bormioli Rocco S.p.A. (Italy), Spiegelau (Germany), O-I Glass, Inc. (United States), Zwiesel Kristallglas AG (Germany), Blenko Glass Company (United States), Pasabahce Glass Group (Turkey), Nachtmann (Germany), Luminarc (France), Krosno Glass S.A. (Poland), Schott Zwiesel (Germany), Libbey Glass Inc. (United States), Baccarat (France), Godinger Silver Art Co. Inc. (United States), Arcopal (France), Durobor (Belgium), Anchor Hocking (United States), Reidel (Austria), Waterford Crystal (Ireland), Simon Pearce (United States), Toyo-Sasaki Glass Co., Ltd. (Japan), Marquis by Waterford (United States) |

Global Beer Glass Market - Outlook 2020-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.